New Hampshire Cannabis Market Analysis: The Last New England Holdout and the Revenue Bleeding South

New Hampshire stands alone—the only New England state without legal adult-use cannabis, hemorrhaging hundreds of millions annually to Massachusetts while maintaining the region's most expensive medical program.

The Silent Majority 420 | November 2025

The New Hampshire Paradox: "Live Free or Die"—Except for Cannabis

New Hampshire's motto—"Live Free or Die"—embodies fierce independence, minimal government intervention, and individual liberty. The state famously has no income tax, no sales tax, minimal business regulation, and runs liquor stores as government-operated franchises generating massive revenue. The libertarian ethos is genuine.

Yet New Hampshire maintains prohibition on adult-use cannabis while literally every neighboring state has legalized: Massachusetts (2016), Maine (2016), and Vermont (2018) all allow recreational cannabis. Canada borders New Hampshire to the north—adult-use legal since 2018.

The contradiction is stark and expensive.

Drive 30 minutes south from Manchester or Nashua and you're at Massachusetts dispensaries offering competitive prices, extensive selection, and convenient access. Every weekend, thousands of Granite Staters make the pilgrimage—spending money that should circulate in New Hampshire, generating tax revenue for Massachusetts instead.

New Hampshire's Therapeutic Cannabis Program exists—7 dispensaries operated by 3 non-profit Alternative Treatment Centers (ATCs) serving approximately 14,700 patients. But the program is expensive, restrictive, and under-scaled. Patients complain about high prices ($548 for six-week supply), limited access (only 7 locations statewide), and no home cultivation allowed.

