IRC Section 280E: The 40-Year Tax Penalty Costing Cannabis Businesses $25 Billion Annually

Internal Revenue Code Section 280E—a 1982 provision designed to punish cocaine dealers—forces legal cannabis businesses to pay 70-90% effective federal tax rates while competing against untaxed black market operations. Schedule III rescheduling eliminates this penalty automatically, reducing operator costs 20-30% and enabling legal markets to finally compete on price.

Trulieve Cannabis received $115 million in 280E tax refunds after filing amended returns for 2019-2021. Curaleaf increased working capital by $117.2 million through 280E exemption claims. Verano saved $177.5 million. These refunds represent taxes paid under a punitive provision that treats state-licensed dispensaries identically to heroin traffickers despite operating in full compliance with state law.

What Is IRC Section 280E?

Internal Revenue Code Section 280E states: "No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (within the meaning of schedule I and II of the Controlled Substances Act) consists of trafficking in controlled substances."

Congress enacted 280E in 1982 following Edmondson v. Commissioner, a Tax Court case where a convicted cocaine trafficker successfully deducted business expenses—packaging materials, telephone costs, and rent—on his federal tax return under normal IRC Section 162 provisions allowing "ordinary and necessary" business expense deductions. Congress found this outcome unacceptable and created 280E to prevent drug dealers from claiming tax benefits.

The provision lay dormant for decades as federal drug enforcement focused on criminal prosecution rather than tax collection. Then states began legalizing medical cannabis (California 1996, expanding to 38 states by 2025), followed by adult-use legalization (24 states representing 183 million Americans). IRS applied 280E to these state-legal operations despite compliance with state regulatory frameworks, creating massive tax burdens on businesses operating legally under state law while still classified as "trafficking in controlled substances" under federal law.

What Cannabis Businesses Cannot Deduct

280E prohibits deductions for every operating expense except Cost of Goods Sold (COGS):

Cannot Deduct:

- Rent: Facility leases for retail, cultivation, manufacturing

- Salaries & wages: Employee compensation from budtenders to executives to cultivation staff

- Utilities: Electricity, water, gas for operations (except direct cultivation costs included in COGS)

- Marketing & advertising: Brand building, customer acquisition, promotional campaigns

- Professional services: Legal fees, accounting costs, consulting expenses

- Insurance: Property, liability, workers' compensation premiums

- Maintenance & repairs: Facility upkeep, equipment repairs

- Security: Armed guards, surveillance systems, alarm monitoring

- Technology: Point-of-sale systems, inventory tracking, website development

- Office expenses: Supplies, phones, internet, administrative costs

- Depreciation: Non-inventory assets (furniture, fixtures, vehicles, buildings)

- Interest: Business loan interest payments

- Taxes: State and local business taxes

- Travel: Business meetings, industry conferences, site visits

- Training: Employee education, compliance certifications

- Research & development: Product testing, cultivation optimization

- Compliance: Testing costs beyond COGS, regulatory reporting

Can Deduct:

- Cost of Goods Sold only: Direct costs of cannabis inventory production including wholesale cannabis purchases, direct labor for cultivation/processing, materials consumed in production, facilities and equipment directly used for production

This means a dispensary purchasing $2.5M wholesale cannabis can deduct that cost, but $1.5M in rent, salaries, utilities, security, and other operating expenses generates ZERO tax deductions despite being necessary to operate legally.

