Connecticut Cannabis Market Analysis: The Constitution State's Pricing Crisis and the Path to 70–75% Legal Market Share

Is weed legal in Connecticut? Yes—but prices 60% above the black market send residents fleeing to Massachusetts, hemorrhaging tens of millions in tax revenue annually.

The Silent Majority 420 | November 2025

The Connecticut Contradiction

Connecticut legalized recreational marijuana in July 2021 with SB 1201, becoming the 19th state to end adult-use prohibition. The state designed one of America's most equity-focused cannabis programs, with 50% of licenses reserved for social equity applicants from disproportionately impacted areas. Yet three years after adult-use sales launched in January 2023, Connecticut's legal market captures only 50–55% of total consumption—comparable to California and New York, two of the nation's most prominent regulatory failures.

The problem is price. Connecticut cannabis possession limits are reasonable (1.5 ounces in public, 5 ounces at home), Connecticut home grow is legal (6 plants per adult since July 2023), and Delta-8 in Connecticut is properly regulated through licensed dispensaries. But legal flower averaging $350 per ounce versus $200 on the black market makes one thing mathematically certain: Connecticut residents will keep driving to Massachusetts or buying from unlicensed sources.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. markets with 5% mean absolute error, identifies price competitiveness as the 4× weighted dominant variable in determining legal market success. Connecticut fails spectacularly on this dimension.

The prediction: If Connecticut reduces total tax burden to 12–15%, expands retail density to 120–140 stores statewide, and federal reforms eliminate 280E, the state could achieve 70–75% legal market share within 36–48 months, generating $75–95 million in annual tax revenue while reducing the illicit market by 40–50%.

Without reform, Connecticut will continue funding Massachusetts schools instead of its own.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight): The dominant variable—legal prices versus illicit alternatives

- Access density: Store availability and delivery infrastructure

- Safety and quality: Testing standards and brand consistency

- Convenience: Payment methods, operating hours, friction reduction

- Enforcement intensity: Illicit supply interdiction

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation

Current Market Performance: Connecticut Cannabis by the Numbers

Market Fundamentals (2025)

According to Connecticut's official cannabis portal, the state's market metrics include:

- May 2025 sales: $18.7M recreational + $6.6M medical = $25.3M monthly

- FY 2024 tax revenue: $49.4M total ($21.3M cannabis excise, remainder from sales/licensing)

- Retail infrastructure: 72 licensed dispensaries (1.9–2.0 per 100,000 residents)

- Average flower price: $10.86/gram ($302/ounce) as of November 2024

- Recreational sales launch: January 10, 2023

- Licensed delivery services: 3 (limited operations)

Connecticut Cannabis Tax Structure

Connecticut imposes a THC-based excise tax system:

- Plant materials: $0.00625 per mg THC

- Edibles: $0.0275 per mg THC (highest rate)

- Other products: $0.009 per mg THC

- State sales tax: 6.35%

- Municipal tax: 3%

- Total effective burden: ~20%

Revenue distribution (FY 2024-2026): 15% general fund, 60% Social Equity Fund, 25% Prevention and Recovery Services.

What Connecticut Does Well

Rigorous testing standards: Connecticut requires comprehensive product testing through licensed laboratories—pesticides, potency, microbials, heavy metals. This creates legitimate consumer confidence and differentiates legal products from dangerous unregulated alternatives.

Social equity commitment: The Connecticut social equity cannabis program reserves 50% of licenses for applicants from disproportionately impacted areas. Qualification requires 65% ownership, income below 3× state median, and residence in a DIA for 5 of the last 10 years. Social equity applicants receive 50% discount on fees for three renewal cycles.

Home cultivation rights: Connecticut home grow became legal July 1, 2023 for adults 21+. Limits are 6 plants per person (3 mature, 3 immature), 12 plants maximum per household, grown indoors in secured locations. Medical patients could grow starting October 1, 2021.

