Nebraska Cannabis Market Analysis: The Cornhusker State's Medical Mandate and the Path to Comprehensive Reform

Using the CBDT Framework to predict Nebraska's trajectory from prohibition to medical implementation to eventual adult-use legalization

The Silent Majority 420 | November 2025

The Nebraska Contradiction: Overwhelming Support Meets Uncertain Implementation

On November 5, 2024, Nebraska voters decisively ended the state's status as one of only two states without any medical cannabis access. Initiative 437 passed with 70.74% support, while Initiative 438—establishing the Nebraska Medical Cannabis Commission—received 66.95% approval. Despite legal challenges, Governor Jim Pillen signed proclamations on December 12, 2024, officially enacting both measures.

The vote wasn't close. More than two-thirds of Nebraskans across the political spectrum—conservative Omaha suburbs, liberal Lincoln precincts, rural agricultural counties—demanded safe legal access to medical cannabis.

Yet uncertainty persists. Governor Pillen and Attorney General Mike Hilgers issued statements cautioning "the proclamations do not express a judgment on the validity of the measures." Opponents continue pursuing legal challenges in the Nebraska Supreme Court. The newly created Nebraska Medical Cannabis Commission must implement regulations by July 1, 2025, and begin licensing businesses by October 1, 2025—if allowed to proceed.

This reflects Nebraska's fundamental tension: pragmatic, fiscally conservative voters versus ideologically rigid state leadership. Nebraskans understand what works. They've watched Colorado generate billions in tax revenue. They've seen Michigan achieve 85% legal market share through sensible policy. They've observed Illinois underperform through excessive taxation.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Nebraska's potential: With optimized medical implementation plus eventual adult-use legalization, Nebraska could achieve 75–82% legal market share within 48 months—outperforming Illinois, matching Colorado, approaching Michigan.

Nebraska possesses significant structural advantages: geographic concentration in the Omaha-Lincoln corridor, strong law enforcement culture, fiscally conservative governance favoring revenue optimization over ideology, and clean regulatory slate without legacy program complications.

But achieving this requires three critical conditions: medical program survives Supreme Court challenge, state leadership learns from neighbors' policy failures, and federal reform occurs (Schedule III rescheduling + SAFE Banking Act).

Without all three, Nebraska risks repeating Illinois's mistakes: high-tax policy creating expensive legal cannabis working-class Nebraskans cannot afford, persistent black markets thriving on price differentials, medical programs serving few while enriching politically connected licensees.

The question Nebraska faces: Will state leadership respect the overwhelming voter mandate and implement evidence-based policy? Or will ideological opposition undermine what 70%+ of Nebraskans demanded?

This analysis assumes the medical program survives legal challenge and Nebraska eventually moves toward adult-use legalization—predicting what happens when, not if, Nebraska joins the 24 states that have chosen this path.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Nebraska's Structural Advantages: Why the Cornhusker State Could Excel

Despite current prohibition, Nebraska possesses characteristics favoring legal market optimization—IF policymakers implement evidence-based policy.

Geographic Concentration

Nebraska's population distribution (2025):

- Omaha metro: 1,001,010 residents (50% of state population)

- Lincoln metro: 350,626 residents (17.5% of state)

- Combined Omaha-Lincoln: 67.5% of state's 2 million residents

- Top 3 metros: 72% of population

Douglas County (Omaha) alone contains 30% of the state. Lancaster County (Lincoln) contains 16%.

Framework significance: States with concentrated populations achieve higher access density per dispensary. Alaska struggles with 733,000 residents across 665,000 square miles. Montana must serve 1.1 million residents across 147,000 square miles. Nebraska's challenge is more manageable: 2 million residents with 67% concentrated in two metro areas.

Optimal strategy: 65–85 dispensaries could effectively serve 85%+ of Nebraska's population:

- Omaha metro: 35–45 dispensaries

- Lincoln metro: 12–18 dispensaries

- Grand Island-Kearney corridor: 5–8 dispensaries

- Rural coverage: Statewide delivery mandate

This achieves efficient density requiring neither Alaska-style aviation logistics nor California-style fragmentation battles. Comparable states like Colorado (55% population in Denver metro) and Nevada (73% in Las Vegas metro) achieve strong legal market share through urban concentration plus rural delivery.

Conservative Fiscal Culture as Competitive Advantage

Nebraska's political culture typically resists progressive social policy but strongly favors fiscal pragmatism and revenue optimization.

Framework significance: States with strong revenue motivations implement more thoughtful tax policy than states viewing cannabis primarily as cultural issue. Nebraska's fiscal conservatism could paradoxically produce better cannabis policy than progressive states.

Tax policy implications:

- Conservative philosophy: Maximize total revenue through volume, not per-unit taxation

- Progressive philosophy: Maximize per-unit taxation as "sin tax," accept lower volume

- Result: Conservative states often achieve higher legal market share through lower tax rates

Evidence from existing markets:

- Illinois (progressive governance): 25–40% total tax burden → 55–60% legal market share

- Colorado (mixed governance, revenue focus): 17–18% total burden → 73–78% legal market share

- Michigan (mixed governance, moderate taxes): 16% total burden → 85% legal market share

Nebraska's conservative fiscal culture suggests moderate tax rates (15–20% range) to maximize market share, revenue optimization through efficient enforcement, minimal bureaucratic overhead, and pragmatic approach valuing economic outcomes over ideological purity.