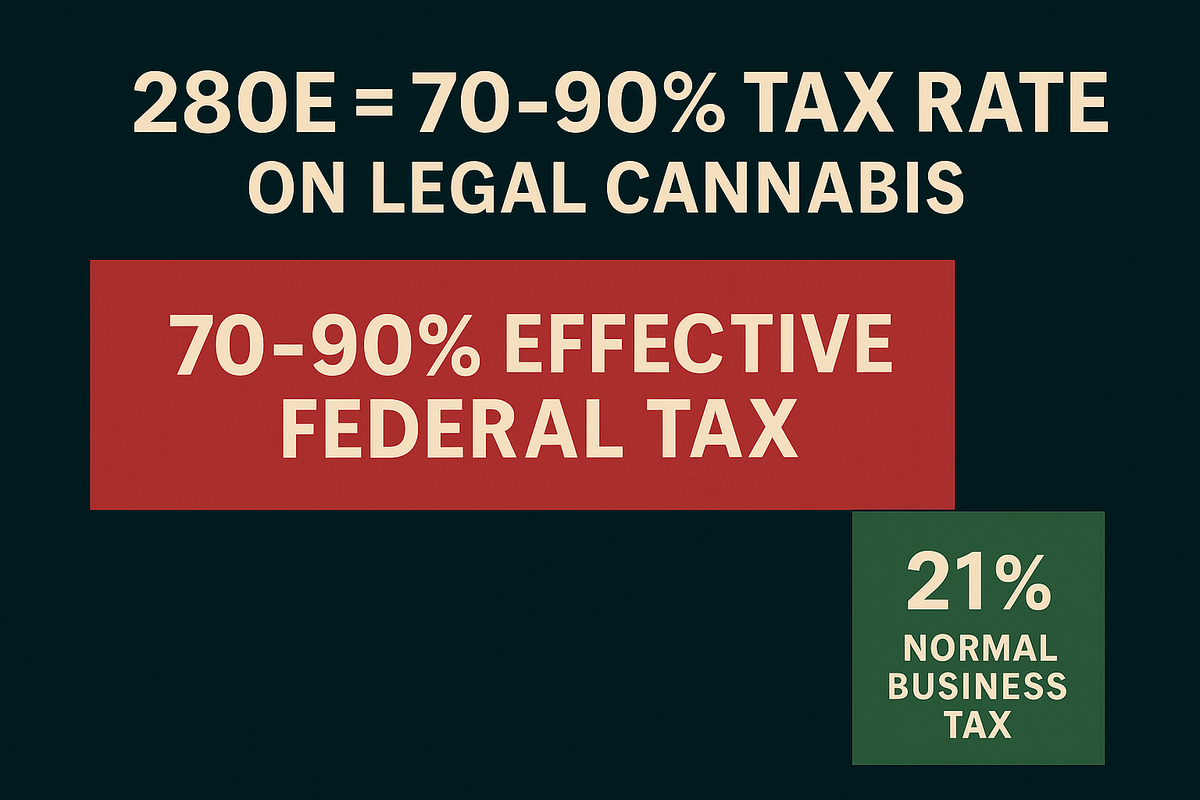

The 70-90% Effective Tax Rate

280E creates effective federal tax rates of 70-90% versus the statutory 21% corporate rate that normal businesses pay:

Normal Business Tax Calculation:

- Revenue: $5,000,000

- Cost of Goods Sold: -$2,500,000

- Operating Expenses: -$1,500,000

- Taxable Income: $1,000,000

- Federal Tax (21%): $210,000

- Effective Rate: 21% (on actual profit)

Cannabis Business Under 280E:

- Revenue: $5,000,000

- Cost of Goods Sold: -$2,500,000

- Operating Expenses: $0 (NOT DEDUCTIBLE under 280E)

- Taxable Income: $3,500,000 (inflated by disallowed expenses)

- Federal Tax (21%): $735,000

- Effective Rate: 73.5% (on actual profit of $1M)

- Excess Tax Burden: $525,000 annually

The dispensary pays $735,000 in federal taxes on $1,000,000 actual profit—an effective 73.5% rate—versus $210,000 (21%) for an identical business in any other industry. This $525,000 annual excess burden forces retail prices 15-25% higher than economically necessary, destroying price competitiveness versus untaxed black market dealers who pay zero federal taxes.

Analysis by accounting firm Cohn Reznick examining 2022 financials for Curaleaf, Cresco Labs, Green Thumb Industries, and Trulieve found current tax expense aligned within 15-25% of expected values when assuming federal taxable income equals 21% of gross profit (revenue minus COGS) with no expense deductions. This validates that 280E forces federal taxation on gross profit rather than net income, creating 70-90% effective rates depending on business model and expense ratios.

Why Effective Rates Vary: Business Model Matters

Vertically Integrated Operators (cultivation + manufacturing + retail) can capitalize more expenses into COGS through inventory accounting:

- Cultivation labor becomes COGS

- Manufacturing equipment depreciation becomes COGS

- Facility costs for production areas become COGS

- Utilities for grow operations become COGS

- Effective federal tax rate: 50-65% (still punitive but better than retail-only)

Retail-Only Dispensaries purchasing wholesale product have minimal COGS:

- Purchase price of inventory only COGS

- All facility, labor, and operational costs non-deductible

- Effective federal tax rate: 70-90% (devastating)

This explains why 27% of Michigan cannabis operators remain unprofitable despite strong market fundamentals—280E tax burden consumes margins.

The Competitive Price Disadvantage

280E's most damaging impact: forcing legal cannabis to charge 40-50% price premiums versus economically efficient pricing, guaranteeing black market price advantages.

