Nevada Cannabis Market Analysis: Tourism's Double-Edged Sword and the Illicit Market Resurgence

The state that launched recreational cannabis in the West now watches sales decline for four straight years while the illicit market captures 30% of demand—proving first-mover advantage means nothing without sustained optimization

The Silent Majority 420 | November 2025

The Nevada Paradox: From Pioneer to Problem Child

Nevada made history July 1, 2017, launching recreational cannabis sales mere six months after voters approved Question 2. The state that built an economy on vice legalization—gambling, alcohol, adult entertainment—seemed perfectly positioned to dominate legal cannabis.

Eight years later, the results are deeply troubling.

Nevada's legal cannabis market peaked at $1.004 billion in fiscal year 2021. Since then, sales have declined every single year: FY 2022 ($965M, -4%), FY 2023 ($900M, -7%), FY 2024 ($829 million, -8%). A 25% revenue decline in four years while Nevada's population grew 5.4% and Las Vegas tourism recovered to 41.7 million visitors annually.

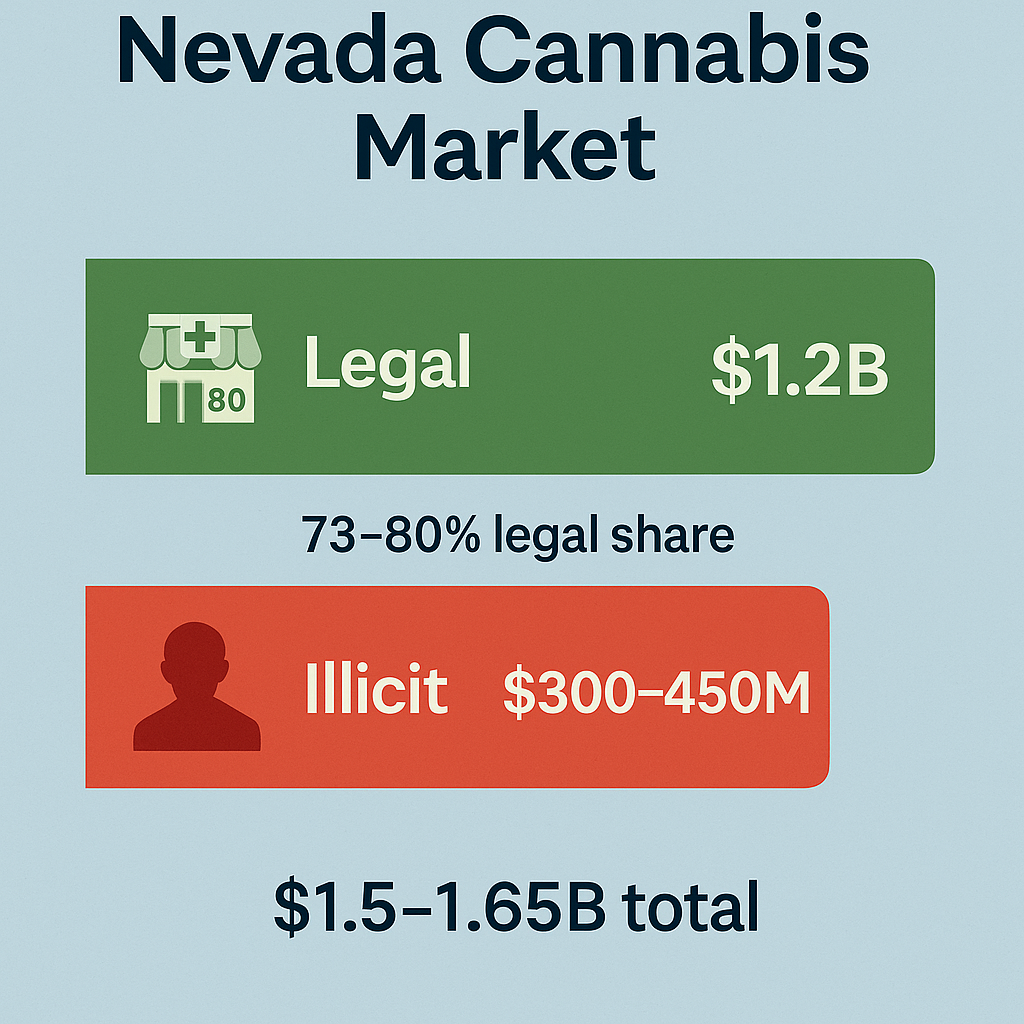

Meanwhile, Nevada's illicit cannabis market generates $242–370 million annually, representing 25–33% of total cannabis demand—among the highest illicit market shares in the Western United States. The Nevada Cannabis Compliance Board (CCB) produced its first comprehensive illicit market analysis in September 2024, finally acknowledging what industry operators have warned about for years.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Nevada's core problem: The state optimized for tourism subsidy but neglected fundamentals. Nevada's cannabis market performs well for Strip visitors making impulse purchases but fails catastrophically for residents facing 33% effective tax rates, just 8 POST-certified enforcement agents for a billion-dollar market, and openly operating illicit delivery services advertising on Instagram.

Nevada currently achieves 67–75% legal market share—better than California (50%) or Illinois (55–60%), but worse than neighboring Arizona (75–80%), Oregon (82%), and Colorado (73–78%). More troubling: Nevada's share is declining as illicit operators exploit policy failures.

The framework predicts Nevada could achieve 80–85% legal market share with comprehensive optimization—but only if the state addresses four critical failures:

- Punitive taxation: 15% wholesale + 10% retail + ~8% sales = 33% total burden

