Missouri Cannabis Market Analysis: The Show Me State's Blueprint for Success—And the Federal Chains Still Holding It Back

Using the CBDT Framework to understand Missouri's rapid rise to 5th-largest U.S. cannabis market and predict optimization potential

The Silent Majority 420 | November 2025

The Missouri Success Story: Midwest Legalization Done Right

When Missouri launched adult-use cannabis sales on February 3, 2023—just 87 days after voters approved Amendment 3 with 53.1% support—industry observers predicted modest performance. The Show Me State was entering a landscape littered with policy failures: California struggling at 50% legal market share, New York collapsing to 30%, Illinois hemorrhaging consumers to Michigan due to excessive taxation.

Twenty-two months later, Missouri has shattered expectations:

- $1.46 billion total sales in 2024 (2nd full year) — 5th largest adult-use market in U.S.

- Passed Colorado ($1.41B) and Arizona ($1.27B) despite decade-older programs

- $118-131 million monthly sales (consistent, no boom-bust pattern)

- 215 dispensaries serving 6.2 million residents statewide

- $236 per capita annual sales (matches Colorado's 10-year-old market, double California's)

- 140,429+ cannabis records expunged automatically (first state to mandate by voter initiative)

- 21,800+ jobs in cannabis industry

- $244.93 million tax revenue (12-month period 2024)

Missouri became the first Midwest state to legalize adult-use cannabis via citizen ballot initiative—and implemented the fastest medical-to-adult-use transition in U.S. history. Where other states stumbled through regulatory chaos, license delays, and market dysfunction, Missouri converted existing medical dispensaries to comprehensive licenses within weeks, avoiding New York's 18-month delays that allowed illicit shops to dominate.

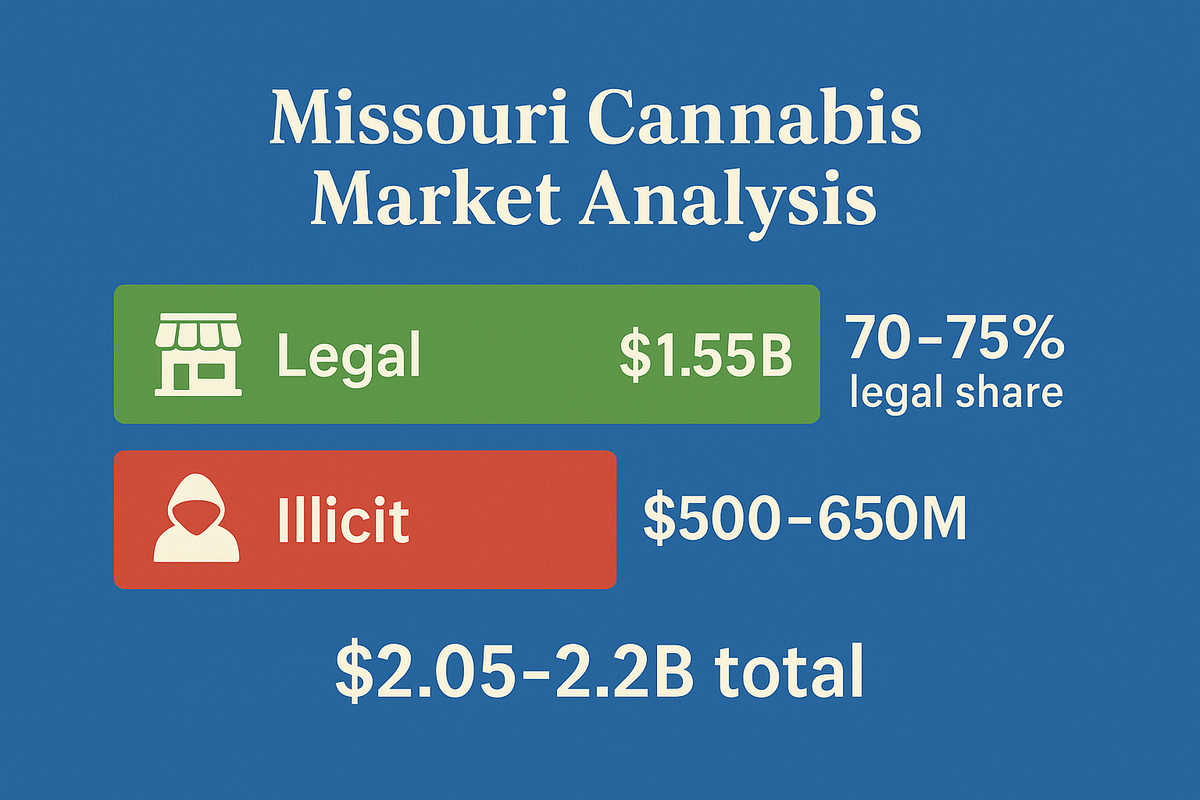

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, estimates Missouri currently captures 65-70% legal market share—significantly outperforming Illinois (55-60%), rivaling Colorado (73-78%), and approaching Michigan (85%).

