Michigan Cannabis Market Analysis: The Great Lakes State's Success Story Faces Its Greatest Test

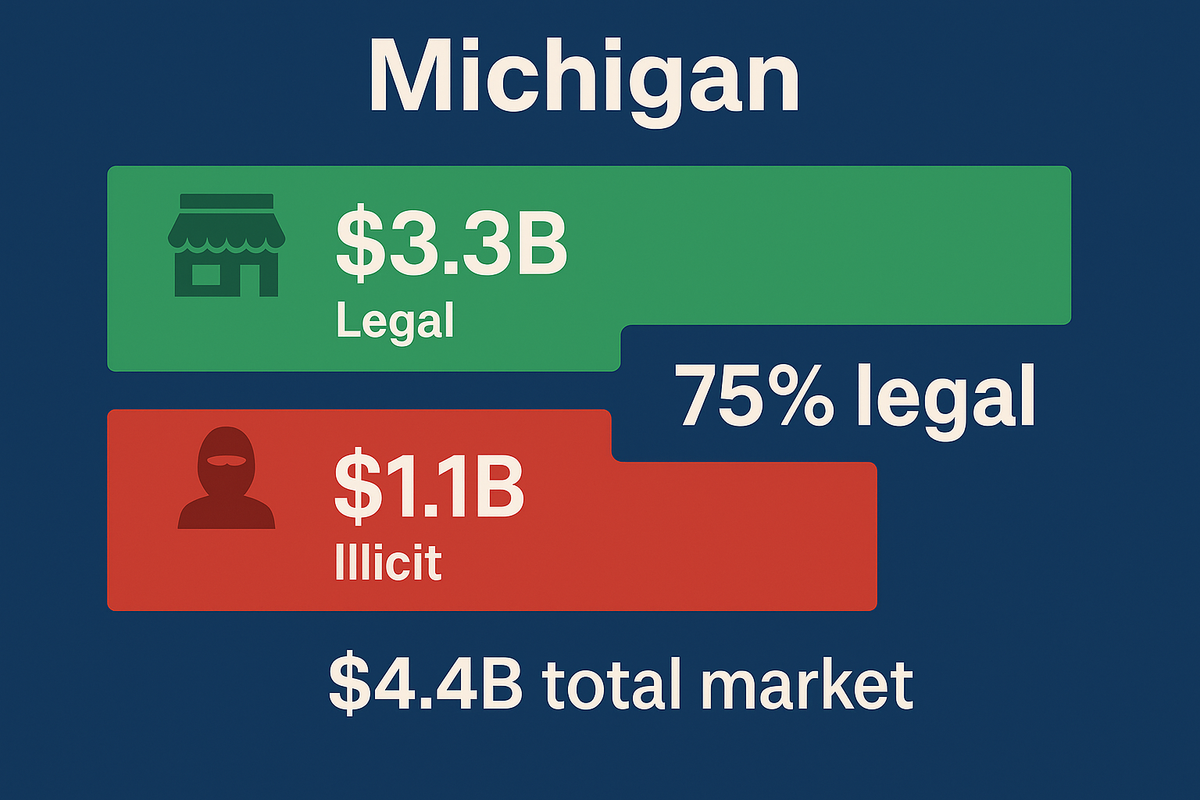

Is weed legal in Michigan? Yes. Adults 21+ can possess 2.5 ounces publicly and 10 ounces at home. Michigan allows 12 plants per household for personal cultivation—the most generous home grow provision in any non-Alaska state. The state operates 851 licensed dispensaries (8.5 per 100,000 residents) with statewide delivery available. Michigan's legal cannabis market captured an estimated 85% of total consumption in 2024—the highest legal market share in the continental United States alongside Nevada.

Yet this remarkable success story faces an existential threat: a 24% wholesale cannabis tax taking effect January 1, 2026. Combined with Michigan's existing 10% excise and 6% sales taxes, this new levy pushes the total effective tax burden to 40%—matching the failed high-tax regimes of California and Washington that drove consumers back to illicit markets. Michigan spent six years building America's most functional legal cannabis market. The question is whether policymakers will destroy it through short-sighted overtaxation.

Note: This article analyzes Michigan's current cannabis market structure and performance. A separate comprehensive analysis of House Bill 4951 (the 24% wholesale tax) and its projected impact on legal market share will be published shortly. HB 4951 represents the single greatest policy threat to Michigan's cannabis market since legalization—we'll examine exactly why in that dedicated analysis.

Framework Validation: The CBDT Model

This analysis uses the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error and r=0.968 correlation. The framework models legal market share as a function of five weighted variables:

- Price Gap (4× weight): Legal-to-illicit price differential

- Access (1× weight): Dispensary density, delivery availability, geographic coverage

- Safety/Quality (1.2× weight): Testing standards, product regulation, consumer trust

- Convenience (1× weight): Purchase limits, payment options, operating hours

- Enforcement (0.6× weight): Illicit market interdiction, penalty structures

Michigan's estimated 85% legal market share ranks as the model's most successful performance alongside Nevada (78-85%). The framework predicts Michigan could achieve 90-95% legal share with federal tax reform (280E repeal, SAFE Banking)—but also predicts a catastrophic decline to 55-65% legal share if the 24% wholesale tax takes effect without offsetting federal reforms.

Validation data: Harvard Dataverse (DOI: 10.7910/DVN/MDVDTQ)

Michigan's Launch: What Went Spectacularly Right

Michigan voters approved Proposal 1 in November 2018 with 56% support, legalizing adult-use cannabis and making Michigan the first Midwestern state to do so. Adult-use sales began December 1, 2019. Six years later, Michigan operates the second-largest cannabis market in the United States (after California) and the most successful by nearly every quality metric.