- Enforcement collapse: 8 agents cannot police $1B+ market with $242–370M illicit competition

- Tourism dependency: 73% of population in Las Vegas metro pays same high taxes as tourists

- Federal 280E burden: Inflates prices 15–20%, undermining competitiveness

Nevada's crisis proves a harsh lesson: Early-mover advantage dissipates quickly without sustained optimization. But the state can reclaim leadership through aggressive policy reform—IF policymakers act before the window closes.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Nevada's Structural Characteristics: Tourism's Double-Edged Sword

Nevada enters cannabis market analysis with unique characteristics that simultaneously enable success and create vulnerabilities.

The Tourism Subsidy: Unique Market Amplifier

Las Vegas tourism statistics (2024):

- Annual visitors: 41.7 million

- Average stay: 3.4 nights

- Strip dominance: 88% of gambling occurs on Strip

Cannabis tourism subsidy: Strip dispensaries benefit from massive foot traffic—40+ million annual tourists passing between casinos and hotels. This creates artificial demand elasticity: Tourists pay premium prices for convenience without price sensitivity.

Estimated tourism share: 35–45% of Nevada cannabis sales (approximately $290–370M at FY2024 levels). Nevada residents (3.2 million) generate less revenue than 41.7 million annual tourists—a 12:1 visitor-to-resident ratio producing roughly 1:1 sales ratio.

Framework significance: Tourism subsidy masks resident market failure. Nevada policymakers view $829M in sales and assume success, but decomposition reveals tourist market stable while resident market collapses. If tourism disappeared (pandemic-style), Nevada's legal market would shrink 40–50%—revealing structural fragility.

Geographic Concentration: Efficient but Fragile

Nevada population distribution:

- Clark County (Las Vegas metro): 2.4 million (73% of state)

- Washoe County (Reno-Sparks): 480,000 (15% of state)

- Rural Nevada: 320,000 (12% of state)

Dispensary distribution:

- Clark County: 90+ dispensaries (87% of state total)

- Washoe County: 10–12 dispensaries

- Rural Nevada: <5 total

Framework significance: Extreme concentration creates efficient retail coverage (73% of population served by 87% of dispensaries) but also market vulnerability. Nevada functions essentially as Las Vegas cannabis market with small Northern appendage—unlike states with multiple metros (California, Arizona).

