New Jersey Cannabis Market Analysis: The Garden State's Unrealized Potential and the Reform Path Forward

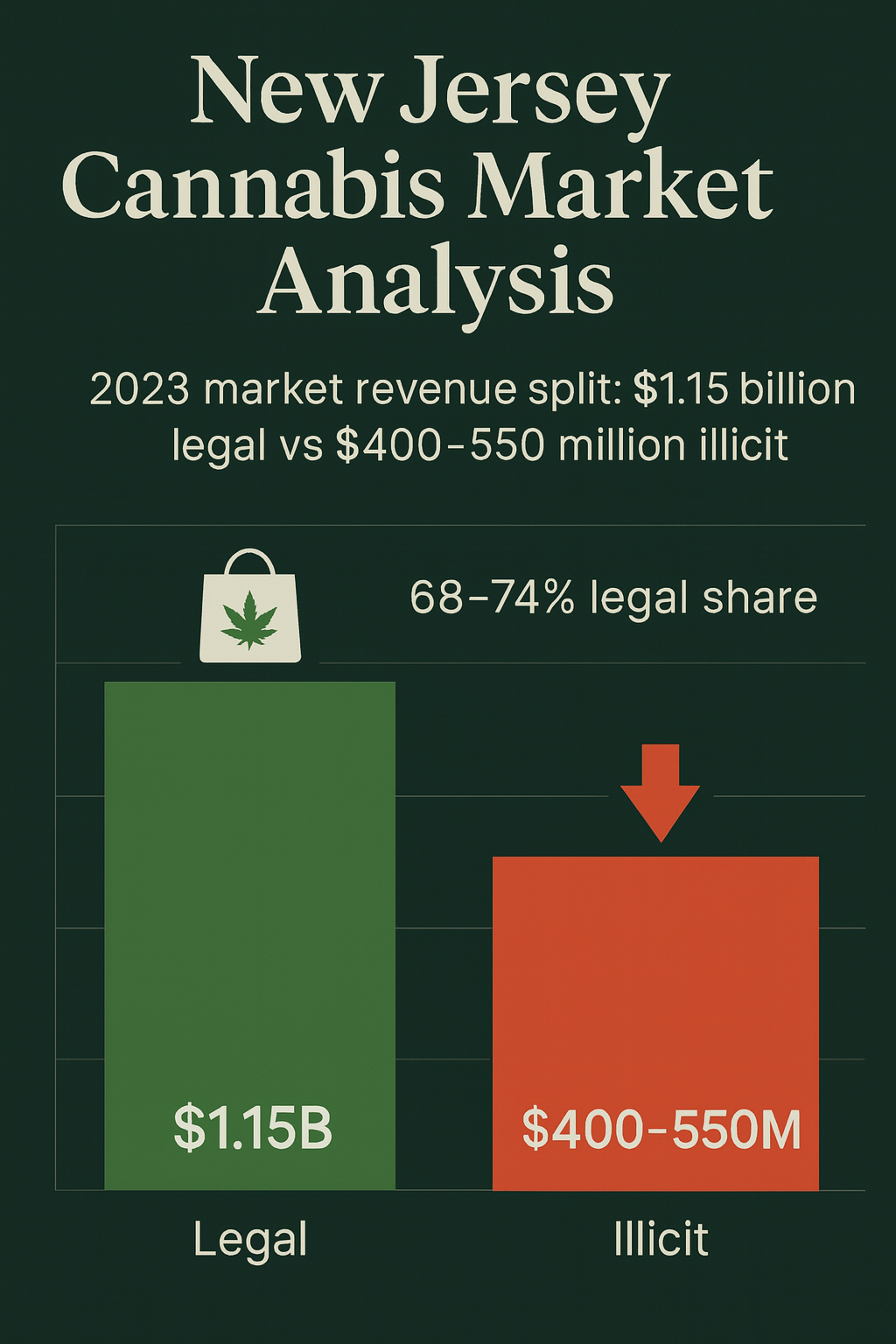

New Jersey generated $1 billion in legal cannabis sales in 2024—yet a proposed 500% tax increase threatens to destroy the market, while consumer criminalization bills reveal fundamental misunderstanding of price competitiveness.