2024 Performance: Record-Breaking Numbers

Total sales: $3.27 billion (+9.9% from 2023)

- Adult-use: $3.05 billion

- Medical: $220 million (~7% of total market)

Per capita dominance: $328 spent per capita (trailing only Alaska)

- Nearly triple California's $119 per capita

- Double Colorado's $165 per capita

- Demonstrates that policy design—not population size—determines market success

Tax revenue: $314.9 million in cannabis excise taxes (fiscal year 2024)

- 10% excise tax at retail

- 6% sales tax

- Total: 16% tax burden (4th-lowest nationally)

Consumer demand: 1.1+ million pounds of flower sold in 2024 (+17% from 2023)

- August 2024 peak: 100,000 pounds sold in a single month

- December 2024: $264.7 million in sales (single-month record)

- Cumulative since 2019: $12.5+ billion in total sales

Employment: 40,446 licensed cannabis workers (September 2025)

- Direct jobs in cultivation, processing, retail, testing, transportation

- Estimated 60,000-80,000 total jobs including ancillary services

Retail access: 851 adult-use dispensaries across 71 of 83 counties

- Density: 8.5-8.7 dispensaries per 100,000 residents

- Comparison: California 3.2 per 100k, Oregon 16.8 per 100k

- Major metros have excellent coverage (Detroit: 70+ licenses, Grand Rapids: 40+, Ann Arbor: 15+)

The Four Pillars of Michigan's Success

Michigan's remarkable performance stems from policy choices that early-legalizing states failed to implement:

Pillar 1: Low Tax Burden Michigan's 16% total tax burden (10% excise + 6% sales) sits in the research-validated "sweet spot" of 12-18% that maximizes both legal market share and tax revenue. Unlike California (30%+ total), Washington (37%+), or Illinois (40%+), Michigan kept taxes competitive with illicit prices.

Research consistently shows every 5-point tax increase reduces legal market share by 2-3 percentage points. Michigan's moderate 16% rate enabled the state to capture 85% of consumption—triple California's 28% legal share despite California having 4× Michigan's population.

Pillar 2: Abundant Retail Access Michigan's Cannabis Regulatory Agency (CRA) cannot limit license issuance—if applicants meet state and local requirements, they receive approval. This unlimited licensing created abundant retail access:

- 851 dispensaries statewide (vs. California's ~1,300 for 4× the population)

- Present in 71 of 83 counties

- Consumers rarely drive more than 15-20 minutes to reach legal dispensary

- Statewide delivery legal (cannot be prohibited by municipalities)

When legal cannabis is more accessible than calling a dealer, consumers overwhelmingly choose legal—even at slightly higher prices.

Pillar 3: Permissive Home Cultivation Michigan allows 12 plants per household for personal cultivation—tied with Alaska for the nation's most generous home grow provision. This extends the legal market's reach to consumers who prefer growing and creates a safety valve during price spikes or supply disruptions.

Home cultivation is often dismissed as "cannibalizing" retail sales, but this misunderstands market dynamics. Home growers typically still purchase from dispensaries (convenience, variety, concentrates/edibles) and would otherwise buy illicit if retail prices exceeded their willingness to pay. Michigan's generous limit represents progressive policy that prioritizes legal market dominance over short-term revenue maximization.

Pillar 4: Statewide Delivery Michigan's MRTMA explicitly permits statewide cannabis delivery and prohibits municipalities from banning delivery within their boundaries. This ensures consumers in jurisdictions that ban retail dispensaries (12 of 83 counties) still have legal access.

Delivery requirements:

- Licensed retailer must hold delivery endorsement

- Deliveries only to residential addresses

- Customer must be 21+ with valid ID at delivery

- 2.5 oz daily purchase limit applies

- Cash payment required (no card processing due to federal banking restrictions)

Combined, these four pillars created the ideal environment for legal cannabis to dominate: low taxes, abundant access, permissive home cultivation, and guaranteed statewide delivery.

Legal Market Share: 85% and Rising

The CBDT Framework estimates Michigan captures 85% of total cannabis consumption—the highest legal market share in the continental United States. This estimate derives from:

Sales velocity analysis: $3.27B legal sales ÷ $328 per capita = approximately 10 million consumers × average consumption rates = estimated total market of $3.85B, suggesting 85% legal share

Price competitiveness: Michigan's $63/oz average (September 2025) approaches parity with illicit prices ($50-75/oz depending on quality)

Access density: 8.5 dispensaries per 100k residents provides superior convenience vs. illicit sourcing

Regulatory compliance: High consumer trust in testing (mandatory for all products) and labeling

Enforcement impact: Moderate enforcement against large-scale illicit operators (though inconsistent)

Michigan's 85% legal market share compares favorably to:

- Nevada: 78-85% (comparable, tourism-heavy)

- Colorado: 73-78% (mature market)

- Oregon: 65-70% (oversupply crisis)

- Washington: 60-65% (high taxes)

- California: 28-35% (systemic failure)

- New York: 10-15% (catastrophic failure)

Only Alaska (90%+ estimated) performs better—but Alaska's small population (733,000), limited road access, and unique geography create conditions not replicable elsewhere.

The Michigan Crisis: Four Threats to Dominance

Despite Michigan's remarkable success, four interconnected crises threaten to unravel what smart policy built:

Crisis 1: The Price Collapse Paradox

Michigan's cannabis prices have plummeted 85% in five years:

Price trajectory:

- November 2018 (launch): $419/oz average

- December 2020: $300/oz

- August 2022: $150/oz

- December 2024: $69/oz (all-time low)

- September 2025: $63/oz current average

This price collapse has dual effects:

The good: Consumer welfare dramatically improved. Heavy users who spent $200/week on cannabis now spend $50/week—an extra $7,800 annually in disposable income. Price parity with illicit market drives consumers toward legal (safer, tested, convenient).

The bad: Only 27% of Michigan cannabis operators were profitable in 2024. Another 32% operated at a loss, with the remainder breaking even. When prices fall 85% but operating costs fall only 30-40%, margins evaporate.