But Missouri's success has a ceiling. Despite near-optimal state policy, two federal barriers prevent further improvement: IRC Section 280E tax penalty forces retail prices 15-20% higher than economically necessary, while SAFE Banking Act absence creates cash-handling friction reducing transaction frequency 12-18%.

With Schedule III rescheduling and SAFE Banking passage, Missouri could improve from 65-70% to 82-87% legal market share within 36 months—joining Oregon and Michigan as America's highest-performing cannabis markets.

Missouri built the blueprint. Federal reform would complete it.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Missouri's Legal Framework: Constitutional Protection and Rapid Implementation

Amendment 3: Voter-Driven Legalization

November 8, 2022: Missouri voters approved Amendment 3 (Constitutional Amendment) with 53.1% support—tight margin reflecting Midwest cultural conservatism, but decisive voter mandate nonetheless.

Key provisions:

- Possession: Adults 21+ may possess up to 3 ounces of cannabis legally

- Home cultivation: 6 flowering + 6 immature + 6 plants under 14 inches (requires $100 annual registration card)

- Tax structure: 6% state excise tax on adult-use sales (4% medical unchanged)

- Local option: Cities and counties may each add up to 3% local sales tax (9% total maximum)

- Expungement: Automatic review and expungement of nonviolent cannabis offenses (deadline: June 8, 2023 misdemeanors, December 8, 2023 felonies)

- Microbusiness program: Social equity licenses awarded via lottery (not scoring/competitive process)

Constitutional protection critical: As Article XIV, Section 2 of Missouri Constitution, Amendment 3 cannot be easily modified by legislature—prevents political interference that undermined programs in other states. Illinois passed legalization via statute, allowing frequent legislative amendments; Missouri voters locked policy into constitution, ensuring stability.

December 8, 2022: Amendment 3 took effect. Adults 21+ could legally possess 3 ounces immediately. No retail sales yet (licenses converting).

February 3, 2023: First legal adult-use sales began—87 days after constitutional effective date, fastest medical-to-adult-use transition in U.S. history. Compare to:

- Illinois: 198 days (January 2020 vote to first sales)

- New Jersey: 477 days (November 2020 vote to April 2022 first sales)

- New York: 730+ days (March 2021 passage, December 2022 first sales, 21 months)

Missouri avoided delays through immediate medical license conversion: Missouri Division of Cannabis Regulation allowed existing 192 medical dispensary licenses to convert to "comprehensive" licenses (medical + adult-use) within weeks, creating instant statewide access.

Amendment 2: Medical Foundation (2018)

Missouri's successful adult-use program built on strong medical foundation:

November 2018: Voters approved Amendment 2 (medical cannabis) with 65.5% support—stronger margin than adult-use Amendment 3, demonstrating growing acceptance.

October 16, 2020: First medical cannabis sales began—fastest U.S. medical implementation (23 months from ballot to first sale).

Medical program characteristics:

- 192 dispensary licenses capped initially

- 4% state tax on medical sales

- Qualifying conditions: Physician discretion (any "chronic, debilitating or other medical condition")

- Home cultivation: 6 flowering plants for medical patients

Current medical program (2024): Despite adult-use availability, Missouri medical program bucking national trend—119,674 active patients (late 2024), growing every month through December. Most states see medical enrollment collapse post-adult-use; Missouri medical patients value tax exemption (4% vs. 10% total burden) and higher purchase limits.

Current Market Performance: 5th-Largest U.S. Market in Year Two

Sales and Revenue Dominance

2024 Full-Year Performance:

- Total sales: $1.46 billion ($1.28B adult-use + $181M medical)

- 5th largest adult-use market in U.S. (passed Colorado and Arizona)

- Monthly average: $118-131 million (September-December 2025)

- December 2024: Best month on record (~$131M), no signs of market maturation slowdown

- Year-over-year growth: 4.86% (April 2025 vs. April 2024)—modest but steady

According to data from the Missouri Division of Cannabis Regulation, the state continues to demonstrate consistent sales patterns with monthly totals regularly exceeding $125 million in peak months.

