Minnesota Cannabis Market Analysis: The North Star State's Tribal-Led Launch and the Federal Reforms That Will Determine Success

Is weed legal in Minnesota? YES. Minnesota legalized adult-use cannabis on August 1, 2023, becoming the 23rd state to do so. Adults 21+ can possess 2 ounces of cannabis flower publicly (2 pounds at home), grow 8 plants (4 flowering maximum), and purchase from licensed dispensaries starting September 2025.

Minnesota made history not just through legalization but through unprecedented tribal-state partnerships enabling sovereign nations to supply the legal market. The state's Office of Cannabis Management (OCM) issued licenses to 150+ cannabis retailers by November 2025, though only 15-20 operate currently. The

market launched just weeks ago—too new for meaningful sales data, but policy foundations are strong.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Minnesota's trajectory: 62-68% legal market share currently (strong early performance), with potential for 78-85% within 36-48 months if federal reforms pass. Without federal support, Minnesota risks plateauing at 55-62%—underperforming Michigan by 20+ percentage points despite innovative policy design.

Minnesota's tribal compact model works. Federal policy determines whether it succeeds or fails.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Minnesota's Legal Framework: HF 100 and the 840-Day Delay

Governor Tim Walz signed HF 100 into law on May 30, 2023, making Minnesota the 23rd state to legalize adult-use cannabis. The law took effect August 1, 2023—but retail sales didn't begin until September 16-17, 2025. That's an 840-day delay between legalization and retail launch, the longest in U.S. history.

The delay wasn't dysfunction—it was deliberate caution. Minnesota's Office of Cannabis Management prioritized getting policy right over speed, learning from California's chaos and New York's disaster.

What Minnesota got right:

- Rigorous testing standards (comprehensive safety/quality requirements)

- METRC seed-to-sale tracking (inventory reconciliation, supply chain monitoring)

- Tribal-state compacts (sovereign nations as market participants and suppliers)

- Social equity framework (50% of retail licenses reserved, $12M business development fund)

- Automatic expungement (cannabis convictions up to 2 pounds eligible)

The cost of caution: During 26 months between legalization and retail, consumers continued sourcing from dealers, home cultivation, or Michigan dispensaries. The illicit market that legalization aimed to eliminate instead adapted and persisted. Border crossings to Michigan normalized—particularly from Duluth (2 hours) and northeastern Minnesota.

Current Minnesota cannabis laws:

| Category | Limit |

|---|---|

| Public possession | 2 oz flower, 8g concentrate, 800mg edibles |

| Private possession | 2 lbs flower at home |

| Home cultivation | 8 plants (4 flowering max), enclosed/locked, not public view |

| Purchase age | 21+ years old |

| Consumption locations | Private residences, licensed consumption areas |

| Driving limits | DUI illegal, open container prohibited |

Tax structure:

- State excise: 15% (raised from 10% in June 2025—BEFORE sales began)

- State sales: 6.875%

- Local sales: 0.5-1.5% varies

- Total burden: 22-23% effective

- Medical cannabis: Tax-exempt

Minnesota's cannabis tax structure increased from 10% to 15% effective July 1, 2025. The 15% excise tax represents a 50% increase from the original 10% rate. Minnesota lawmakers raised taxes pre-emptively before the market launched—giving the illicit market a pricing advantage from day one. This was a fiscal decision (revenue need), not an optimization decision (market analysis).

Current Market Performance: Strong Start, Federal Handicaps

Minnesota's cannabis market is weeks old. Traditional metrics don't exist—no monthly sales data, no pricing equilibrium, no mature supply chain. What exists is framework: Policy architecture, regulatory structure, licensing approvals, and initial signals.

Those signals reveal: Minnesota designed policy well but cannot escape federal burden.

Retail Infrastructure: Limited but Growing

Current operational dispensaries (November 2025):

- Green Goods (Vireo Health): 8 locations statewide

- RISE Dispensaries (Green Thumb Industries): 8 locations statewide

- Legacy Cannabis (Duluth): First microbusiness retailer

- Tribal dispensaries: NativeCare (Red Lake Nation), Lake Leaf (Mille Lacs Band), Waabigwan Mashkiki (White Earth Nation), others

- Total operational: ~15-20 dispensaries for 5.7 million residents

Dispensary density: 0.26-0.35 stores per 100,000 population

Comparison:

- Oregon: 16.8 per 100,000 (oversaturated)

- Colorado: 10+ per 100,000 (mature)

- Michigan: 8-10 per 100,000 (growing)

- Illinois: 1.9 per 100,000 (underserved)

- Minnesota: 0.26-0.35 per 100,000 (nascent)

Minnesota's access density is exceptionally low—not by design failure but by timing. The state issued licenses to 160+ businesses: 25 cultivators, 24 manufacturers, 150 retailers, plus mezzobusinesses and microbusinesses. Most remain non-operational, awaiting facility buildout, capital, supply chain maturation, and METRC integration.