IF Nebraska legalizes, fiscal conservatism could override cultural conservatism in policy design—producing competitive framework.

Strong Law Enforcement Infrastructure

Nebraska maintains well-funded, coordinated law enforcement across state and local jurisdictions with active interstate trafficking interdiction at the Colorado border.

Framework significance: Enforcement weighs approximately 0.6× in market outcomes. States with strong enforcement cultures (Nevada, Michigan, Colorado) consistently outperform states with deprioritized enforcement (California, New York) by 15–25 percentage points.

Nebraska's enforcement capacity wouldn't need fundamental restructuring post-legalization—just redirection. Currently targets consumers possessing concentrates and interstate trafficking from Colorado. Post-legalization would target illegal cultivation operations, unlicensed retailers, sales to minors.

Same institutional capacity, different targets, proven effectiveness. California attempted to build enforcement infrastructure during transition to adult-use, resulting in fragmented authority, under-resourced agencies, and persistent illicit market dominance. Nebraska's existing enforcement strength becomes competitive advantage.

Clean Regulatory Slate

Nebraska starts with:

- No legacy medical program to transition

- No existing licensees to grandfather

- No complicated dual-market structure (medical + adult-use)

- No prior policy mistakes to unwind

- Clear voter mandate (70%+ support) for medical access

Framework significance: States transitioning from medical to adult-use often create regulatory structures serving two markets simultaneously—complexity creates inefficiency and loopholes.

- Illinois: Complex medical program (2013) transitioned to adult-use (2020)—regulatory overlap, social equity failures, market fragmentation

- California: 20-year medical market (1996–2016) resistant to adult-use transition—jurisdictional conflicts, persistent illicit market, policy incoherence

- Michigan: Clean separation of medical and adult-use programs—success through simplicity

Nebraska can implement best practices from day one: study Michigan's clean program structure, avoid Illinois's high-tax mistakes, learn from California's fragmentation disaster, implement Colorado's delivery infrastructure, adopt Nevada's enforcement model.

Starting fresh without legacy constraints is strategic advantage—if policymakers use it wisely.

The 70%+ Voter Mandate as Political Foundation

70.74% support for Initiative 437. 66.95% for Initiative 438.

This wasn't narrow victory or urban vs. rural split. Medical cannabis won decisively across conservative rural counties, Omaha suburban precincts, Lincoln urban districts, western agricultural regions, and eastern border communities.

Framework significance: Strong voter mandate creates political foundation for implementation despite leadership opposition. Nebraska's unicameral legislature (only state with single-chamber legislature) simplifies legislative action—no House/Senate coordination required.

Governor and Attorney General may personally oppose cannabis reform, but 2/3 voter support constrains opposition. If Supreme Court upholds medical cannabis and economic benefits materialize (tax revenue, jobs, medical access), adult-use legalization becomes politically viable within 4–8 years.

Comparable trajectories:

- Arizona: Medical 2010 → Adult-use 2020 (10 years)

- Montana: Medical 2004 → Adult-use 2020 (16 years)

- New Jersey: Medical 2010 → Adult-use 2021 (11 years)

Nebraska timeline projection: Medical 2024 → Adult-use 2028–2032 (4–8 years) depending on federal reform and program success.

Current Status (2025): Medical Program Launch, Prohibition Legacy

Nebraska enters 2025 in transition—medical cannabis legally enacted but operationally pending, adult-use cannabis completely prohibited.

The Medical Cannabis Victory (November 2024)

Initiative 437: Nebraska Medical Cannabis Patient Protection Act

Passed with 70.74% voter approval:

- Authorizes qualified patients to possess up to 5 ounces of cannabis

- Patients must obtain written recommendation from licensed healthcare practitioner

- Practitioners determine "potential benefits outweigh potential harms"

- Patients under 18 require practitioner recommendation and parental consent

- Caregivers authorized to possess allowable amount on behalf of patients

Initiative 438: Nebraska Medical Cannabis Regulation Act

Passed with 66.95% voter approval:

- Creates Nebraska Medical Cannabis Commission

- Commission regulates cultivation, processing, distribution, dispensing

- Must establish licensing rules by July 1, 2025

- Must begin issuing licenses by October 1, 2025

- First legal medical sales expected late 2025 or early 2026

The Implementation Challenge

Despite overwhelming voter support, medical cannabis faces continued opposition.

Legal challenges (ongoing):

- Opponents filed lawsuit challenging validity of petition signatures

- Lancaster County District Court Judge Susan Strong rejected challenge December 11, 2024

- Governor issued proclamations December 12, 2024

- Opponents appealed to Nebraska Supreme Court

- Final determination pending

Political opposition: Governor Pillen and Attorney General Hilgers issued joint statement: "The proclamations do not express a judgment on the validity of the measures." Translation: We signed because constitutionally required, not because we support this.

Despite political opposition, the Nebraska Medical Cannabis Commission has begun meeting regularly and reviewing license applications as of late 2025, indicating the program is moving forward operationally even as legal challenges proceed.

This creates uncertainty for businesses planning Nebraska operations. Until Supreme Court rules definitively, investment risk remains elevated.

