California Cannabis Market Analysis: The Golden State's Tarnished Dream and the Path Forward

How federal reform could unlock California's struggling $5 billion legal market

The Silent Majority 420 | November 2025

This analysis uses the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error. View validation data on Harvard Dataverse.

California's Cannabis Paradox

California presents the most striking paradox in the American cannabis experiment: the world's largest legal cannabis market—larger than most small nations' GDP—yet one where the illicit market still dominates by a margin of 2:1 or even 3:1, seven years after adult-use legalization.

Current market reality:

- Legal market size: $5.1–5.4 billion annually (2024-2025)

- Illicit market size: $10–16 billion annually (estimated)

- Legal market share: 38–40% of total consumption

- Licensed production: 1.4 million pounds (2024)

- Illicit production: 7–16.3 million pounds (estimated)

- Dispensary count: ~1,580 active licenses statewide

- Licensed producers: Declining (18% drop in active licenses 2023-2024)

The question isn't whether California's legal market is failing—by many measures, it demonstrably is. The question is: What went wrong in the state that pioneered medical cannabis in 1996, and can federal reforms finally unlock the market's potential?

The answer lies in understanding how a perfect storm of policy failures—punitive federal tax code (280E), banking restrictions, crushing state and local taxes, minimal enforcement against illicit operators, and thousands of local bans—created an environment where it's more profitable to stay illegal than go legal.

The Crisis in Numbers: California's Declining Legal Market

Sales Plummeting Despite Growing Demand

California's legal cannabis market posted its largest sales drop in legalization history in Q1 2025: taxable sales fell 11% year-over-year to $1.088 billion, the lowest quarterly figure in five years. This isn't a one-time anomaly—it's part of a multi-year trend:

- 2021: $5.4 billion legal sales

- 2022: $5.39 billion

- 2023: $5.18 billion

- 2024: ~$5.1 billion (estimated)

- Q1 2025: On pace for <$4.5 billion annualized

Meanwhile, total cannabis consumption in California continues to grow. The disconnect? The illicit market captured virtually all the growth. The Department of Cannabis Control's own commissioned report acknowledges that licensed cannabis supplied only 38% of total consumption in 2024—meaning 62% of California cannabis users still buy from unlicensed sources.

Price Collapse Without Profitability

Wholesale prices have collapsed 57% from their 2020 peak, with outdoor-grown cannabis down 74%. Yet this price compression hasn't translated to profitability or market share gains:

- Outdoor cannabis: Down 74% (wholesale)

- Indoor cannabis: Down 46% (wholesale)

- Mixed-light: Down 60% (wholesale)

- Retail (half ounce): Down 37% ($74.34 → $46.84)

Falling prices typically indicate market maturation and competitive efficiency. In California, they indicate collapse: businesses can't cover costs even with drastically reduced prices, and consumers still find illicit options cheaper and more convenient.

The profitability crisis is real: Only 27% of California cannabis operators were profitable in 2024, while 32% operated at a loss. This isn't sustainable—it's a slow-motion extinction event for legal operators.

The Five Structural Failures Killing California's Legal Market

Failure #1: Federal Tax Code Section 280E—The Invisible Tax Chokehold

Section 280E prevents cannabis businesses from deducting ordinary business expenses on federal tax returns. Because cannabis remains a Schedule I controlled substance, dispensaries cannot deduct:

- Employee salaries and wages

- Rent and utilities

- Marketing and advertising

- Insurance premiums

- Legal and accounting fees

- Delivery vehicle costs

- Security expenses

They can only deduct Cost of Goods Sold (COGS).

The result? An effective federal tax rate of 40–70% on cannabis businesses—while competing illicit operators pay zero taxes. 280E adds 15–20% to retail prices beyond what competitive market economics would dictate. In a price-sensitive market where consumers have easy access to untaxed alternatives, this gap is insurmountable.

The California impact:

A licensed California dispensary selling $2 million annually might have:

- Gross revenue: $2,000,000

- Cost of goods sold: $800,000

- Operating expenses: $900,000 (salaries, rent, utilities, etc.)