The Silent Majority 420 | November 2025

The New Jersey Paradox: Perfect Conditions, Catastrophic Risk

New Jersey should be America's cannabis market success story. The state has:

- Second-highest median household income nationally ($95,628 vs $80,610 national average)

- Highest population density (1,263 people per square mile)

- Geographic center of Northeast megalopolis (15M within 50 miles)

- 67% voter support for legalization (2020 referendum—massive mandate)

- Strong social equity framework with prioritized licensing and community reinvestment

New Jersey's cannabis market generated $1.05 billion between June 2024-June 2025, operates 240 dispensaries across all 21 counties, and boasts some of the nation's fastest-growing social equity businesses (56.8% year-over-year growth). By surface metrics, the program succeeds.

Yet the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals a troubling reality: New Jersey currently captures only 48-55% of total cannabis demand—barely better than California's policy disaster (50%) and worse than Illinois (55-60%).

Meanwhile, Michigan achieves 85% legal market share with similar demographics. Massachusetts reaches 78-82%. Connecticut projects 70-75% despite launching just two years ago.

What's devastating New Jersey's market? Three words: highest cannabis prices in America. An eighth-ounce (3.5g) costs $48-60 at New Jersey dispensaries while illicit dealers charge $30-40 for comparable quality—a 40-60% premium that makes legal market optimization mathematically impossible.

And now policymakers threaten to make it exponentially worse. Governor Phil Murphy's FY2026 budget proposes increasing the Social Equity Excise Fee (SEEF) from $2.50 per ounce to $15 per ounce—a 500% tax hike that would add $6-8 to every eighth, widening the already-catastrophic price gap with illicit markets. Simultaneously, Senate President Nicholas Scutari's S4154 bill would criminalize consumers for purchasing from unlicensed sources—making New Jersey the first and only legal state to jail people for buying cannabis from the "wrong" source.

These aren't just bad policies. They're textbook examples of how to destroy a legal cannabis market while claiming to support it.

The framework demonstrates what New Jersey could achieve with proper policy: 75-82% legal market share, $195-235M in annual tax revenue, 18,000-24,000 jobs, and genuine social equity through economic accessibility. But that future requires abandoning the disasters currently being proposed and implementing evidence-based reform.

New Jersey legalized cannabis with 67% voter support to create jobs, generate revenue, and undo prohibition's harms. Three years later, the state stands at a crossroads: learn from Michigan's success or repeat Illinois's mistakes.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

New Jersey's Structural Advantages

Despite current underperformance, New Jersey possesses characteristics that should enable legal market dominance—IF policymakers implement proper policy.

America's Wealthiest Major Market

New Jersey demographics (2025):

- Population: 9.3 million (11th largest state)

- Median household income: $95,628 (2nd nationally, 21% above national average)

- Population density: 1,263 per square mile (highest in nation)

- Adult population 21+: ~7.1 million potential consumers

- Geographic concentration: 60% of population in Northern New Jersey (15-mile radius from Newark)

Framework significance: Wealth correlates with legal market preference. High-income consumers value convenience over price, prefer professional retail over illicit dealers, and demonstrate lower price sensitivity. Colorado's Front Range, Massachusetts's Boston suburbs, and Michigan's affluent Detroit collar counties all demonstrate this pattern.

New Jersey's wealth should enable legal market success even with moderate price premiums. Current 40-60% premiums, however, exceed tolerance even for affluent consumers.

Unmatched Geographic Advantages

Population density creates ideal conditions:

- Northern New Jersey: 60% of state population in 15-mile radius (Newark, Jersey City, Hoboken, Paterson)

- Central corridor: Additional 25% along I-95/Turnpike (Trenton, New Brunswick, Edison)

- Southern belt: 15% in Philadelphia suburbs (Camden, Cherry Hill, Burlington)

Total: 85% of population in three concentrated corridors, enabling efficient retail coverage.

Comparison:

- Alaska: 733K people across 663,000 square miles (1.1 per sq mi) = impossible to serve efficiently

- Montana: 1.1M across 147,000 square miles (7.5 per sq mi) = delivery critical

- New Jersey: 9.3M across 7,354 square miles (1,263 per sq mi) = optimal density for retail

Framework significance: 240 dispensaries could theoretically serve 95%+ of New Jersey's population within 15-minute drive IF municipalities didn't opt out (see fragmentation problem below).