Current Prohibition for Adult-Use

Nebraska maintains criminal penalties for non-medical cannabis possession:

Decriminalization (1978 Law):

- First offense possession of 1 ounce or less: Civil citation (not criminal arrest), fine up to $300 + court costs, possible mandatory drug education course, no jail time

- Second offense: Up to 5 days jail possible, higher fines

Concentrated cannabis (all amounts): Felony charges—the 1978 decriminalization law does NOT apply to concentrates, edibles, or any non-flower cannabis products.

Cultivation: Any amount results in felony charges regardless of plant count.

The hemp-derived THC loophole: Like most states, Nebraska allows delta-8, delta-9, and delta-10 THC products derived from hemp (≤0.3% THC by dry weight) under 2018 Farm Bill. These products available at gas stations, convenience stores, vape shops—zero regulation, no testing requirements, no age verification in many cases.

Result: Nebraskans can legally purchase intoxicating THC products at truck stops but face felony charges for growing a cannabis plant or possessing a concentrate cartridge.

Border State Pressure

Nebraska is surrounded by states with varying cannabis policies—creating arbitrage opportunities and enforcement challenges.

Colorado (West):

- Adult-use legal since 2014

- Moderate taxes (15% excise + 2.9% state sales)

- Competitive prices ($14–18 per item average)

- Distance from Omaha: 470 miles (7+ hours)

- Distance from western Nebraska (Scottsbluff, Alliance): 90–180 minutes

Border impact: Western Nebraska residents (Scottsbluff, Alliance, North Platte) access Colorado dispensaries. Round-trip costs $40–60 gas but savings on ounce purchase ($80–120 vs. Nebraska illicit prices) justify trip. Estimated cannabis sales flowing from Nebraska to Colorado: $25–40 million annually from western Nebraska residents.

Other borders:

- Kansas (South): Complete prohibition

- Iowa (East): Extremely limited medical program

- South Dakota (North): Medical cannabis legal, adult-use rejected

- Wyoming (Northwest): Complete prohibition

Result: Nebraska's geographic position creates less border pressure than Indiana (surrounded by legal markets) but more than Wyoming (isolated prohibition).

Medical Cannabis Program Design: The Critical First Test

Nebraska's medical cannabis implementation will determine whether the state builds foundation for comprehensive reform or repeats other states' failures.

The Implementation Timeline

Per Nebraska Medical Cannabis Commission:

- Rules and regulations: Due July 1, 2025

- License applications: Open October 1, 2025

- First licensed sales: Late 2025 or Q1 2026 (estimated)

This aggressive timeline creates challenges. The Commission should study successful medical programs (Oklahoma patient-friendly access, Arizona comprehensive regulation, New Mexico tribal integration) and avoid failures (New York licensing delays, Illinois high barriers).

License Structure: The Critical Decision

Nebraska Medical Cannabis Commission faces critical decision: Open licensing vs. limited-license monopoly?

Option 1: Open Licensing (Oklahoma Model)

- Low barriers to entry ($2,500–5,000 application fees)

- Merit-based approval (meet criteria → receive license)

- Market determines optimal number of businesses

- Oklahoma outcome: 2,000+ dispensaries for 4 million residents, rapid market saturation, intensely competitive pricing, some business failures but rapid patient access

Option 2: Limited Licensing (Illinois Model)

- Competitive application process

- High barriers to entry ($50,000–100,000 fees)

- Artificial scarcity through license caps

- Illinois outcome: 244 dispensaries for 12.8 million residents (understocked), high prices due to limited competition, political favoritism in licensing, social equity licensees struggle

Option 3: Moderate Approach (Nebraska's Best Path)

Nebraska should chart middle course:

Cultivation licenses: 15–25 licenses initially, tiered by size (Small <10,000 sq ft, Medium 10,000–25,000, Large 25,000–50,000), geographic distribution encouraged, application fee $10,000–15,000

Processing licenses: 10–15 licenses (concentrates, edibles, topicals), separate from cultivation, testing requirements mandatory, application fee $5,000–10,000

Dispensary licenses: 50–75 initially (1 per 27,000–40,000 residents), population-based allocation (Omaha 25–30, Lincoln 10–12, others distributed), local control limited (zoning only, cannot ban outright), application fee $5,000–10,000

Testing laboratory licenses: 3–5 independent labs, comprehensive panel requirements, ISO certification required, application fee $15,000–25,000

Medical Conditions: Practitioner Discretion

Initiative 437 language gives practitioners discretion to recommend cannabis when "potential benefits outweigh potential harms." This broad language is more permissive than some states' restrictive qualifying condition lists.

Commission should resist pressure to narrow access:

Restrictive state examples to avoid:

- Iowa: 4.5g THC per 90 days maximum (absurdly restrictive)

- Louisiana: Physician must register with state program (discourages participation)

- Texas: ≤0.5% THC (essentially CBD-only, not therapeutic)

Accessible state examples to emulate:

- Oklahoma: Broad practitioner discretion, rapid patient enrollment

- Arizona: Comprehensive condition list plus practitioner discretion

- Montana: Reasonable conditions, smooth implementation

Nebraska's practitioner-discretion language allows program to serve patients who benefit from cannabis without arbitrary bureaucratic barriers.

