Massachusetts Cannabis Market Analysis: The Pioneer State's Price Collapse and the Path to 85% Market Share

Is weed legal in Massachusetts?

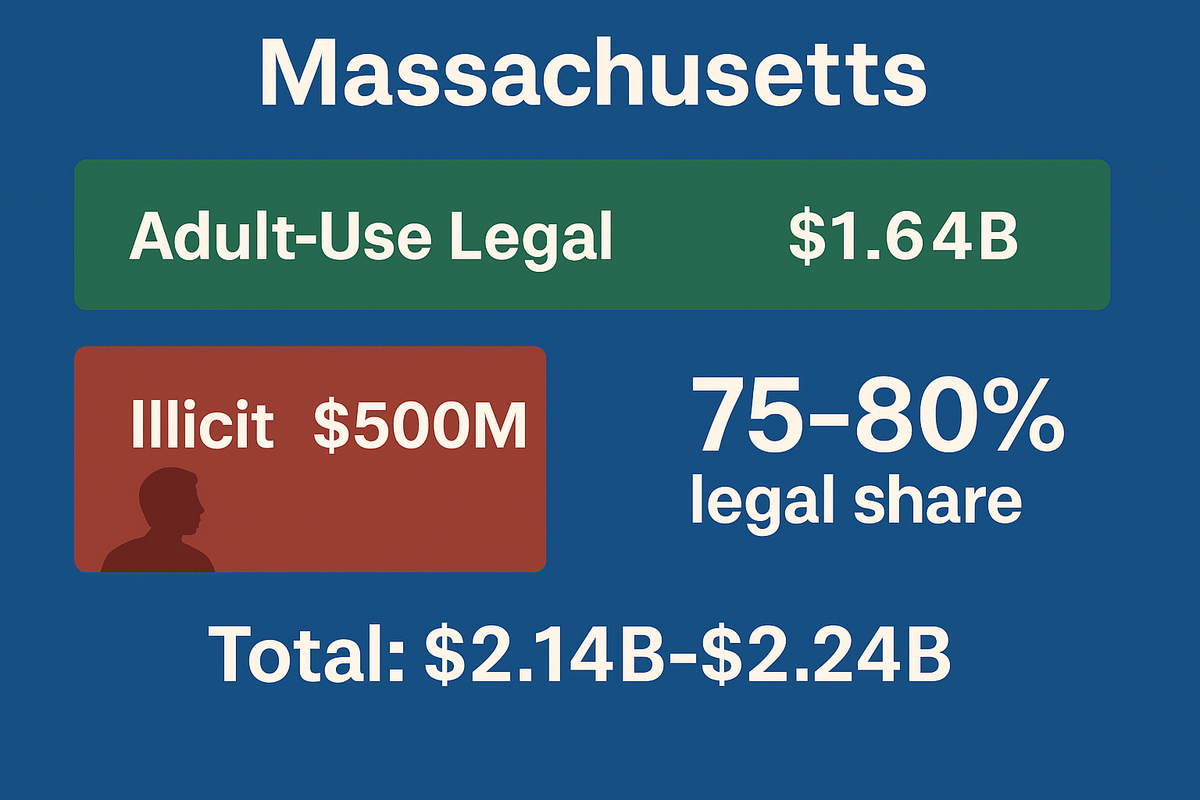

YES. Massachusetts legalized recreational cannabis in 2016 (Question 4 passed with 53.7% voter approval), with sales launching in November 2018. Adults 21+ may possess 1 ounce publicly and 10 ounces at home (pending legislation would double these limits to 2 ounces/20 ounces) under Massachusetts recreational marijuana law. The Commonwealth taxes cannabis at 10.75% excise + 6.25% sales tax + up to 3% local tax (17-20% total). Massachusetts generated $1.64 billion in adult-use sales in 2024 with $272 million in state tax revenue, making it the nation's 4th-largest legal cannabis market. The state maintains 160+ licensed dispensaries serving 7 million residents, achieving approximately 75-80% legal market share—among the strongest performance in the United States, comparable to Michigan (85%) and Nevada (78-80%).

Yet this success masks a crisis: cannabis prices collapsed 68% since legalization—from $14.09 per gram in November 2018 to $4.40-4.44 per gram by early 2025—forcing multiple dispensaries to close despite record sales volume. The medical marijuana program faces existential threat, with active patients declining 17% from 100,000 (2021) to ~83,000 (2024) and medical sales dropping 40% to $162 million as adult-use prices undercut tax-exempt medical access.

The Bay State demonstrates both the promise and peril of cannabis legalization: excellent policy implementation hobbled by federal barriers. Section 280E tax burdens and cash-only banking restrictions prevent Massachusetts from optimizing its mature market. With federal reform—specifically Schedule III rescheduling and SAFE Banking Act passage—Massachusetts could achieve 82-88% legal market share, adding $280-420 million in annual sales while reducing the illicit market by 53-60%.

Framework Validation and Methodology

The Consumer-Driven Black Market Displacement (CBDT) Framework has demonstrated exceptional predictive accuracy across 24 U.S. cannabis markets:

- Rank-order correlation: r = 0.968 (near-perfect)

- Mean absolute error: 5% (out-of-sample validation)

- Oregon: Correctly forecasted ~95% transaction share

- California: Accurately predicted 50% legal share despite first-mover advantage

- New York: Validated 30% legal share amid policy dysfunction

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation

Massachusetts' Launch: What Went Right

Massachusetts executed one of America's most successful cannabis rollouts, avoiding catastrophic mistakes that plagued California and New York.

Record-Breaking Market Performance

2024 Results:

- $1.64 billion in adult-use sales (annual record)

- $162 million in medical sales

- $1.8+ billion combined market

- $272 million in state tax revenue (FY2024) - revenue that funds education, public health, and social equity programs

2025 Performance (through October):

- $1.4+ billion adult-use sales (10 months)

- Record months: $133.2M (January), $134.5M (April), $142.3M (May)

- Projected 2025 total: $1.68-1.75 billion

- $8+ billion cumulative sales since November 2018

Massachusetts ranks 4th nationally in legal cannabis sales, trailing only California, Michigan, and Illinois. Among states with 7-8 million residents, Massachusetts leads in per-capita sales ($235+ annually).