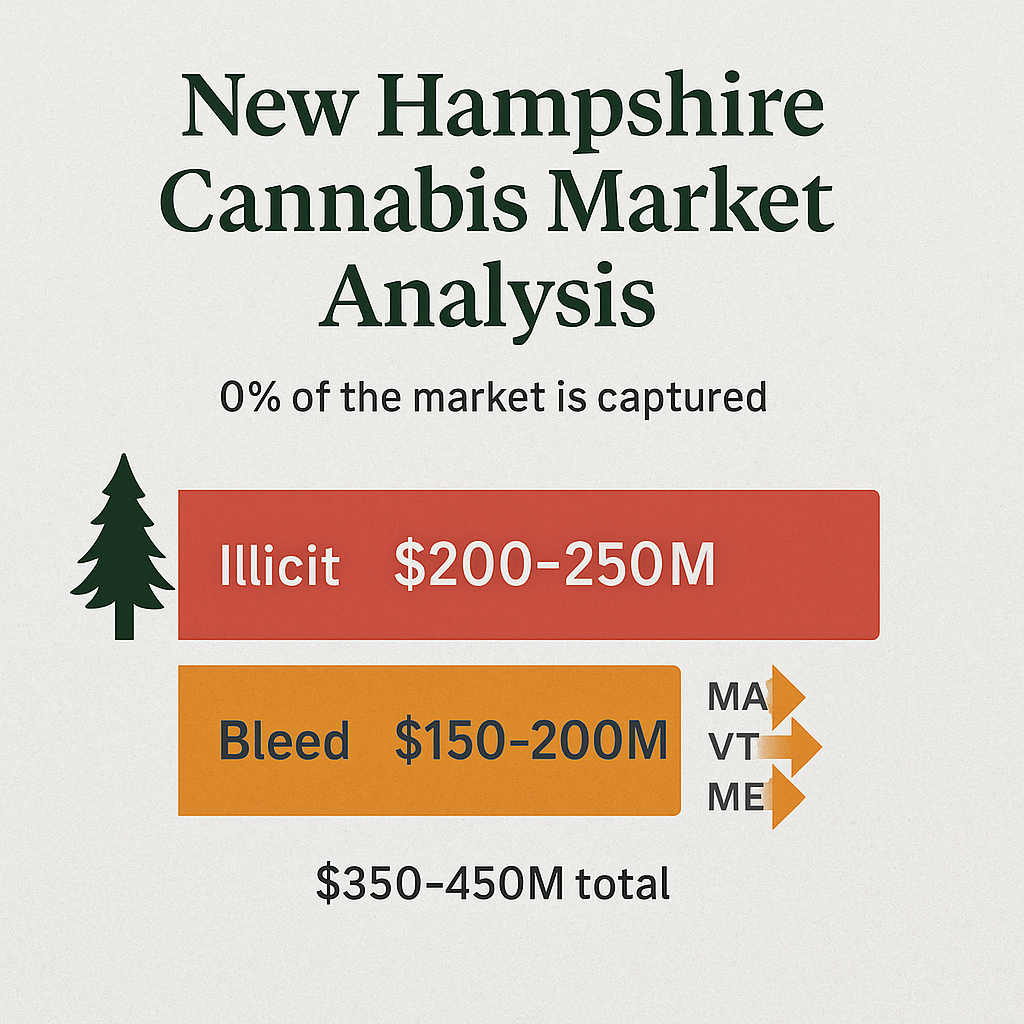

Result: New Hampshire residents—among the nation's highest per-capita income earners—spend an estimated $280–350 million annually on cannabis. Perhaps $75–115M flows to Massachusetts dispensaries. Another $165–235M circulates through illicit markets. New Hampshire captures medical program revenue only: ~$30–50M annually.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals New Hampshire's opportunity: With optimized policy (private retail, competitive taxes, statewide access), New Hampshire could achieve 78–84% legal market share within 36–48 months—matching Massachusetts, outperforming Vermont, generating $39–54M annually in state tax revenue.

But achieving this outcome requires abandoning the failed 2024 HB 1633 state-run franchise model and implementing free-market principles consistent with the state's libertarian values.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

The 2024 Legalization Failure—And Why It Matters

In June 2024, New Hampshire came agonizingly close to ending prohibition. HB 1633 passed the House 239-136 (landslide support), passed Senate with amendments 14-10, and went to Committee of Conference for reconciliation. The compromise bill was ready for final passage—until the House tabled it 178-173 on June 13, 2024, the final legislative day.

What killed it? Not prohibition ideology—but government overreach.

The Senate version (backed by Governor Sununu) imposed state-run franchise model:

- New Hampshire Liquor Commission would oversee operations

- Only 15 dispensaries allowed statewide

- Franchise fee of 15% monthly gross revenue

- Cannabis businesses prohibited from lobbying or political contributions

This model exists nowhere among 24 adult-use states. It combined worst aspects of Soviet-style central planning (only 15 stores for 1.4 million residents), excessive government control (state as "franchisor" of private businesses), and anti-competitive restrictions (no lobbying, capped licenses, franchise fees).

Progressive Democrats opposed it: Too restrictive, insufficient access, franchise model unworkable.

Libertarian Republicans opposed it: Massive government intervention, anti-free market, worse than current prohibition.

The compromise satisfied nobody. The vote was essentially 50-50 split within both Republican and Democratic caucuses—bipartisan opposition to bad policy.

Lesson: New Hampshire voters support legalization (70%+ in polls). Legislature supports legalization. But government-run franchise model poisoned reform.

New Hampshire's Structural Advantages

Despite prohibition, New Hampshire possesses characteristics favoring legal market optimization—IF policymakers implement free-market policy.

Wealthiest Population in New England

New Hampshire demographics (2025):

- Population: 1,415,860 (41st nationally)

- Median household income: $95,628 (highest in New England, 21% above national average)

- Poverty rate: 7.16% (among nation's lowest)

- Education levels: Strong (Boston metro suburbs)

Framework significance: Wealth correlates with legal market preference. High-income consumers value convenience over price, prefer professional retail environment over illicit dealers, and can afford higher prices (reduces tax sensitivity). Massachusetts benefits from wealthy Boston suburbs. Colorado Front Range similarly affluent. Wealth enables legal market success through reduced price sensitivity.

Geographic Concentration

Population distribution:

Southern Tier (I-93 Corridor):

- Manchester: 116,386

- Nashua: 91,851

- Concord: 44,674

- Derry: 34,062

- Salem: ~30,000

- Total southern tier: ~600,000+ (42% of state)

Merrimack River Valley + Seacoast: Additional ~400,000 residents

Total in dense southern/coastal belt: ~1 million (70%+ of population)

Framework significance: 70% of population within 50-mile radius creates efficient retail coverage opportunity. 55–75 dispensaries could serve 95%+ of residents within 30-minute drive. Northern NH challenges (sparse population, mountains, rural access) solvable through delivery infrastructure—same solution Maine employs successfully.

Strong Law Enforcement + Low Crime Culture

New Hampshire consistently ranks among safest U.S. states with strong community policing, well-funded state police, and effective drug interdiction.

Framework significance: States with strong enforcement cultures (Michigan, Nevada, Colorado) achieve 15–25 percentage points higher legal market share than weak-enforcement states (California, New York).

New Hampshire's enforcement capacity wouldn't need restructuring post-legalization—just redirection. Currently targets consumers and interstate trafficking. Post-legalization would target illegal cultivation, unlicensed retailers, diversion to minors. Same institutional strength, different focus, proven effectiveness.

Overwhelming Border Pressure from Massachusetts

Border pressure creates urgency lacking in isolated prohibition states.