- Actual profit: $300,000

Without 280E:

- Taxable income: $300,000

- Federal tax (21%): $63,000

With 280E (current reality):

- Taxable income: $1,200,000 (can't deduct operating expenses)

- Federal tax (21%): $252,000

- Excess tax burden: $189,000 (63% of actual profit)

This isn't marginal—it's existential. Licensed operators are taxed on revenue they don't actually earn, forcing prices 15–20% higher to cover the burden. Meanwhile, illicit dealers face zero federal tax and undercut legal prices by 30–50%.

Between 2020 and 2030, the U.S. cannabis industry will pay an estimated $65.3 billion in excess taxes due to 280E, according to MJBizDaily. If 280E were eliminated, that figure drops to $35 billion—a $30 billion savings that would flow directly into lower consumer prices and industry sustainability.

Federal rescheduling would eliminate 280E overnight. The DEA's proposed reclassification of cannabis to Schedule III (recommended by HHS in 2023) would make 280E inapplicable, allowing cannabis businesses to deduct expenses like any other legal industry. While the DEA's administrative hearing process has been delayed, the direction is clear: 280E's days are numbered.

Failure #2: Banking Restrictions—Cash Is Dangerous, Expensive, and Inefficient

Cannabis businesses cannot access traditional banking services because banks fear federal prosecution for money laundering (the Bank Secrecy Act treats cannabis proceeds as "proceeds from unlawful activity"). The result:

Cash-heavy operations create:

- Security risks: Dispensaries are high-value robbery targets. Armed guards, reinforced safes, armored car transport—all add 5–10% to operating costs.

- Consumer friction: No credit/debit cards means customers must use ATMs (fees: $3–5 per transaction), reducing convenience and impulse purchases.

- Tax compliance challenges: The IRS is inherently suspicious of cash businesses, increasing audit risk.

- Business growth barriers: No access to commercial loans, lines of credit, or traditional financing. Expansion requires cash reserves or expensive private equity.

- Payroll complexity: Some operators literally pay employees in cash, creating HR and tax nightmares.

California dispensaries pay 3–5× higher banking fees than comparable retail businesses (when they can find banking at all), and many face sudden account closures when banks decide cannabis risk outweighs profit.

The SAFER Banking Act (Senate version of SAFE Banking Act) would solve this by creating a federal safe harbor for financial institutions serving state-legal cannabis businesses. The bill passed the Senate Banking Committee in September 2023 with bipartisan support (14–9 vote) but remains stalled awaiting a Senate floor vote.

If SAFER passes:

- Card payment acceptance becomes standard (convenience drives 3–5 percentage point increase in legal market share)

- Banking fees normalize (5–10% cost reduction)

- Access to commercial credit (enables expansion, modernization, competitive pricing)

- Reduced cash-handling security costs (3–5% savings)

- Insurance access improves (premiums decline 10–20%)

Combined with 280E repeal, SAFER would reduce legal cannabis prices by 20–30%—closing the price gap with illicit market competitors.

Failure #3: State and Local Tax Burden—Pricing Out Consumers

California imposes a 15% cannabis excise tax, plus standard state (7.25%) and local sales taxes. Combined burden: 20–25% in most jurisdictions, among the highest in the nation.

And it's about to get worse: California law requires the excise tax to increase to 19% on July 1, 2025, to offset lost revenue from the 2022 suspension of the cultivation tax. The California Legislative Analyst's Office projects this increase will reduce licensed market sales by 6%—$300+ million in lost legal sales, captured instead by untaxed illicit dealers.

Why this matters:

Every 5% tax increase reduces legal market share by 2–3 percentage points. At 20–25% total tax burden, California is well beyond the threshold where legal cannabis can compete on price with untaxed alternatives.

Tax burden comparison:

- Oregon: ~17% total (strong legal market, 75–85% legal share)

- Colorado: ~15% total (mature market, 84–92% legal share)

- Washington: ~37% total initially (struggled with illicit competition until reduced to ~30%)

- California: 20–25% total (→ 24–29% after July 2025 increase)

Research shows the optimal tax burden for maximizing both legal market share and tax revenue is 12–18% total. California is above this range, and moving in the wrong direction.

Local tax variations create additional complexity: Some jurisdictions add local cannabis taxes (business license fees, per-square-foot cultivation taxes, gross receipts taxes), pushing total burden to 30%+ in places like Los Angeles. This incentivizes diversion: legal cultivation in low-tax areas, illicit sales in high-tax areas.