Expected trajectory:

- Mid-2026: 40-60 operational dispensaries

- End-2026: 80-120 operational dispensaries

- 2027-2028: 150-180 operational dispensaries (mature market)

Geographic concentration: Twin Cities metro (Minneapolis-St. Paul) contains 60% of state population and will host 65-70% of initial retail. Duluth, Rochester, St. Cloud, Mankato follow. Tribal dispensaries fill rural gaps but face accessibility challenges for non-reservation residents.

Pricing Reality: The Michigan Problem

Early retail prices (September-October 2025 observations):

- Flower (1/8 oz): $40-50 ($11-14 per gram)

- Pre-rolls (1g): $12-15

- Concentrates: $50-70 per gram

- Edibles (100mg THC): $20-30

Comparison to other markets:

- Illinois: $28-32 average

- Washington: $24-28 average

- Colorado: $14-18 average

- Michigan: $18-22 average

- Minnesota: $22-28 estimated average

Minnesota's prices fall mid-to-high range—not catastrophic like Illinois but significantly above Michigan, the key border competitor.

The Michigan border problem:

Michigan is 4 hours from Twin Cities, 2 hours from Duluth. Minnesota legal cannabis at $40-50 per eighth competes with Michigan legal cannabis at $45-80 per ounce. That's a 400-500% price differential.

Border arbitrage math:

- Round-trip gas to Michigan: $30-50

- Savings on ounce: $120-180

- Rational economic behavior for price-sensitive consumers

Industry observers note thousands of Minnesotans cross to Michigan daily to purchase cannabis. That's $40-70M annually in Minnesota sales captured by Michigan due to price differential and Michigan's 4-year regulatory head start.

Illicit pricing (triangulated estimate):

- Mid-tier flower: $8-10/gram ($220-280/oz)

- High-quality flower: $10-12/gram ($280-340/oz)

- Concentrates: $25-35/gram

Legal vs. illicit differential: 35-55% premium for legal cannabis.

The framework shows legal markets succeed when price premiums stay below 20%. Minnesota's 35-55% premium ensures persistent black market demand—especially among heavy users (20% of consumers, 80% of volume) who are most price-sensitive.

Why are Minnesota cannabis prices high?

Internal Revenue Code Section 280E prevents cannabis businesses from deducting normal operating expenses. Minnesota dispensaries cannot deduct rent, utilities, employee salaries, marketing, insurance, security—only Cost of Goods Sold. This creates an effective 40-70% federal tax rate, forcing retail prices 15-20% higher than economically necessary.

Minnesota decoupled from 280E for state taxes, allowing normal deductions on Minnesota income tax returns. This helps with Minnesota's 9.8% corporate rate but does nothing about the 40-70% federal burden.

Federal 280E overwhelms state-level policy relief.

The Tax Increase That Shouldn't Have Happened

Minnesota raised its cannabis excise tax from 10% to 15% (50% increase) effective July 1, 2025—before retail sales even began.

This was fiscal opportunism, not market optimization. Legislators wanted revenue. They got short-term gain at long-term cost: The rate increase added $2-4 to average item prices, widening the gap between legal and illicit.

The framework shows: Revenue optimization comes through volume (market share) not rates. Michigan generates more per-capita cannabis revenue than Minnesota will despite lower tax rates because Michigan captures 85% market share vs. Minnesota's projected 62-68%.

Minnesota should reduce the rate to 12% once the market matures. Current 15% rate is defensible during launch scarcity but becomes problematic as supply increases and competition with illicit markets intensifies.

Minnesota's Tribal Partnership Model: The Critical Innovation

Minnesota's defining characteristic: Tribal-state compacts enabling sovereign nations to supply the legal market.

As of November 2025, Minnesota has signed compacts with five tribal nations:

- White Earth Nation (May 2025): First off-reservation compact, 50,000 sq ft cultivation facility

- Mille Lacs Band of Ojibwe (Sept 2025): 50,000 sq ft grow facility, Lake Leaf dispensaries

- Prairie Island Indian Community (Oct 2025): Wholesale operations planned

- Fond du Lac Band of Lake Superior Chippewa (Oct 2025): ANANG Native Cannabis Co.

- Leech Lake Band of Ojibwe (Oct 2025): Most recent compact

Why compacts matter:

Minnesota's licensing law required in-state cultivation only—preventing established growers from importing product. This created a supply bottleneck: New cultivators need 4-6 months from licensing to first harvest. Traditional licensees couldn't supply retail opening.

Tribal nations solved the problem.

Tribes began cultivation immediately after August 2023 legalization under their sovereignty, unencumbered by state licensing delays. By September 2025, tribal facilities had mature harvests ready for wholesale.

Legacy Cannabis in Duluth became the first state-licensed retailer to sell tribally grown cannabis flower on September 16, 2025, sourcing from White Earth Nation.

Without tribal supply: Minnesota's retail launch would have failed. Dispensaries would open to empty shelves. The state would repeat New York's disaster: Licenses issued, nothing to sell, illicit market thriving.