Economic Reality:

- $75–115M annually flowing to Massachusetts

- $13–19M in lost tax revenue

- Hundreds of jobs foregone

- Every weekend: Thousands of NH residents driving south

Political Reality:

- Voters see Massachusetts success (no social chaos, tax revenue, legal access)

- Businesses want cannabis industry opportunities

- Law enforcement tired of arresting residents for legal-30-minutes-away behavior

- Fiscal conservatives recognize revenue opportunity

70%+ public support for legalization per polls—higher than most states at legalization moment.

Framework significance: Border pressure accelerates reform. States surrounded by legal markets face greater urgency than isolated prohibitionists. Indiana surrounded by Michigan, Illinois, Ohio—prohibition increasingly untenable. New Hampshire similar: Every neighbor legal creates economic hemorrhage forcing reconsideration.

Clean Regulatory Slate + Learning Advantage

New Hampshire starts 12+ years behind early adopters, creating opportunity to learn from neighbors' mistakes.

What New Hampshire can avoid:

- Massachusetts: High local option taxes (some municipalities 3%+), complex social equity

- Vermont: Potency caps (60% THC limit on concentrates—arbitrary restriction)

- California: Local bans (61% municipalities prohibit retail), excessive taxes

- Illinois: THC-tiered taxes (25–40%), licensing favoritism, capital barriers

What New Hampshire can emulate:

- Massachusetts: Strong testing standards, professional retail, good access density

- Michigan: Moderate taxes (16% total), competitive pricing, 85% legal share

- Colorado: Mature regulatory framework, delivery infrastructure, enforcement effectiveness

Clean slate + 24 state examples = opportunity to implement best practices day one.

The Border Hemorrhage: Quantifying Massachusetts's Gain

New Hampshire faces unique border pressure—surrounded by legal states capturing Granite State dollars.

Massachusetts (South—30 Minutes from Major Population Centers)

Massachusetts opened adult-use November 2018:

- 400+ dispensaries statewide

- Competitive market ($35–55 per eighth after tax)

- Moderate taxes (10.75% excise + 6.25% sales + local option = 17–20% total typical)

- Professional retail environment

Southern New Hampshire Impact:

Manchester (116,386 residents), Nashua (91,851), Salem (~30,000), Derry (34,062) all within 20–45 minutes of Massachusetts border. Combined southern NH population: ~500,000 residents in Massachusetts border zone.

Economic Loss Estimate:

Conservative calculation:

- 12% of adults consume cannabis regularly (national average)

- Southern NH cannabis consumers: 50,000–60,000

- Percentage shopping Massachusetts vs. illicit market: 60–70%

- 35,000–40,000 regular Massachusetts shoppers

- Average annual spending: $1,200–1,600 per consumer

- Total annual flow to Massachusetts: $45–65 million from southern NH alone

Add central NH (Concord area, Lakes Region) with occasional Massachusetts trips: Additional $30–50M annually.

Total New Hampshire → Massachusetts Flow: $75–115 million annually

Massachusetts benefits:

- Excise tax revenue: $8–12M annually from NH residents

- Sales tax revenue: $5–7M annually

- Economic activity: Jobs, tourism, downstream spending

New Hampshire loses:

- $13–19M annually in potential tax revenue

- $75–115M in economic activity

- Hundreds of retail/cultivation/processing jobs

- Cannabis tourism potential

The Restrictive Medical Program: Why It Fails

Therapeutic Cannabis Program (established 2013 under RSA 126-X):

Current Structure:

- 3 licensed Alternative Treatment Centers (non-profit organizations only)

- 7 dispensary locations: Chichester, Conway, Dover, Keene, Lebanon, Merrimack, Plymouth

- Operators: GraniteLeaf Cannabis, Sanctuary Medicinals, Temescal Wellness

- ~14,700 registered patients + caregivers (1% of population)

- Patients may possess up to 2 ounces within 10-day period

- No home cultivation allowed

The Cost Problem:

Concord Monitor investigation (September 2025) documented patient experiences:

- Typical patient spending: $70–130 per visit (stretches 1+ month for low-dose users)

- Heavy users: $548 for six-week supply

- No insurance coverage

- Patients timing purchases around sales to afford medicine

Compare to Massachusetts prices: Same products cost 30–40% less at competitive retail market.

The Access Problem:

Seven dispensaries for 1.4 million residents = 1 per 200,000 people.

Comparison:

- Massachusetts: 400+ dispensaries for 7 million (1 per 17,500)

- Vermont: 73 dispensaries for 647,000 (1 per 8,860)

- Maine: 170+ dispensaries for 1.4 million (1 per 8,235)

New Hampshire has worst access in New England by factor of 10–20×.

Predicted Market Outcomes: IF New Hampshire Legalizes Properly

The framework allows prediction of New Hampshire's market performance under different policy scenarios.