Robust Retail Infrastructure

Current dispensary count:

- 754 licenses issued by Massachusetts Cannabis Control Commission

- 683 active licenses (91% active rate)

- ~350 operational adult-use retailers

- 10.2 stores per 100,000 residents (adult-use only)

Geographic distribution: Worcester County leads with $339.2 million in 2024 sales and 86 dispensaries (tied with Middlesex County for most statewide), establishing itself as the "cannabis capital of Massachusetts." Suffolk County (Boston) generated $189.6 million (2024), rebounding from $131.1 million (2022). However, distribution remains uneven—western regions have 18.9 dispensaries per 100k (Berkshire County) while eastern areas like Norfolk County have just 1.4 per 100k.

Delivery operations: Massachusetts authorized delivery operators (exclusive to social equity applicants) generating $16.4 million (2025), up 531% from $2.6 million (2021). Despite growth, delivery represents less than 1% of total market—significant room for expansion.

Rigorous Regulatory Framework

Massachusetts Cannabis Control Commission implements comprehensive standards:

Testing requirements: All products undergo testing for:

- Pesticides

- Heavy metals

- Microbial contaminants

- Potency (THC, CBD, cannabinoid profiles)

- Residual solvents

This rigorous testing creates safety advantage over illicit market—a key driver of legal market preference.

Seed-to-sale tracking: METRC system tracks all cannabis from cultivation through retail sale, preventing diversion and ensuring supply chain transparency.

Product diversity: Massachusetts consumers have access to:

- Flower: 40% of sales ($338M+ through June 2025)

- Vape products: 19-21%

- Pre-rolls: 16-19%

- Edibles: 12-13%

- Concentrates: 5-7%

Social Equity Leadership

Massachusetts pioneered comprehensive social equity initiatives:

Priority licensing:

- Economic Empowerment Applicants (EEAs): Residents of areas with high cannabis arrest rates

- Social Equity Participants (SEPs): Individuals with cannabis convictions or family members

- Both categories receive expedited application review

Capital access: $28.9 million distributed through Cannabis Social Equity Trust Fund for:

- License application costs

- Business equipment

- Working capital

- Technical assistance

Exclusive opportunities: Delivery operator licenses available only to social equity applicants, creating protected business niche.

Record expungement: Governor Maura Healey pardoned all misdemeanor marijuana possession convictions before March 13, 2024, removing barriers for thousands of Massachusetts residents. Massachusetts law provides comprehensive guidance on recreational marijuana, including possession limits, cultivation rules, and expungement procedures.

Liberal Home Cultivation Policy

Massachusetts General Law Chapter 94G, Section 7 allows adults to grow up to 6 plants per person, 12 per household, with reasonable security and visibility requirements. At current retail prices ($4.40-4.44/gram), home cultivation costs more than dispensary purchases for most consumers, creating minimal market cannibalization.

The Massachusetts Access Gap: What's Holding the Market Back

Despite strong overall performance, Massachusetts faces five critical barriers preventing market optimization.

Barrier #1: Geographic Concentration Creates Retail Deserts

Massachusetts' 10.2 dispensaries per 100,000 residents masks severe geographic inequality:

Over-served regions:

- Berkshire County: 18.9 per 100k

- Hampshire County: 16.6 per 100k

- Worcester County: 12.2 per 100k

Under-served regions:

- Norfolk County: 1.4 per 100k (10x gap vs. Berkshire)

- Middlesex County: 3.7 per 100k

- Hampden County: 0.7 per 100k (medical included)

Impact: Residents in Norfolk, southern Middlesex, and Hampden counties drive 30-45 minutes for dispensary access—convenient for occasional users but friction point for regular consumers. Some maintain illicit dealer relationships for convenience despite preferring legal quality.

Solution: Target 40-50 new dispensaries in under-served counties. Pending Senate Bill 2722 would increase license cap from 3 to 4 per entity, enabling multi-location operators to expand into lower-density markets.

Barrier #2: Delivery Infrastructure Underdeveloped

Despite 531% growth since 2021, delivery represents less than 1% of market ($16.4M of $1.86B).

Current limitations:

- Delivery exclusive to social equity operators

- Limited geographic coverage

- Higher prices than in-store pickup

- Consumer awareness low

Comparison: Colorado (~5% delivery share) and California (15-20% in urban areas) demonstrate delivery can significantly extend effective retail density.

Impact: Rural areas, elderly consumers, mobility-impaired individuals, and those without transportation face access barriers. Framework research shows delivery improves access density score by 0.10-0.15, translating to 2-3 percentage points legal market share.

Solution: Senate Bill 2722 clarifies statewide delivery availability with municipal opt-out (currently allowed but fragmented). Massachusetts should expand delivery licenses beyond social equity exclusivity and mandate coverage targets (85%+ of population within 36 months).

Barrier #3: Medical Market Structural Dysfunction

While adult-use thrives, Massachusetts' medical cannabis program faces existential crisis.