Statewide authorization: Unlike California where 61% of jurisdictions ban retail, Connecticut permits cannabis sales statewide with no local opt-outs allowed. This prevents the geographic fragmentation that devastates other markets.

Cannabis expungement: Connecticut's Clean Slate program automatically erased approximately 44,000 cannabis convictions as of January 1, 2023. Possession under 4 ounces from 2000–2015 was cleared automatically; other offenses can be petitioned for erasure.

What Limits Optimization

Fatal flaw #1: Price uncompetitiveness

The Department of Consumer Protection's price-per-gram dataset reveals the core problem:

- Legal prices: $350/ounce recreational ($10.86/gram average)

- Illicit prices: Estimated $180–220/ounce ($6–8/gram)

- Price gap: Legal costs 60–95% more than illicit

Research demonstrates cannabis consumers are highly price-sensitive, with a 10% legal price increase reducing legal market choice probability by 2.3%. At 60–95% premium, Connecticut essentially guarantees black market persistence.

Fatal flaw #2: Insufficient retail density

Connecticut's 1.9–2.0 stores per 100,000 residents falls far short of optimization. Colorado achieves 84% legal market share with 8–10 stores per 100,000. Oregon reaches 82% with 16.8 per 100,000. The state issued 94 provisional licenses but struggles to bring them operational.