With tribal supply: Minnesota achieved viable retail launch with product availability from day one. Tribal cultivators are scaling rapidly to meet growing demand as more dispensaries come online.

Economic impact:

Tribal cannabis operations generate:

- Jobs in high-unemployment reservation communities

- Diversified revenue beyond gaming

- Capital for infrastructure, healthcare, education investment

- Proof-of-concept for tribal enterprise in emerging industries

The compact model works economically and politically:

- Tribes benefit from early market entry advantage

- State benefits from supply chain stability

- Consumers benefit from product availability

- Federal reform model: Gaming compacts work, cannabis compacts should too

Minnesota's innovation: Treating tribal nations as equal partners rather than obstacles.

What Minnesota Got Right: Policy Foundations for Success

Minnesota learned from predecessor states' mistakes. Several policy choices position the state for success.

Comprehensive Regulatory Structure

Minnesota copied Colorado's seed-to-sale tracking and Oregon's testing standards while avoiding California's fragmentation:

Licensing categories:

- Cannabis cultivators (25 licensed)

- Cannabis manufacturers (24 licensed)

- Cannabis retailers (150 licensed)

- Mezzobusinesses (vertically integrated medium-scale)

- Cannabis microbusinesses (small-scale, social equity-focused)

- Testing laboratories (multiple pending)

- Cannabis transporters

METRC seed-to-sale tracking: Mandatory inventory reconciliation, real-time state access to all transaction data, comprehensive supply chain monitoring from cultivation through retail sale.

Testing requirements:

- Potency testing (THC, CBD, minor cannabinoids)

- Pesticide screening (comprehensive panel)

- Heavy metals testing (lead, arsenic, cadmium, mercury)

- Microbial contaminant testing (E. coli, Salmonella, Aspergillus)

- Mycotoxin testing (aflatoxins)

- Residual solvents testing (for concentrates)

Minnesota's testing standards meet or exceed most established markets. Quality advantage over illicit market is clear and significant.

Minimal Geographic Fragmentation

Unlike California (61% of jurisdictions ban retail), Minnesota state law limits local prohibitions:

Municipal authority:

- Cities can limit dispensary density (one per 12,500 residents minimum)

- Cities can regulate zoning and hours of operation

- Cities cannot prohibit licensed dispensaries outright (with narrow exceptions)

Result: Geographic access gaps will be minimal. Minnesota avoided California's fragmentation disaster through state preemption of most local bans.

Expected final density: 2.5-3.5 dispensaries per 100,000 residents statewide once market matures (150-200 total for 5.7M population).

Social Equity Framework (Strong Foundations)

Minnesota embedded social equity into licensing from day one:

- 50% of retail licenses reserved for social equity applicants (75 out of 150 total)

- Cannabis Business Development Fund: $12 million for loans and technical assistance

- Automatic expungement: Cannabis convictions up to 2 pounds eligible

- Microbusiness licensing: Lower barriers, smaller operations, social equity-focused

Early results: As of November 2025, several social equity licensees have received approval. Legacy Cannabis in Duluth represents successful micro-business launch. But capital access remains the defining challenge—a problem requiring federal SAFE Banking Act passage to solve.

Home Cultivation Rights

Minnesota allows adults 21+ to cultivate 8 cannabis plants per residence, with maximum 4 mature and flowering (Minnesota Statutes Section 342.31).

This is smart policy often overlooked:

Research shows home cultivation complements retail rather than competes. Most consumers find cultivation too costly, time-intensive, or complicated—they choose retail convenience. But allowing cultivation provides a legal option for budget-conscious consumers, reduces illicit market pressure from cultivation supply, and aligns with civil liberties principles.

Minnesota joins Colorado, Michigan, Oregon, Massachusetts, and others permitting home grow. Illinois, New Jersey, and Washington prohibit it—creating resentment and unnecessary enforcement costs.

The framework shows: Home cultivation rights improve legal market performance by 2-4 percentage points by reducing illicit cultivation's appeal.

What Holds Minnesota Back: Federal Barriers

Minnesota designed policy well. Federal law prevents optimization.

Barrier #1: The 280E Federal Tax Burden

Internal Revenue Code Section 280E, enacted 1982 during the War on Drugs, prohibits cannabis businesses from deducting ordinary business expenses.

Impact on Minnesota dispensaries:

Minnesota dispensary, $2M annual revenue:

Normal business (without 280E):

- Revenue: $2,000,000

- COGS: $600,000

- Operating expenses: $1,100,000

- Profit: $300,000

- Federal tax (21% corporate): $63,000

- Net profit after tax: $237,000

Cannabis business (with 280E):

- Revenue: $2,000,000

- COGS (deductible): $600,000

- Operating expenses (NON-deductible): $1,100,000

- Taxable income: $1,400,000 (not $300,000)

- Federal tax: $294,000 (not $63,000)

- Actual profit after tax: $6,000 (97% reduction)

The 280E penalty: $231,000 in extra federal taxes destroying profitability.