The ugly: Business failures accelerating despite record consumer demand:

- TerrAscend (20-store, four-facility operator): Completely exited Michigan in 2025

- PharmaCann: Closed 207,000-sq-ft Warren cultivation facility, laid off 222 workers (January 2025)

- Fluresh LLC: Closed $46M Adrian grow facility (November 2024)—CEO stated "it cost more to grow than I could sell for"

- Multiple smaller operators closed 2024-2025

Crisis 2: The Oversupply Emergency

Michigan's unlimited licensing + favorable growing conditions + entrepreneur enthusiasm = massive oversupply:

Cultivation statistics (June 2024):

- Active plants in cultivation: 3.2+ million

- Retail inventory: 160,000+ pounds awaiting sale

- Fresh-frozen inventory: 1.5 million pounds (+316% year-over-year)

- New grower licenses approved Q1 2025: 28 (despite obvious oversupply)

Wholesale price collapse:

- Fresh-frozen bulk cannabis: $0.08-0.15 per gram (essentially pennies)

- Wholesale flower: $1,042/lb ($65/oz) in March 2025—down 28% year-over-year

- Some bulk transactions under $50/lb reported

This oversupply stems from Michigan's unlimited licensing structure. Unlike limited-license states (Arizona, Illinois, Maryland) that artificially constrain supply, Michigan's CRA cannot deny licenses to qualified applicants. The result: anyone with capital can enter cultivation, creating textbook oversupply.

The problem: Market forces will eventually rebalance supply-demand through business failures, but this "correction" causes severe pain:

- Cultivators lose millions in sunk investments

- Workers lose jobs (hundreds already laid off)

- Social equity operators disproportionately harmed (less capital to sustain losses)

- Consolidation favors well-capitalized MSOs over small operators

Crisis 3: Medical Market Dysfunction

Michigan's medical marijuana program is collapsing:

Patient decline:

- Peak enrollment (2021): 240,000 registered patients

- Current enrollment (2025): ~80,000 patients (-67% decline)

- Trend: Losing 3,000-5,000 patients monthly

Sales decline:

- 2023 medical sales: $320+ million

- 2024 medical sales: $220 million (-31%)

- Medical share of total market: 7% (down from 20%+ in 2020)

Dispensary closures:

- Medical provisioning centers: Declining rapidly

- Many converting to adult-use-only (higher volume, lower compliance burden)

- Only 160 medical provisioning center licenses active vs. 851 adult-use retailers

Why medical is dying: Michigan's medical program faces structural disadvantages vs. adult-use:

- Medical registration requires doctor certification + $40 fee (adult-use requires only ID)

- Medical patients must renew annually (extra friction)

- Medical dispensaries face higher licensing fees ($48,000 annually vs. $6,000 adult-use)

- Adult-use prices now comparable to medical (eliminates medical's historical price advantage)

- Adult-use has better geographic access (851 locations vs. 160 medical)

The sole medical advantage: Tax exemption. Medical patients pay 0% tax vs. adult-use 16% tax burden. For heavy users consuming $200-300/month, this saves $32-48 monthly ($384-576 annually). But many patients find the registration hassle not worth the savings, especially as adult-use prices fell.

Consequences:

- Patients with serious medical needs losing specialized access

- Medical dispensaries closing reduces access for remaining patients

- Industry knowledge about medical cannabis applications deteriorating

- Social stigma persists (fewer people identifying as medical patients)

Crisis 4: House Bill 4951 – The Existential Threat

In October 2025, Michigan lawmakers passed House Bill 4951, imposing a 24% wholesale cannabis excise tax taking effect January 1, 2026. This legislation represents the single greatest policy threat to Michigan's cannabis market since legalization.

The tax structure:

- 24% tax on first sale/transfer from grower/processor to retailer

- Example: Grower sells $1,000 wholesale flower → $240 tax due → Retailer pays $1,240

- Retail price increases 20-30% as wholesale tax passes through to consumers

- Combined with existing 10% excise + 6% sales = 40% effective total tax burden

Legislative process:

- House passage: September 25, 2025 (78-21)

- Senate passage: October 3, 2025 (19-17)—razor-thin margin after intense industry opposition

- Governor Whitmer signature: October 7, 2025

- Effective date: January 1, 2026

Projected revenue: $420.7 million annually for road repairs—but projection assumes legal sales remain constant (they won't)

Constitutional challenge: Michigan Cannabis Industry Association (MiCIA) filed lawsuit alleging HB 4951 violates the voter-approved Michigan Regulation and Taxation of Marihuana Act (MRTMA). MiCIA argues additional cannabis excise taxes require direct MRTMA amendment, not separate legislation. Court hearing scheduled November 26, 2025 in Detroit Court of Claims.

Projected impact: Research across all legal markets shows every 5-point tax increase reduces legal market share by 2-3 percentage points. A 20-point effective tax increase (16% → 40%) would reduce Michigan's legal market share by 8-12 percentage points, dropping from 85% to 73-77% or worse.

California's experience with 30-40% total taxes resulted in capturing only 28% of consumption. Michigan is now replicating California's mistakes after spending six years successfully avoiding them.

Note: A comprehensive analysis of HB 4951's specific provisions, constitutional challenges, CBDT Framework scoring, and projected market impact will be published as a separate article. The magnitude of this policy error demands dedicated examination beyond this general market analysis.

Federal Barriers: The 280E Burden and Banking Crisis

Michigan's state-level policy excellence cannot overcome federal prohibition's structural disadvantages. Two federal barriers impose massive costs on Michigan's legal cannabis industry: Section 280E tax penalties and banking restrictions under federal money laundering laws.