Failure #4: Inadequate Enforcement—The Illicit Market Operates with Impunity

California's enforcement against the illicit market is functionally nonexistent relative to the problem's scale. The Department of Cannabis Control (DCC) served 92 search warrants in Q3 2024—their highest three-month total in years.

Think about that: In a state with an estimated 7–16.3 million pounds of illicit production annually, serving one warrant per day is rounding error enforcement. For context, illicit cannabis in California generates $10–16 billion in untaxed annual revenue. The state seized $200 million in illegal cannabis in 2024—impressive headline, but only 1.25–2% of the illicit market.

Why enforcement is so minimal:

- Limited resources: DCC enforcement division is understaffed and underfunded relative to the problem scale.

- Political will: California's progressive culture makes aggressive cannabis enforcement politically unpopular, even against illicit operators.

- Interstate complexity: Much California-grown illicit cannabis ships out-of-state (where adult-use remains illegal), complicating jurisdiction.

- Grey-market sophistication: Many illicit operations use fake licensing documentation, QR codes, and professional packaging indistinguishable from legal products.

The result: Illicit operators face negligible risk. Expected value of illegal operation:

- Revenue: $500,000/year (modest illicit grow)

- Risk of enforcement: <2% annually

- Penalty if caught: Civil fine (often negotiated down), asset seizure (partial)

- Expected cost: <$10,000/year

- Net expected profit: $490,000/year

Compare to legal operation:

- Revenue: $500,000/year

- Federal tax (280E): $150,000

- State/local taxes: $100,000

- Compliance costs: $80,000 (testing, licensing, reporting, security)

- Net profit: $170,000/year

The rational economic choice is clear: Stay illicit. Legal operators face 3× the tax burden plus massive compliance costs, while illicit operators face <2% enforcement risk with negotiable penalties.

Failure #5: Local Bans and Limited Retail Access

More than half of California's cities and counties ban commercial cannabis operations. This creates "cannabis deserts" where legal access is nonexistent or requires 30–60+ minute drives, while illicit delivery services operate with impunity.

The access problem:

- California population: ~39 million

- Active dispensaries: ~1,580 (as of late 2024)

- Dispensaries per 100,000 residents: ~4.1

Compare to optimal markets:

- Oregon: 16.8 per 100k (excellent access)

- Colorado: 14.2 per 100k (mature market)

- Oklahoma: 26+ per 100k (medical-only, but demonstrates access importance)

California's density is 1/4 to 1/6 of optimal access levels. Low density + local bans = massive convenience advantage for illicit market.

Geographic disparities are stark:

- Los Angeles County: Good retail density in permissive areas, but county size means many residents face long drives

- Alameda County: Retail count dropped from 157 (2022) to 100 (2024)—licensed retailers are leaving the market

- San Bernardino County: Minimal retail access for 2.2 million residents

- Kern County, Fresno County, others: Effectively zero legal retail despite large populations

When legal retail is inconvenient, illicit delivery fills the gap. Unlicensed delivery services operate openly on social media, offering broader product selection and lower prices than licensed competitors—with minimal enforcement risk.

What Federal Reform Would Change: The 280E and SAFER Impact

Schedule III Rescheduling: The $2+ Billion Annual Impact

The DEA's proposed reclassification of cannabis from Schedule I to Schedule III (following HHS's August 2023 recommendation) would eliminate 280E automatically. Cannabis would no longer be subject to the "trafficking in controlled substances" prohibition.

California-specific impact:

Current legal market: $5.1 billion (2024)

- 280E excess tax burden: ~$765 million (15% of revenue, conservative estimate)

- Passed through to consumers in higher prices: 15–20% price premium

Post-rescheduling (Schedule III):

- 280E burden eliminated: $765 million freed up

- Price reduction: 15–20% drop in retail prices

- Competitive gap closes: Legal prices approach illicit parity

- Market share gain: 10–15 percentage point increase (38% → 48–53%)

- New legal market size: $6.8–8.0 billion (volume growth + higher legal share)

- Net state tax revenue: $1.02–1.2 billion (lower rate × larger base = similar or higher revenue)

Why this works:

Price elasticity in cannabis markets is high. A 15–20% legal price reduction (from eliminating 280E burden) doesn't just retain current legal consumers—it converts price-sensitive illicit consumers who were buying unlicensed products due to cost, not preference.