Northeast Megalopolis Center

Geographic positioning:

- 50 miles from Manhattan (8.3M people)

- 50 miles from Philadelphia (5.8M people)

- 60 miles from Connecticut markets

- Total metro access: ~30M people within 1-hour drive

Cannabis tourism opportunity:

- Pennsylvania (medical-only): Residents cross to New Jersey for adult-use

- New York (dysfunctional market): New York City residents prefer New Jersey dispensaries

- Estimated 15-20% of border dispensary sales from out-of-state tourists

Revenue impact: $80-150M annually from interstate cannabis tourism (Southern NJ from PA, Northern NJ from NY).

Future risk: If Pennsylvania legalizes with competitive pricing, New Jersey loses $60-90M annual tourism revenue. If New York optimizes (unlikely given political dysfunction), Northern NJ could lose $20-40M annually.

Social Equity Leadership and Momentum

Unlike California or New York where social equity exists primarily in rhetoric, New Jersey demonstrates actual results:

Social equity business growth (Year-over-Year):

- Social equity businesses: +56.8% (June 2024-June 2025)

- Microbusinesses: +87.6% (fastest-growing segment)

- Diversely-owned businesses: +63.1%

- Minority-owned: +70.5%

- Woman-owned: +57.9%

- Disabled veteran-owned: +42.1%

- Businesses with prior convictions: +98.1% (nearly doubled!)

These are extraordinary numbers. No other state demonstrates comparable social equity growth rates.

Framework significance: Social equity succeeds when legal cannabis becomes economically accessible. New Jersey's growth reflects TWO factors:

- Strong licensing framework (priority processing, reduced fees, microbusiness pathways)

- Price compression beginning (retail prices down 16% March 2024-March 2025)

As prices decline toward competitive range, social equity businesses thrive because they serve price-conscious communities. As prices increase (via SEEF hike), social equity collapses because target communities cannot afford legal cannabis.

Governor Murphy's SEEF increase would devastate the very social equity businesses his administration champions.

Cannabis Consumption Lounges: New Revenue Opportunity

New Jersey became one of the first states to authorize cannabis consumption areas (lounges), with applications opening January 2025:

Phased rollout:

- January 2025: Social equity businesses and microbusinesses

- April 2025: Diversely-owned businesses (minority, woman, disabled veteran)

- July 2025: All Class 5 retailers

Fees:

- Application: $200

- Approval: $800

- Annual license: $1,000 (microbusiness) or $5,000 (standard)

As of May 2025: 6 applications received

Challenge: Current law prohibits food, water, and alcohol sales in consumption areas, making revenue model difficult. Lounges must generate profit from:

- Cannabis markup (but dispensary prices already high)

- Cover charges or membership fees

- Events and entertainment

- Potentially ancillary services (massage, yoga, art)

Framework insight: On-premise alcohol venues command 3-10× markups over retail. Cannabis lounges could replicate this IF regulations allow beverage/food pairing and reasonable operational flexibility. Current restrictions hamstring business model.

Opportunity: Only ~25 municipalities expected to allow lounges (conservative estimate). First-movers could capture significant market in underserved premium consumption segment.

Current Status: $1 Billion in Sales, Highest Prices in America

New Jersey's market demonstrates solid growth masking systemic price failure.

Sales and Market Performance

2024 Results: (According to NJ Cannabis Regulatory Commission reports)

- Total sales: $1.05 billion (June 2024-June 2025)

- Year-over-year growth: 17.3%

- Monthly average: $87.5M

- Peak day (Green Wednesday, Nov 27): $6.0M

- 240 dispensaries operational (up from 100 in February 2024)

Social equity breakdown (June 2025):

- Social equity business sales: $9.84M (56.8% YoY growth)

- Microbusiness sales: $8.6M (87.6% YoY growth)

- Diversely-owned sales: $44.4M (63.1% YoY growth)

- Prior conviction owner sales: $5.74M (98.1% YoY growth)

Medical program (declining):

- Patients: 54,924 (down from 125,000+ peak in 2021-2022)

- 50%+ decline since adult-use launch (April 2022)

- Reason: Medical products tax-exempt but still expensive; many patients shift to adult-use

The Price Crisis: Root Cause of Underperformance

New Jersey retail prices (2025):