Optimized Scenario: Free-Market Excellence

Policy Design:

- Private retail: State-issued licenses, merit-based approval, no caps (market determines optimal number)

- Total tax rate: 18–22% (10–12% excise + 8–10% existing business taxes)

- Competitive with Massachusetts (17–20% typical)

- Prevents border arbitrage

- Avoids Illinois high-tax mistake (25–40%)

- Retail authorization: State licenses, local control limited to zoning only (prevent fragmentation)

- Density target: 55–75 dispensaries statewide (3.9–5.3 per 100K residents)

- Manchester: 12–16 stores

- Nashua: 8–12 stores

- Concord: 4–6 stores

- Seacoast (Portsmouth-Dover): 6–8 stores

- Lakes Region: 4–6 stores

- White Mountains: 3–5 stores

- Remaining distribution: 18–22 stores

- Statewide delivery: Mandatory for areas >25 miles from retail

- Testing standards: Comprehensive (New England's best)

- Enforcement budget: $8–12M annually ($5.65–8.50 per capita)

- ATC conversion priority: Existing medical dispensaries receive first adult-use licenses

- ASSUMES: Federal Schedule III (280E elimination) + SAFE Banking passage

Framework Inputs:

- Price competitiveness: g = -0.22 (legal 22% cheaper than illicit, competitive with Massachusetts)

- Access density: D = 0.82 (55–75 stores + delivery covers 90%+ population effectively)

- Safety/quality: S = 0.85 (rigorous testing, professional regulation)

- Convenience: F = 0.78 (SAFE Banking enables cards, normal retail hours, online ordering)

- Enforcement: E = 0.75 (strong interdiction capability, professional agencies, political will)

- Fragmentation: F_frag = -0.10 (minimal local bans through state preemption)

Predicted Outcomes:

- Transaction share: 82–88% (consumers choosing legal over illicit/Massachusetts)

- Volume share: 78–84% (accounting for heavy user patterns, Massachusetts competition)

- Timeline: 36–48 months to reach steady state

Economic Impact:

- Adult cannabis consumers: 130,000–170,000 (9–12% of adults aged 21+)

- Legal market size: $195–270M annually (mature in-state market)

- Capture from Massachusetts: $40–65M annually (NH residents who currently shop MA)

- State tax revenue: $39–54M annually (at 18–22% rate)

- Jobs: 1,950–2,700 direct + indirect

- Illicit market: Reduced from $280–350M to $45–75M (80–85% reduction)

- Medical program transition: 30–40% of medical patients maintain cards for tax benefits

Comparable Performance:

New Hampshire would achieve outcomes similar to:

- Massachusetts: 78–82% legal share (current New England leader)

- Michigan: 85% legal share (national leader)

- Colorado (with federal reform): 84–88% projected

This represents best-case New Hampshire: Learning from regional examples, implementing free-market principles consistent with state culture, competing effectively with Massachusetts, leveraging wealthy consumer base.

Failed Scenario: State-Run Franchise Disaster (HB 1633 Model)

Policy Design:

- State-run franchise model: NH Liquor Commission oversight, only 15 dispensaries statewide

- Franchise fee: 15% monthly gross revenue (on top of taxes)

- Cannabis business restrictions: No lobbying, no political contributions, extensive state control

- High effective tax burden: Franchise fee + excise + business taxes = 30–35% total

- Limited licenses: Artificial scarcity, political favoritism in selection

- No delivery: Not included in franchise model

- 280E remains (no federal reform)

Predicted Outcomes:

- Transaction share: 52–60%

- Volume share: 48–56%

- Comparable to: Illinois (55–60%), Washington early years (65%)

Economic Impact:

- Legal market: $105–155M annually (underperformance)

- Tax revenue: $32–47M annually (high rate, small base—similar total to optimized but worse outcomes)

- Jobs: 1,050–1,550

- Illicit market: $150–210M (persistent due to high legal prices)

- Massachusetts cross-border shopping: Continues unabated ($60–90M annually—franchise model can't compete)

Why This Fails:

- 15 dispensaries for 1.4M residents = 1 per 93,000 (terrible access)

- Franchise fees + taxes + 280E create prices 40%+ higher than Massachusetts

- No delivery = northern/rural NH unserved

- State control alienates libertarian culture

- Artificial scarcity ensures black market thrives

- Massachusetts remains cheaper and more convenient—border hemorrhage continues

This represents policy disaster: New Hampshire "legalizes" but implements worst-in-nation model, failing to compete with Massachusetts, maintaining substantial illicit market, generating revenue disappointment while claiming legalization achieved.

This is why HB 1633 failed—bipartisan opposition to terrible policy masquerading as reform.