Tax Structure for Medical Program

Nebraska's optimal approach: Medical cannabis should be tax-exempt except for regular 5.5% state sales tax. No excise tax on medicine.

Rationale:

- Medicine shouldn't face sin tax

- Patients often on fixed incomes (Social Security, disability)

- Tax revenue from medical program would be modest (small patient base)

- Compassionate policy builds public support for adult-use legalization

When adult-use legalization occurs: Implement excise tax on adult-use only (15–18% rate), continue exempting medical. This creates price differential encouraging legitimate medical patients to maintain medical cards—reducing adult-use program burden on medical supply.

The Federal Policy Barrier

Nebraska cannot achieve optimized outcomes under current federal policy, regardless of state-level regulatory excellence. Two federal barriers create 25–30% performance ceiling:

The 280E Problem

Internal Revenue Code Section 280E, enacted 1982, prohibits cannabis businesses from deducting ordinary business expenses. This forces retail prices 15–20% higher just to remain viable.

Impact on hypothetical Nebraska dispensary:

- Without 280E: $800K revenue, $420K operating expenses, $140K profit, $29K federal tax, $111K net profit

- With 280E: $800K revenue, $420K NON-deductible expenses, $560K taxable income, $118K federal tax, $22K net profit

The 280E penalty destroys profitability and forces price increases. Nebraska dispensaries competing with Colorado dispensaries 470 miles west and illicit market cannot absorb this federal penalty.

Solution: Schedule III rescheduling eliminates 280E, reducing retail prices 12–18% industry-wide.

The SAFE Banking Problem

Without SAFE Banking Act passage, Nebraska financial institutions refuse cannabis business accounts. Cash-only operations create security costs ($35,000–120,000 annually), consumer friction (reduces transaction frequency 18–25%), crime risk, and payment convenience disadvantage versus Colorado dispensaries.

Nebraska-specific challenges: Omaha is major regional financial center—First National Bank of Omaha, Union Bank & Trust, major regional banks headquartered in state. Yet cannabis businesses—potentially generating $240–320M annually—cannot access normal banking.

Solution: SAFE Banking Act passage enables normal banking relationships, credit/debit card payments, online ordering, business lending, payroll efficiency, and reduced cash handling costs. Federal banking reform adds 5–8 percentage points to legal market share.

Nebraska Cannot Optimize Alone

State policy determines 70–75% of market outcomes, but federal barriers create 25–30% performance ceiling.

- Michigan: 85% legal share despite 280E/SAFE Banking barriers. With federal reform could reach 90–93%

- Illinois: 55–60% due to high state taxes compounded by 280E. With federal reform + state tax cuts could reach 75–82%

- Nebraska's optimized scenario (75–82% legal share) requires both state and federal policy alignment

Predicted Market Trajectories: IF Nebraska Legalizes Adult-Use

The framework allows prediction of Nebraska's market performance under different policy scenarios. These predictions assume medical program succeeds and Nebraska eventually legalizes adult-use (likely timeline: 2028–2032).

Optimized Scenario: Learning From Neighbors

Policy design:

- Total tax rate: 15–18% (competitive with Colorado 18%, undercuts Illinois 25–40%)

- Retail authorization: State licenses, minimal local opt-outs (preempt fragmentation)

- Density target: 65–85 dispensaries statewide (3.3–4.3 per 100K residents)

- Statewide delivery: Mandatory for areas >25 miles from nearest dispensary

- Testing standards: Comprehensive (pesticides, heavy metals, microbials, potency)

- Enforcement budget: $10–15M annually ($5–7.50 per capita) targeting illegal grows

- Assumes: Federal Schedule III (280E elimination) + SAFE Banking passage

Framework inputs:

- Price competitiveness: g = -0.20 (legal 20% cheaper than illicit)

- Access density: D = 0.75 (65–85 stores + delivery covers 80%+ population)

- Safety/quality: S = 0.80 (comprehensive testing, professional regulation)

- Convenience: F = 0.75 (SAFE Banking enables cards, online ordering)

- Enforcement: E = 0.70 (strong interdiction capability, political will)

- Fragmentation: F_frag = -0.12 (minimal local bans due to state preemption)

Predicted outcomes:

- Transaction share: 80–86% (consumers choosing legal over illicit)

- Volume share: 75–82% (accounting for heavy user preferences)

- Timeline: 42–54 months to reach steady state

Economic impact:

- Adult cannabis consumers: 180,000–240,000 (9–12% of adults aged 21+)

- Legal market size: $240–320M annually (mature market)

- State tax revenue: $40–55M annually (at 15–18% rate)

- Jobs: 2,400–3,200 direct + indirect

- Illicit market: Reduced from $310–380M to $60–95M (75–80% reduction)

Comparable performance: Nebraska would achieve outcomes similar to Michigan (85% legal share), Colorado with federal reform (84–88% projected), Montana (78–82%).

This represents best-case Nebraska: Learning from neighbors' mistakes, implementing evidence-based policy, leveraging structural advantages, benefiting from federal reform.