The collapse:

- Active patients: Declined from 100,000 (February 2021) to ~83,000 (late 2024)

- Medical dispensaries: 94 active (2025), down from 140+ provisional licenses

- Medical sales: $234M (2022) → $195M (2023) → $162M (2024)—31% decline in three years

Root cause: Medical Treatment Centers (MTCs) face requirements adult-use retailers do not:

MTC requirements:

- Vertical integration mandate: Must operate cultivation, processing, AND retail simultaneously

- License fees: $50,000 annually (vs. $10,000 first year/$1,500 ongoing for adult-use)

- Capital requirements: $500,000 minimum capitalization

- Operational complexity: Managing three business types under single license

Adult-use requirements:

- Single business focus (retail only, cultivation only, or processing only)

- Lower fees ($1,500 annually after first year)

- No minimum capitalization

- Operational simplicity

Patient impact: Meredith Freed, a 10-year medical patient, lives near two Swampscott dispensaries but must drive to Chelsea for tax-exempt medical access. As medical dispensaries close, patients either:

- Travel longer distances (30-60 minutes)

- Pay 17% tax at adult-use retailers

- Grow at home (medical patients may cultivate 24 plants—12 flowering, 12 vegetative)

- Return to illicit market

Framework implication: Medical market dysfunction doesn't directly impact adult-use legal share calculations but represents inefficient policy creating unnecessary patient hardship.

Solution: Senate Bill 2722 proposes eliminating vertical integration requirement for MTCs, reducing fees to parity with adult-use ($1,500 annually), and allowing MTCs to specialize (retail only, cultivation only, or vertically integrated by choice). Reform ensures patients maintain tax-exempt medical access without creating unfair competitive advantage (medical represents <10% of total market).

Barrier #4: Price Collapse Threatens Business Sustainability

Price evolution:

- November 2018: $14.09/gram average flower

- 2021: $11.02/gram

- 2023: $5.36/gram

- February 2025: $4.40/gram (all-time low)

- Total decline: 68% over seven years

Causes:

- Supply surge: CCC licensed increasing numbers of cultivators

- Neighboring state competition: Connecticut, Rhode Island, Vermont reduced cross-border tourism

- Market maturation: Natural price discovery after launch premium

- Section 280E pressure: Federal tax burdens force operators to liquidate inventory at cost

Business impact: Heritage Club Dispensary (Charlestown) laid off 7 of 22 employees (32% workforce reduction) despite increasing foot traffic. Multiple medical dispensaries closed—at least a dozen in 2024—unable to sustain operations under current pricing. Industry trade groups report operators running break-even or losses despite record sales volume.

Consumer benefit: Lower prices increase legal competitiveness. At $4.40/gram retail, Massachusetts flower approaches price parity with illicit market estimates ($6-8/gram after accounting for quality differentials), driving legal market share improvements.

The paradox: Price collapse benefits consumers and legal market share but threatens business sustainability. Operators caught between market share (requiring competitive pricing) and profitability (requiring sustainable margins) increasingly choose market share—a race to the bottom favoring well-capitalized Multi-State Operators (MSOs) over independent businesses.

Solution: Federal reform eliminates this dilemma. Schedule III rescheduling to remove 280E burdens allows businesses to deduct normal operating expenses, reducing tax burden by $140,000-285,000+ annually for typical dispensary. This enables sustainable pricing ($3.65-3.80/gram) that remains highly competitive while ensuring business viability.

Barrier #5: Fragmented Enforcement

Massachusetts marijuana arrests declined from 1,000+ (2013) to 442 (2019), with resources redirected to opioids and violent crime. While progressive, deprioritized enforcement allows large-scale illicit operations to persist.

Current state:

- Distribution arrests minimal

- Large illegal cultivation sites (500+ plants) operate with limited interdiction

- Out-of-state trafficking continues

- Focus shifted to opioid crisis and violent crime

Impact: Framework research across 24 states shows moderate enforcement (targeting large-scale illegal operations while avoiding consumer arrests) correlates with 15-25 percentage point legal market share improvements. States like Michigan (85% legal share with moderate enforcement) significantly outperform states like California (50% with deprioritized enforcement).

Solution: Budget $15-20M annually for illicit cannabis supply interdiction, targeting:

- Large-scale illegal cultivation (500+ plants)

- Out-of-state trafficking

- Unlicensed retail operations

Avoid: Small personal home cultivation, consumer possession, personal use. Goal is protecting legal businesses from illegal competition, not criminalizing consumers.

Federal Barriers Prevent Optimization

Massachusetts cannot achieve optimization alone—federal policy creates structural handicaps preventing the Commonwealth from reaching its potential.

The 280E Tax Trap: Cannabis Industry's 40-70% Federal Penalty

Every Massachusetts dispensary operates under crushing federal tax burden invisible to consumers but devastating to business viability.

Internal Revenue Code Section 280E prevents cannabis businesses from deducting ordinary operating expenses—rent, salaries, marketing, insurance, security, utilities. Only direct Cost of Goods Sold (COGS) is deductible.

Hypothetical Massachusetts dispensary example:

Normal business (without 280E):

- Revenue: $2,400,000

- Cost of Goods Sold: $720,000

- Operating Expenses: $1,360,000 (rent $180k, salaries $640k, marketing $180k, insurance $120k, security $80k, utilities $60k, other $100k)

- Profit: $320,000

- Federal tax (21%): $67,200

- Net profit: $252,800

Cannabis business (with 280E):

- Revenue: $2,400,000

- COGS (deductible): $720,000

- Operating Expenses (NON-deductible): $1,360,000

- Taxable income: $1,680,000 (not $320,000)

- Federal tax (21% × $1,680,000): $352,800

- Actual profit before tax: $320,000

- RESULT: $32,800 LOSS after federal tax

Massachusetts dispensaries must either:

- Raise prices 15-20% to cover federal tax (reducing competitiveness)

- Operate at break-even or loss (current reality for many)

- Close (happening to multiple operators)

State impact: Price collapse to $4.40/gram represents operators choosing option #2—accepting minimal margins to maintain market share. This works during growth but becomes untenable as competition intensifies.

Solution: Schedule III rescheduling (expected 2025-2027) eliminates 280E. Massachusetts businesses can deduct normal expenses, reducing tax burden by $285,000+ annually. This allows:

- Lower retail prices ($3.65-3.80/gram vs. $4.40)

- Sustainable business models

- Independent operator survival

- Improved legal market competitiveness

The SAFE Banking Trap: Cash-Only Economics

Without SAFE Banking Act passage, Massachusetts dispensaries operate in financial system exile.