Most Likely Scenario: Cautious Private Market

New Hampshire's political culture suggests eventual legalization through private retail (not franchise) but with conservative implementation:

Policy Design:

- Private retail: State-issued licenses, merit-based, phased rollout

- Moderate tax: 20–25% total (higher than optimal but not Illinois-level)

- Controlled initial licensing: 40–55 dispensaries initially, expansion based on demand

- Medical ATC conversion priority: Existing operators get first licenses

- Strong regulatory oversight: Thorough state control without franchise model

- Enforcement maintained: Apply existing capacity to illegal operators

- Federal reform: Assumed partial (Schedule III likely, SAFE Banking uncertain)

Predicted Outcomes:

- Transaction share: 72–79%

- Volume share: 68–76%

- Timeline: 48–60 months (slower rollout than optimized)

Economic Impact:

- Legal market: $165–230M annually

- Tax revenue: $35–50M annually

- Jobs: 1,650–2,300

- Massachusetts competition: Reduced but not eliminated ($30–50M annual cross-border)

- Illicit market: $80–125M (reduced but not optimized)

This represents good-but-not-optimal: Better than HB 1633 franchise disaster, better than doing nothing, not quite matching Massachusetts. New Hampshire's conservatism produces competent outcomes without excellence.

The Federal Policy Barrier

New Hampshire cannot achieve optimized outcomes under current federal policy. While detailed coverage of these issues is available in our pillar pages on IRC Section 280E and the SAFE Banking Act, here's why they matter specifically for New Hampshire:

The 280E Problem

Internal Revenue Code Section 280E prohibits cannabis businesses from deducting ordinary expenses, forcing NH dispensaries to raise prices 15–20% just to survive. Already competing with established Massachusetts market across border, this federal penalty creates insurmountable disadvantage.

Solution: Schedule III rescheduling eliminates 280E. NH businesses deduct normal expenses like any business, reducing retail prices 12–18%, dramatically improving competitiveness with Massachusetts.

Without 280E elimination, New Hampshire legal market cannot optimize regardless of state policy quality.

The SAFE Banking Problem

Without SAFE Banking Act passage, NH dispensaries operate cash-only, reducing transaction frequency 18–25% according to Federal Reserve research. NH consumers accustomed to card payments everywhere face significant friction with cash-only cannabis retail.

Solution: SAFE Banking Act passage enables credit/debit card payments, online ordering integration, business lending, and improved customer experience. NH instantly competitive with Massachusetts on payment convenience.

New Hampshire Cannot Optimize Alone

Framework demonstrates: State policy determines 70–75% outcomes, federal barriers create 25–30% ceiling.

- Massachusetts: 78–82% despite 280E/banking barriers

- Illinois: 55–60% due to high state taxes compounded by 280E

- New Hampshire optimized scenario (78–84%) requires both state AND federal policy alignment

Good state policy alone achieves 68–75%. Federal reform adds final 10–15 percentage points plus competitive advantage over Massachusetts.

Policy Recommendations: The New Hampshire Path Forward

IF New Hampshire moves toward legalization (likely 2026–2028), evidence-based recommendations:

Priority #1: Reject State-Run Franchise Model

Recommendation: Private retail with state regulation—like every other successful legal state

Rationale: HB 1633 franchise model failed for good reasons:

- Unprecedented in U.S. cannabis markets (zero successful examples)

- Violates New Hampshire's free-market principles

- Creates artificial scarcity (15 stores inadequate)

- High franchise fees act as hidden tax

- State liability exposure (government as "franchisor")

- Prevents competition, innovation, efficiency

Private retail model (all 24 legal states):

- Market determines optimal store count

- Competition drives prices down, quality up

- State role: Licensing, regulation, enforcement (not operations)

- Proven successful across diverse states

- Consistent with NH libertarian culture

Comparison:

- Massachusetts: 400+ stores, competitive market, 78–82% legal share

- Vermont: 73 stores, growing market, smaller population

- Maine: 170+ stores, strong competition, good prices

New Hampshire should implement private retail with merit-based licensing—let market competition determine store count, locations, pricing.

Priority #2: Competitive Tax Structure

Recommendation:

- State excise tax: 10–12%

- Existing business taxes: 8–10% (Business Profits Tax + Business Enterprise Tax)

- Total state burden: 18–22%

- Local option: 2–3% maximum (capped to prevent stacking, optional not mandatory)

- Total effective rate: 20–25% (competitive with Massachusetts 17–20%, avoids Illinois disaster 25–40%)

Rationale: New Hampshire must compete with Massachusetts on price—60% of NH residents live within 45 minutes of MA dispensaries.