Cannabis business generating $1M profit must cover $525K excess 280E burden (versus normal taxation) plus state/local taxes totaling $600K plus maintain profit target. To achieve $1M net profit, business must generate $2.1M in pre-tax income, requiring $6M+ revenue versus $5M economically efficient level—translating to 20-30% higher retail prices.

Black market dealer selling identical product:

- Wholesale cost: $2,000/pound ($4.40/gram)

- Desired margin: 100% markup

- Retail price: $4,000/pound ($8.80/gram)

- Federal taxes: $0

- State taxes: $0

- Price advantage: 40% cheaper than legal operator charging $14-16/gram to cover 280E burden

Market Impact: The CBDT Framework Evidence

The Consumer-Driven Black Market Displacement Framework quantifies 280E's market impact through the Price Gap (g) coefficient. Framework validation across 24 U.S. markets demonstrates:

Price Gap coefficient: -4.0 (most powerful predictor of legal market share)

Every 10 percentage point increase in legal price premium reduces legal market share by 8-10 percentage points. Cannabis businesses operating under 280E maintain 25-35% price premiums above economically efficient levels, suppressing legal market share by 20-28 percentage points versus post-280E elimination scenarios.

Use the CBDT Framework Calculator to model 280E elimination impacts:

California Current Status:

- Price Gap: +35% (legal significantly more expensive)

- Predicted Legal Share: 52% (actual 50-55%)

California Post-280E Elimination:

- Price Gap: +10% (reduced by 25 points as costs decline)

- Predicted Legal Share: 68-72% (improvement of 16-20 points)

Single policy change—280E elimination via Schedule III rescheduling—increases California legal market from $4B to $7.3-8.3B, displacing $3.3-4.3B from untaxed black markets annually. State tax revenue increases from $1.1B to $1.4-1.6B despite lower per-unit operator burden.

Schedule III Rescheduling: Automatic 280E Elimination

280E applies only to Schedule I and Schedule II controlled substances. DEA rescheduling cannabis to Schedule III automatically eliminates 280E application—no additional Congressional action required.

Once final rule published in Federal Register, 280E inapplicability immediate for tax years beginning after effective date. Cannabis businesses can deduct ordinary operating expenses under normal IRC Section 162 provisions applying to all other industries.

The Refund Wave: Operators Fighting Back

Multiple MSOs filed amended returns challenging 280E applicability:

- Trulieve Cannabis: $115M refunds received (2019-2021)

- Curaleaf Holdings: $117.2M working capital increase

- Verano Holdings: $177.5M savings

- Cresco Labs: $73.9M increase in operating cash

- Ascend Wellness: Filed amended returns 2020-2022

Industry insiders estimate sector-wide tax pivot saved billions, with tax attorney James Mann stating: "It's keeping most of these companies solvent and afloat. I mean, its impact cannot be understated."

Post-280E Elimination: The Transformation

Before 280E Elimination (Mid-sized Dispensary):

- Federal Tax (21% on gross profit): $735,000

- Net Profit: $565,000 (11.3% margin)

After 280E Elimination:

- Federal Tax (21% on net profit): $210,000

- Net Profit: $1,190,000 (23.8% margin)

- Improvement: +$625K annual profit (+111% increase)

This $625K enables:

- Price reduction: Lower retail 20-25% increasing volume and market share

- Wage increases: Competitive compensation attracting/retaining talent

- Expansion: Second location, additional cultivation capacity

- Quality improvement: Better testing, product development

- Marketing: Brand building, customer acquisition

The Federal Revenue Math: Why 280E Costs Government Money

Joint Committee on Taxation methodology demonstrates Schedule III rescheduling generates $26.9B net government revenue over 10 years despite federal collections declining $24.1B:

- Federal revenue loss: -$24.1B

- State/local revenue gain: +$38.2B (expanded legal markets)

- Criminal justice savings: +$12.8B

- Net government revenue: +$26.9B over 10 years

280E elimination increases total government revenue $65-90B over 10 years despite federal direct loss—state gains + criminal justice savings overwhelm federal decline.

Conclusion: The Case for Immediate Action

280E represents federal policy malpractice: provision designed to punish cocaine dealers applied to state-licensed cannabis businesses, creating 70-90% effective tax rates forcing impossible economics while competing against untaxed black markets.

President Trump endorsed Schedule III rescheduling September 2024. DEA final rule eliminates 280E automatically. Once cannabis rescheduled, legal markets gain price competitiveness, black markets lose advantages, tax revenue expands, criminal enterprises shrink.

The only question: when will federal government stop taxing legal cannabis businesses like heroin traffickers?