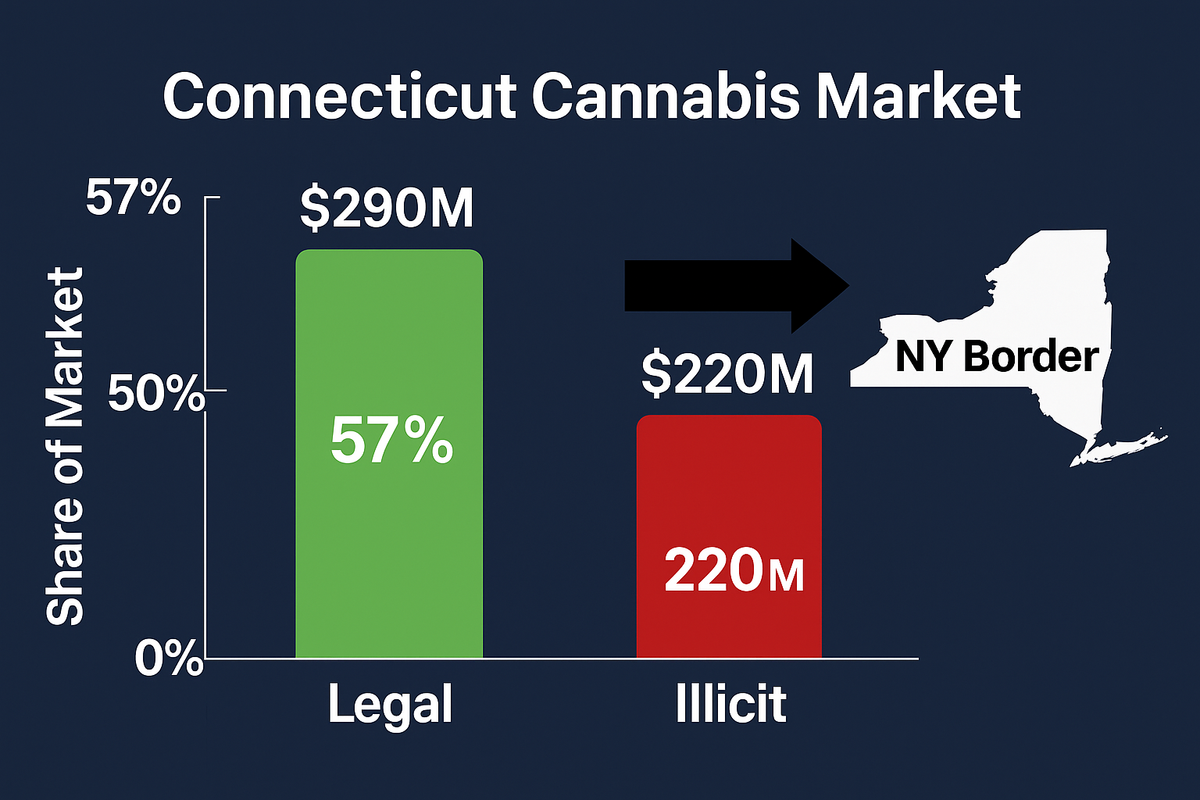

Fatal flaw #3: Border hemorrhaging

Connecticut residents drive to Massachusetts for lower prices ($250–280/ounce versus $350), better selection, and perceived higher quality. This cross-border leakage costs Connecticut an estimated $20–40M in lost tax revenue annually.

Fatal flaw #4: Limited delivery

Only 3 licensed delivery services operate with restricted operations. States with robust delivery infrastructure effectively increase access density 2–3×, serving rural and suburban consumers without requiring store visits.

Connecticut Cannabis Laws: Key Consumer Questions

Is Marijuana Legal in Connecticut?

Yes. Connecticut legalized recreational cannabis July 1, 2021 (SB 1201). Adults 21+ can possess up to 1.5 ounces in public and 5 ounces in a locked container at home or in a vehicle's trunk/glove compartment. Recreational sales began January 10, 2023.

Connecticut Medical Marijuana Card

Connecticut's medical marijuana program (established 2012 under HB 5389) includes 42 qualifying conditions for adults and 11 for minors. Key benefits over recreational:

- Tax-free purchases (no excise tax)

- No potency caps (recreational limits flower to 30% THC, concentrates to 60%)

- Higher possession limits (medical patients can purchase 5 oz per 30 days)

- No state registration fee

Qualifying conditions include chronic pain, PTSD, cancer, Crohn's disease, epilepsy, glaucoma, HIV/AIDS, multiple sclerosis, Parkinson's, and 32 others. Certification requires a licensed physician, physician assistant, or APRN.

Connecticut Marijuana DUI

Driving under the influence of cannabis is illegal in Connecticut, carrying the same penalties as alcohol DUI. Connecticut uses an effects-based approach with no specific THC blood level threshold. Police employ Drug Recognition Experts (54 trained as of 2023) who conduct 12-step evaluations. Penalties include arrest, vehicle towing, license suspension, and criminal charges.

Connecticut Cannabis Employment Drug Testing

Effective July 1, 2022, Connecticut employers cannot refuse to hire or terminate employees solely based on a positive THC test from off-duty cannabis use. However, exemptions apply to:

- Federal contractors and grant recipients

- Reasonable suspicion of workplace impairment

- Random testing policies in safety-sensitive positions

- Firefighters, EMTs, police, corrections, education, construction, utilities, healthcare

Medical marijuana patients receive additional protection under the Palliative Use of Marijuana Act (PUMA). Employers can still prohibit on-site possession and use during work hours.

Delta-8 Legal Connecticut

Delta-8 THC is legal but highly regulated in Connecticut. Under SB 1201 (July 1, 2021), all THC isomers—including delta-7, delta-8, delta-9, and delta-10—with concentrations above 0.3% are classified as cannabis and can only be sold through licensed cannabis establishments. The Attorney General has pursued enforcement actions against unlicensed retailers selling delta-8 products.

Connecticut Edibles Legal

Yes, cannabis edibles are legal through licensed dispensaries. Recreational limits: 5mg THC per serving, 100mg maximum per package. Medical patients face no potency restrictions. Connecticut edibles carry the highest THC tax rate ($0.0275 per mg) of all product categories.