IRC Section 280E: A 40-70% Effective Federal Tax Rate

Section 280E of the Internal Revenue Code prohibits businesses trafficking Schedule I/II controlled substances from deducting ordinary business expenses on federal tax returns. Because cannabis remains Schedule I, Michigan dispensaries cannot deduct:

- Employee salaries and wages

- Rent and utilities

- Marketing and advertising

- Insurance premiums

- Legal and accounting fees

- Delivery vehicle costs

- Security expenses

They can only deduct Cost of Goods Sold (COGS).

Michigan example: A dispensary with $2M annual revenue might face:

- Revenue: $2,000,000

- Cost of goods sold: $800,000

- Operating expenses: $900,000

- Actual profit: $300,000

Without 280E (normal business):

- Taxable income: $300,000

- Federal tax (21%): $63,000

With 280E (current reality):

- Taxable income: $1,200,000 (can't deduct operating expenses)

- Federal tax (21%): $252,000

- Excess tax burden: $189,000 (63% of actual profit)

This isn't marginal—it's existential. Licensed operators are taxed on revenue they don't actually earn, forcing prices 15-20% higher to cover the burden. Meanwhile, illicit dealers face zero federal tax and undercut legal prices.

Michigan's 280E burden: With $3.27B in 2024 sales, Michigan cannabis businesses likely paid approximately $490-655M in federal taxes under 280E—of which $200-300M represents excess burden compared to normal businesses. This quarter-billion dollars couldn't be invested in lower prices, higher wages, better security, or improved technology.

The solution: Cannabis rescheduling to Schedule III (recommended by HHS August 2023, pending DEA action) would eliminate 280E automatically. If rescheduling occurs, Michigan operators see 15-20% cost reduction, legal market share increases 8-12 percentage points, and industry profitability transforms from 27% profitable to 60-70%+ profitable.

Learn more: IRC Section 280E: The Hidden Federal Tax Destroying State Cannabis Markets

SAFE Banking Act: The $300M Annual Cash-Handling Tax

Cannabis businesses cannot access traditional banking services because banks fear federal prosecution for money laundering under the Bank Secrecy Act (BSA), which treats cannabis proceeds as "proceeds from unlawful activity."

Michigan's banking crisis:

- Michigan Attorney General Dana Nessel joined bipartisan coalition (July 2025) calling for SAFER Banking Act passage

- Noted that "21 states collect cannabis tax revenues, but many state agencies have been turned away by financial institutions when attempting to deposit cannabis-related payments"

Cash-heavy operations create:

- Security costs: Armed guards ($50k-80k/year per location), reinforced safes ($20k-50k), armored transport (3-5% of revenue) = 5-10% operating cost burden

- Consumer friction: No credit/debit cards = ATM fees ($3-5 per transaction), reduced basket sizes, lost impulse purchases

- Tax compliance challenges: IRS suspicious of cash businesses, increased audit risk

- Business growth barriers: No commercial loans, lines of credit, or mortgages; expansion requires cash reserves or expensive private equity

- Banking fees (when available): 3-5× higher than normal businesses, constant threat of account closure

Estimated Michigan impact: $300M+ annually in excess costs across 2,200+ licensed businesses

The solution: SAFER Banking Act passed Senate Banking Committee (September 2023, 14-9 bipartisan vote), awaits Senate floor vote. If passed:

- Card payment acceptance becomes standard → 3-5 point increase in legal market share

- Banking fees normalize → 5-10% cost savings

- Commercial credit access → interest rates drop from 12-18% to 6-10%

- Security costs decline → 3-5% cost savings

Combined 280E + SAFER impact: 20-30% cost reduction → legal prices drop 20-30% → legal market share increases 10-15 points → industry stabilizes

Learn more: SAFE Banking Act: The Hidden Costs of Cannabis Banking Prohibition

Schedule III Rescheduling: The Game-Changer

The DEA's proposed reclassification of cannabis from Schedule I to Schedule III (following HHS August 2023 recommendation) would:

- Eliminate 280E automatically (no longer "trafficking in controlled substances")

- Enable institutional investment (cannabis becomes "regulated substance," not "illegal drug")

- Improve insurance access (property/liability insurance at reasonable rates)

- Reduce stigma (federal government acknowledging medical value)

BUT: Schedule III does NOT legalize cannabis federally, does NOT solve banking access (still needs SAFER Act), does NOT enable interstate commerce.

Timeline: DEA administrative hearing process delayed; rescheduling unlikely before mid-2026 at earliest.

Michigan impact when rescheduling occurs:

- Legal market share: 85% → 90-95%

- Industry profitability: 27% profitable → 60-70%+ profitable

- State tax revenue: Increases despite no rate change (larger taxable base)

- Licensed employment: +8,000-12,000 jobs

Learn more: Cannabis Rescheduling to Schedule III: What It Is and What It Isn't

Michigan's Medical Marijuana Program: Managed Decline

Michigan's medical marijuana program, established by voter initiative in 2008, is experiencing systematic collapse as adult-use legalization eliminates the medical program's historical advantages.

Current Program Structure

Patient eligibility: Michigan residents with qualifying conditions certified by physician

- Cancer, glaucoma, HIV/AIDS, hepatitis C

- Amyotrophic lateral sclerosis (ALS)

- Crohn's disease, Alzheimer's disease

- Nail patella syndrome

- Conditions causing chronic pain, severe nausea, seizures, muscle spasms

- PTSD (added 2019)

Registration process:

- Physician certification required

- $40 two-year registry fee (Michigan Department of Health and Human Services)

- Registry identification card issued

- Card must be renewed every two years

Possession limits:

- Registered patients: 2.5 oz usable marijuana (same as adult-use)

- Home cultivation: 12 plants (same as adult-use)

- Monthly purchase limit: 10 oz

Tax benefit:

- Medical marijuana sales: 0% tax

- Adult-use: 16% tax (10% excise + 6% sales)

- Heavy users save $384-576 annually at $200-300 monthly consumption

The Medical Market Collapse

Patient enrollment crisis:

- 2021 peak: 240,000 registered patients

- 2025 current: ~80,000 patients (-67%)