Minnesota's state-level 280E decoupling helps with Minnesota's 9.8% corporate income tax but does nothing about the 40-70% effective federal rate.

Social Equity Impact:

280E devastates under-capitalized businesses disproportionately:

- Social equity licensees lack reserves to absorb 280E losses

- Established MSOs have sophisticated tax structures, capital, and accountants

- Result: Social equity businesses struggle, partner with MSOs, or fail

280E operates as de facto barrier to minority and small business ownership in cannabis.

Barrier #2: Banking Restrictions and Payment Friction

Without SAFE Banking Act passage, Minnesota cannabis businesses remain largely unbanked:

Current banking situation in Minnesota:

- ~5-10 banks/credit unions serve cannabis businesses

- All operate "anonymously" (require NDAs, don't advertise publicly)

- Services provided at 3-5× normal fees

- Constant risk of account closure if federal priorities shift

Mastercard prohibition (effective August 2023): Mastercard ceased processing cannabis debit transactions industry-wide. 70-80% of cannabis consumers preferred debit cards where available. The prohibition forced increased cash reliance.

Impact on Minnesota operations:

Crime and safety:

- Cash-intensive businesses are robbery targets

- Dispensary employees face elevated risk

- Armored transport costs: $600-2,500 per pickup

- Security requirements: $50,000-180,000 annually per location

- Insurance premiums: 30-50% higher than normal retail

Consumer friction:

- Cash-only reduces transaction frequency by 18-25%

- Average transaction with debit: $13-18 higher than cash-only

- Younger, tech-savvy consumers particularly frustrated

Minnesota-specific challenges:

- No home delivery permitted yet (cash payment logistics impossible)

- No online payment processing

- No commercial lending for expansion

- Credit building impossible for social equity applicants

Minnesota sacrifices $100-150M annually in potential legal market activity due to payment friction alone.

Barrier #3: The Michigan Border Competition

Minnesota faces unique pressure from Michigan's mature, competitive market across the border.

Michigan opened adult-use market November 2019 (four years before Minnesota) and immediately outperformed:

Michigan advantages:

- Taxes: 10% excise + 6% sales = 16% total

- Minnesota taxes: 15% excise + ~7-8% sales/local = 22-23% total

- Michigan retail prices: $18-22 per item average

- Minnesota retail prices: $22-28 per item average

- Michigan achievement: 85% legal market share

- Minnesota projection: 62-68% legal market share (current)

- Michigan dispensaries: 900+ statewide

- Minnesota dispensaries: 15-20 currently, 150-200 eventually

Border impact:

Minnesota residents near Michigan border (Duluth area, northeastern counties) drive to Michigan for lower prices:

- Duluth to Ironwood, MI: 120 miles (2 hours)

- Round-trip gas cost: $30-40

- Savings on ounce: $120-180 (Michigan $45-80/oz vs. Minnesota $160-220/oz)

- Rational economic behavior for regular consumers

Economic loss: Estimated 8-12% of Minnesota's northern/northeastern cannabis consumers make regular Michigan purchases. That's $40-70M annually in Minnesota sales captured by Michigan due to price differential and regulatory head start.

The irony: Minnesota's legal cannabis policy subsidizes Michigan's economy.

Framework Assessment: Minnesota's Current Position and Potential

The CBDT Framework reveals Minnesota's current position and optimization potential.

Current Performance Estimate: 62-68% Legal Market Share

Transaction share: Estimated 68-75% (percentage of users choosing legal over illicit for at least some purchases)

Volume share: Estimated 62-68% (accounting for heavy user behavior patterns)

This represents strong initial performance for a market that launched three months ago. Minnesota exceeds:

- Illinois: 55-60% (high taxes, five years operational)

- California: 50% (policy disaster, nine years operational)

- Washington: 65% (high taxes, declining)

Minnesota approaches but underperforms:

- Colorado: 73-78% (moderate taxes, mature market)

- Michigan: 85% (low taxes, strong policy)

- Oregon: 82% (very low taxes, oversupplied)

Why Minnesota Performs Well Initially

Strong policy foundation:

- Minimal fragmentation (limited local bans)

- Comprehensive testing (quality advantage clear)

- Home cultivation rights (legal option for budget consumers)

- Tribal partnership supply (product availability from day one)

- Moderate taxes (not optimal but not catastrophic like Illinois)

Why Minnesota Cannot Sustain Growth Without Reform

Price competitiveness (4× weight): MODERATE CONCERN

Minnesota legal prices 35-55% above illicit:

- Legal: $11-14/gram flower, $50-70/gram concentrate

- Illicit: $8-10/gram flower, $25-35/gram concentrate

The framework shows legal markets struggle when prices exceed illicit by >20%. Minnesota's 35-55% premium is concerning but not catastrophic (Illinois is 40-60%, California is 50-80%).