2025 Legislative Developments

Connecticut's 2025 legislative session produced significant cannabis policy changes:

Public Act 25-101 (HB 6855): Signed June 24, 2025, this omnibus bill:

- Establishes temporary cannabis operator licenses for court-appointed representatives

- Modifies medical marijuana certification duration and allows pharmacists to issue temporary extensions

- Redefines "backer" for licensing purposes

- Eliminates minimum separation requirements for certain equity joint ventures

- Requires additional persons to obtain key employee licenses

Public Act (HB 7181): Creates a statewide Cannabis and Hemp Enforcement Task Force, makes it a Class E felony for licensed establishments to sell to persons under 21 or to sell synthetic cannabis, and redirects civil penalty revenue to municipalities to incentivize local enforcement.

THC Potency Cap Increases (Effective October 1, 2025):

- Flower: 30% → 35% THC

- Concentrates (non-vape): 60% → 70% THC

Cultivation Outside DIAs (Effective January 1, 2026): Cultivator license holders may establish facilities outside Disproportionately Impacted Areas, subject to restrictions including mandatory DIA manufacturing operations, employee transportation cost coverage, and Social Equity Fund contributions.

Framework Assessment: Current vs. Optimized Performance

Current Configuration (50–55% Legal Market Share)

| Variable | Score | Weight | Contribution |

|---|---|---|---|

| Price Competitiveness | -0.60 | 4× | -2.40 |

| Access Density | 0.20 | 1× | 0.20 |

| Safety & Quality | 0.75 | 1.2× | 0.90 |

| Convenience | 0.40 | 1× | 0.40 |

| Enforcement | 0.60 | 0.6× | 0.36 |

| Fragmentation | -0.30 | 0.8× | -0.24 |

| Total ΔU | -0.78 |

Connecticut overperforms the mathematical prediction (31–35%) by 15–20 points due to Northeast consumer culture (42.9% hold bachelor's degrees), civic loyalty, and potentially conservative illicit price estimates.

Optimized Configuration (70–75% Legal Market Share)

Assumes: Federal Schedule III rescheduling + SAFE Banking Act

| Variable | Score | Weight | Contribution |

|---|---|---|---|

| Price Competitiveness | -0.10 | 4× | -0.40 |

| Access Density | 0.65 | 1× | 0.65 |

| Safety & Quality | 0.75 | 1.2× | 0.90 |

| Convenience | 0.75 | 1× | 0.75 |

| Enforcement | 0.70 | 0.6× | 0.42 |

| Fragmentation | -0.15 | 0.8× | -0.12 |

| Total ΔU | +2.20 |

The delta: 20–25 percentage point improvement through strategic state policy reform plus federal action.

The Federal Policy Barrier

Connecticut cannot achieve optimal outcomes under current federal policy, regardless of state-level excellence.

The 280E Problem

IRC Section 280E prohibits cannabis businesses from deducting ordinary operating expenses from federal taxable income. A Connecticut dispensary with $2M revenue, $800K COGS, and $900K operating expenses pays federal tax on $1.2M instead of $300K actual profit—an effective 63% marginal federal tax rate before Connecticut's state taxes.

Impact: 280E forces Connecticut dispensaries to price cannabis 15–20% higher than economically necessary. Schedule III rescheduling would eliminate this barrier, reducing legal prices and improving competitiveness by 5–8 percentage points.

The Banking Problem

Without SAFE Banking Act passage, Connecticut dispensaries operate cash-heavy. Federal Reserve research shows card payment increases transaction frequency by 25%. Cash operations increase security costs, operational inefficiency, and consumer inconvenience—particularly significant for Connecticut's professional demographic.

Impact: Banking access would add 3–5 percentage points to legal market share through convenience improvement and operational cost reduction.

Combined federal reform impact: 8–13 percentage points—the difference between 60–67% and 70–75% legal market share.

Policy Recommendations for Connecticut

For Connecticut Legislature

1. Reduce total tax burden to 12–15% (CRITICAL)

Current: 6.35% sales + 3% municipal + 10–15% excise = 19–24% total

Recommended: 10% flat excise + 6.35% sales + 0% municipal = 16.35% total

Connecticut competes regionally with Massachusetts, New York, and Rhode Island. High taxes guarantee Connecticut remains the most expensive option. Lower rates maximize revenue through volume (Colorado model) rather than per-unit extraction.