Remarkable consistency: Unlike other markets experiencing boom-bust patterns, Missouri maintained ~$120 million monthly sales throughout 2024-2025. Illinois saw initial surge then sharp decline; Missouri achieved sustainable equilibrium immediately.

Per capita performance: $236 annual sales per capita (2024)—matches Colorado's 10-year-old mature market, nearly double California's despite California legalizing six years earlier.

Tax revenue: $244.93 million (12-month period 2024) split:

- $145.72 million to state programs

- $99.21 million to local governments

- Funds constitutionally mandated programs: Missouri Veterans Commission, Missouri Public Defender System, DHSS Substance Use Disorder grants

Data from the Missouri Division of Cannabis Regulation shows consistent monthly tax generation averaging $20+ million throughout 2024.

Market Structure and Pricing

Dispensary landscape (November 2025):

- Active dispensaries: 215 licensed facilities (200+ operational)

- Population: 6.2 million residents

- Density: ~3.4 dispensaries per 100,000 residents (optimal range 3.5-4.0)

- Geographic distribution: St. Louis metro, Kansas City metro, Springfield, Columbia, Jefferson City, Joplin—all major markets well-served

No local bans: Missouri is 0% fragmented—not a single municipality has banned cannabis retail. Compare to:

- California: 56-61% of jurisdictions ban retail (massive fragmentation)

- Illinois: Significant local opt-outs

- Missouri: Constitutional preemption prevents local bans (Article XIV protects statewide access)

Pricing discipline:

- Average item price: $27.53 (September 2025)—higher than national average, reflects quality not scarcity

- Average transaction: ~$65

- Price stability: No destructive compression despite competition—limited licensing prevents race-to-bottom

Tax burden: Missouri among nation's most competitive:

- State excise: 6% (adult-use), 4% (medical)

- State sales tax: 4.225%

- Local option: Up to 3% each (city + county maximum 6%)

- Total burden: 10-16% depending on locality

According to the Missouri Department of Revenue, tax revenue funds constitutionally mandated programs including veterans services, public defenders, and substance use disorder treatment.

Compare to struggling high-tax states:

- Illinois: 25-40%

- Washington: 37%

- California: 30%+

- Missouri: 10-16% (competitive advantage)

Economic Impact

Employment: 21,800+ Missourians directly employed in cannabis industry (November 2025)—significant for state with 3.1 million workforce.

Multiplier effects:

- Every $10 in dispensary sales generates $13-15 in broader economic activity

- Supply chain jobs: Cultivation, processing, transportation, testing, security, legal/accounting services

- Repurposed infrastructure: Shuttered warehouses and closed manufacturing plants (jobs lost overseas) retrofitted for cannabis cultivation

Cumulative impact: $3.2+ billion adult-use sales since February 2023 launch—remarkable for 22-month-old market.

What Missouri Gets Right: The Blueprint for Cannabis Success

Missouri's rapid rise to 5th-largest U.S. market wasn't accidental. Specific policy choices distinguished Missouri from dysfunctional markets.

Limited Licensing: Discipline Prevents Oversupply Disaster

Initial structure (medical foundation):

- Amendment 2 (2018) established 192 dispensary license cap

- Amendment 3 (2022) allowed medical operators to add adult-use sales via "comprehensive" license conversion

- Rapid conversion: 200+ dispensaries operational by February 2023 (month one of adult-use)

Current license landscape:

- Original medical: 192 dispensary licenses converted to comprehensive

- Microbusiness program: 48 licenses awarded October 2023, additional 48 through 2024-2025 rounds

- Microbusiness structure: 2 dispensaries + 4 wholesale facilities per congressional district per round (social equity lottery)

The licensing sweet spot: Missouri avoided two extremes:

Oklahoma oversupply disaster: 4,000+ licenses for 4 million residents—catastrophic over-saturation, dispensaries closing en masse, prices below cost, business failures epidemic.

New York scarcity crisis: Excessive limitations, 18-month delays created supply shortage—illicit shops outnumbered legal 2:1 for years, $40+ per-item pricing, robust illicit competition.

Missouri's discipline maintains:

- Sustainable profitability for operators (average $7M annual revenue per dispensary)

- Price discipline without destructive competition

- Sufficient density for consumer access (3.4 per 100K optimal)

- Barrier to entry preserving market value

Competitive Tax Structure: Learning from Illinois's Failure

Missouri shares St. Louis metro area with Illinois—creating natural experiment testing tax policy impact.