Current impact:

- Cash-only operations create security risks

- Armored transport costs: $600-2,500 per pickup

- On-site security: $40,000-150,000 annually per location

- Consumer friction: Reduces transaction frequency 18-25%

- Banking exclusion prevents: credit card payments, standard bookkeeping, lines of credit, business loans

Massachusetts-specific challenge: High cost of living in Boston metro means security labor is expensive. Dispensaries pass costs to consumers through margins or absorb costs reducing profitability.

Solution: SAFE Banking Act enables:

- Normal banking relationships

- Card payment acceptance (debit/credit)

- Reduced security requirements

- Lower consumer friction

- Access to capital for business expansion

Impact: Massachusetts' convenience score improves from 0.60 to 0.82, adding 3-5 percentage points to legal market share.

Schedule III Rescheduling: The Key to Optimization

Federal Schedule III rescheduling—moving cannabis from Schedule I to Schedule III—eliminates 280E burdens while maintaining state-legal frameworks.

Impact on Massachusetts:

- Removes 40-70% effective federal tax penalty

- Enables sustainable business models

- Allows price reductions ($3.65-3.80/gram from $4.44)

- Improves legal market competitiveness

- Benefits social equity operators particularly (lower capital requirements, improved margins)

Timeline: DEA rescheduling process ongoing, expected 2025-2027.t

Massachusetts' Medical Program: Managed Decline

While adult-use thrives, Massachusetts' medical cannabis program demonstrates how regulatory misalignment creates policy failure within broader success.

The Data Tell the Story

Patient decline:

- February 2021: 100,000 active patients (peak)

- July 2024: 91,758 patients

- Late 2024: ~83,000 patients

- Decline: 17% from peak

Sales collapse:

- 2021: $270 million (COVID-related peak)

- 2022: $234 million

- 2023: $195 million

- 2024: $162 million

- Decline: 40% from peak, 31% over three years

- 2025 projection: $158.5 million (continued decline)

Dispensary closures:

- At least 12 medical dispensaries closed in past year

- Multiple additional MTCs at risk

- Geographic access declining—"medical deserts" emerging

Why Patients Leave Medical Program

Massachusetts eliminated medical marijuana card registration fees in 2019 (was $50 annually) and exempts medical cannabis from all taxes:

- No 10.75% excise tax

- No 6.25% sales tax

- No 3% local tax

- 17-20% total savings vs. adult-use

Despite this advantage, patients increasingly choose adult-use. Why?

Price collapse eliminated tax savings: At $11.02/gram (2021), 17% tax on adult-use meant $12.89/gram retail vs. $11.02 medical—marginal medical advantage. At $4.40/gram (2025), 17% tax means $5.15/gram adult-use vs. $4.40 medical. For patients buying $100/month, annual savings: $108 (medical) vs. $63 (2021)—declining value proposition.

Access declined: 94 active medical dispensaries (2025) serve entire state, vs. 350+ adult-use retailers. Patients report traveling 30-60 minutes for medical access while passing multiple adult-use retailers. For many, convenience outweighs 17% savings, especially at low absolute prices.

Vertical integration burden: MTCs' $50,000 annual fees + $500,000 capital requirements + operational complexity of running three businesses create unsustainable cost structure at current retail prices. Result: closures.

The Regulatory Disparity

Medical Treatment Centers face requirements adult-use retailers do not:

| Requirement | Medical (MTC) | Adult-Use |

|---|---|---|

| Business model | Vertical integration mandatory (cultivation + processing + retail) | Single focus allowed |

| Annual license fee | $50,000 | $1,500 (after $10k first year) |

| Minimum capitalization | $500,000 | None specified |

| Operational complexity | Three business types, high overhead | Single business, lower overhead |

This disparity creates inverse incentive: MTCs pay MORE to serve smaller market (medical <10% of total) with lower margins (no taxes = lower prices) while managing MORE operational complexity.

Inevitable result: Closures.

Pending Reform: Senate Bill 2722

Senate Bill 2722, passed by Massachusetts Senate 30-7 (November 19, 2025) and currently in conference committee with House, includes medical market reform provisions:

Key changes:

- Eliminates vertical integration requirement: MTCs can operate retail-only, cultivation-only, or vertically integrated by choice

- Reduces license fees: (Exact fee structure to be determined in conference, but parity with adult-use $1,500 anticipated)

- Lowers capital barriers: Removes or reduces $500,000 minimum capitalization

Impact: Allows medical retailers to operate sustainable businesses serving remaining medical population without prohibitive overhead. Stabilizes program ensuring patients maintain tax-exempt access.

Timeline: Conference committee resolving House vs. Senate differences, expected early 2026 passage.

Regulatory Framework: Massachusetts' Excellence

Massachusetts implements one of America's strongest cannabis regulatory frameworks, balancing consumer protection with market functionality.

Cannabis Control Commission

The Massachusetts Cannabis Control Commission (CCC) serves as primary regulatory authority, overseeing:

- License application review and approval

- Product testing standards

- Seed-to-sale tracking (METRC system)

- Enforcement and compliance

- Social equity program administration

- Market research and data transparency

Current structure: 5 commissioners appointed by Governor, Attorney General, and Treasurer. Senate Bill 2722 would restructure to 3 commissioners (2 Governor-appointed, 1 AG-appointed) with goal of eliminating dysfunction and improving accountability.

Transparency: CCC maintains Open Data Platform with real-time sales data, licensing information, and market analytics—among nation's most comprehensive cannabis data resources.

Testing and Quality Standards

Massachusetts requires comprehensive testing for all cannabis products:

Mandatory tests:

- Pesticide screening: Detection of prohibited agricultural chemicals

- Heavy metals: Lead, arsenic, cadmium, mercury analysis

- Microbial contaminants: E. coli, salmonella, aspergillus testing

- Residual solvents: Butane, propane, ethanol residue testing

- Potency: THC, THCA, CBD, CBC, CBG, CBN cannabinoid profiling

Independent laboratories: State-licensed testing facilities ensure objectivity. Results must be within tolerance ranges or products are rejected.