Heavy users (20% of consumers, 80% of volume) are most price-sensitive. Many will choose illicit markets or Michigan.

Access density (2.8× combined weight): TEMPORARILY WEAK, IMPROVING

- Current: 0.26-0.35 per 100,000 (nascent)

- Expected 2026: 2.5-3.5 per 100,000 (adequate)

- Optimal Minnesota density: 3.5-4.5 per 100,000

Rural areas particularly underserved. Tribal dispensaries help but face accessibility challenges. No delivery permitted yet—legislative priority for 2025-2026.

Convenience (includes payment friction): WEAK

- Cash-only or limited debit (Mastercard prohibited)

- Reduces transaction frequency 12-18%

- No delivery permitted

- Operating hours: Varies by location, generally 9 AM - 9 PM

- Online ordering for pickup available

Safety/Quality (1.2× weight): STRONG

Minnesota excels:

- Rigorous testing requirements

- METRC seed-to-sale tracking

- Professional dispensary operations

- Quality advantage over illicit market clear

But quality advantage matters less when price differential is 35-55%. Consumers accept moderate quality reduction for 40-50% cost savings.

Enforcement (0.6× weight): MODERATE

Minnesota law enforcement focuses on:

- Interstate trafficking (Michigan border monitoring)

- Large-scale illegal cultivation

- Unlicensed sales operations

Not Nevada-level interdiction but not California-level abdication either. Adequate but not aggressive.

Market Fragmentation Penalty: LOW

Minnesota's state preemption prevents most local bans. Geographic gaps exist (rural areas) but limited compared to California or Illinois.

Optimized Scenario: What Minnesota Could Achieve

With federal reform and minor state adjustments, Minnesota could improve from mid-tier to top-tier performance.

Requirements for Optimization

Federal Level:

- Schedule III rescheduling (280E elimination): Reduces retail prices 12-18%

- SAFE Banking Act passage: Enables card payments, reduces cash friction

State Level (Minor Adjustments):

- Tax rate reduction: From 15% to 12% excise once market matures

- Delivery authorization: Statewide delivery for rural/mobility-limited access

- License cap removal: Allow market-driven growth to 200-250 dispensaries

Predicted Outcomes (Optimized Policy + Federal Reform)

Timeline: 36-48 months after implementation

Legal Market Share:

- Transaction share: 82-88%

- Volume share: 78-85%

Economic Impact:

- Legal market: $750M-950M annually (mature market projection)

- State tax revenue: $90M-125M annually

- Illicit market: Reduced from $400M-500M to $120-180M (70-75% reduction)

- Jobs: 7,000-9,500 total

Price Impact:

- Retail prices drop 25-35% from current levels

- Average item price: $15-20 (vs. current $22-28)

- Legal cannabis becomes price-competitive with illicit

- Legal/illicit differential: 15-25% (acceptable for quality/convenience)

Comparable Performance: Minnesota would achieve outcomes similar to Michigan and Colorado—top-tier legal market performance with minimal black market persistence.

Social Equity Impact:

- SAFE Banking enables capital access for social equity licensees

- 280E elimination allows small businesses to achieve profitability

- Lower prices make legal cannabis accessible to disadvantaged communities

- Market expansion creates opportunity for new entrants

Border Competition:

- Reduced Michigan arbitrage (Minnesota prices now competitive)

- Recapture $30-50M annually in border sales

- Minnesota becomes destination for Wisconsin/Iowa/Dakotas consumers

Failed Scenario: Stagnation Without Reform

Without federal support, Minnesota's promising start deteriorates.

Continuation of Current Policy

What causes decline:

- Federal reform doesn't happen (280E remains, SAFE Banking fails)

- Minnesota maintains 15% tax rate (or increases due to budget pressure)

- Michigan continues capturing Minnesota consumers

- Supply constraints and high prices persist

- Social equity program struggles with capital access

Predicted Outcomes (No Reform)

Timeline: 2025-2030

Legal Market Share:

- Transaction share: 62-70% (slow growth, plateaus)

- Volume share: 55-62% (declining as heavy users choose illicit/Michigan)

Economic Impact:

- Legal market: $450M-600M annually (below potential)

- State tax revenue: $60M-85M annually

- Illicit market: Persists at $350-450M (30-40% of total demand)

- Jobs: 4,500-6,000 (below potential)

Border State Losses:

- $50-80M annual sales lost to Michigan

- Minnesotans increasingly cross border for lower prices

- Tax revenue flowing to Michigan economy

Social Equity Challenges:

- Capital-constrained licensees unable to compete

- Ownership consolidation to MSOs continues

- Disadvantaged communities continue buying illicit due to price

The Failed Policy Outcome:

Minnesota would join Washington State as a case study: Good initial policy undermined by federal barriers, resulting in persistent black market, disappointing revenue, and social equity failure.

The difference: Washington State has 37% excise tax (policy choice failure). Minnesota has 15-22% burden (federal penalty failure). Minnesota did policy right. Federal obstruction prevents success.