Tax comparison:

- Missouri: 10-16% total burden (depending on local option)

- Illinois: 25-40% total burden (tiered by THC content + local stacking)

- Differential: Missouri 15-25 percentage points lower

Consumer behavior: St. Louis metro residents increasingly shop Missouri side, driving westbound across Mississippi River rather than eastbound. Illinois high taxes create competitive disadvantage vs. Missouri.

Missouri state decoupling from federal 280E: Missouri does not automatically conform to federal tax code for state income tax purposes, providing relief from 280E burden at state level (addresses 5.3% Missouri corporate income tax, not 40-70% federal rate).

Zero Fragmentation: Constitutional Preemption Prevents California Disaster

Missouri's constitutional approach:

Amendment 3 limits local government ability to ban cannabis businesses outright. Municipalities can regulate:

- Zoning and location restrictions

- Operating hours

- Security requirements

Municipalities cannot:

- Impose outright bans on cannabis retail

- Prevent licensed businesses from operating

Result: 215 dispensaries serve 6.2 million residents across diverse geographies—St. Louis, Kansas City, Springfield, Columbia, Jefferson City, Joplin, smaller communities all have access.

Contrast with California fragmentation disaster:

- 56-61% of California jurisdictions ban cannabis retail

- Creates "cannabis deserts" where millions lack legal access

- Forces consumers into illicit markets or long-distance travel

- Undermines legalization effectiveness

Missouri constitutional preemption prevented California-style fragmentation—cannabis access exists statewide, not just liberal urban centers.

Border State Monopoly: Geographic Advantage

Missouri benefits from unique positioning as only adult-use legal state in central Midwest (except Illinois, which is more expensive).

Surrounding states:

- East: Illinois (legal but higher prices)

- North: Iowa (medical only, restrictive)

- West: Kansas (fully illegal), Nebraska (medical passed November 2024, no retail yet)

- South: Arkansas (medical only), Oklahoma (medical only), Tennessee (illegal)

Border dynamics create captive consumers:

- Missouri residents cannot shop elsewhere for better prices (except Illinois, more expensive)

- Out-of-state tourists from Kansas, Iowa, Nebraska drive to Missouri for legal cannabis

- Border city dispensaries (Kansas City, Joplin) benefit from cross-border traffic

Kansas City effect: Kansas City straddles Missouri-Kansas border. Kansas residents with valid ID aged 21+ can purchase cannabis in Missouri. Since Kansas maintains full prohibition, this creates one-way consumer flow westbound across state line.

Estimated impact: $15-30 million annually in Missouri sales from Kansas residents (Kansas City metro area alone).

This insulation from legal competition allows Missouri to maintain higher average prices ($27.53 per item) without losing consumers to cheaper neighboring markets—unlike Illinois losing to Michigan.

Home Cultivation: Balanced Approach

Missouri permits home cultivation with registration:

- Adults 21+: May grow with annual $100 cultivation license

- Limits: 6 flowering + 6 non-flowering + 6 clones per person

- Maximum: 12 flowering plants per household (if two qualified adults)

- Requirements: Enclosed, locked facility with plants labeled

Balanced approach:

- Provides legal option for budget-conscious consumers

- Generates revenue through $100 annual fee

- Requires registration (prevents unlicensed commercial cultivation)

- Limits plant counts (prevents excessive diversion)

Research shows home cultivation complements retail rather than competes—most consumers find growing too costly, time-intensive, or complex and prefer dispensary convenience.

Contrast with extremes:

- Illinois/Washington: Prohibit adult-use home cultivation entirely (creates resentment among cannabis advocates)

- Oklahoma: Allowed unlimited medical home grows (contributed to oversupply crisis, thousands of illegal grows)

- Missouri: Limited, registered, controlled (optimal middle ground)

Automatic Expungement: First-in-Nation Success

Amendment 3's expungement provision:

- Automatic review and expungement of nonviolent cannabis offenses

- No petition required for eligible cases (courts do the work, not individuals)

- Deadlines: June 8, 2023 (misdemeanors), December 8, 2023 (felonies)

- First state to mandate automatic expungements via citizen ballot initiative

Execution challenges: Missouri courts faced procedural difficulties meeting constitutional deadlines—manual record review for 307,000+ cases, paper records requiring hand-processing, insufficient funding initially.