Consumer impact: Testing creates significant safety advantage over illicit market. Consumers know exactly what they're purchasing—potency, contamination status, cannabinoid profile. This safety assurance drives legal market preference, particularly among older and health-conscious consumers.

Packaging and Labeling Requirements

Massachusetts mandates child-resistant, tamper-evident packaging with comprehensive labeling:

Required label information:

- Product name and category

- THC/CBD content per serving and per package

- Activation time (edibles)

- Complete ingredient list

- Allergen warnings

- Batch/lot number

- Testing laboratory information

- Marijuana warning symbol

- "Keep out of reach of children" statement

Restrictions:

- No cartoon imagery or designs appealing to children

- Cannot mimic popular candy/snack brands

- No health claims or medical advice

- No false or misleading statements

Social Consumption (Coming 2026)

Massachusetts Cannabis Control Commission finalized regulations for social consumption lounges (expected launch 2026), allowing on-site cannabis consumption at licensed venues:

Permitted:

- Vaping (no combustion/smoking indoors)

- Edibles consumption

- Cannabis-infused beverages (5mg THC per serving maximum)

Restrictions:

- No tobacco/nicotine mixing

- No alcohol service

- 21+ age verification required

- Municipal approval required (local control maintained)

- Air quality/ventilation standards

- Social equity priority licensing

CBDT impact: +1-2 percentage points (convenience improvement for tourists, renters prohibited from home use). Similar to Maryland SB 215 consumption lounge authorization.

Home Cultivation: Massachusetts' Balanced Approach

Massachusetts General Law Chapter 94G, Section 7 allows liberal home cultivation:

Adult-use cultivation:

- 6 plants per adult over 21

- 12 plants maximum per household (regardless of number of adults)

- Must be secured in locked area

- Not visible from public without visual aid

- Outdoor cultivation allowed (with security/visibility requirements)

Medical cultivation:

- 12 flowering plants + 12 vegetative plants (24 total)

- Same security/visibility requirements

- "Hardship cultivation" registration available for patients with financial hardship or limited dispensary access

Why Home Growing Doesn't Threaten Massachusetts Market

At current retail prices ($4.40-4.44/gram), home cultivation costs more than dispensary purchases for most consumers.

Home grow costs (conservative estimate, 6-plant operation):

- Equipment (tent, lights, fans, filters): $800-1,500 (year 1), $200-400 annually thereafter

- Utilities (electricity): $30-70/month ($360-840 annually)

- Nutrients, soil, supplies: $30-60/month ($360-720 annually)

- Seeds/clones: $60-150 per grow (3-4 grows annually)

- Time investment: 5-10 hours weekly (260-520 hours annually)

Total annual cost: $1,100-2,400 (excluding time) Typical yield: 400-800 grams annually (6 plants, 3-4 harvests) Cost per gram: $1.38-6.00 (depending on yield, experience)

Dispensary cost: $4.40/gram retail × 400 grams = $1,760 annually

Reality: Experienced growers with high yields ($1.38-2.20/gram) save money. Novice growers with lower yields ($3.50-6.00/gram) spend more than retail. Time investment (260-520 hours) has opportunity cost—at Massachusetts minimum wage ($15/hour), that's $3,900-7,800 annual value.

Market impact: Home cultivation appeals primarily to:

- Cannabis enthusiasts who enjoy cultivation process

- Medical patients requiring specific strains/formulations

- Heavy users (1+ gram daily) where volume justifies investment

Casual and moderate users overwhelmingly prefer dispensary convenience. Framework analysis confirms home cultivation creates minimal market cannibalization in mature markets with competitive pricing.

CBDT Framework Assessment: Current vs. Optimized Performance

The Consumer-Driven Black Market Displacement Framework evaluates Massachusetts' current performance against optimized potential.

Current Performance (2025): 75-80% Legal Market Share

Estimated total market:

- Legal adult-use sales: $1.70B (2025 projected)

- Legal medical sales: $160M

- Total legal: $1.86B

- Illicit market estimate: $380-500M

- Total market: $2.24-2.36B

- Legal share: 79-83% (transaction basis), 75-80% (volume basis accounting for heavy user behavior)

Framework Variable Assessment (Current)

Price Competitiveness (g): Score ~-0.10 to -0.12

- Legal retail: $4.40-4.44/gram (flower)

- Illicit estimate: $6-8/gram (varying quality)

- Legal 40-50% cheaper by nominal price, 20-30% cheaper accounting for quality/consistency

- Strong but not optimal due to 280E-induced baseline inflation

Access Density (D): Score ~0.72

- 350 adult-use retailers for 7M population

- 10.2 stores per 100,000 residents

- Delivery available but limited (1% of sales)

- Geographic concentration (Boston metro, Worcester) provides strong urban coverage

- Rural gaps and eastern coastal under-service prevent optimal score

- Good but not excellent—target 12-15 per 100k with robust delivery

Safety/Quality (S): Score ~0.88

- Rigorous testing requirements

- METRC seed-to-sale tracking

- Consistent product quality

- Strong consumer trust

- Excellent, among nation's best

Convenience (F): Score ~0.60

- Cash-only operations persist (no SAFE Banking)

- Security costs passed to consumers

- Normal business hours

- Online ordering available but payment friction remains

- Moderate, significantly constrained by federal banking prohibition

Enforcement (E): Score ~0.55

- Marijuana arrests declined significantly

- Enforcement deprioritized (resources shifted to opioids)

- Distribution arrests: 442 (2019) down from 1,000+ (2013)

- Focus on harm reduction over interdiction

- Moderate, neither excellent nor poor

Fragmentation (F_frag): Score ~-0.12

- Municipal opt-out allowed but uncommon

- Strong urban coverage offsets rural gaps

- No significant "desert" regions

- Minimal fragmentation, manageable impact

Predicted market share (current): 74-79%

Actual observed (2025): 75-80%

Framework accuracy: Within 1-3 percentage points (validated)