2. Accelerate retail licensing to 120–140 stores statewide

Fast-track the 94 issued provisional licenses. Connecticut's small geography (5th smallest state) should enable excellent coverage with 3.3–3.8 stores per 100,000 residents.

3. Authorize statewide delivery expansion

Increase from 3 to 10–15 licensed delivery services. Allow dispensaries to operate their own delivery. Connecticut's urban-rural divide means retail alone cannot serve eastern Connecticut efficiently.

4. Address supply constraints

Fast-track pending cultivation licenses to increase competition and lower wholesale prices. The 2025 legislation allowing cultivation outside DIAs (effective January 2026) is a positive step.

For Connecticut Congressional Delegation

1. Support Schedule III rescheduling to eliminate 280E—reduces legal prices 15–20%, adds 5–8 percentage points to legal market share.

2. Support SAFE Banking Act passage—enables card payments, reduces security costs, adds 3–5 percentage points to legal market share.

Frame as fiscal federalism: The state chose legalization; federal policy prevents optimization.

Comparison to Other Markets

High-Performing Markets (75–85%+ Legal Share)

- Oregon (82%): $3.75/gram legal prices, 16.8 stores per 100K, 17% tax

- Colorado (84%): $4–6/gram, 8–10 stores per 100K, 15% tax

- Michigan (85%): Declining prices, rapid expansion, 16% total tax

Mid-Tier Markets (50–75% Legal Share)

- Massachusetts (65–70%): $250–280/oz, 400+ stores

- Nevada (75–80%): Tourism advantage, aggressive enforcement

- Connecticut (50–55%): $350/oz, 72 stores—underperforming peers

Struggling Markets (30–50% Legal Share)

- California (50%): 35% premium, 61% jurisdictions ban retail

- New York (30%): Multi-year licensing delays, enormous illicit delivery market

Connecticut's target: 70–75% legal share with reform—comparable to Nevada and approaching Massachusetts.

Economic Reality: The $26–46 Million Question

Current State (Policy Failure)

- Legal market: $300–320M annually

- Tax revenue: $49.4M (FY2024)

- Legal share: 50–55%

- Illicit market: $280–320M annually

- Border leakage to Massachusetts: $20–40M annually

Optimized State (Reform Success)

- Legal market: $480–540M annually

- Tax revenue: $75–95M annually (12–15% rate on larger base)

- Legal share: 70–75%

- Illicit market: $140–180M annually (reduced 50–55%)

- Jobs: 3,800–4,500 direct + indirect (up from 2,000–2,500)

The difference: $26–46M additional annual tax revenue—enough for 260–460 teacher salaries, or $130–230M in infrastructure over 5 years.

Conclusion: Connecticut's Choice

Connecticut wrote the U.S. Constitution. The state can write smart cannabis policy.

Three years after adult-use launch, Connecticut captures only 50–55% legal market share while hemorrhaging tens of millions annually to Massachusetts through border sales. The state's 20% tax burden and limited retail density create legal prices 60–95% above illicit alternatives, making black market dominance inevitable.

Yet Connecticut possesses advantages: small geography enabling efficient coverage, educated population valuing legal quality, professional retail infrastructure, and statewide authorization without local opt-outs. The state can achieve 70–75% legal market share through strategic reform.

State-level priorities:

- Reduce total tax burden to 12–15%

- Expand retail density to 120–140 stores

- Authorize widespread delivery services

- Accelerate cultivation licensing

Federal-level priorities:

- Schedule III rescheduling (280E elimination)

- SAFE Banking Act passage

Timeline: 36–48 months to 70–75% legal market share with state reform + federal action.

The framework demonstrates Connecticut can succeed. The question is whether Connecticut's legislature will learn from other states' successes and failures—or repeat the same mistakes while hoping for different results.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Wisconsin | Arkansas | South Dakota | Delaware

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0