Failed Scenario: Illinois Redux (High-Tax Disaster)

Policy design:

- High tax rate: 25–35% (attempting to maximize per-unit revenue)

- Limited retail licenses: Political favoritism, artificial scarcity

- No statewide delivery: Local control prevents mandate

- Weak enforcement: Budget constraints or political deprioritization

- 280E remains in effect (no federal Schedule III)

Predicted outcomes:

- Transaction share: 58–65%

- Volume share: 52–60%

- Comparable to: Illinois (55–60%), Washington (65%)

Economic impact:

- Legal market: $160–210M annually (underperformance)

- Tax revenue: $40–63M annually (high rate, smaller base—similar total to optimized scenario but worse outcomes)

- Jobs: 1,600–2,200 (fewer opportunities)

- Illicit market: $180–240M (persistent competition)

This represents policy failure: Nebraska legalizes but replicates Illinois's high-tax mistakes, ensuring legal market cannot compete on price, persistent black market, unrealized economic potential.

Most Likely Scenario: Conservative Competence

Nebraska's political culture suggests cautious-but-thoughtful implementation if legalization occurs:

Policy design:

- Moderate tax: 18–22% (competitive but not optimal)

- Phased licensing: Medical-first approach, adult-use contingent on success

- Controlled rollout: Limited initial dispensaries, expansion based on demand

- Strong regulatory oversight: Typical Nebraska bureaucratic thoroughness

- Enforcement applied: Existing capacity redirected to illegal operators

Predicted outcomes:

- Transaction share: 72–78%

- Volume share: 68–75%

- Timeline: 54–66 months (slower rollout than optimized)

Economic impact:

- Legal market: $215–285M annually

- Tax revenue: $43–57M annually (at 18–22% rate)

- Jobs: 2,000–2,800

- Illicit market: $95–140M (reduced but not eliminated)

This represents good-but-not-optimal: Better than Illinois, not quite matching Michigan. Nebraska's fiscal conservatism produces competent but not excellent outcomes—avoiding disasters while missing optimization opportunities.

Policy Recommendations: The Nebraska Path Forward

If Nebraska moves toward adult-use legalization (likely 2028–2032), evidence-based policy recommendations:

Priority #1: Competitive Tax Structure

Recommendation:

- State excise tax: 12–15%

- State sales tax: 5.5% (existing rate applies)

- Total state burden: 17.5–20.5%

- Local option: 2–3% maximum (capped to prevent stacking)

- Total effective rate: 19.5–23.5% (competitive with Colorado 18%, undercuts Illinois 25–40%)

Rationale: Revenue optimization comes through volume (market share) not rates. Lower taxes → lower prices → higher legal market share → more transactions → more total revenue. Nebraska must price-compete with Colorado (18% total, 470 miles west) and illicit market (zero taxes). Research across 24 states demonstrates cannabis consumers are highly price-sensitive, with 10% legal price increases reducing legal choice probability by 2.3%.

Priority #2: Statewide Access Without Fragmentation

Recommendation:

- State-issued retail licenses (Nebraska Department of Revenue oversight)

- Target: 65–85 dispensaries statewide (3.3–4.3 per 100K residents)

- Geographic distribution: Omaha metro 35–42 stores, Lincoln metro 12–16 stores, Grand Island-Kearney 4–6 stores, Regional coverage 14–21 stores

- Statewide delivery mandatory for areas >25 miles from retail location

- Municipalities: Can regulate zoning/buffers, CANNOT ban retail outright

- State preemption: Prevents California-style fragmentation (61% local bans)

Rationale: Prevent California fragmentation disaster. Nebraska lacks strong home rule tradition—state preemption politically feasible. Unicameral legislature simplifies passage. Delivery critical: 33% of Nebraskans in rural areas. Without delivery mandate, fragmentation penalty reduces legal share by 12–18 percentage points.

Priority #3: Leverage Enforcement Strengths

Recommendation:

- Budget: $10–15M annually dedicated to illicit supply interdiction ($5–7.50 per capita)

- Focus: Large-scale illegal cultivation (500+ plants), unlicensed retail, interstate trafficking

- Avoid: Consumer harassment, small-scale home cultivation (if permitted)

- Coordination: Nebraska State Patrol + county sheriffs + federal DEA cooperation

Rationale: Nebraska's existing law enforcement culture becomes competitive advantage. States with strong interdiction (Nevada, Michigan, Colorado) outperform weak-enforcement states (California, New York) by 15–25 percentage points. Budget $10–15M enforcement generates 5–7× return through higher legal market share (more tax revenue), public safety improvement (tested products), criminal justice cost reduction (fewer prosecutions), interstate trafficking reduction.

Priority #4: Banking and Payment Flexibility

Recommendation:

- State-chartered financial institutions: Incentivize cannabis banking through state-backed insurance fund

- Credit unions: Encourage formation of cannabis-focused credit union (Colorado model)

- Federal advocacy: Nebraska Congressional delegation push SAFE Banking Act

- State workaround: Explore state-backed payment processing system if federal reform stalls

Rationale: Banking access improves convenience factor by 15–22% in framework. Card payments increase transaction frequency, reduce security costs, enable delivery infrastructure. Nebraska is regional financial center—has institutional capacity for innovative solutions. State-chartered banks could serve cannabis industry with state backing reducing federal risk.