Research across multiple states shows that every 10% price reduction in legal cannabis increases legal market share by 4–6 percentage points. Eliminating 280E's 15–20% burden would be the single most impactful policy change for California's legal market.

SAFER Banking: The Convenience Revolution

The SAFER Banking Act would normalize banking access for state-legal cannabis businesses, eliminating federal prosecution risk for financial institutions serving the industry.

California impact:

Direct effects:

- Card payments accepted: 70–80% of consumers prefer cards to cash. Removing cash-only friction increases impulse purchases and basket size.

- Banking fees normalize: From 3–5× normal rates to standard commercial banking fees. Saves 5–10% of operating costs.

- Commercial credit access: Dispensaries can get business loans, lines of credit for expansion, equipment financing. Enables competition, modernization, lower prices.

- Security costs decline: Less cash handling = reduced armored car transport, vault requirements, guard expenses. Saves 3–5% of costs.

Indirect effects:

- Professionalization: Better accounting systems, cleaner books, improved tax compliance.

- Investor confidence: Institutional capital enters the market, funding consolidation and efficiency gains.

- Insurance access: Property and liability insurance becomes available at reasonable rates (10–20% premium reduction).

Combined 280E + SAFER impact: 20–30% reduction in legal cannabis prices, driving legal market share from 38% → 55–65% within 2–3 years. This would add $2.5–4 billion to California's legal market annually while crippling illicit competition through price parity.

California's Additional Self-Inflicted Wounds

Federal reform is necessary but insufficient. California must also address state-level policy failures:

The July 2025 Tax Increase: Gasoline on the Fire

Raising the excise tax from 15% to 19% when the legal market is already losing ground to illicit competition is economic malpractice. The Legislative Analyst's Office projects 6% sales decline ($300+ million), but this likely underestimates black market recapture.

Alternative approach:

- Reduce state excise tax to 10–12% (revenue-neutral when legal market share increases)

- Offset with enhanced enforcement against illicit operators (funded by cannabis tax revenue)

- Achieve higher total revenue through volume growth, not rate increases

The Retail Access Problem: Local Bans and Market Deserts

More than half of California municipalities ban cannabis retail. This is anti-competitive policy failure:

Solutions:

- State preemption: Override local bans for retail (not cultivation/manufacturing, which affect local land use)

- Delivery-only licenses: Low-cost license category for delivery services serving retail deserts

- County-level licensing: Allow counties to authorize retail in unincorporated areas where cities ban operations

The Enforcement Gap: Targeted Strategies vs. Symbolic Gestures

California needs smart enforcement, not more enforcement:

High-value targets:

- Interstate trafficking networks: California-grown illicit cannabis shipped to non-legal states generates billions in untaxed revenue

- Fake-license operations: Grey-market operators using counterfeit QR codes and packaging

- Unlicensed delivery platforms: Social media-based delivery services operating openly

Low-value targets:

- Small personal grows: Waste of enforcement resources

- Legacy operators: Many have customer loyalty, aren't converting to legal despite penalties

Effective strategy: Target 200–300 highest-volume illicit operations annually (not 92 random warrants). Prioritize interstate trafficking and grey-market counterfeiting. Publicize enforcement actions to create deterrent effect.