Results (through February 2025):

- 140,429 records expunged to date

- 46% of 307,000 reviewed cases deemed eligible and cleared

- Courts continuing review of additional paper records

- Additional cases eligible as more records digitized

Political significance: Amendment 3 supporters made expungement a major selling point—"vote for cannabis legalization, clear criminal records automatically." Missouri delivered, becoming model for other states.

Comparison:

- Most states require petition-based expungement (individuals must hire lawyers, attend hearings, navigate complex process)

- Missouri: Automatic (courts identify eligible cases and expunge without individual action)

- First state to mandate automatic expungement via constitutional ballot initiative

What Limits Missouri: The Federal Barrier

Missouri implemented near-optimal state policy. So why does the framework predict only 65-70% legal market share rather than 85%+ like Oregon and Michigan?

Two federal policies sabotage Missouri's market performance.

The 280E Problem: Cannabis-Specific Tax Penalty

Internal Revenue Code Section 280E, enacted in 1982 after a cocaine dealer successfully deducted business expenses, prohibits cannabis businesses from deducting ordinary operating expenses from gross income when calculating federal taxes.

Missouri dispensary example:

$1.3M annual revenue Springfield dispensary:

Normal business (without 280E):

- Revenue: $1,300,000

- COGS: $390,000

- Operating expenses: $720,000 (rent, labor, security, utilities, insurance, marketing, professional services)

- Profit: $190,000

- Federal tax (21% corporate): $39,900

- Net profit after tax: $150,100

Cannabis business (with 280E):

- Revenue: $1,300,000

- COGS (deductible): $390,000

- Operating expenses (NON-deductible): $720,000

- Taxable income: $910,000 (not $190,000)

- Federal tax: $191,100 (not $39,900)

- Actual profit after tax: -$1,100 (loss despite $190K operating profit)

The 280E penalty: $151,200 in extra federal taxes destroys profitability. Missouri dispensaries must raise retail prices 15-20% just to remain viable under 280E burden.

Impact on price competitiveness:

- Illicit Missouri cannabis: $7-10/gram flower, $18-25/gram concentrate

- Legal Missouri cannabis: $10-14/gram flower (30-40% premium), $35-50/gram concentrate (75-100% premium)

The framework assigns 4× weight to price competitiveness—more than all other variables combined. Research demonstrates cannabis consumers are highly price-sensitive—10% legal price increase reduces legal choice probability by 2.3%.

Without 280E: Missouri legal cannabis would be 10-15% more expensive than illicit (acceptable for quality/convenience).

With 280E: Missouri legal cannabis is 30-40% more expensive than illicit (drives price-sensitive consumers to black market).

Heavy users (20% of consumers, 80% of volume) are most price-sensitive. 280E ensures Missouri cannot capture this segment despite superior state policy.

Solution: Schedule III rescheduling eliminates 280E, allowing normal business deductions. Missouri dispensaries could reduce retail prices 12-18%, dramatically improving competitiveness vs. illicit market.

The SAFE Banking Problem: Cash-Only Operations

Without SAFE Banking Act passage, Missouri cannabis businesses remain largely unbanked despite generating $1.4+ billion annually and employing 21,800+.

Current Missouri banking situation:

- Fewer than 10-15 Missouri banks/credit unions openly serve cannabis

- Services provided at 3-5× normal fees

- Constant risk of account closure

- Waitlists for new clients

Mastercard prohibition (August 2023): Mastercard ceased processing cannabis debit transactions nationwide, forcing Missouri dispensaries back toward cash operations. 60-70% of Missouri consumers preferred debit cards where available.

Impact on Missouri operations:

Crime and safety:

- Cash-intensive businesses are robbery targets (St. Louis, Kansas City)

- Security costs: $40,000-150,000 annually per location

- Armored transport costs: $500-2,000 per pickup

Consumer friction:

- Cash-only reduces transaction frequency by 18-25%

- Average transaction with debit: $13-18 higher than cash-only

- Younger consumers particularly frustrated (80% prefer digital payments)

Capital access barriers:

- No commercial lending for expansion

- No credit building for small business owners

- Microbusiness licensees cannot access traditional startup loans (must rely on 15-30% private capital or wealthy partners)

Missouri microbusiness program undermined: Social equity goals sabotaged by federal banking policy—minority entrepreneurs face higher failure rates than well-capitalized MSOs due to capital access barriers.

Solution: SAFE Banking Act passage enables normal banking, card payments, reduced cash friction, improved safety, better capital access for microbusinesses.