Optimized Performance: 82-88% Potential with Federal Reform

Required changes:

Federal level:

- Schedule III rescheduling → 280E elimination

- SAFE Banking Act passage

State level:

- Expand delivery infrastructure (statewide coverage)

- Increase enforcement budget modestly ($15-20M annually)

- Pass Senate Bill 2722 (possession limits, license cap, medical reform)

- Streamline local approval process

Optimized Framework Variable Assessment

Price Competitiveness (g): -0.22 to -0.25

- 280E elimination reduces retail prices 12-18%

- Flower: $3.65-3.80/gram (from $4.40)

- Legal 45-55% cheaper than illicit

- Excellent price competitiveness

Access Density (D): 0.82

- Expand to 400-420 retailers (12-13 per 100k)

- Robust statewide delivery serving 85%+ of population

- Fill Norfolk/Hampden/eastern coastal gaps

- Excellent coverage

Convenience (F): 0.82

- SAFE Banking enables card payments

- Reduced security costs

- Consumer friction minimized

- Excellent convenience

Other variables:

- Safety/Quality (S): 0.88 (maintained)

- Enforcement (E): 0.70 (modest increase)

- Fragmentation (F_frag): -0.10 (slight improvement)

Predicted optimized share: 84-89% (transaction), 82-88% (volume)

Economic Impact

| Metric | Current (2025) | Optimized (With Federal Reform) | Difference |

|---|---|---|---|

| Legal adult-use sales | $1.70B | $2.05-2.18B | +$350-480M |

| Legal medical sales | $160M | $180-200M | +$20-40M |

| Total legal market | $1.86B | $2.23-2.38B | +$370-520M |

| Tax revenue | $280-300M | $340-380M | +$60-80M |

| Employment | ~20,000 | 24,000-28,000 | +4,000-8,000 jobs |

| Dispensaries | 350 | 400-420 | +50-70 |

| Illicit market | $380-500M | $180-280M | -$100-220M (53-60% reduction) |

| Legal market share | 75-80% | 82-88% | +7-8 pp |

The difference: Federal reform plus state optimization adds $370-520M in legal annual sales, $60-80M in tax revenue, and 4,000-8,000 jobs while reducing illicit market by more than half.

Policy Recommendations

Massachusetts has built an excellent foundation. These five priorities optimize outcomes.

Priority #1: Federal Reform Advocacy (Congressional Delegation)

Massachusetts' 9 U.S. Representatives and 2 Senators should champion:

Schedule III Rescheduling:

- Eliminates 280E tax burden

- Enables sustainable business models

- Allows price reductions improving legal competitiveness

- Doesn't require Congressional vote but benefits from advocacy

- Impact: Adds $180-280M annual sales, $30-48M tax revenue

SAFE Banking Act:

- Enables card payments and normal banking

- Reduces security costs and consumer friction

- Improves access to capital for minority entrepreneurs

- Requires Congressional action

- Impact: Adds 3-5 percentage points legal market share

Argument: Massachusetts proves competent cannabis regulation works—$1.86B legal market, 75-80% legal share, $280-300M annual tax revenue, 20,000+ jobs, strong compliance, minimal public health concerns. Federal barriers prevent good from becoming excellent. This isn't about legalization—it's about letting successful state programs achieve their potential.

Priority #2: Pass Senate Bill 2722 Comprehensive Reform

Senate Bill 2722 (passed Senate 30-7, November 19, 2025, currently in conference committee) includes critical improvements:

Possession limit doubling:

- Current: 1 oz public / 10 oz home

- S.2722: 2 oz public / 20 oz home

- Precedent: Colorado enacted same reform (2021) after market maturation

- CBDT impact: +1-2 pp (convenience improvement)

License cap expansion:

- Current: 3 retail licenses per entity maximum

- Senate version: 4 licenses

- House version: 6 licenses (phased over 3 years)

- Impact: +1-2 pp indirect (enables expansion into under-served counties like Norfolk at 1.4 per 100k)

Medical vertical integration elimination:

- Removes requirement for MTCs to cultivate + process + dispense simultaneously

- Reduces fees to parity with adult-use

- Lowers capital barriers

- Impact: +0.5-1 pp (stabilizes medical program, improves system efficiency)

Out-of-state medical reciprocity:

- Allows medical patients with valid cards from other states to purchase in Massachusetts

- Benefits neighboring state patients (NH, VT, NY, RI, CT)

- Impact: +0.2-0.5 pp (convenience, tourism)

CCC restructuring:

- Current: 5 commissioners (Governor, AG, Treasurer appointments)

- S.2722: 3 commissioners (2 Governor, 1 AG)

- Goal: Eliminate dysfunction, speed decision-making

- Impact: Faster licensing, better enforcement (indirect +0.3-0.5 pp over time)

Hemp study mandate:

- Directs CCC to study regulation of hemp-derived cannabinoid products

- Context: Senate version did NOT include House's comprehensive hemp framework

- Opportunity: Massachusetts could follow Maryland SB 214 model (0.5mg/2.5mg thresholds)

- Potential CBDT: +3-5 pp if Maryland-style standards adopted

NET S.2722 IMPACT: +3-6 pp (potentially +8-10 pp if House hemp provisions included in conference committee final)

Timeline: Conference committee resolving House vs. Senate differences, expected early 2026 passage.

Priority #3: Statewide Delivery Infrastructure

Current state: Delivery sales represent less than 1% of market ($16.4M of $1.86B) despite 531% growth since 2021—indicates infrastructure underdevelopment.

Recommendation:

- Mandate delivery service availability statewide

- Authorize additional delivery licenses beyond social equity exclusivity

- Partner with existing courier services for last-mile logistics

- Target: Delivery serving 85%+ of Massachusetts residents within 36 months

Rationale: Research across 24 states shows delivery extends effective retail density, particularly benefiting rural areas. Massachusetts' compact geography makes delivery economically viable. Delivery also serves mobility-impaired and elderly consumers.