Priority #5: Home Cultivation Decision

Two viable approaches depending on political feasibility:

Option A: Prohibit Home Grow Initially

- Medical patients: No home cultivation (dispensary-only)

- Adult-use: No home cultivation

- Review after 3 years based on market performance

- Rationale: Simpler regulation, easier law enforcement, higher legal market share

Option B: Restricted Home Cultivation

- Medical patients: 6 plants maximum (3 mature, 3 immature)

- Adult-use: 3 plants maximum (1 mature, 2 immature) per adult, 6 per household maximum

- Enclosed locked facility required (no outdoor grows)

- Registration optional but provides affirmative defense

Framework analysis: Home cultivation reduces legal market share by 3–7 percentage points when permitted. However, prohibition creates enforcement challenges and appears authoritarian to cannabis supporters. Nebraska's conservative political culture suggests Option A (prohibition) more politically palatable initially. Can liberalize later based on experience.

Comparison to Other Markets

How does Nebraska's predicted performance compare to existing legal markets?

High-Performing States (80%+ Legal Share)

Michigan: 85% Legal Share

- Success factors: Moderate taxes (16% total), strong enforcement, good access density

- Similarity to Nebraska: Geographic concentration, enforcement capacity, moderate conservative culture

- Key lesson: Moderate taxes + strong enforcement outperform progressive social goals alone

Oregon: 82% Legal Share

- Success factors: Low taxes (17% total), excellent access density, minimal fragmentation

- Difference from Nebraska: Oregon more progressive culture, over-saturated retail

- Key lesson: Low taxes enable legal market dominance even in challenging conditions

Nevada: 75–80% Legal Share

- Success factors: Competitive prices, strong enforcement, tourism amplification

- Similarity to Nebraska: Strong enforcement culture, revenue-focused governance, concentrated population

- Key lesson: Conservative governance can produce excellent cannabis policy when revenue-motivated

Mid-Tier States (65–75% Legal Share)

Colorado: 73–78% Legal Share

- Performance: Strong but declining from 2021 peak

- Similarity to Nebraska: Moderate conservative culture, established enforcement, geographic concentration

- Key lesson: First-mover advantage fades without continuous policy optimization

Washington: 65% Legal Share

- Underperformance despite 2012 legalization: High taxes (37% excise), enforcement gaps

- Key lesson: High taxes undermine legal market regardless of other policy strengths

Struggling States (40–60% Legal Share)

Illinois: 55–60% Legal Share

- Underperformance causes: Excessive taxes (25–40%), limited access, 280E burden, weak enforcement

- Key lesson for Nebraska: Avoid Illinois's high-tax mistake—cannot tax your way to successful legal market

California: 50% Legal Share

- Failure factors: Extreme fragmentation (61% local bans), high taxes, weak enforcement

- Key lesson: Market size doesn't guarantee legal market success—policy quality determines outcomes

New York: 30% Legal Share

- Policy crisis: Licensing delays, enforcement gaps, illegal shops proliferating

- Key lesson: Ideological goals without pragmatic implementation guarantee failure

Where Nebraska Fits

Nebraska's predicted 75–82% optimized legal market share would place it among high-performing states: Michigan (85%), Oregon (82%), Nebraska (75–82%), Nevada (75–80%), Colorado (73–78%)

Most likely scenario (68–75% legal share) would place Nebraska in mid-to-high tier: Michigan (85%), Oregon (82%), Nevada (75–80%), Nebraska (68–75%), Colorado (73–78%), Washington (65%)

Even in conservative implementation, Nebraska avoids bottom-tier performance of Illinois (55–60%), California (50%), New York (30%)—IF it learns from neighbors' mistakes.

Timeline and Path Forward

Realistic timeline for Nebraska cannabis reform:

Phase 1: Medical Program Implementation (2025–2026)

2025:

- Q1: Nebraska Medical Cannabis Commission establishes rules (due July 1)

- Q2–Q3: Application period opens (October 1), license review process

- Q4: First cultivation licenses approved, facility construction begins

2026:

- Q1: First medical dispensaries open (late 2025 or early 2026 projected)

- Q2–Q3: Supply chain stabilization, patient enrollment growth

- Q4: Program evaluation, rule adjustments based on experience

Success metrics: 15,000–25,000 registered patients by end of Year 1, 30–50 licensed dispensaries operational, $35–60M in medical sales annually (mature), zero major regulatory scandals.

Phase 2: Medical Program Maturation (2027–2029)

Key developments:

- Patient base expands to 40,000–60,000 (2–3% of adult population)

- Supply chain matures, wholesale prices stabilize

- Tax revenue demonstrates fiscal benefits ($8–15M annually from medical)

- Federal Schedule III rescheduling occurs (probable 2026–2027)

- SAFE Banking Act passes (probable 2026–2028)

Political evolution:

- Governor Pillen's term ends (2027)—successor's position critical

- Legislative discussions begin on adult-use framework

- Business community supports expansion

- Law enforcement reports medical program hasn't increased crime or youth usage

Phase 3: Adult-Use Legalization (2030–2032 Most Likely)

Pathway options:

Option A: Legislative Action (Most Likely)

- Nebraska's unicameral legislature can pass adult-use bill if federal government reschedules cannabis, medical program demonstrates success, fiscal pressures create revenue need, neighboring states' success becomes undeniable

- Timeline: 2029–2031 legislative session

Option B: Ballot Initiative (Less Likely)