- Decline rate: 3,000-5,000 patients monthly

Sales decline:

- 2023: $320+ million

- 2024: $220 million (-31%)

- 2025 projected: ~$180-200 million

- Medical share of total market: 7% (down from 20%+ in 2020)

Provisioning center closures:

- Active medical dispensaries: ~160 (vs. 851 adult-use)

- Many converting to adult-use-only or closing entirely

- Rural patients losing access to tax-exempt purchases

Why patients are leaving:

- Adult-use convenience: No registration, no physician visit, no renewal hassle

- Geographic access: 851 adult-use locations vs. 160 medical locations

- Price parity: Adult-use prices fell 85%; medical's tax exemption matters less at $63/oz

- Product variety: Adult-use retailers stock more SKUs, newer products

- Social stigma reduced: "Recreational" user vs. "patient" distinction fading

Who remains in medical:

- Heavy users for whom 16% tax exemption justifies registration ($300+ monthly consumption)

- Patients requiring specific CBD ratios unavailable in adult-use market

- Those philosophically committed to medical cannabis identity

- Older adults uncomfortable with "recreational" dispensary environment

Medical Program Recommendations

Immediate stabilization:

- Reduce medical registration fee: $40 → $10 (remove barrier)

- Extend renewal period: 2 years → 3 years (reduce friction)

- Telemedicine certification: Expand access for rural patients

- Higher purchase limits: 2.5 oz → 5 oz (differentiate from adult-use)

Long-term reform:

- Eliminate registration entirely: Tax-exempt purchases via physician letter (no state registry)

- Medical-specific products: Require high-CBD, low-THC products available only via medical pathway

- Insurance coverage: Advocate for medical marijuana insurance reimbursement (requires federal rescheduling)

Accept reality: Michigan's medical program will continue shrinking until federal rescheduling enables medical marijuana to be treated as actual medicine (insurance coverage, physician prescription, pharmacy dispensing). Current medical program serves primarily as tax exemption mechanism for heavy users—not as comprehensive medical treatment pathway.

Regulatory Framework: The Cannabis Regulatory Agency

Michigan's Cannabis Regulatory Agency (CRA) oversees all aspects of cannabis regulation, from licensing to enforcement to data reporting. The CRA's transparent, data-driven approach has been critical to Michigan's success.

Licensing Structure

Cultivation licenses (three classes):

- Class A: Up to 500 plants

- Class B: Up to 1,000 plants

- Class C: Up to 1,500 plants

- License fees: $6,000-18,000 annually depending on class

Processing licenses:

- Standard processor: Concentrate production, edibles manufacturing

- Excess marijuana grower: Processes own harvest only

- License fees: $24,000 annually

Retail licenses:

- Retailer: Adult-use sales only

- Provisioning center: Medical sales only

- Microbusiness: Integrated cultivation (up to 200 plants) + processing + retail

- License fees: $6,000-25,000 annually

Other licenses:

- Safety compliance facility: Testing laboratories

- Secure transporter: Licensed transportation of cannabis products

- Temporary marijuana event: Special event sales

Unlimited issuance: Michigan law prohibits CRA from capping license numbers. If applicants meet state and local requirements, they receive approval. This creates abundant access but contributes to oversupply crisis.

Testing and Safety Standards

Mandatory testing for all products:

- Potency (THC/CBD content)

- Microbial contamination (E. coli, Salmonella, Aspergillus)

- Mycotoxins (aflatoxins, ochratoxin A)

- Heavy metals (arsenic, cadmium, lead, mercury)

- Pesticide residues (Michigan-specific action levels)

- Residual solvents (for concentrates)

Product recalls: CRA publishes public recall notices for products failing safety testing. Transparently builds consumer trust in legal market.

Packaging and labeling requirements:

- Child-resistant packaging mandatory

- Warning labels required

- Potency clearly displayed

- Batch/lot tracking via Metrc system

Social Equity Program

Created under MCL Section 333.27958(1)(j): Promotes participation from communities disproportionately impacted by cannabis prohibition.

Qualification criteria:

- Lived in "disproportionately impacted community" for 5+ consecutive years (past 10 years)

- Low-income status (250% of federal poverty level)

- Prior marijuana-related misdemeanor/felony conviction

- Registered medical marijuana caregiver (2+ years)

Benefits:

- 25% licensing fee discount (residency in impacted community)

- 25% discount (misdemeanor conviction)

- 40% discount (felony conviction)

- 10% discount (caregiver experience)

- Priority review for licenses in high-demand areas

Disproportionately impacted communities: Areas with high marijuana arrest rates and high poverty (20%+ below federal poverty level). Predominantly Detroit, Flint, Pontiac, Saginaw, Battle Creek neighborhoods.

Performance: Social equity program has helped diversify Michigan's cannabis industry, though well-capitalized operators still dominate. Price collapse + oversupply crisis disproportionately harms social equity operators with less capital to sustain losses.

Data Transparency

CRA publishes detailed monthly statistical reports covering:

- Sales by product category (flower, edibles, concentrates, etc.)

- Active licenses by type

- Plants in cultivation

- Retail inventory

- Wholesale and retail prices

- Licensed employees

This data transparency enables evidence-based policymaking and market analysis—a stark contrast to states like California where reliable market data is scarce.

Home Cultivation: Michigan's Hidden Competitive Advantage

Michigan allows 12 plants per household for personal cultivation—tied with Alaska for the nation's most generous home grow provision. This policy extends the legal market's reach and creates a safety valve against price spikes.