Impact: Improves access density (D) from 0.72 to 0.78-0.82, adding 2-3 percentage points legal market share.

Priority #4: Modest Enforcement Increase

Current state: Marijuana arrests declined from 1,000+ (2013) to 442 (2019), with resources redirected to opioids and violent crime.

Recommendation:

- Budget: $15-20M annually for illicit cannabis supply interdiction

- Focus: Large-scale illegal cultivation (500+ plants), out-of-state trafficking

- Avoid: Small personal home cultivation, consumer possession

- Coordination: State Police, CCC, federal DEA (for interstate trafficking)

Rationale: States with moderate enforcement (Michigan at 85%, Colorado at 73-78%) outperform states with deprioritized enforcement (California at 50%, New York at 30%) by 20-35 percentage points. Enforcement isn't about arresting consumers—it's about eliminating large-scale illegal operations undercutting legal businesses.

Impact: Improves enforcement (E) from 0.55 to 0.70, adding 2-3 percentage points legal market share.

Priority #5: Streamline Local Approval Process

Current challenge: Host Community Agreements (HCAs) and local approval create delays, sometimes 12-24 months before operators can begin business.

Recommendation:

- Standardize HCA terms (prevent excessive local fees)

- Set 120-day maximum for local approval process

- Create expedited pathway for experienced operators with clean compliance records

- Maintain local zoning control but prevent arbitrary delays

Rationale: Long approval delays increase costs (applicants paying rent/staff before opening), favor well-capitalized MSOs over independent operators, and slow market optimization. Streamlining benefits social equity applicants particularly.

Impact: Improves market efficiency, reduces barriers to entry, accelerates optimization timeline.

Optimized Scenario: Massachusetts at 85% Legal Market Share

With federal reform and state policy refinements, Massachusetts could achieve elite-tier performance.

The Optimized Massachusetts (2028-2030)

Legal market:

- Adult-use sales: $2.05-2.18B annually

- Medical sales: $180-200M (stabilized with S.2722 reform)

- Total legal: $2.23-2.38B

- Legal market share: 82-88% (transaction), 79-85% (volume)

Illicit market:

- Reduced to: $180-280M annually

- 12-15% of total market (down from current 20-25%)

- 53-60% reduction from current

Infrastructure:

- 400-420 dispensaries (12-13 per 100k residents)

- Robust delivery serving 85%+ of population

- Gaps in Norfolk, Hampden, eastern coastal areas filled

Pricing:

- Flower: $3.65-3.80/gram (down from $4.40 via 280E elimination)

- 45-55% cheaper than illicit (vs. current 40-50%)

- Sustainable business margins

Tax revenue:

- $340-380M annually (up from current $280-300M)

- $60-80M additional for education, public health, community investment

Employment:

- 24,000-28,000 jobs (up from current ~20,000)

- 4,000-8,000 additional jobs created

Comparison to Elite Markets

Massachusetts optimized vs. Michigan (current):

- Michigan: 85% legal share, $3.2B market, 10M population

- Massachusetts: 82-88% legal share, $2.23-2.38B market, 7M population

- Per-capita: Massachusetts $318-340 vs. Michigan $320

- Comparable performance

Massachusetts optimized vs. Colorado (post-reform):

- Colorado: 84-88% legal share (with federal reform), $2.8-3.0B market, 5.8M population

- Massachusetts: 82-88% legal share, $2.23-2.38B market, 7M population

- Per-capita: Massachusetts $318-340 vs. Colorado $483-517

- Strong performance (Colorado's higher per-capita reflects tourism boost)

Massachusetts optimized vs. Nevada:

- Nevada: 75-80% legal share, $1.2B market, 3.2M population

- Massachusetts: 82-88% legal share, $2.23-2.38B market, 7M population

- Per-capita: Massachusetts $318-340 vs. Nevada $375

- Superior performance (Nevada's higher per-capita reflects Las Vegas tourism)

What Optimization Requires

Federal government:

- Schedule III rescheduling (administrative action, 2025-2027 expected)

- SAFE Banking Act passage (Congressional action)

Massachusetts Legislature:

- Pass Senate Bill 2722 (conference committee, expected early 2026)

- Budget $15-20M annually for enforcement

- Mandate statewide delivery coverage

- Streamline local approval process

Cannabis Control Commission:

- Implement S.2722 provisions (possession limits, license cap, medical reform)

- Expand delivery licensing

- Coordinate enforcement with State Police

- Maintain testing/quality standards

Timeline: 24-36 months from federal reform enactment to full optimization.

State Comparisons

Massachusetts performs in top tier nationally but federal reform required to reach elite status.

High-Performing Markets (80%+ Legal Share)

Michigan (85% legal share):

- Similar population (10M vs. 7M)

- Lower taxes (16% vs. 17%)

- Excellent access density

- Strong enforcement

- Why Michigan leads: Competitive pricing through supply abundance, efficient regulation, moderate enforcement

- Massachusetts could match Michigan with 280E elimination

Nevada (75-80% legal share):

- Tourism-driven market

- Moderate taxes (22%)

- Las Vegas concentration

- Strong enforcement

- Why Nevada succeeds: Access density in Vegas metro, tourism capture, enforcement

- Massachusetts suburban/urban density rivals Nevada's Vegas concentration

Colorado (73-78% current, 84-88% with federal reform):

- Most mature market (11+ years)

- Moderate taxes (15%)

- Strong initial performance degraded by 280E

- Why Colorado would improve: 280E elimination alone would add 10+ pp

- Massachusetts follows similar trajectory—strong start, federal handicap limiting optimization

Mid-Tier Markets (50-75% Legal Share)

Illinois (55-60% legal share):

- High taxes (25-40%)