Strong Regulatory Infrastructure

Nevada maintains rigorous testing standards through licensed laboratories, METRC track-and-trace from cultivation through retail, and vertical integration enabling operational efficiencies. Product safety scandals have been minimal compared to other markets, building consumer confidence.

Framework significance: Safety/quality score (S): 0.82—one area where Nevada maintains excellence.

What Limits Optimization

Punitive tax structure:

- 15% wholesale excise tax (cultivation level)

- 10% retail excise tax (adult-use sales)

- 6.85% state sales tax + 1–2% local = ~8% total sales tax

- Combined burden: 33–35% on adult-use cannabis

Nevada imposes one of the highest effective tax burdens in the Western United States. Comparison: Oregon (17%), Colorado (20–25%), Arizona (16% + sales), California (recently reduced to ~23%), Nevada (33–35%).

Enforcement collapse: Just 8 POST-certified enforcement agents for entire state—catastrophically insufficient for:

- 387 licensed facilities (compliance monitoring)

- Unknown number of illicit cultivation sites

- Unlicensed delivery services (operating openly via Instagram, Telegram)

- Interstate trafficking (California imports, Arizona exports)

Comparison to other states:

- Michigan (10M population): 50+ enforcement agents

- Colorado (5.8M population): 40+ enforcement agents

- Nevada (3.2M population): 8 enforcement agents

Nevada has 1/5th to 1/6th the per-capita enforcement capacity of comparable states. CCB acknowledges enforcement division "needs more resources" but lacks budget.

Resident-tourist pricing conflict: Tourists will pay $60/eighth; residents won't. Yet both face same 33% tax burden. Nevada has no mechanism for differential taxation despite fundamentally different price sensitivities.

Current Market Performance (2025): The Decline Continues

Sales Trajectory

Fiscal year performance:

- FY 2021 (peak): $1.004 billion

- FY 2022: $965M (-3.9%)

- FY 2023: ~$900M (-6.7%)

- FY 2024: $829M (-7.9%)

- FY 2025 (projected): $758M (-8.6%)

Cumulative decline from peak: 24.5% over four years. This occurred despite Nevada population growth (+5.4%), Las Vegas visitor recovery (41.7M), and U.S. cannabis market growth (+15–20% nationally).

Tax revenue impact: FY 2024 cannabis tax revenue: $108 million transferred to State Education Fund from retail excise tax. Declining sales directly impact school funding—Nevada's education system depends on cannabis revenue eroding 7–9% annually.

The Illicit Market Crisis

CCB illicit market analysis (September 2024):

- Annual illicit sales: $242–370 million

- Share of total market: 25–33%

- Growth trajectory: Expanding (as legal market contracts)

Primary illicit sources:

- Legacy dealers (pre-legalization networks)

- Unlicensed delivery services (Instagram, Telegram advertising)

- Home cultivation excess (Nevada allows 6 plants/adult; some exceed limits)

- California imports (wholesale arbitrage)

Price differential: Legal dispensaries average $40/eighth. Illicit market estimates: $5/eighth according to UNLV Cannabis Policy Institute research—an 800% price advantage for illicit sellers.

Consumer perception: CCB report notes consumers "distrust the legal market, finding products less potent and more expensive, and did not connect increased government oversight to increased safety." This perception gap drives illicit market growth.

Price Collapse and Market Composition

The UNLV Cannabis Policy Institute's 2024 Nevada Cannabis Economy Overview, produced in partnership with UC Davis Cannabis Economics Group, provides detailed analysis of Nevada's price dynamics and structural challenges.

Price decline acceleration (May 2023 to May 2024):

- Ordinary flower: -21.4% ($6.18/gram → $5.11/gram)

- Small buds: -7.1%

- Solvent-based concentrates: -27% (vape cartridges, distillates)

- Solventless concentrates: -2% (premium live resin, live rosin)

- Edibles: -11.1%

- Pre-rolls: +1.2% (only category with rising prices)

The infused pre-roll phenomenon: While ordinary pre-rolls declined slightly, infused pre-rolls (dusted with THC crystals or concentrate) showed rising prices AND rising volumes—the only product category with simultaneous growth in both metrics. UNLV analysis suggests consumer shift toward higher-potency products, with retailers reporting difficulty selling flower below 20% THC.