- Nebraska allows citizen-initiated ballot measures but requirements stringent (10% of registered voters, single-subject rule)

- Timeline: 2030–2032 election cycle

Option C: Federal Pressure (Possible)

- If federal government legalizes cannabis or moves to Schedule III, state prohibition becomes economically untenable

- Timeline: 2028–2032 timeframe

Phase 4: Adult-Use Market Launch (2032–2034)

Assuming adult-use legalization passes 2030–2031:

Implementation timeline:

- Year 1 (2031–2032): Regulatory development, license applications, facility expansion

- Year 2 (2032–2033): First adult-use sales, market adjustment, supply scaling

- Year 3 (2033–2034): Market stabilization, steady-state operations achieved

- Year 4 (2034–2035): Full mature market, 75–82% legal share achieved (optimized scenario)

Success indicators: Tax revenue $40–55M annually from adult-use (optimized), jobs 2,400–3,200 positions, legal market share 75–82% (optimized) or 68–75% (most likely), illicit market reduced by 75–80%.

Economic Reality: What Nebraska Stands to Gain (or Lose)

Current State: Prohibition Costs

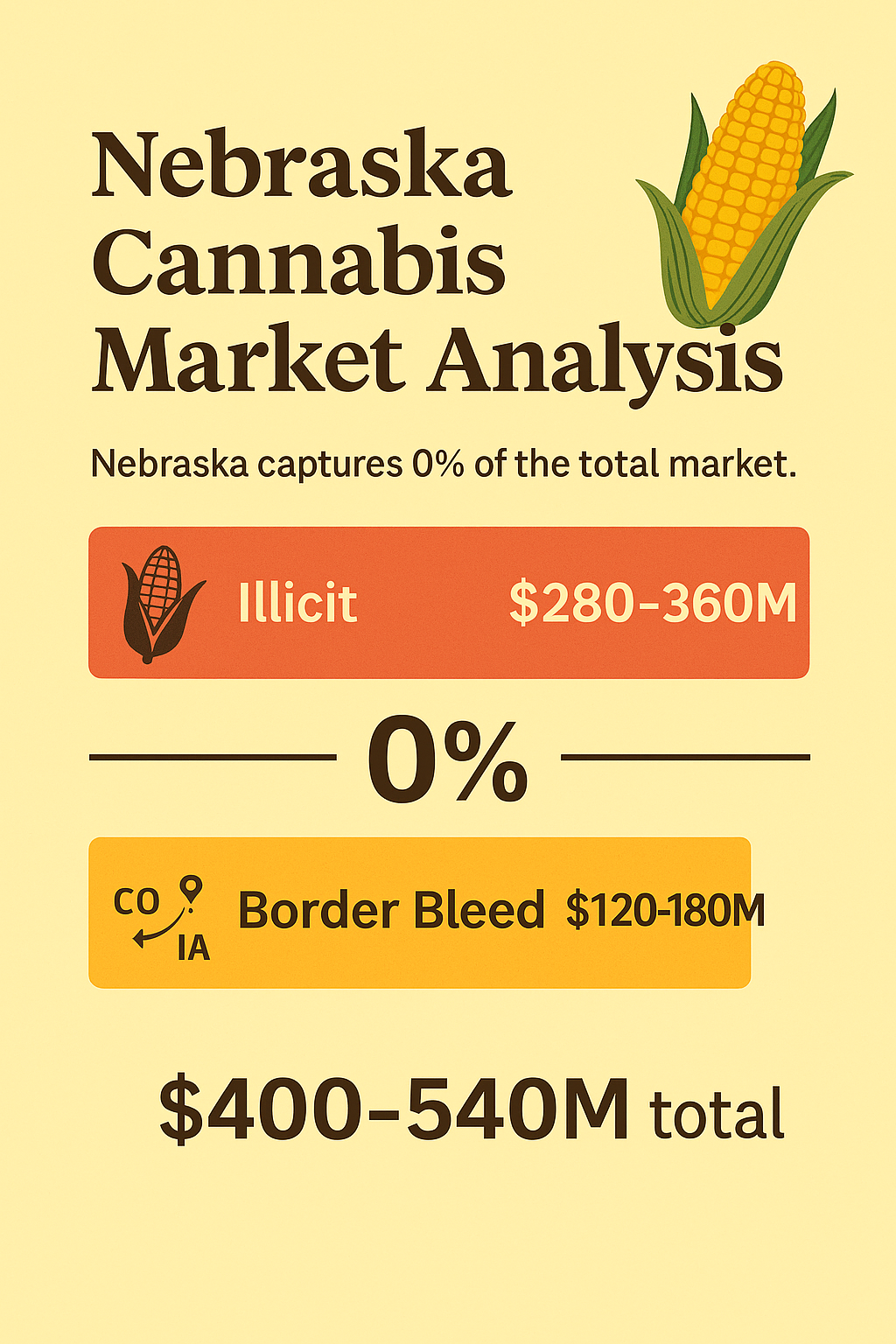

Annual cannabis demand (estimated):

- Adult consumers: 180,000–240,000 Nebraskans (9–12% of adults 21+)

- Total market size: $310–380M annually (all illicit)

- Average per consumer: $1,400–1,800 annually

Foregone tax revenue: At 18% tax rate: $56–68M annually. Current revenue: $0

Criminal justice costs: First-offense citations 3,000–4,000 annually, court processing $450K–1.2M annually, felony prosecutions (concentrates, cultivation) add $1–3M annually. Total prohibition cost: foregone tax revenue $56–68M, criminal justice expenses $1.5–4M, economic activity lost $310–380M not circulating in-state, jobs not created 2,400–3,200 positions.