Policy Recommendations: The Path Forward

Minnesota designed policy well. Minor adjustments and federal reform enable optimization.

Priority #1: Federal Reform Advocacy

Schedule III Rescheduling (280E Elimination):

Current Minnesota impact:

- 280E costs Minnesota cannabis businesses $40-60M annually in excess federal taxes

- Forces retail prices 15-20% higher than economically necessary

- Reduces legal market share by 8-12 percentage points

- Costs Minnesota $20-35M in lost state tax revenue

Post-Schedule III projection:

- Minnesota businesses save $40-60M in federal taxes annually

- Savings partially passed to consumers through 10-15% price reductions

- Legal market share improves to 70-75% within 18-24 months

- Minnesota gains $25-40M in additional state tax revenue

SAFE Banking Act Passage:

Current Minnesota impact:

- Cash-only operations create public safety risk

- Payment friction reduces transaction frequency 12-18%

- Costs Minnesota businesses $30-50M annually (security, elevated operating costs)

- Social equity licensees cannot access capital

Post-SAFE Banking projection:

- Card payment access increases transaction frequency 18-25%

- Minnesota market grows by $80-120M annually

- State tax revenue increases $12-18M annually

- Social equity access to commercial lending improves dramatically

Priority #2: Minor State Tax Adjustment (Future)

Minnesota's 15% excise rate is defensible during launch scarcity (limited supply justifies higher prices). As market matures and supply increases, the state should reduce to 12% to improve price competitiveness.

Recommended timeline:

- 2025-2026: Maintain 15% (supply-constrained market)

- 2027: Reduce to 13% (supply stabilizing)

- 2028+: Reduce to 12% (mature market optimization)

Political challenge: Legislators resist tax cuts fearing revenue loss.

Counter-argument: Revenue optimization comes through volume (market share) not rates. Lower taxes → lower prices → higher legal market share → more transactions → more total revenue despite lower rates.

Michigan proves this: 16% total burden generates more per-capita revenue than Minnesota's 22-23% will because Michigan captures 85% market share vs. Minnesota's projected 62-68%.

Priority #3: Authorize Statewide Delivery

Current: Home delivery prohibited. Legislation considered but not passed (2024-2025).

Recommended: Statewide delivery authorization

- Initially limit to licensed transporters

- Require age verification, purchase limits

- Enable cashless delivery once SAFE Banking passes

- Priority licenses for social equity applicants

- Tribal operations eligible for delivery licensing

Impact: Delivery improves access for rural areas, elderly consumers, mobility-limited individuals. The framework shows delivery authorization improves legal market share by 3-5 percentage points.

Michigan authorized delivery statewide. Illinois prohibited it (legislative failure). Minnesota should follow Michigan's example.

Priority #4: Continued Tribal Partnership Expansion

Minnesota should finalize compacts with all 11 tribes interested in cannabis operations. Current 5 compacts represent strong start. Remaining 6 tribes should receive identical partnership offers.

Tribal supply will be critical for Minnesota's market success. State-licensed cultivators will scale slowly (capital constraints, learning curves). Tribal facilities can scale faster (gaming profits provide capital, sovereignty enables rapid decisions).

Recommended state support:

- Technical assistance for tribes developing cannabis programs

- Expedited compact negotiation for interested tribes

- METRC integration support (state covers costs)

- Marketing support for tribally produced cannabis (quality branding)

The tribal partnership is Minnesota's competitive advantage. Double down on what works.

Timeline and Economic Projections

Phase 1 (Current — 2026): Market Launch and Scaling

Focus:

- Retail expansion from 15-20 to 60-100 dispensaries

- Tribal supply scaling to meet growing demand

- Social equity licensees becoming operational

- Price stabilization as supply increases

- Federal advocacy for Schedule III and SAFE Banking

Expected Market Performance:

- Legal market: $280M-380M annually (rapid growth phase)

- Legal market share: 62-68% (holding)

- Tax revenue: $42M-57M annually

- Jobs: 3,500-5,000

Key Challenge: Limited retail access in rural areas, high initial prices, payment friction.

Phase 2 (2026-2027): Schedule III Implementation

Assumes: DEA completes Schedule III rescheduling (likely 2025-2027)

Impact:

- Minnesota businesses save $40-60M annually in federal taxes

- Savings partially passed to consumers (8-12% retail price reductions)

- Price competitiveness improves moderately

Predicted Outcomes (12-18 months post-implementation):

- Legal market: $420M-550M annually (+50-65%)

- Legal market share: 68-73% (+6-10 points)

- Tax revenue: $63M-82M annually (+50%)

- Jobs: 5,000-6,500 (+1,500-2,000)

Note: Schedule III alone insufficient for optimization. SAFE Banking and minor state tax reduction still needed.