Market composition by revenue (FY 2024):

- Flower/small buds: 45%

- Concentrates: 33%

- Pre-rolls (including infused): 12%

- Edibles: 12%

Wholesale price crisis: Nevada wholesale flower averaged $1,270–1,350 per pound in 2023–2024—more than double neighboring states:

- California: $646/lb

- Oregon: $588/lb

- Arizona: $584/lb

- Washington: $777/lb

Why Nevada costs double: Over 80% of Nevada cannabis is indoor-grown (most expensive cultivation method) versus neighboring states where outdoor and greenhouse cultivation dominate. Nevada's geography—extreme heat, scarce water, expensive electricity—makes outdoor cultivation challenging. This creates structural cost disadvantage versus California's Humboldt County or Oregon's Willamette Valley.

Retail-wholesale margin compression: As retail prices fell faster than wholesale prices, dispensary margins declined from 110% to below 100% during 2023. Lower margins mean reduced operating capital for compliance, security, and quality control—forcing some operators toward cost-cutting that undermines legal market advantages.

UNLV conclusion: "Nevada's wholesale prices still have much further to fall... the decline will likely be nonlinear, with steep cliffs generated by regulatory changes such as interstate commerce." When interstate trade becomes legal, Nevada cultivators face existential threat—competing against California outdoor flower at $200/lb versus Nevada indoor at $1,300/lb.

2025 Legislative Session: Missed Enforcement Opportunity

Nevada's 2025 legislative session addressed cannabis market challenges with mixed results.

AB 504 (PASSED) - Hemp Products to Dispensaries Only:

- Change: Intoxicating hemp-derived products (Delta-8, Delta-9, Delta-10, THC-O, HHC) must be sold exclusively through licensed dispensaries

- Rationale: Eliminates gas station/convenience store sales of unregulated intoxicating products

- CBDT Impact: +0.5 to +1.0 pp (channels intoxicating products through tested/taxed system, eliminates unregulated competition)

- Status: Signed into law, effective 2025

AB 76 (FAILED) - CCB Enforcement Authority:

- Proposed: Authorize Cannabis Compliance Board to issue subpoenas and summonses to unlicensed cannabis sellers

- Rationale: CCB currently lacks tools to compel testimony/evidence from illicit operators

- CBDT Impact if passed: +0.5 to +1.0 pp from enhanced enforcement capability

- Status: Passed committees, referred to budget committee, never received floor vote (effectively dead)

- Why failed: Budget constraints—no agency wants unfunded enforcement mandates

AB 203 (FAILED) - DPS Enforcement Expansion:

- Proposed: Add enforcement responsibilities for Department of Public Safety

- Status: Passed committee, stuck in budget (no floor vote)

- Impact: Would have coordinated state-level enforcement targeting large illicit operations

Story of 2025 session: Nevada passed smart hemp regulation (AB 504) but failed to fund enforcement expansion (AB 76, AB 203) despite industry and CCB advocacy. Political will exists but fiscal constraints prevent action.

Consumption Lounges: Implementation Failure

Background: Nevada authorized cannabis consumption lounges through AB 341 (2021)—one of few states permitting on-site consumption. CCB projected 60–65 licenses would be issued.

Current status (November 2025): Only 1 state-licensed lounge operates statewide—Dazed! inside Planet 13 in Las Vegas. Smoke and Mirrors opened in 2024 but has since closed. Tribal-regulated facilities (like Nuwu) operate independently and aren't counted in state totals.