The Path Forward: What California Needs

Near-Term (2025–2026): State-Level Reforms

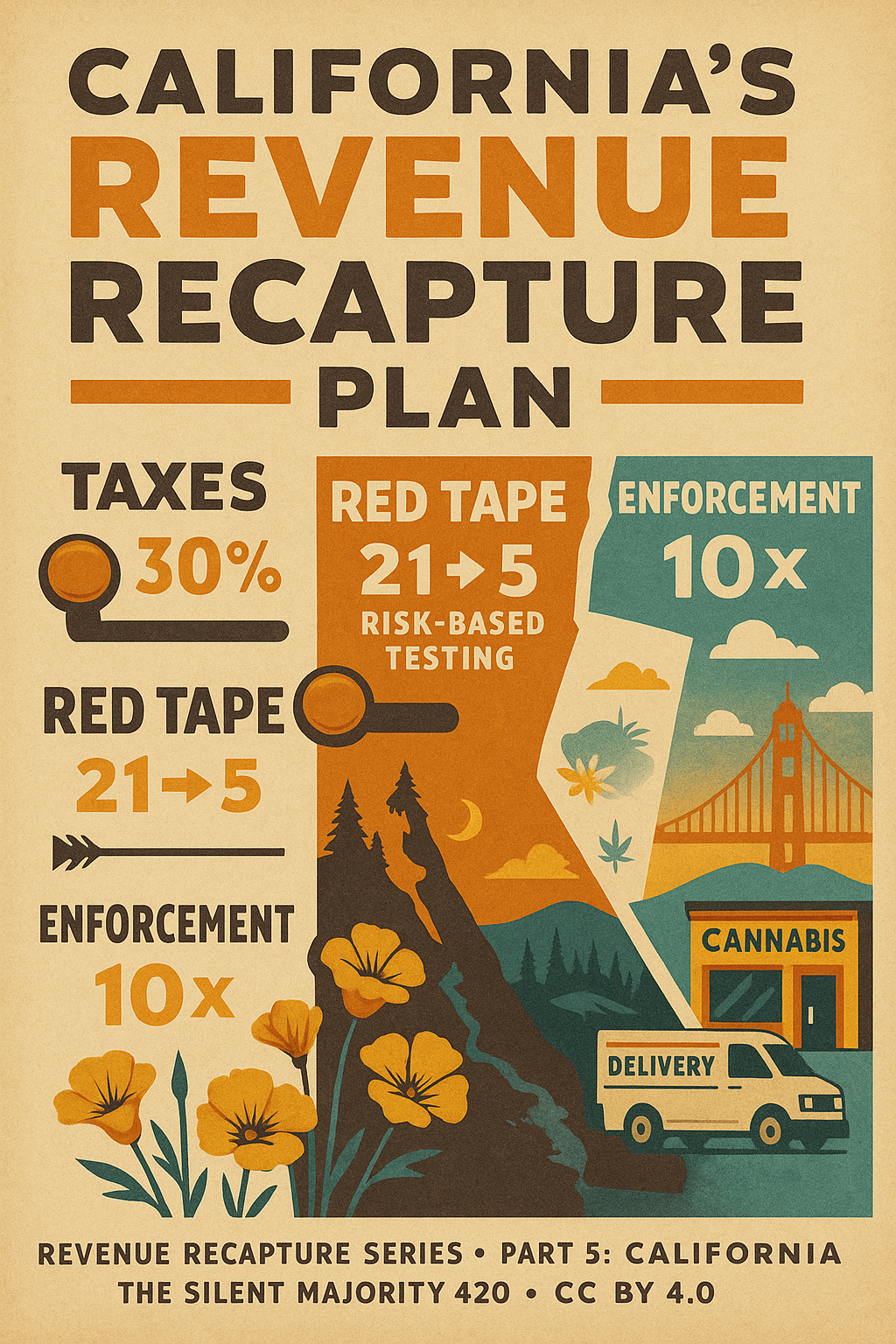

- Block the July 2025 tax increase. Assemblymember Matt Haney proposed legislation to prevent the 15% → 19% excise tax hike. This should pass—it's basic economic rationality.

- Reduce long-term tax burden. Phase down excise tax to 10–12% over 3 years. Offset with enforcement-driven legal market growth (revenue-neutral or revenue-positive).

- Expand retail access. Authorize state preemption of local retail bans in retail deserts. Create delivery-only license category for underserved areas.

- Smart enforcement. Triple enforcement budget, target 200–300 highest-volume illicit operations annually, focus on interstate trafficking and counterfeit operations.

Mid-Term (2026–2027): Federal Reform Advocacy

California's Congressional delegation should aggressively push federal cannabis reform:

- SAFER Banking Act: Demand Senate floor vote. California senators (Padilla, Butler) should co-sponsor and lobby leadership.

- Schedule III rescheduling: Support DEA's proposed reclassification, submit public comments, participate in administrative hearings.

- Interstate commerce: Once federal barriers fall, California should advocate for interstate sales (exports to non-producing states = massive revenue opportunity).