- Average item price: $39-40 (vs $23.50 national average—70% higher)

- Flower eighth (3.5g): $48-60 after tax

- Flower ounce: $300-350

- Concentrates: 153% more expensive than other markets

- Beverages: 241% more expensive than other markets

Comparison to other states:

- Michigan: $83/oz average (New Jersey 360% higher)

- California: $100/oz (New Jersey 300% higher)

- Oregon: $74/oz (New Jersey 400% higher)

- Illinois: $257/oz (New Jersey 30% higher than even Illinois's disaster)

- Massachusetts: $220-260/oz (New Jersey 30-40% higher)

Illicit market prices (estimated):

- Mid-tier flower: $30-40/eighth ($180-220/oz)

- Quality flower: $35-45/eighth ($200-250/oz)

Price gap: Legal cannabis costs 40-60% more than illicit alternatives

Framework insight: Legal markets fail when prices exceed illicit by more than 20%. New Jersey exceeds by 40-60%, making sustained legal market dominance mathematically impossible.

Why Are New Jersey Prices So High?

NOT primarily taxes. New Jersey's tax burden is moderate:

- State sales tax: 6.625% (adult-use only; medical tax-exempt)

- Municipal option tax: Up to 2% (most municipalities charge 0-2%)

- SEEF (cultivation tax): $2.50/oz ($40/lb)

- Total effective burden: ~15-20% (comparable to Colorado 15%, lower than Massachusetts 20%, far lower than Illinois 25-40%)

The real culprit: Supply scarcity

Wholesale prices tell the story:

- New Jersey: $2,600/lb (May 2025, among nation's highest)

- National average: $1,050/lb

- Michigan: $225/lb (91% lower than NJ!)

- California: $259/lb (90% lower than NJ!)

- Oregon: $180/lb (93% lower than NJ!)

New Jersey wholesale costs 2.5× national average, 11× Michigan.

Why supply remains constrained:

- Limited operational cultivators: 515 licenses awarded, only ~150-200 actively growing at scale

- Capital barriers: Licensed cultivation facilities cost $3-8M to build and operationalize

- Slow licensing conversion: Conditional-to-annual approval takes 6-18 months

- Indoor-only economics: New Jersey weather and municipal restrictions effectively require indoor grows (3-5× more expensive than greenhouse/outdoor)

- 63% municipal opt-outs: Limit cultivation site options

- No interstate commerce: Can't import surplus from Michigan/Oregon to alleviate shortages

Framework prediction: As new cultivators operationalize (2025-2026), wholesale prices will decline toward $1,200-1,800/lb, retail prices toward $200-260/oz. But this takes 2-4 years without policy intervention to accelerate supply expansion.

The Fragmentation Problem: 63% Municipal Opt-Outs

New Jersey municipal landscape:

- Total municipalities: 564

- Permit cannabis businesses: 207 (37%)

- Ban or restrict: 357 (63%)

- At least one operation in all 21 counties: Yes (minimally)

Comparison to other fragmented markets:

- California: 61% ban (tied for worst with NJ)

- New York: ~40% ban

- Massachusetts: ~30% ban

- Michigan: ~25% ban

- Connecticut: ~35% ban

Framework significance: Fragmentation is the SECOND most damaging variable after price competitiveness (applies -0.20 to -0.25 penalty to legal market share).

Impact:

- Creates "cannabis deserts" where residents must travel 30-60 minutes to dispensary

- Some choose illicit convenience over legal travel

- Concentrates dispensary competition in permitting municipalities (inflates real estate, reduces profitability)

- Drives cultivator costs higher (fewer viable locations)

New Jersey's 63% opt-out rate partially explains the 48-55% legal market share underperformance.

The Looming Disasters: Three Ways to Destroy a Cannabis Market

New Jersey currently faces three policy threats that would transform underperformance into catastrophic failure.

Disaster #1: Governor Murphy's 500% SEEF Tax Increase

Current SEEF: $2.50 per ounce ($40 per pound)

Murphy's FY2026 proposal: $15 per ounce ($240 per pound)

Increase: 500% (sixfold)

The proposal also includes $30/oz ($480/lb) SEEF on hemp-derived THC products.