Phase 3 (2027-2029): SAFE Banking + Tax Adjustment

Assumes:

- SAFE Banking Act passes (bipartisan support exists, timing uncertain)

- Minnesota reduces excise to 12% (political challenge)

Combined Effect: Minnesota legal cannabis becomes price-competitive with illicit alternatives:

- Current legal: $22-28 per item

- Post-reform legal: $15-20 per item

- Illicit: $12-18 per item equivalent

- Legal price premium: 15-25% (acceptable for quality/convenience/safety)

Predicted Outcomes (12-24 months post-implementation):

- Legal market: $680M-880M annually (+62-90% from Phase 2)

- Legal market share: 78-85% (+10-17 points from Phase 2)

- Tax revenue: $92M-120M annually (lower rate, much higher volume)

- Jobs: 7,000-9,000 (+2,000-3,500 from Phase 2)

- Illicit market: Reduced from $400M to $120-180M (70% reduction)

Phase 4 (2029-2032): Optimized Steady State

Sustained Outcomes:

- Legal market: $750M-950M annually (inflation-adjusted growth)

- Legal market share: 78-85% (sustained)

- Tax revenue: $90M-125M annually

- Jobs: 7,500-9,500

Remaining Illicit Market (15-22%):

- Extreme price-sensitive heavy users (~8-10%)

- Home cultivation networks (~3-4%)

- Geographic gaps (very rural) (~2%)

- Social/cultural illicit preference (~2-4%)

This represents the optimization ceiling. Further improvement requires price reductions below economically sustainable levels for businesses.

Comparison to Other Markets

Minnesota's 62-68% initial legal market share represents strong launch performance.

High-Performing Markets (80%+)

Michigan (85% volume):

- Lower taxes (16% total vs. Minnesota 22-23%)

- Four-year head start (2019 vs. 2023)

- Mature supply chain (900+ dispensaries)

- Superior banking access

- Statewide delivery authorized

- Why Michigan leads: Price competitiveness + mature infrastructure

Oregon (82% volume):

- Very low taxes (17% total)

- Oversupply creates price competition

- Legal prices often below illicit

- Strong enforcement

- Why Oregon leads: Extreme price competitiveness

Colorado (73-78% volume):

- Moderate taxes (19-23% effective)

- Mature infrastructure (11 years operational)

- Minimal fragmentation

- Home cultivation permitted

- Why Colorado succeeds: Balanced policy, pioneer experience

Mid-Tier Markets (60-75%)

Minnesota (62-68% volume) — current projection:

- Moderate taxes (22-23%)

- Nascent infrastructure (3 months operational)

- Strong policy foundation

- Federal barriers prevent optimization

Washington (65% volume):

- High taxes (37% flat excise)

- No home cultivation

- Declining sales (mature market fatigue)

- Similar federal burden to Minnesota but worse state policy

Struggling Markets (40-60%)

Illinois (55-60% volume):

- Very high taxes (25-40%)

- Under-optimized despite 5 years operational

- Price uncompetitive with illicit/Michigan

- Social equity undermined by economic inaccessibility

California (50% volume):

- Very high taxes (30%+ effective)

- Massive fragmentation (61% local bans)

- Minimal enforcement

- Policy disaster despite ideal conditions

Minnesota's Position:

Minnesota performs well initially because policy foundation is sound. Minnesota cannot sustain growth because federal 280E adds 15-20% to prices and SAFE Banking absence creates friction.

The trajectory: With federal reform, Minnesota joins Michigan/Colorado as top-tier market (78-85%). Without federal reform, Minnesota plateaus like Washington (55-62%).

Policy choice at federal level determines outcome.

The Medical Cannabis Program

Minnesota's medical cannabis program, established in 2014, has evolved significantly. As of 2023, the program expanded to "any medical condition" for which a healthcare practitioner has recommended cannabis—effectively opening eligibility to all patients with doctor certification.

Medical Program Details:

- Qualifying conditions: Any condition certified by participating healthcare practitioner (19 specific conditions listed, but "any medical condition" language added)

- Registration: No physical card issued—registry enrollment only

- Fees: $0 since July 2023 (previously $50-200)

- Providers: Green Goods (8 locations), RISE (8 locations)

- Tax status: Medical cannabis exempt from all cannabis taxes

Medical vs. Adult-Use:

Unlike many states where adult-use legalization devastates medical programs, Minnesota maintained separation:

- Medical providers converted to "medical cannabis combination businesses"

- Can sell both medical and adult-use (separate inventory/tracking)

- Medical patients maintain tax exemption (22-23% savings)

- Registry enrollment remains relevant for heavy users seeking tax savings

Medical enrollment incentive: For consumers spending $100+/month, medical registration saves $22-23/month (22-23% tax differential). Over a year, that's $264-276 savings—worth the registration hassle for many.

Conclusion: Minnesota's Success Depends on Federal Reform

Minnesota made smart policy choices: Tribal partnerships, comprehensive regulation, social equity focus, minimal fragmentation, home cultivation rights, moderate taxes. The state learned from predecessors' mistakes and implemented a framework designed to succeed.