Tax rate comparison:

- Massachusetts: 10.75% excise + 6.25% sales + local option 0–3% = 17–20% typical

- Vermont: 14% excise + 6% sales = 20% total

- Maine: 10% excise + 5.5% sales = 15.5% total

- Illinois: 25–40% (FAILURE—creates persistent black market)

New Hampshire at 18–22% would:

- Remain competitive with Massachusetts (prevent border shopping)

- Generate substantial revenue ($35–50M annually estimated)

- Avoid pricing out working-class consumers

- Maximize legal market share through volume strategy

Critical: No sales tax in NH means excise tax must be higher than MA's 10.75% to achieve similar total burden—but existing business taxes add 8–10%, creating 18–22% total which matches MA's 17–20% effective rate.

Priority #3: Statewide Access Through Retail + Delivery

Recommendation:

- State-issued retail licenses (NH Department of Health and Human Services oversight)

- Target: 55–75 dispensaries statewide (3.9–5.3 per 100K residents)

- Geographic distribution:

- Southern tier (Manchester-Nashua-Salem corridor): 30–40 stores

- Capital region (Concord-Lakes): 8–12 stores

- Seacoast (Portsmouth-Dover-Rochester): 8–12 stores

- North Country (White Mountains-Coös): 4–8 stores

- Delivery required: Statewide mandate for areas >25 miles from retail

- Municipalities: Can regulate zoning/buffers, CANNOT prohibit retail outright (state preemption)

- ATC conversion priority: Existing medical dispensaries (Granite Leaf, Sanctuary, Temescal) receive first adult-use licenses

Rationale: Prevent California fragmentation (61% local bans) while respecting local input on locations/buffers.

NH's concentrated southern population + sparse northern regions requires hybrid approach:

- Dense retail in Manchester-Nashua-Concord triangle (where 70% of residents live)

- Strategic retail in mid-sized cities (Portsmouth, Keene, Lebanon, Laconia)

- Delivery infrastructure for North Country, rural areas

Comparison:

- Massachusetts: 5.7 stores per 100K (400+ total)

- Vermont: 11.3 per 100K (73 total)

- Maine: 12.1 per 100K (170+ total)

NH target 3.9–5.3 per 100K (55–75 total) appropriate for smaller population, less dense northern regions, delivery compensation.

Priority #4: Leverage Enforcement Strengths

Recommendation:

- Budget: $8–12M annually dedicated to illicit supply interdiction ($5.65–8.50 per capita)

- Focus: Large-scale illegal cultivation, unlicensed retail, interstate trafficking

- Avoid: Consumer harassment, small-scale home cultivation

- Coordination: State Police + local PD + federal DEA

- Metrics: Illegal grow busts, unlicensed retailer closures, market share monitoring

Rationale: NH's strong enforcement culture becomes competitive advantage—not liability.

States with effective enforcement (Michigan 85%, Nevada 75–80%) outperform weak-enforcement states (California 50%, New York 30%) by 15–25 percentage points.

$8–12M enforcement budget appears expensive but generates 4–6× return:

- Higher legal market share → more tax revenue ($4–8M additional annually)

- Public safety improvement (tested products, licensed operators)

- Reduced interstate trafficking

- Consumer confidence in legal market

Priority #5: Home Cultivation Decision

Recommendation: Restricted home cultivation (political compromise)

- Medical patients: 6 plants (3 mature, 3 immature)

- Adult-use: 3 plants (1 mature, 2 immature) per adult, 6 per household maximum

- Enclosed locked facility required (indoor only, not visible from public)

- Registration optional but provides legal protection

Rationale: Home cultivation reduces legal market share by 3–7 percentage points when permitted. However, prohibition creates enforcement challenges and appears authoritarian.

NH's libertarian culture expects personal cultivation rights—prohibition politically difficult. Restricted approach balances:

- Personal liberty (individuals can grow for personal use)

- Market protection (limits discourage commercial-scale grows)

- Enforcement practicality (registration + limits create legal framework)

Comparison:

- Massachusetts: 6 plants per adult, 12 per household

- Vermont: 2 mature + 4 immature per adult

- Maine: 3 mature plants, up to 12 immature

NH at 3 plants (1 mature)/adult, 6 household max = conservative but reasonable—allows personal cultivation without enabling large-scale diversion.

Priority #6: Federal Banking Advocacy

Recommendation:

- NH Congressional delegation: Active SAFE Banking Act advocacy

- State-level workarounds: Explore state-chartered bank/credit union participation

- Regional coordination: Work with MA/VT/ME on New England banking solutions

- Business preparation: Assume eventual SAFE Banking passage, build infrastructure accordingly

Rationale: Banking access critical for consumer convenience, business efficiency, competitive advantage. NH consumers expect seamless payment—cash-only creates significant friction with wealthy, tech-savvy population.

Massachusetts dispensaries with banking access achieve higher sales, better customer satisfaction, lower security costs.

Federal SAFE Banking most important single reform (after Schedule III) for NH market success.