Long-Term (2027–2030): Market Optimization

With federal reforms in place and state policy optimized:

California could achieve:

- Legal market share: 60–70% (up from 38%)

- Legal market size: $8–10 billion annually

- State tax revenue: $1.0–1.5 billion annually (at optimized 12–15% rate)

- Jobs: 60,000–80,000 direct cannabis employment

- Economic impact: $12–15 billion including multiplier effects

This requires:

- 280E elimination

- SAFER Banking passage

- State tax reduction to 12–15% total

- Expanded retail access (2,500–3,000 dispensaries statewide)

- Sustained enforcement against illicit market

The Bottom Line: California's Choice

California cannabis legalization has failed by most meaningful metrics:

- Legal market share: 38% (should be 60–75%)

- Illicit market: 2× larger than legal market (should be 1/3 to 1/4)

- Business sustainability: 73% of operators unprofitable or breaking even

- Sales trajectory: Declining despite growing demand

The root causes are identifiable and fixable:

- Federal 280E burden: 15–20% price premium → eliminated by Schedule III rescheduling

- Banking restrictions: Cash-only friction, high costs → eliminated by SAFER Banking Act

- State/local tax burden: 20–25%+ total → reducible to 12–15% through state action

- Inadequate enforcement: <2% illicit operator risk → increasable through focused resources

- Limited retail access: 4.1 per 100k population → expandable through preemption, delivery licenses

Federal reform (280E + SAFER) would:

- Reduce legal cannabis prices 20–30%

- Increase legal market share 15–25 percentage points

- Add $2.5–4 billion to legal market annually

- Improve operator profitability, enabling consolidation and efficiency

State reforms (tax reduction, access expansion, smart enforcement) would:

- Further reduce prices 5–10%

- Increase legal market share another 5–10 percentage points

- Generate higher total tax revenue through volume growth

Combined impact: California's legal cannabis market could reach $8–10 billion annually by 2028–2030, with 60–70% legal market share, generating $1.0–1.5 billion in state tax revenue while creating 60,000+ jobs and crippling the illicit market through competitive pricing and enforcement.

The alternative—status quo—leads to continued market contraction, business closures, declining tax revenue, and an entrenched illicit market that grows stronger while the legal market withers.

California voters legalized cannabis in 2016 expecting a well-regulated, taxed, and safe market. Seven years later, they got a failed experiment. Federal reform offers a path to redemption—but only if California acts simultaneously to fix its self-inflicted wounds.

The question is whether political leaders will seize this opportunity or continue doubling down on policies that demonstrably don't work.

About This Analysis

This analysis is based on the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error (r = 0.968 correlation). The framework models legal market share as a function of price competitiveness, retail access, regulatory environment, enforcement effectiveness, and other key variables.

Key data sources:

- California Department of Cannabis Control (DCC) — California Cannabis Market Outlook 2024 Report (ERA Economics, March 2025)

- California Department of Tax and Fee Administration — Cannabis excise tax data (Q1 2025)

- NPR — Illegal Cannabis Outcompetes Legal Weed (February 5, 2025)

- MJ Biz Daily — California Cannabis Production Grows But Illicit Market Thrives (March 4, 2025)

- Cannabis Business Times — 60% of Cannabis Consumed in California Comes From Unregulated Market (March 2025)

- Whitney Economics — Cannabis industry profitability data (2024)

- National Cannabis Industry Association — 280E reform advocacy, SAFER Banking status

- Congressional Research Service — SAFE Banking Act, SAFER Banking Act summaries

- DEA/HHS — Cannabis rescheduling proposed rule (May 2024)

- Harvard Dataverse — CBDT Framework Validation Data (DOI: 10.7910/DVN/MDVDTQ)

Related analysis:

- The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

- Arkansas Cannabis Market Analysis: Medical Success, Adult-Use Potential, and the Bible Belt Challenge

For Policymakers, MSOs, and Stakeholders

Interested in detailed California-specific analysis including:

- Exact legal market share projections under multiple policy scenarios

- County-level market opportunity assessments

- Federal reform impact modeling (revenue, employment, tax effects)

- Enforcement strategy optimization

- Competitive intelligence and MSO market entry analysis

Contact:

- Twitter/X: @The_Silent_420

- Email: silentmajority420@proton.me

- Website: silentmajority420.com

The Silent Majority 420 is an anonymous cannabis policy analyst with 25 years of market participation. The CBDT Framework represents the first validated consumer-utility model for predicting legal market outcomes in cannabis legalization. Analysis licensed CC BY 4.0 (free use with attribution).