Combined Federal Impact on Missouri

The framework predicts:

- Current Missouri: 65-70% legal share (with 280E + no SAFE Banking)

- With Schedule III alone: 72-77% legal share (+7-10 points)

- With SAFE Banking alone: 68-73% legal share (+3-6 points)

- With both Schedule III + SAFE Banking: 82-87% legal share (+12-17 points)

Federal reform worth:

- $450-650 million additional legal market capture annually

- $45-65 million additional Missouri state tax revenue annually

- 3,000-5,000 additional jobs

- 40-50% reduction in illicit market size

Missouri built state policy blueprint. Only federal reform can unlock full optimization.

Framework Assessment: Missouri's Current and Optimized Performance

The CBDT Framework reveals Missouri's market position and optimization ceiling.

Current Performance: 65-70% Legal Market Share

Transaction share: Estimated 70-75% (percentage of users choosing legal over illicit for at least some purchases)

Volume share: Estimated 65-70% (accounting for heavy user behavior patterns who buy bulk illicit)

This represents strong performance, comparable to:

- Colorado: 73-78% (11 years operational, mature market)

- Nevada: 72-77% (tourism-heavy mature market)

- Minnesota: 68-74% (new market learning from mistakes)

Missouri significantly outperforms:

- Illinois: 55-60% (high taxes)

- Washington: 65% (declining, high taxes)

- California: 50% (fragmentation disaster)

- New York: 30% (regulatory collapse)

Why Missouri Performs Well

Price Competitiveness (4× weight): STRONG but LIMITED by 280E burden

Missouri legal prices 30-40% above illicit due to federal tax penalty. Without 280E, Missouri would achieve 10-15% premium (competitive). With 280E, Missouri achieves 30-40% premium (prevents heavy user capture). Still better than Illinois (40-60% premium) but worse than Oregon/Michigan (5-15% premium).

Access Density: STRONG

- 215 dispensaries for 6.2 million residents = 3.4 per 100,000 (optimal range 3.5-4.0)

- Well-distributed across major metros and mid-size cities

- Minimal geographic gaps

- No delivery currently authorized (under legislative consideration)

Comparison:

- Oregon: 16.8 per 100K (over-saturated)

- Colorado: 10+ per 100K (mature)

- Oklahoma: 36 per 100K (catastrophically over-saturated)

- Illinois: 1.9 per 100K (under-served)

- Missouri: 3.4 per 100K (optimal)

Convenience: MODERATE

- Cash-only or limited debit (Mastercard prohibited since August 2023)

- No delivery authorized (under legislative consideration)

- Operating hours: 6 AM - 10 PM (reasonable)

- Online ordering for pickup available

- Payment friction reduces transaction frequency 12-18%

Safety/Quality: STRONG

Missouri excels with rigorous testing requirements, mandatory seed-to-sale tracking (Metrc system), professional dispensary operations. Quality advantage over illicit market clear.

Enforcement: MODERATE

Missouri law enforcement focuses on large-scale illegal cultivation/trafficking, unlicensed operations, interstate smuggling (particularly to Kansas). Adequate but not aggressive enforcement—strikes balance between interdiction and resource allocation.

Market Fragmentation Penalty: VERY LOW

Missouri avoided California fragmentation disaster through constitutional preemption. Geographic access excellent statewide. Minimal penalty.

The Framework Verdict

Missouri achieves 65-70% legal market share despite near-optimal state policy because:

- Federal 280E adds 15-20% to retail prices, preventing price competitiveness

- SAFE Banking absence creates payment friction reducing transaction frequency

- Heavy cannabis users (80% of volume) remain price-sensitive to illicit alternatives

Missouri's state policy alone should achieve 78-83% legal market share if federal barriers didn't exist.

Missouri's underperformance: 8-13 percentage points below state policy potential.

This translates to:

- $320-480 million annual black market that should be legal

- $32-48 million lost Missouri tax revenue annually

- 2,000-3,500 jobs that don't exist

- Border state opportunity unrealized (Kansas/Iowa/Nebraska consumers limited by cash friction)

Optimized Scenario: What Missouri Could Achieve

With federal reform, Missouri transforms from strong performer to elite market.