Legal Framework

Adult-use home cultivation (MRTMA Section 4):

- Up to 12 plants per household (regardless of number of adults)

- Must be kept in enclosed, locked facility

- Not visible from public view

- Maintain possession limit (10 oz harvested marijuana + all marijuana at harvest site)

Medical home cultivation (MMMA Section 4):

- Registered patients: 12 plants

- Caregivers: 12 plants per patient (up to 5 patients = 60 plants)

- Same security requirements as adult-use

Home Growing Economics

Setup costs:

- Indoor grow tent setup: $800-2,000 (tent, lights, ventilation, pots, medium)

- Outdoor in-ground: $100-300 (seeds, nutrients, pest control)

- Seeds/clones: $50-150 per plant

- Nutrients and supplies: $200-400 per season

Ongoing costs:

- Electricity (indoor): $40-150 monthly depending on lights

- Water: $10-30 monthly

- Nutrients: $20-50 per grow cycle

- Annual cost (indoor): ~$800-2,200

Yield expectations:

- Indoor (4 plants, 3 harvests/year): 300-600 grams annually (10-21 oz)

- Outdoor (12 plants, 1 harvest/year): 1,200-3,600 grams (42-127 oz)

- Cost per ounce home-grown: $10-25 indoor, $5-10 outdoor

Dispensary comparison:

- Retail price: $63/oz average (September 2025)

- Home-grown: $5-25/oz depending on method

- Savings for heavy user (2 oz/month): $888-1,392 annually

Market Impact

Home cultivation affects legal market dynamics in complex ways:

Positive impacts:

- Extends legal market reach to price-sensitive heavy users who would otherwise buy illicit

- Creates cultural normalization (home cultivation = legal/acceptable)

- Provides safety valve during price spikes or supply disruptions

- Home growers become advocates for legal market (vested interest in maintaining legalization)

- Many home growers still purchase from dispensaries (convenience, variety, concentrates/edibles)

Negative impacts:

- Reduces retail sales volume (heavy users substitute home-grown for retail purchases)

- Some home growers divert excess production to illicit market (though 12-plant limit constrains this)

Net assessment: Home cultivation's benefits outweigh costs. Michigan's generous 12-plant limit acknowledges that prohibition failed because consumers want cannabis access—and if legal retail doesn't meet their needs (price/quality/convenience), they'll find alternatives. Better to have consumers growing at home (legal, untaxed) than buying from illicit dealers (illegal, untaxed, unsafe).

Research from Colorado and Oregon (both permit home cultivation) shows legal retail and home growing can coexist successfully. Michigan's experience confirms this: despite generous home grow provisions, Michigan captured 85% legal market share—the highest in the continental U.S.

CBDT Framework Assessment: Current vs. Optimized Michigan

Current Performance (2024-2025): 85% Legal Market Share

Price Gap (4× weight): STRONG (+16 points baseline)

- Legal retail: $63/oz average (September 2025)

- Illicit market: $50-75/oz depending on quality

- Near parity achieved through massive price collapse

- Wholesale tax will destroy this advantage (+12 points after tax, major deterioration)

Access (1× weight): EXCELLENT (+9 points)

- 851 dispensaries (8.5 per 100k residents)

- Present in 71 of 83 counties

- Statewide delivery available

- Most consumers within 15-minute drive of legal retail

Safety/Quality (1.2× weight): STRONG (+10 points)

- Mandatory testing for all products

- Transparent recall system

- Consumer trust high in legal market testing/labeling

Convenience (1× weight): EXCELLENT (+9 points)

- 2.5 oz daily purchase limit (generous)

- 12-plant home cultivation (most permissive outside Alaska)

- Statewide delivery available

- Cash-only payment reduces score (federal banking restrictions)

Enforcement (0.6× weight): MODERATE (+4 points)

- Periodic large-scale bust headlines (August 2024: $10M+ seizure)

- But lacks sustained, strategic enforcement program

- No dedicated cannabis task force or intelligence-led targeting

Total CBDT Score: ~84 points → 85% legal market share

Federal Reform Scenario: 90-95% Legal Market Share

If 280E repealed + SAFER Banking passes:

Price Gap: DOMINANT (+18 points)

- 280E repeal: 15-20% cost reduction

- SAFER Banking: 5-10% cost reduction

- Combined: 20-30% legal price reduction

- Legal retail: $45-50/oz vs. illicit $50-75/oz

- Legal undercuts illicit on price while providing superior quality/convenience

Access: EXCELLENT (+9 points, unchanged)

- Existing dispensary network remains excellent

Safety/Quality: STRONG (+10 points, unchanged)

- Maintains current testing/safety standards

Convenience: EXCELLENT (+9 points, improved)

- Card payment acceptance (+2 points from SAFER Banking)

- Basket sizes increase 15-25%

- Impulse purchases increase

Enforcement: MODERATE-STRONG (+5 points, modest improvement)

- Some illicit operators exit due to lack of profitability

- Remaining illicit market smaller, easier to target

Total CBDT Score: ~92-95 points → 90-95% legal market share

HB 4951 Catastrophe Scenario: 55-65% Legal Market Share

If 24% wholesale tax takes effect without federal reform:

Price Gap: DESTROYED (+8 points, massive deterioration)

- Wholesale tax increases retail prices 20-30%

- Legal retail: $80-90/oz vs. illicit $50-75/oz

- 20-40% price premium for legal

- Illicit market becomes dramatically more competitive

Access: DECLINING (+7 points, deterioration)

- 20-40% of operators close within 18 months

- Dispensary density falls to 5-6 per 100k

- Geographic coverage gaps emerge

Safety/Quality: DECLINING (+8 points, deterioration)

- Some consumers prioritize price over safety

- Trust erodes as tax perceived as government "greed"

Convenience: MODERATE (+7 points, deterioration)

- Reduced basket sizes (customers buying less per trip)

- Some consumers return to delivery illicit sources

Enforcement: MODERATE (+4 points, slightly worse)

- Illicit market grows 30-50%

- Enforcement resources overwhelmed

- Licensed operators diverting product to avoid tax

Total CBDT Score: ~62-68 points → 55-65% legal market share

This would represent a 20-30 point collapse in legal market share—Michigan transforming from America's best legal market to a California-style failure in 12-24 months.