Timeline and Path Forward

Realistic timeline for NH cannabis reform:

Phase 1: Political Shift (2025–2026)

2025:

- Governor Ayotte maintains opposition

- No legalization bills introduced (legislative fatigue after HB 1633 failure)

- Medical program continues restricted operations

- Massachusetts border hemorrhage continues ($75–115M annually)

- Federal Schedule III rescheduling occurs (probable 2025–2026)

2026:

- New legislative session (two-year cycle)

- Post-HB 1633 lessons learned: No franchise model

- Revised legislation: Private retail model (similar to MA/VT/ME)

- Political calculation: Federal rescheduling reduces opposition, border pressure increases urgency

Success Factors for 2026:

- Federal Schedule III creates momentum

- SAFE Banking passage (possible 2025–2026)

- Massachusetts success becomes undeniable

- Border revenue loss politically unsustainable

- Revised legislation abandons franchise model

Phase 2: Legislative Action (2027–2028)

Most Likely Path: Legislative Passage

Timeline:

- Early 2027: Legalization bill introduced (private retail model)

- Mid-2027: Committee hearings, amendments, debate

- Late 2027: House passage (requires simple majority)

- Early 2028: Senate consideration (historically more conservative)

- Mid-2028: Governor decision (sign or veto)

Political dynamics:

- Governor Ayotte term ends January 2027—successor's position critical

- If Ayotte re-elected: Veto likely unless federal reform changes calculation

- If Democrat elected: More favorable to legalization

- If moderate Republican: Possible compromise (depends on federal status)

Phase 3: Implementation (2028–2030)

Assuming passage 2027–2028:

Year 1 (2028–2029): Regulatory Development

- Cannabis Control Commission established

- Rules promulgated (6–12 months)

- License applications released

- Existing medical ATCs apply for adult-use conversion

- Supply chain preparation begins

Year 2 (2029–2030): Market Launch

- First adult-use licenses issued (medical ATCs first, new retailers follow)

- Initial sales begin

- 25–35 dispensaries operational Year 1

- Supply scales up through Year 2

- Additional licenses issued based on demand

- Delivery infrastructure develops

Year 3 (2030–2031): Market Maturation

- 45–65 dispensaries operational

- Supply-demand balance achieved

- Prices stabilize

- Legal market share approaches steady state (68–76% most likely scenario)

- Tax revenue flows to state (~$35–45M annually)

Phase 4: Optimization (2031–2033)

Steady State Achievement:

- 55–75 dispensaries mature operations

- Legal market share 68–84% (depending on policy quality + federal reform)

- Tax revenue $35–54M annually

- 1,650–2,700 jobs created

- Illicit market reduced 75–85%

- Massachusetts cross-border shopping reduced but not eliminated

Economic Reality: What New Hampshire Stands to Gain (Or Continue Losing)

Current State: Prohibition Costs

Annual cannabis demand (estimated):

- Adult consumers: 130,000–170,000 New Hampshire residents (9–12% of adults 21+)

- Total market size: $280–350M annually

Current distribution:

- Massachusetts purchases: $75–115M (residents shopping MA dispensaries)

- Illicit market: $165–235M (NH-based dealers, informal networks)

- NH medical program: $30–50M (14,700 patients through ATCs)

Foregone tax revenue: At 20% tax rate on entire market: $54–70M annually

Current revenue: ~$0 (medical program non-profit, untaxed)

Border state losses:

- Residents shopping Massachusetts: $75–115M annually

- Massachusetts tax revenue from NH residents: $13–19M annually

- Jobs not created in NH but created in MA: 300–500 positions

Total prohibition cost:

- Foregone tax revenue: $54–70M annually

- Economic activity flowing out-of-state: $75–115M to Massachusetts

- Jobs not created: 1,650–2,700 positions

- Illicit market thriving: $165–235M untaxed, unregulated

Optimized Adult-Use Market Economics (2032+)

Market size:

- Adult-use sales: $195–270M annually

- Medical sales: $30–50M annually (patients maintaining cards for tax exemption)

- Total legal market: $225–320M annually

State tax revenue:

- Adult-use (20% effective rate): $39–54M annually

- Medical (untaxed): $0

Jobs created:

- Direct cannabis jobs: 1,650–2,200 (cultivation, processing, retail, testing, security)

- Indirect/induced: 300–500 (construction, legal, accounting, transport)

- Total employment impact: 1,950–2,700 jobs

Illicit market reduction:

- Current illicit: $165–235M

- Post-legalization illicit: $45–75M

- Reduction: $120–160M (75–80% decrease)

Massachusetts border competition:

- Current MA shopping: $75–115M annually

- Post-legalization MA shopping: $30–50M annually (convenience seekers, border residents)

- Captured back to NH: $25–65M annually

Economic multiplier:

- Every $1 in dispensary sales generates $1.50–1.80 total economic impact

- $225–320M dispensary sales → $337–576M total economic activity

Conservative vs. Failed Implementation

Optimized Implementation (Private Retail, Competitive Taxes):

- Tax revenue: $39–54M annually

- Jobs: 1,950–2,700

- Legal market share: 78–84%

- Illicit reduction: 75–80%

- 10-year economic impact: $3.9–5.4B total activity

Failed Implementation (HB 1633 Franchise Model):

- Tax revenue: $32–47M annually (similar nominal, worse outcomes)

- Jobs: 1,050–1,550

- Legal market share: 48–56%

- Illicit reduction: 50–60%

- 10-year economic impact: $2.1–3.1B total activity

Difference: $1.8–2.3B economic activity over decade, 900–1,150 fewer jobs, persistent black market, continued Massachusetts border hemorrhage.

Continuing prohibition:

- Tax revenue: $0

- Jobs: 200–350 (medical only)

- 10-year cost: $540–700M foregone revenue, $750M–1.15B to Massachusetts

Policy quality matters enormously. Free-market legalization generates 2–3× better outcomes than government franchise model.

Conclusion: New Hampshire's Choice

New Hampshire stands at crossroads.

Current path: Continue prohibition, watch thousands of residents drive south to Massachusetts every weekend, lose $54–70M annually in potential tax revenue, maintain expensive medical monopoly serving 1% of population, arrest citizens for possessing plant legal 30 minutes away.

Alternative path: Implement free-market legalization consistent with "Live Free or Die" values, competitive with Massachusetts on price/access/quality, generate $39–54M annually in state revenue, create 1,950–2,700 jobs, reduce illicit market by 75–80%, respect individual liberty.

The framework reveals New Hampshire's potential: With optimized policy (private retail, moderate taxes 18–22%, statewide access, strong enforcement) New Hampshire could achieve 78–84% legal market share within 48 months—matching Massachusetts, outperforming regional competitors, becoming New England's most efficient cannabis market.

New Hampshire possesses structural advantages:

- Wealthiest population in New England (high income enables legal market preference)

- Geographic concentration in south (efficient retail coverage, 70% of residents in dense corridor)

- Strong enforcement culture (redirected toward illegal operators creates competitive advantage)

- Clean regulatory slate (learn from 12+ years of neighbor experiences)

- Libertarian political culture (should favor individual liberty, free markets, minimal government)

- Overwhelming border pressure (Massachusetts hemorrhage creates urgency)

The 2024 HB 1633 failure wasn't rejection of legalization—it was rejection of terrible policy. State-run franchise model combining worst of central planning + government overreach died deservedly. Bipartisan opposition (Republicans and Democrats split ~50-50 on both sides) reflected shared wisdom: Bad legalization worse than continued prohibition.

The path forward is clear:

- Abandon franchise model: Implement private retail like every other successful legal state

- Competitive taxes: 18–22% total (match Massachusetts, avoid Illinois disaster)

- Statewide access: 55–75 dispensaries + delivery (prevent fragmentation, serve rural areas)

- Strong enforcement: Leverage existing capacity against illegal operators (not consumers)

- Federal reform advocacy: Push Schedule III + SAFE Banking (eliminates competitive disadvantages)

- Learn from neighbors: Massachusetts provides model (mature market, professional operations, moderate success)—improve on it

IF New Hampshire:

- Passes private retail legalization (2026–2028 timeline)

- Implements competitive tax structure (18–22%)

- Ensures statewide access through retail + delivery

- Maintains strong enforcement against illegal market

- Benefits from federal reform (Schedule III + SAFE Banking)

THEN New Hampshire achieves:

- 78–84% legal market share within 48 months (optimized scenario)

- $39–54M annual tax revenue

- 1,950–2,700 jobs created

- 75–80% illicit market reduction

- Competitive with Massachusetts (captures cross-border shopping)

- Consistent with state's libertarian values

The alternative: Continue watching Massachusetts profit from New Hampshire prohibition. Continue arresting citizens for behavior legal across the border. Continue losing $54–70M annually while neighbors prosper.

70%+ of New Hampshire voters support legalization. The political will exists. What's lacking is competent policy design and courage to implement free-market principles consistently with state's founding values.

"Live Free or Die"—except for cannabis? The contradiction is unsustainable. Eventually, New Hampshire will join every neighbor in legalizing. The only questions: When? And will leadership implement smart policy or repeat HB 1633's government-run mistakes?

The framework provides the roadmap. Economic analysis demonstrates the opportunity. Regional examples prove the model. Federal reform removes barriers. Massachusetts shows what's possible—and what New Hampshire could improve upon.

The choice is New Hampshire's.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Florida | Texas | Minnesota | Arizona

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0