Barriers preventing lounge openings:

- $200K minimum liquidity requirement (blocking social equity applicants)

- Lengthy licensing process (2–3 years from application to opening)

- Property owner resistance (many landlords won't lease to cannabis businesses)

- Complex zoning/fire safety regulations

CBDT significance: Consumption lounges theoretically add +0.3 to +0.5 pp to legal market share (improved convenience, tourism enhancement), but actual impact near zero due to implementation failure. Las Vegas thrives on on-premises consumption (casinos, bars, nightclubs)—cannabis lounges fit perfectly but remain unrealized potential.

Tourism opportunity: UNLV Cannabis Policy Institute analysis emphasizes that "consumers like to go out and spend money in groups and, especially in Las Vegas, they spend large amounts on out-of-home food and beverage purchases." On-premise alcohol venues command 3× to 10× markups over retail—cannabis lounges integrated with entertainment could capture similar premiums while increasing legal market capture from tourists currently using illicit delivery.

CCB response: Held resource fair November 2025 for 21 conditional license holders who haven't opened, signaling awareness of implementation challenges.

The Federal Policy Barrier

Nevada cannot achieve optimized outcomes under current federal policy, regardless of state-level regulatory excellence.

The 280E Problem

Internal Revenue Code Section 280E, enacted 1982, prohibits cannabis businesses from deducting ordinary operating expenses. Combined with Nevada's 33% state tax burden, 280E forces retail prices 40–50% above economic equilibrium.

Nevada dispensary example (Strip location):

- Revenue: $2,500,000

- COGS (deductible): $750,000

- Operating expenses (NON-deductible): $1,400,000 (rent, payroll, security, insurance)

- Without 280E: $350K profit → $73.5K federal tax → $276.5K net

- With 280E: $1,750K taxable income → $367.5K federal tax → -$117.5K loss

Nevada's high operating costs (Strip rent premium, elevated security for cash operations) amplify 280E impact beyond other states. Dispensaries must inflate prices 40–50% just to survive—making illicit market price advantage insurmountable.

Solution: Schedule III rescheduling eliminates 280E, allowing normal business deductions. Nevada dispensaries could reduce prices 20–25% while maintaining profitability.

The SAFE Banking Problem

Without SAFE Banking Act passage, Nevada cannabis businesses operate cash-based, creating security costs ($50K–150K per dispensary), consumer friction (reduces transaction frequency 18–25%), and payment disadvantages versus illicit delivery accepting Venmo/Zelle.

Nevada-specific impact: Tourism context magnifies cash friction. Tourists carry cash for gambling, but suburban residents prefer card payments. Cash withdrawal specifically for cannabis is inconvenient—illicit delivery ironically more convenient than legal cash-only.

Solution: SAFE Banking enables credit/debit card payments, reduces cash handling costs 50–60%, improves consumer convenience, and adds 4–6 percentage points to legal market share.

Predicted Market Trajectories

The framework allows prediction of Nevada's market performance under different policy scenarios.

Current Trajectory: Continued Decline

If Nevada maintains current policies:

2027–2028 projection:

- Legal sales: $680–720M annually (-15–20% from 2025)

- Illicit market growth: $320–400M annually

- Legal market share: 62–68% (declining)

- Tax revenue: $90–100M annually (education funding crisis)

Drivers of decline:

- Price-sensitive residents continue migrating to illicit market

- Enforcement vacuum allows illicit expansion

- Word-of-mouth networks accelerate illicit adoption

- 280E + high state taxes make legal price competitiveness impossible

Tourism buffer: Strip dispensaries survive (tourists price-insensitive) but resident-focused dispensaries face consolidation or closure. Nevada risks bifurcated market: strong tourism component, dead resident market.