Policy Recommendations: Saving Michigan's Cannabis Market

Michigan stands at a crossroads. The state built America's most successful cannabis market through smart policy—and now risks destroying it through short-sighted tax grabs. Here's what Michigan must do to prevent catastrophe:

Immediate Priority (2025-2026): Stop the Wholesale Tax

Option 1: Full repeal before January 1, 2026

- Optimal outcome: Preserve Michigan's competitive advantage

- Legislature admits mistake, seeks alternative road funding

- Political difficulty: High (requires acknowledging error)

Option 2: Delay implementation 2-3 years

- Allows federal reforms (280E repeal, SAFER Banking) to take effect first

- Federal reforms provide 20-30% cost reduction, offsetting state tax increase

- Gives industry time to stabilize after oversupply crisis resolves

- Political difficulty: Moderate (reframes as "thoughtful phase-in")

Option 3: Reduce rate to 8-12% (not 24%)

- 8-12% wholesale tax = approximately 22-28% total effective burden (vs. 40% at 24% rate)

- Still harmful but not catastrophic

- Research suggests 22-28% total burden reduces legal share 4-6 points (vs. 8-12 points at 40%)

- Political difficulty: Moderate (revenue projections fall short)

Option 4: Sunset clause

- Wholesale tax automatically repeals in 2028 unless Legislature reauthorizes

- Forces reassessment based on actual market impact vs. revenue projections

- Political difficulty: Low (preserves initial revenue while building in safety valve)

Recommended approach: Pursue Option 2 (delay 2-3 years) + Option 4 (sunset clause). This gives federal reforms time to take effect while preserving exit ramp if market damage becomes evident.

Federal Reform Advocacy (2025-2027)

Michigan Congressional Delegation must aggressively push:

- SAFER Banking Act: Senator Peters, Senator Slotkin must co-sponsor and demand Senate floor vote

- 280E repeal through rescheduling: Governor Whitmer use bully pulpit to pressure DEA on cannabis rescheduling

- Attorney General Nessel: Continue leading bipartisan coalitions for federal banking reform

Timeline pressure: Federal reforms likely 2026-2027. If Michigan implements 24% wholesale tax January 2026 while federal reforms remain 12-24 months away, industry sustains 12-24 months of catastrophic damage before relief arrives.

Critical point: Federal reform cannot overcome state-level sabotage. Even with 280E repeal + SAFER Banking (20-30% cost reduction), Michigan's 40% total tax burden would still leave legal cannabis more expensive than illicit alternatives.

Industry Stabilization (2025-2026)

Immediate relief for struggling operators:

- Emergency relief fund from existing cannabis tax revenue

- Temporary 50% reduction in licensing fees for 2026

- Payment plans for operators behind on taxes

- Fast-track license renewals (reduce bureaucratic friction)

Address oversupply:

- Six-month licensing moratorium on new grower licenses (allow supply-demand rebalancing)

- Price floor for wholesale transactions (prevents predatory pricing by well-capitalized operators)

- Interstate commerce preparation (position Michigan as export leader post-federal legalization)

Social equity support:

- Grant funding for social equity operators (from existing tax revenue)

- Technical assistance for business planning, compliance, financial management

- Prioritize social equity operators in high-demand license categories

Long-Term Optimization (2027-2030)

Optimal tax structure:

- Total tax burden: 12-15% (excise + sales + local)

- Current 16% was sustainable

- Post-federal-reform optimal: 12-15% maximizes both legal market share AND total tax revenue

- Research consistently shows 12-18% sweet spot

Licensing reform:

- Implement tiered licensing fees based on revenue (small operators pay less)

- Consider limited caps in oversaturated categories (prevent repeat oversupply crises)

- Maintain unlimited retail licensing (prioritize consumer access)

Enhanced enforcement:

- Establish dedicated cannabis enforcement task force ($30-50M annual budget)

- Intelligence-led targeting of high-value illicit operations

- Interstate trafficking focus (Michigan → non-legal states)

- Federal coordination (DEA, U.S. Attorneys)

Interstate commerce readiness:

- Post-federal legalization, Michigan positioned as major exporter

- Low production costs + oversupply = competitive advantage in national market

- Develop quality/safety standards exceeding federal minimums (premium branding)

The Optimized Michigan: 90-95% Legal Market Share

With federal reform + reasonable state policy, Michigan can achieve 90-95% legal market share by 2028-2030:

Market impact:

- Legal market: $4.2-4.8B annually (vs. current $3.27B)

- State tax revenue: $630-720M annually at 15% rate (double current revenue despite lower rate)

- Licensed employment: 55,000-65,000 jobs (vs. current 40,446)

- Retail prices: $45-55/oz (lower than current $63/oz)

- Illicit market: 5-10% residual (contained, manageable)

Path requires:

- Federal 280E repeal + SAFER Banking = +8-10 points legal share

- Prevent/repeal wholesale tax = maintain price competitiveness

- Enhanced enforcement = +1-2 points

Michigan already came 85% of the way. The remaining 5-10 points requires federal cooperation and state-level discipline to avoid self-inflicted wounds.