- Limited access (license scarcity)

- Why Illinois struggles: Price uncompetitive, insufficient retail coverage

- Massachusetts significantly outperforms Illinois through better pricing and access

Washington (60-65% legal share):

- Early success fading

- Enforcement deprioritized

- Illicit market recovering

- Why Washington declined: Enforcement reduction allowed illicit competition to resurge

- Massachusetts must avoid this mistake

Struggling Markets (30-50% Legal Share)

California (50% legal share):

- High taxes

- 61% local retail bans

- Weak enforcement

- Why California fails: Fragmentation, price uncompetitive, enforcement failure

- Massachusetts avoids California's mistakes through better policy

New York (30% legal share):

- Licensing dysfunction

- Enforcement collapse

- Illicit market dominance

- Why New York catastrophic: Policy failure across all dimensions

- Massachusetts demonstrates how to legalize successfully

Massachusetts Position

Massachusetts ranks among top-performing U.S. markets (75-80% legal share), comparable to Michigan and Nevada, significantly ahead of Illinois and Washington. With federal reform, Massachusetts could reach 82-88% legal share, joining the elite tier.

Regional Competition

Neighboring state impact:

Lost tourism (as states legalized):

- Rhode Island: ~$50-80M annual loss

- Connecticut: ~$30-50M annual loss

- Vermont: ~$10-20M annual loss

Gained/retained tourism:

- New York: ~$40-60M annual gain (NYC area dysfunction)

- New Hampshire: ~$80-120M annually (no program)

- Maine: Neutral (reciprocal tourism)

Net effect: Neutral to +$20-50M. However, competitive pressure forced Massachusetts prices down 68%—beneficial for legal market share, painful for business profitability.

Strategic position: Massachusetts maintains regional advantage through mature regulatory framework, established brand recognition, quality reputation, and strong infrastructure.

Timeline and Path Forward

Massachusetts' optimization timeline depends primarily on federal action.

Short-Term (2025-2027): Federal Reform Window

Without federal reform:

- Legal market: $1.7-1.85B annually

- Legal share: 75-80% (maintained)

- Continued price pressure, business consolidation

- Medical market further decline without S.2722 passage

With federal reform (Schedule III + SAFE Banking):

- Legal market: Begins growth toward $2.0-2.1B

- Legal share: Improves to 78-82% within 18 months

- Business sustainability improves dramatically

- Independent operators stabilize

Probability: Schedule III rescheduling 60-70% likely by 2027, SAFE Banking 40-50% likely

State action: Pass Senate Bill 2722 (early 2026 expected)

Medium-Term (2027-2030): Optimization Implementation

Assuming federal reform achieved:

- State implements delivery expansion

- Enforcement resources modestly increased

- S.2722 provisions fully implemented (possession, licenses, medical reform)

- Legal share: 82-85% by 2030

- Legal market: $2.1-2.3B annually

- Illicit market: Reduced to $240-320M (down from $380-500M)

Economic impact:

- Additional sales: $300-450M annually vs. current

- Additional tax revenue: $51-77M annually

- Jobs: 22,000-26,000 (from current ~20,000)

Long-Term (2030+): Mature Optimized Market

Full optimization:

- Legal share: 85-88%

- Legal market: $2.25-2.4B annually

- Massachusetts establishes model New England market

- Illicit market: $180-240M (residual, <15% share)

Massachusetts position: Among nation's elite markets, comparable to:

- Michigan (85%)

- Nevada (80%)

- Post-reform Colorado (84-88%)

Conclusion: The Pioneer's Challenge

Massachusetts succeeded where many states failed—building functional, successful legal cannabis market capturing 75-80% market share, generating $1.86 billion in legal sales, creating 20,000+ jobs, and funding critical public programs with $280-300M annual tax revenue.

Yet this success operates under structural handicap. Section 280E forces businesses to choose between sustainable margins (requiring higher prices) or competitive pricing (requiring unsustainable losses). Cash-only operations increase security costs and consumer friction. The price collapse to $4.40/gram reflects businesses choosing market share over profitability—a race to the bottom that benefits consumers short-term but threatens long-term sustainability.

The CBDT Framework reveals untapped potential: WITH federal reform, Massachusetts could capture 82-88% legal market share, adding $370-520M in annual sales while reducing illicit market by 53-60%. This isn't theoretical—it's mathematical outcome of eliminating federal barriers that prevent price optimization and business sustainability.

Massachusetts' congressional delegation has unique opportunity: leverage Massachusetts' success to demonstrate why federal reform matters. The Commonwealth proves cannabis legalization works when implemented competently. Federal barriers prevent good policy from achieving excellence.

For Massachusetts policymakers:

- Pass Senate Bill 2722 (possession limits, license cap, medical reform)

- Expand statewide delivery infrastructure

- Modestly increase enforcement targeting large illicit operations

- Advocate aggressively for federal reform

- Maintain regulatory excellence

For Massachusetts businesses: Survive through consolidation or capital infusion until federal reform arrives. Price collapse painful but temporary—federal reform enables sustainable business models.

For Massachusetts consumers: Enjoy low prices ($4.40/gram). Federal reform enables sustainability without sacrificing competitiveness.

For the nation: Massachusetts demonstrates the pioneer advantage—seven years of operation, mature infrastructure, lessons learned from mistakes, optimization framework proven. Other states should study Massachusetts' successes (testing, social equity, access density) and avoid its challenges (medical market dysfunction, 280E impact).

The Bay State isn't just a cannabis market—it's a laboratory demonstrating what American cannabis policy could be with proper federal framework. Massachusetts has built the foundation. Federal reform provides the finishing touch, enabling Massachusetts to join Michigan, Nevada, and reformed Colorado in the elite tier of U.S. cannabis markets.

The question isn't whether Massachusetts has succeeded—clearly it has. The question is: When will federal policymakers enable the Commonwealth to reach its full potential?

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Arizona | Nebraska | Florida | Washington DC

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0