Optimized Scenario: Nevada Reclaims Leadership

Policy changes required:

- Tax reform: Reduce retail excise 10% → 5%, target 25% total burden (from 33%)

- Enforcement surge: Triple agents 8 → 25, budget $10–15M annually

- Delivery infrastructure: Streamline licensing, third-party delivery, same-day standard

- Consumption lounge acceleration: Fast-track licensing, casino integration

- Federal reform: Schedule III + SAFE Banking

Framework inputs (optimized):

- Price competitiveness: g = -0.18 (legal 18% cheaper after reforms)

- Access density: D = 0.82 (delivery fills gaps)

- Safety/quality: S = 0.82 (maintain standards)

- Convenience: F = 0.78 (SAFE Banking + delivery)

- Enforcement: E = 0.75 (25 agents, focused strategy)

- Fragmentation: F_frag = -0.06 (rural improvements)

Predicted outcomes:

- Transaction share: 81–85%

- Volume share: 80–85%

- Timeline: 36–48 months after reforms implemented

Economic impact (optimized state):

- Legal market: $1.1–1.2B annually (return to FY2021 levels)

- Resident market growth: $580–650M (from current $460–480M)

- Tourism market: $450–500M (maintain current)

- State tax revenue: $160–180M annually

- Illicit market: $180–220M (reduced 40–50%)

Comparable performance: Optimized Nevada would match Arizona (75–80%), approach Colorado (73–78%), rival Oregon (82%).

Most Likely Scenario: Partial Reform

Nevada's political culture suggests cautious optimization over next 5 years:

Policy design:

- Moderate tax reduction: 10% → 7% retail excise (not optimal 5%)

- Enforcement increase: 8 → 15 agents (not optimal 25)

- Delivery expansion: Limited third-party licensing

- Consumption lounges: Slow growth (5–10 operational by 2030)

- Federal reform: IF occurs (not guaranteed)

Predicted outcomes:

- Transaction share: 74–78%

- Volume share: 72–76%

- Timeline: 48–60 months (slower than optimized)

Economic impact:

- Legal market: $950M–1.05B annually

- Tax revenue: $140–160M annually

- Illicit market: $220–280M (reduced but persistent)

This represents good-but-not-optimal: Better than current trajectory, worse than full optimization. Nevada avoids catastrophe but misses leadership reclamation opportunity.

Policy Recommendations: Reversing the Decline

Nevada can reverse market decline through strategic, phased reforms.

Priority #1: Tax Reform (Immediate)

Recommendation: Reduce retail excise tax from 10% to 5%. Total burden reduction: 33–35% → 28–30%.

Rationale: Every state with >30% total burden struggles with illicit competition (Illinois 25–40%, Washington 37%). States with 20–25% achieve higher capture (Oregon 17%, Colorado 20–25%, Arizona 16%). Research demonstrates cannabis consumers are highly price-sensitive.

Revenue optimization: 5% rate reduction causes -$40–50M short-term but generates +$80–120M long-term through resident recapture. Net effect: +$25–40M annually.

Political strategy: Frame as education funding protection. Current trajectory: $108M declining 7–9% annually. Tax reform reverses decline, stabilizing school funding long-term.

Priority #2: Enforcement Surge (Critical)

Recommendation: Triple enforcement agents 8 → 25, annual budget $10–15M (from current ~$3–4M).

Focus areas:

- Large-scale illicit cultivation (500+ plant operations)

- Unlicensed delivery services (Instagram/Telegram advertising)

- Interstate trafficking (California imports)

Rationale: Eight agents for $1B+ market with $242–370M illicit competition is catastrophic underinvestment. States with robust enforcement (Michigan 50+ agents, Colorado 40+) consistently outperform weak enforcement (Nevada 8, California minimal) by 15–25 percentage points.

Funding source: Increase wholesale excise 1–2% (cultivation level): +$8–12M annually. Cultivation facilities absorb increase (wholesale margins support it). Retail prices unchanged.

Partnership strategy: Leverage federal (DEA, Border Patrol), local (Las Vegas Metro, Washoe Sheriff), and agricultural (NV Dept of Agriculture) resources. CCB cannot police entire state alone.

Priority #3: Delivery Infrastructure

Recommendation: Streamline delivery licensing, allow third-party services, integrate with gig platforms (DoorDash, Uber), mandate same-day delivery standard.