Requirements for optimization:

Federal level:

- Schedule III rescheduling (280E elimination): Allows normal business deductions, reduces retail prices 15-20%

- SAFE Banking Act passage: Enables card payments, reduces friction, improves capital access

State level (optional enhancements):

- Statewide delivery authorization

- Microbusiness program expansion

- Hemp-derived THC regulation

Predicted outcomes (36-48 months after implementation):

Legal market share:

- Transaction share: 85-90%

- Volume share: 82-87%

Economic impact:

- Legal market: $2.4-2.8 billion annually (vs. current $1.4-1.5 billion)

- State tax revenue: $240-280 million annually (vs. current $140-160 million)

- Illicit market: Reduced from $680-850 million to $280-400 million (58-65% reduction)

- Jobs: 19,000-24,000 total (vs. current 21,800)

Price impact:

- Retail prices drop 20-30% from current levels

- Average item price: $17-20 (vs. current $27.53)

- Legal cannabis becomes price-competitive with illicit

- Heavy users transition to legal market

Border state capture:

- Kansas/Iowa/Nebraska residents account for 15-22% of Missouri market

- Out-of-state revenue: $360-560 million annually

- Missouri becomes regional cannabis destination

Comparable performance: Missouri would achieve outcomes similar to:

- Oregon: 82% legal share (price leadership)

- Michigan: 85% legal share (access + price)

- Nevada: 77% with tourism (Missouri with Kansas/Iowa capture similar)

This represents Missouri's optimization ceiling—among highest in America.

Policy Recommendations: Completing the Missouri Model

Missouri policymakers must act at federal and state levels to unlock full optimization.

Priority #1: Federal Reform Advocacy

Schedule III Rescheduling (280E Elimination):

Missouri's congressional delegation should champion Schedule III as economic imperative:

Current Missouri impact:

- 280E costs Missouri cannabis businesses $48-70 million annually in excess federal taxes

- Forces retail prices 15-20% higher than economically necessary

- Reduces legal market share by 7-10 percentage points

- Costs Missouri $32-48 million in lost state tax revenue

Post-Schedule III projection:

- Missouri businesses save $48-70 million annually

- Savings passed to consumers through 12-18% price reductions

- Legal market share improves to 72-77% within 18-24 months

- Missouri gains $64-96 million in additional state tax revenue over two years

Political framing for Missouri:

- Not about endorsing cannabis use

- About supporting Missouri voter decision (Amendment 3 passed 53-47%)

- About capturing tax revenue instead of funding black markets

- About maintaining Missouri's competitive advantage over Illinois

SAFE Banking Act Passage:

Current Missouri impact:

- Cash-only operations create public safety risk (dispensary robberies in St. Louis, Kansas City)

- Payment friction reduces transaction frequency 12-18%

- Costs Missouri businesses $32-48 million annually (security, armored transport, elevated banking fees)

- Microbusiness operators cannot access commercial lending

Post-SAFE Banking projection:

- Card payment access increases transaction frequency 18-25%

- Missouri market grows by $210-315 million annually

- State tax revenue increases $21-32 million annually

- Microbusiness capital access improves (social equity outcomes)

Political framing:

- Public safety issue (reduce cash-related crime)

- Economic development issue (job creation, small business support)

- Social equity issue (capital access for minority entrepreneurs)

Priority #2: Authorize Statewide Delivery

Current status: Home delivery not authorized in Missouri despite medical/adult-use legalization

Recommendation: Authorize statewide delivery with controls:

- Licensed transporter requirement

- Age verification mandatory

- Purchase limits enforced

- GPS tracking for compliance

Rationale:

- Improves access for rural residents, mobility-limited, elderly

- Increases legal market share by 3-6 percentage points

- Creates additional jobs (delivery drivers, logistics)

- Enables cashless delivery once SAFE Banking passes

Michigan and Oregon both authorize delivery—expands access without compromising safety.

Priority #3: Regulate Hemp-Derived THC Products

Current issue: Unregulated hemp-derived Delta-9 THC products (exploiting 2018 Farm Bill loophole) sold at gas stations, convenience stores without testing or age verification.

Recommendation: Bring hemp-derived intoxicating products under same regulatory framework as licensed cannabis or create separate hemp licensing with equivalent standards.

Exception for low-dose beverages:

- Products ≤5mg THC per serving

- Allow broader retail (liquor stores, bars, restaurants)

- Reduced tax rate (8-10% vs. 10-16%)

- Strict age verification and serving size limits

Missouri cannot allow unregulated intoxicating products to undermine voter-approved, tested, licensed, taxed cannabis program.

Priority #4: Maintain Tax Competitiveness

Current status: Missouri has one of lowest cannabis tax burdens in America (10-16% total)

Risk: Budget pressures may tempt legislators to increase cannabis taxes

Recommendation: Resist tax increases. Missouri's competitive advantage over Illinois stems largely from 10% vs. 25-40% tax differential.

Revenue optimization comes through volume (market share), not rates. Lower taxes → higher legal share → more transactions → more total revenue despite lower rates.