Border state losses: Western Nebraska residents shopping Colorado: $25–40M annually. Lost tax revenue to Colorado: $5–8M annually.

Medical Program Economics (2026–2030)

Patient enrollment projections:

- Year 1 (2026): 15,000–20,000 patients

- Year 2 (2027): 25,000–35,000 patients

- Year 3 (2028): 35,000–50,000 patients

- Mature market: 40,000–60,000 patients (2–3% of adults)

Market size: Average patient spending $2,000–3,000 annually. Mature market revenue $80–150M annually.

Tax revenue (if medical taxed at 5.5% sales tax only): Annual state revenue $4.4–8.25M

Jobs created: Direct (cultivation, processing, retail, testing) 800–1,200. Indirect (construction, security, legal, accounting) 300–500. Total 1,100–1,700 jobs.

Patient benefits: Access to legal medicine 40,000–60,000 patients. Reduced opioid use: Studies show 20–25% reduction in opioid prescriptions in medical states.

Optimized Adult-Use Market Economics (2034+)

Market size:

- Adult-use sales: $240–320M annually

- Medical sales: $60–90M annually (patients maintain cards for tax exemption)

- Total legal market: $300–410M annually

State tax revenue:

- Adult-use (18% effective rate): $43–58M

- Medical (5.5% sales tax): $3.3–5M

- Total state cannabis revenue: $46–63M annually

Jobs:

- Direct cannabis jobs: 2,400–3,200

- Indirect/induced: 1,800–2,500

- Total employment impact: 4,200–5,700 jobs

Illicit market reduction: Current illicit market $310–380M. Post-legalization illicit $60–95M. Reduction: $250–285M (75–82% decrease).

Criminal justice savings: Arrests eliminated 3,000–4,000 annually. Court costs saved $450K–1.2M annually. Incarceration costs saved $500K–1.5M annually.

Economic multiplier: Every $1 in dispensary sales generates $1.50–1.80 in total economic activity. $300–410M dispensary sales → $450–740M total economic impact.

Federal reform amplification: Schedule III + SAFE Banking adds additional 10–15 percentage points to legal market share, additional tax revenue $8–12M annually, additional jobs 400–600 positions, further illicit market reduction to 85–90% vs. current.

Conservative vs. Progressive Fiscal Impact

Optimized implementation: Tax revenue $46–63M annually, jobs 4,200–5,700, legal market share 75–82%, illicit market reduction 75–82%, 10-year economic impact $4.5–6.3B in economic activity.

Failed implementation (Illinois model): Tax revenue $40–55M annually (similar total, worse outcomes), jobs 2,800–3,800, legal market share 52–60%, illicit market reduction 50–60%, 10-year economic impact $2.8–3.8B in economic activity.

The difference: $1.7–2.5B in economic activity over decade, 1,400–1,900 fewer jobs, persistent black market competition. Policy quality matters more than ideology.

Conclusion: Nebraska's Choice

Nebraska voters made their decision November 5, 2024: 70.74% demanded medical cannabis access. Two-thirds of Nebraskans—across partisan, geographic, and demographic divides—said prohibition has failed.

Now state leadership faces choice: Implement the voters' will competently or obstruct through continued litigation and regulatory hostility?

The framework reveals what's possible: Nebraska possesses structural characteristics favoring legal market success. Geographic concentration in Omaha-Lincoln corridor enables efficient retail coverage. Strong law enforcement culture can be redirected toward illegal operations rather than consumers. Fiscal conservatism incentivizes revenue optimization over ideological posturing. Clean regulatory slate allows implementation of best practices without legacy program constraints.

IF Nebraska:

- Successfully implements medical cannabis program (survives Supreme Court challenge, opens dispensaries 2025–2026)

- Learns from neighbors' policy mistakes (avoids Illinois high-tax disaster, prevents California fragmentation)

- Benefits from federal reform (Schedule III eliminates 280E burden, SAFE Banking enables card payments)

- Eventually legalizes adult-use (probable 2028–2032 timeline)

THEN Nebraska achieves 75–82% legal market share within 48 months of adult-use launch—matching or exceeding Michigan, outperforming Colorado, dramatically surpassing Illinois.

The alternative: Nebraska continues prohibition, loses $56–68M annually in tax revenue, arrests thousands for behavior 24 states have legalized, watches western residents drive to Colorado dispensaries, maintains persistent black market enriching criminal enterprises rather than state coffers.

Nebraska's November 2024 vote wasn't about cultural progressivism. It was pragmatic recognition that prohibition has failed and patients deserve legal access to medicine. The same pragmatic conservatism that built Nebraska's agricultural economy and strong communities should guide cannabis policy.

70%+ of Nebraskans understand what works. The question is whether state leadership will listen.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Missouri | Pennsylvania | Vermont | Mississippi

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0