Rationale: Las Vegas sprawl (Henderson, North Las Vegas, Summerlin) creates 15–30 minute dispensary trips. Illicit delivery advertises on Instagram, accepts Venmo, delivers within 2 hours. Legal delivery must match convenience.

Framework impact: Robust delivery improves convenience score (F) from 0.68 to 0.74, adding 3–4 percentage points to legal market share.

Priority #4: Consumption Lounge Acceleration

Recommendation: Fast-track licensing, reduce $200K liquidity requirement, enable casino-integrated lounges, promote Las Vegas as cannabis tourism destination.

Rationale: Las Vegas thrives on on-premises consumption (casinos, bars, nightclubs). Cannabis lounges fit perfectly but implementation has been glacial (only 1 operating after 4 years).

Declining alcohol consumption opportunity: UNLV Cannabis Policy Institute research identifies "decreasing alcohol sales among younger consumers" as major trend threatening hotel/restaurant/gaming revenue. Cannabis lounges and THC beverages could "help mitigate that effect as the 'lower-alcohol' demographic comes of age." Nevada's cannabis regulation evolution must anticipate alcohol substitution—consumers drink less but consume more cannabis.

Tourism uplift: Consumption lounges could increase tourism sales 20–30% through enhanced experiential offerings. Major Strip resorts should integrate lounges (Venetian rooftop lounge, MGM properties, Caesars Roman-themed experiences). UNLV analysis: "On-premise alcohol venues command 3× to 10× markups over retail—cannabis lounges integrated with entertainment could capture similar premiums."

THC beverage integration: Nevada's premium THC beverage market ($10/can at dispensaries vs. $5/can in Texas hemp stores) positions lounges perfectly. Bars/restaurants currently generate massive profits from marked-up alcohol—cannabis lounges can replicate model with THC drinks, edibles, and social consumption experiences.

Revenue impact: 20–30 operational lounges generating $2–4M each = $40–120M incremental annual sales.

Priority #5: Federal Reform Advocacy

Recommendation: Nevada congressional delegation prioritize SAFE Banking Act and Schedule III rescheduling.

Nevada's advantages: First Western adult-use state (leadership credibility), tourism economic model (unique perspective), bipartisan voter approval (66% in 2016), strong tax revenue generation. Nevada is ideal federal reform messenger—not California/Colorado (perceived liberal) but gaming/tourism powerhouse demonstrating vice regulation success.

Comparison to Other Markets

Nevada's performance places it mid-tier among U.S. cannabis markets—better than disasters, worse than leaders.

Western neighbors:

- Oregon (82% legal share): Low taxes (17%), oversupply drives prices down. Nevada lesson: Price competitiveness matters most.

- Arizona (75–80%): Moderate taxes (16% + sales), strong enforcement. Nevada lesson: Newer market executing better through learning from Nevada's mistakes.

- California (50%): Fragmentation (61% local bans), high taxes. Nevada lesson: Nevada avoiding California's worst errors but still underperforming.

- Colorado (73–78%): Mature market (since 2014), similar timeline. Nevada lesson: Colorado maintains share while Nevada declines—execution matters.

Nevada's trajectory: 2017–2021 (Growth): Rapid rollout, tourism integration, market growth. 2021–2025 (Decline): Rested on early success, failed to optimize, illicit market exploited gaps. 2025–2030 (Decision point): Optimize → reverse decline OR Stagnate → continued erosion.