State Comparisons: Michigan vs. Other Legal Markets

| State | Legal Share | Per Capita | Tax Burden | Dispensaries/100k | Home Grow |

|---|---|---|---|---|---|

| Michigan | 85% | $328 | 16% (rising to 40%) | 8.5 | 12 plants |

| Nevada | 78-85% | $441 | 24% | 7.2 | 6 plants (med only) |

| Colorado | 73-78% | $165 | ~15% | 6.1 | 6 plants (12 med) |

| Oregon | 65-70% | $137 | ~17% | 16.8 | 4 plants |

| Washington | 60-65% | $154 | 37% | 4.8 | Prohibited |

| Massachusetts | 75-80% | $243 | 17-20% | 10.2 | 6 plants (12 med) |

| Illinois | 55-60% | $86 | 40% | 1.9 | Prohibited |

| California | 28-35% | $119 | 30-40% | 3.2 | 6 plants |

| New York | 10-15% | $12 | 13% | 0.8 | 3 plants (6 med) |

Key insights:

Michigan's current advantages:

- Highest per capita sales (excluding Nevada tourism)

- Highest legal market share (tied with Nevada)

- Moderate tax burden (16% competitive)

- Strong dispensary density (8.5 per 100k)

- Most generous home grow (12 plants)

Michigan's threats:

- Tax burden rising to 40% (would match California/Illinois failures)

- Oversupply crisis worse than Oregon

- Medical market decline steeper than Colorado

Peer performance:

- Nevada (78-85% legal share): Higher taxes (24%) but offset by tourism, fewer home growers

- Colorado (73-78% legal share): Lower taxes (15%), mature market, stable

- Oregon (65-70% legal share): Oversupply crisis similar to Michigan, but sustained lower taxes

- California (28-35% legal share): High taxes (30-40%), limited access, massive illicit market—Michigan's future if HB 4951 not reversed

Michigan risks California-style collapse unless HB 4951 repealed/delayed/reduced. California's experience proves high taxes + abundant illicit supply = legal market failure.

Timeline and Path Forward

Near-Term (2025-2026): Crisis Management

January 1, 2026: 24% wholesale tax takes effect (if not delayed/repealed)—retail prices increase 20-30%, consumer backlash begins, illicit market gains share

Q1-Q2 2026: Business closures accelerate, state tax revenue disappoints vs. projections, legal market share drops 5-8 points (85% → 77-80%), federal SAFER Banking vote likely

Mid-2026: Federal rescheduling possible (Schedule III), 280E burden eliminated if rescheduling occurs

Mid-Term (2026-2028): Stabilization or Collapse

Scenario A - Policy Correction: Legislature repeals/reduces wholesale tax, federal reforms take effect (280E + SAFER), legal market stabilizes at 88-90% share

Scenario B - Catastrophic Failure: Wholesale tax remains at 24%, federal reforms delayed, legal market collapses to 65-70% share, Michigan becomes California 2.0

Key variable: Whether federal reforms arrive before Michigan's legal market sustains irreversible damage

Long-Term (2028-2030): Optimization or Aftermath

Optimized path: 90-95% legal share, $4.2-4.8B market, $630-720M tax revenue, 55,000-65,000 jobs, national model

Failure path: 65-70% legal share, $2.5-3.0B market, $400-500M tax revenue, 25,000-30,000 jobs, cautionary tale

The choice is Michigan's.

Conclusion: Don't California Our Michigan

Michigan built America's most successful cannabis market by learning from the failures of early-legalizing states. While California implemented high taxes, limited access, and hostile local control, Michigan chose low taxes, abundant licenses, and permissive home cultivation. The result: Michigan captures 85% of cannabis consumption while California captures only 28%.

This isn't theoretical—it's empirical. Michigan demonstrates that sensible policy creates functional legal cannabis markets. Michigan's per capita sales ($328) nearly triple California's ($119) despite California's supposed advantages (larger population, longer legalization history, established cannabis culture). Policy design, not market characteristics, determines success.

Yet Michigan now risks squandering this success through the 24% wholesale cannabis tax taking effect January 1, 2026. This tax transforms Michigan's competitive 16% total burden into a California-matching 40% burden. Research across all legal markets shows every 5-point tax increase reduces legal market share by 2-3 percentage points. A 20-point increase would devastate Michigan's legal market, dropping legal share from 85% to potentially 55-65%—a catastrophic collapse that would cost Michigan:

- $500M-800M in lost legal sales annually

- $200M-300M in foregone tax revenue (despite higher rates, smaller base yields less)

- 15,000-20,000 licensed jobs eliminated

- Resurgent illicit market capturing 35-45% of consumption

- Consumer safety compromised (untested products, unregulated potency)

All this to fund roads with revenue that may never materialize.

The alternative is straightforward: Repeal or delay the wholesale tax, advocate for federal reform (280E repeal, SAFER Banking), and maintain Michigan's competitive advantage until federal relief arrives. Federal reforms would provide the 20-30% cost reduction needed to offset state tax increases—but those reforms are 12-24 months away. Implementing the wholesale tax now, before federal relief arrives, inflicts 12-24 months of catastrophic damage the industry may not survive.

Michigan's path forward requires three commitments:

1. State-level discipline: Repeal/delay/reduce the wholesale tax. Maintain competitive tax burden until federal reforms take effect.

2. Federal reform advocacy: Michigan Congressional Delegation must aggressively push SAFER Banking Act and support DEA rescheduling. Attorney General Nessel and Governor Whitmer must use their platforms to demand federal action.

3. Strategic enforcement: Establish dedicated cannabis task force targeting high-value illicit operations. Enforcement alone won't win, but absence of enforcement guarantees failure.

These three commitments would position Michigan to achieve 90-95% legal market share by 2030—the highest in the nation, a genuine elimination of the illicit market, and validation that prohibition's replacement with regulated markets can succeed.

Or Michigan can implement the 24% wholesale tax, watch its legal market collapse California-style, and become the cautionary tale other states cite when explaining why cannabis legalization "doesn't work."

The choice is binary. The consequences are permanent. The time to act is now.

Michigan voters legalized cannabis in 2018 expecting a well-regulated, taxed, and safe market. They got the most successful legal cannabis market in America. Political leaders must decide whether to protect this success—or squander it for short-term road funding that high taxes may never deliver.

As Michigan Senator Jeff Irwin warned when voting against the wholesale tax: "This is truly a great day for illegal drug dealers and criminal gangs in Michigan."

Don't California our Michigan.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Wyoming | Texas | Ohio | Vermont | Florida

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0