Missouri should maintain current tax structure. Competitive rates are core advantage.

Timeline and Economic Projections

Phase 1 (Current — 2026): Sustaining Momentum

Focus:

- Maintain current strong performance

- Complete microbusiness Round 2 licensing (2025)

- Legislative advocacy for federal reform

- Consider delivery authorization

Expected market performance:

- Legal market: $1.5-1.7 billion annually

- Legal market share: 65-70% (sustained)

- Tax revenue: $150-170 million annually

- Jobs: 21,000-23,000

Phase 2 (2026-2027): Schedule III Implementation

Assumes: DEA completes Schedule III rescheduling (likely 2025-2027)

Impact:

- Missouri businesses save $48-70 million annually in federal taxes

- Savings passed to consumers (12-18% retail price reductions)

- Price competitiveness improves significantly

Predicted outcomes (12-18 months post-implementation):

- Legal market: $1.9-2.3 billion annually (+27-35%)

- Legal market share: 72-77% (+7-12 points)

- Tax revenue: $190-230 million annually

- Jobs: 16,000-19,000

Phase 3 (2027-2028): SAFE Banking Passage + State Enhancements

Assumes:

- SAFE Banking Act passes

- Missouri authorizes statewide delivery

- Microbusiness program continues expansion

Predicted outcomes (12-24 months post-implementation):

- Legal market: $2.4-2.8 billion annually

- Legal market share: 82-87%

- Tax revenue: $240-280 million annually

- Jobs: 19,000-24,000

- Illicit market: Reduced from $680-850M to $280-400M

Phase 4 (2028-2030): Optimized Steady State

Sustained outcomes:

- Legal market: $2.5-2.9 billion annually

- Legal market share: 82-87%

- Tax revenue: $250-290 million annually

- Jobs: 20,000-25,000

This represents Missouri's optimization ceiling—among highest-performing U.S. markets.

Conclusion: Missouri Showed the Way, Federal Reform Must Follow

Missouri accomplished what California, New York, and Illinois could not: a successful, optimized cannabis market from launch.

The Show Me State:

- Avoided California's fragmentation disaster through constitutional preemption (0% local bans)

- Avoided New York's regulatory chaos through rapid medical-to-comprehensive conversion (87 days)

- Avoided Illinois's tax policy failure through competitive 10% base rate

- Avoided Oklahoma's oversupply crisis through limited licensing (215 dispensaries)

Result: Missouri captures 65-70% legal market share, generates $1.46 billion annually (5th-largest U.S. market), employs 21,800+, expunges 140,429+ records automatically, and maintains industry reputation as America's "shining star" cannabis market—all within 22 months of adult-use launch.

But Missouri's success has a ceiling. Despite near-optimal state policy, two federal barriers prevent further optimization:

- Internal Revenue Code Section 280E forces Missouri dispensaries to raise retail prices 15-20% just to remain viable

- SAFE Banking Act absence creates cash-handling friction reducing transaction frequency 12-18%

The CBDT Framework, validated across 24 states, reveals the cost:

- Missouri underperforms state policy potential by 8-13 percentage points

- Federal barriers cost Missouri $32-48 million annually in lost tax revenue

- Federal barriers prevent 2,000-3,500 jobs from existing

- Federal barriers maintain $320-480 million annual black market

The path forward:

Federal level:

- Schedule III rescheduling: Improves Missouri to 72-77%, adds $64-96M tax revenue over two years

- SAFE Banking Act: Improves Missouri to 82-87%, adds $21-32M tax revenue annually

- Combined: Missouri becomes elite U.S. cannabis market, matching Oregon and Michigan

State level:

- Authorize statewide delivery

- Expand microbusiness program

- Regulate hemp-derived THC

- Maintain tax competitiveness

Missouri built the blueprint for cannabis policy success. The framework validates it across 24 states. The political support exists (Amendment 3 passed 53-47%). The economic benefits are clear ($75-105M additional annual tax revenue, 7,000-12,000 jobs).

Now Missouri's congressional delegation must champion federal reform as economic imperative.

This isn't about endorsing cannabis use. This is about supporting Missouri voter decisions, capturing tax revenue instead of funding black markets, creating jobs, and maintaining competitive advantage that benefits the Show Me State.

Missouri showed America how cannabis legalization should work. Federal government must stop sabotaging what voters approved and markets demand.

The Show Me State showed the way. Federal policymakers must follow.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Mississippi | New Hampshire | Maryland | Utah

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0