Timeline and Path Forward

Nevada can reverse market decline over 3–5 years through phased implementation:

Phase 1: Tax Reform (2027–2028)

- 2027 legislative session: Pass retail excise reduction 10% → 5%

- Expected outcomes: Resident prices decline 5–6%, legal market stabilizes, sales $780–820M (2028) vs. projected $720M without reform

Phase 2: Enforcement Surge (2028–2029)

- Hire 15–17 additional agents (8 → 25 total), budget $10–15M annually

- High-visibility enforcement actions deter illicit market entry

- Legal market share: 72–76% (recovering)

Phase 3: Delivery Infrastructure (2029–2030)

- Third-party delivery licensing streamlined, gig economy integration

- Same-day delivery becomes standard

- Legal market share: 75–78%

Phase 4: Federal Reform Response (2029–2031)

- If Schedule III occurs: Dispensaries reduce prices 20–25%, legal share 80–85%

- If SAFE Banking passes: Card payments standard, tourism sales increase, legal share +4–6 pp

- Combined impact: Legal sales $1.1–1.3B annually (exceed FY2021 peak), tax revenue $165–195M, illicit market <$180M

Without federal reform: Nevada maxes at 75–78% legal share (state optimization only), sales plateau $880–950M (below FY2021 peak).

Economic Reality: Current State vs. Optimized State

Current state (FY2025):

- Legal sales: $758M (projected)

- Tax revenue: $122–130M

- Jobs: 5,000–6,000 direct + indirect

- Illicit market: $242–370M (25–33% share)

- Market bifurcation: Tourists generate similar revenue to residents despite 13:1 population ratio

Optimized state (2030 with federal reform):

- Legal sales: $1.1–1.3B annually

- Tax revenue: $165–195M annually

- Jobs: 8,000–10,000 (including delivery 500–700, lounges 400–600)

- Illicit market: $140–180M (reduced 40–50%, 12–16% share)

- Market health: Tourist $480–580M (lounge integration growth), Resident $620–720M (recovery from tax relief)

Net benefit (optimized vs. current):

- Additional tax revenue: $35–65M annually

- Additional economic activity: $350–550M annually

- Additional jobs: 3,000–4,000

- Education funding stability: Reverses current 7–9% annual decline

Conclusion: Nevada's Cautionary Tale and Path to Redemption

Nevada pioneered recreational cannabis in the American West. Eight years later, Nevada's market is collapsing: Sales down 25% from peak, illicit market capturing 30%, residents fleeing to untaxed alternatives, education fund suffering.

Nevada's failure is not inevitable—it's correctable. The framework reveals a clear path: Tax reform, enforcement surge, delivery infrastructure, consumption lounge acceleration. With federal reform (280E elimination + SAFE Banking), Nevada could achieve 80–85% legal market share and return to FY2021 peak sales.

But Nevada must act. Every year of inaction means $50–80M flowing to illicit markets, $8–12M lost education revenue, hundreds of jobs that could exist but don't, market perception hardening that "legal cannabis is overpriced."

What Nevada did right: Rapid implementation (first-mover advantage), tourism integration potential, vertical integration, testing standards, AB 504 hemp channeling.

What Nevada did wrong: Punitive taxation (33% burden), enforcement neglect (8 agents, AB 76 failure), resident market abandonment, consumption lounge implementation failure, complacency.

Nevada demonstrates that early-mover advantage dissipates without continuous optimization. Arizona implemented four years after Nevada yet performs better—proving execution matters more than timing. Oregon and Michigan surpass Nevada through superior price competitiveness and enforcement. Colorado maintains share while Nevada declines.

The framework is clear. The solutions are known. Nevada policymakers must choose: Optimize (tax reform + enforcement surge → 80–85% legal share → $1.1–1.3B sales → $165–195M tax revenue) OR Stagnate (maintain current policies → continued erosion → 60–65% legal share by 2030 → education funding crisis).

Nevada voters approved cannabis legalization 66%–34% in 2016. They expected regulated market to displace illicit alternatives, fund schools, create jobs. Instead: declining legal sales, growing illicit markets, eroding education funding.

Nevada can still fulfill that promise. The state that pioneered recreational cannabis can reclaim leadership through aggressive optimization. But the window is closing. Arizona, Oregon, Michigan have surpassed Nevada. Colorado maintains performance Nevada is losing.

Nevada's choice: Pioneer or cautionary tale. Lead or follow. Optimize or decline.

The framework shows the path. Will Nevada take it?

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Maryland | S Dakota | Mississippi | Vermont

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0