But good state policy cannot overcome federal barriers:

- IRC Section 280E adds 15-20% to retail prices

- SAFE Banking prohibition creates payment friction

- Federal prohibition prevents interstate commerce

- Combined effect: Legal market underperforms potential by 15-20 percentage points

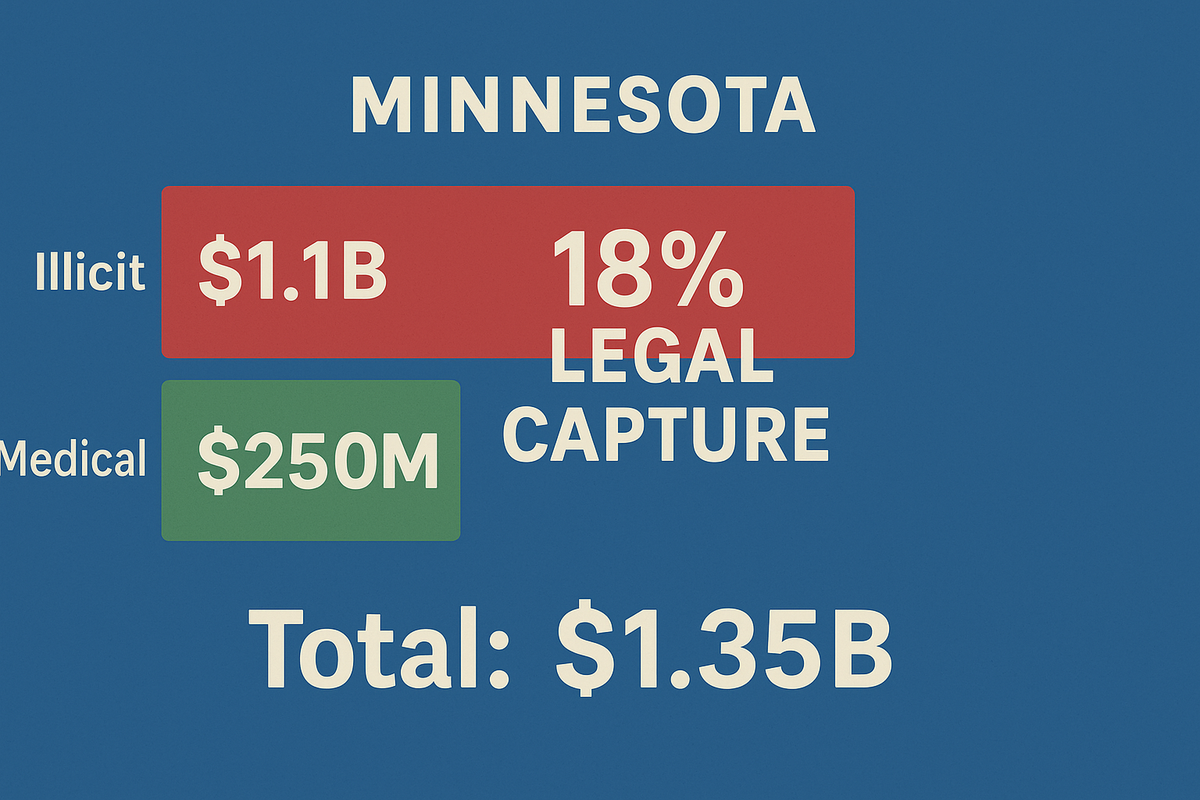

Current trajectory: 62-68% legal market share, $450M-600M annual market, $60M-85M state tax revenue

Optimized trajectory: 78-85% legal market share, $750M-950M annual market, $90M-125M state tax revenue

Difference: $30-40M annually in state revenue, 3,000-4,500 jobs, 60-70% black market reduction

Minnesota's tribal compact model works. It enables rapid market launch, supply chain stability, economic development for sovereign nations, and a cooperative federalism blueprint applicable nationwide.

The prediction: Minnesota will achieve 78-85% legal market share if Schedule III rescheduling and SAFE Banking Act pass by 2027. Without federal reform, Minnesota plateaus at 55-62%—underperforming Michigan by 20-25 percentage points despite superior tribal partnership model.

Federal policy determines whether Minnesota's innovation succeeds or fails.

Minnesota pioneered smart cannabis policy through tribal partnerships. Now Minnesota must advocate for federal reform that allows state innovation to flourish.

The tribal compact model offers a proven path forward for nationwide cannabis policy. Gaming compacts work. Cannabis compacts can too.

Minnesota shows what's possible when state policy respects tribal sovereignty, learns from others' mistakes, and designs for consumer needs. But even excellent state policy cannot overcome federal obstruction.

Congress must act. Schedule III, SAFE Banking, and tribal compact framework legislation would enable Minnesota (and all legal states) to achieve the public safety, economic, and social equity outcomes legalization promised.

Minnesota chose success at the state level. Federal choice determines whether success becomes reality.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: New Mexico | S Dakota | Georgia | Delaware | Maine

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0