Why this would be catastrophic:

Wholesale impact:

- Current burden: $40/lb on $2,600/lb wholesale = 1.5% of cost (minimal)

- Proposed burden: $240/lb on $2,600/lb wholesale = 9.2% of cost (significant)

- Added retail cost: $6-8 per eighth (cultivators will pass through to dispensaries, dispensaries to consumers)

Retail price impact:

- Current: $48-60/eighth

- Post-SEEF increase: $54-68/eighth

- Illicit: $30-40/eighth (unchanged)

- Price gap widens from 40-50% to 50-70%

Framework prediction (CBDT model):

Current scenario (SEEF $2.50/oz):

- Legal market share: 48-55%

- Legal market size: $1.05B annually

- Sales tax revenue: $70M

- SEEF revenue: $2.5M

- Total state revenue: $72.5M

Proposed scenario (SEEF $15/oz):

- Legal market share: 35-45% (consumers flee to illicit due to higher prices)

- Legal market size: $700-900M annually (-15 to -33%)

- Sales tax revenue: $46-60M (-34 to -14%)

- SEEF revenue: $7.0-9.0M (6× rate but smaller base)

- Total state revenue: $53-69M (-8% to -27% DECLINE)

Why higher tax rates generate LESS revenue:

Price increases → consumers shift to illicit → legal sales volume declines → sales tax base shrinks → SEEF applies only to legal sales (can't tax illicit market) → total revenue DECLINES despite higher rate.

This is the fundamental mistake Illinois made: High per-unit taxation that destroys legal market volume, generating less total revenue than moderate taxation with higher legal market share.

Economic research across 24 markets demonstrates: Revenue optimization comes through VOLUME (legal market share) not RATE (per-unit tax).

Industry impact:

- 20-30% of marginal dispensaries close (cannot compete at higher prices)

- Social equity businesses disproportionately harmed (newer, less capitalized)

- MSO consolidation accelerates (only well-funded operators survive)

- Investment in New Jersey market declines

Social equity catastrophe:

Remember those extraordinary growth numbers? +56.8% social equity business growth, +87.6% microbusiness growth, +98.1% prior conviction owner growth?

All those gains reverse if SEEF increases to $15/oz. Social equity businesses serve price-conscious communities. When legal cannabis becomes 50-70% more expensive than illicit, those communities cannot participate in legal market—destroying social equity through economic exclusion.

The political scandal:

$7M+ in SEEF funds collected since 2022, $0 disbursed to impact zones. Murphy administration proposes 500% tax increase while not spending existing revenue supposedly dedicated to community reinvestment.

Framework recommendation: REJECT the SEEF increase. Instead, REDUCE SEEF to $1/oz as supply increases and wholesale prices decline. Lower rate, higher volume, MORE total revenue.

Disaster #2: S4154 Consumer Criminalization—Unprecedented and Counterproductive

Bill: S4154 (Scutari, introduced February 2025)

Status: Pending Senate Judiciary Committee (no vote taken after May 29 hearing)

Provisions:

- Third-degree crime for operating unlicensed cannabis business (3-5 years prison, $15,000 fine)

- Second-degree crime for leading illegal cannabis business network (5-10 years prison, $150,000 fine)

- Disorderly persons offense for knowingly purchasing from unlicensed source (up to 6 months jail, $1,000 fine)

Point #3 is UNPRECEDENTED: No other legal state criminalizes consumers based on where they purchase cannabis.

Sponsor's rationale (Sen. Scutari):

"We would not accept the corner store that didn't have a liquor license to sell liquor. We should not accept the corner store selling cannabis product without a license."

Framework analysis: This confuses symptoms with disease.

The actual problem:

- Legal cannabis costs $48-60/eighth

- Illicit cannabis costs $30-40/eighth

- Consumers rationally choose 40-50% savings

S4154's "solution":

- Criminalize consumers for making economically rational choice

- Up to 6 months jail for buying from "wrong" source

- $1,000 fine (exceeding cost savings from multiple illicit purchases)

Why this fails:

Framework insight: Enforcement COMPLEMENTS price competitiveness; it doesn't REPLACE it.

Successful enforcement model (Michigan):

- Competitive legal prices ($83/oz)

- Strong enforcement against SUPPLIERS (50+ agents, $10M+ budget)

- Result: 85% legal market share

Failed enforcement model (New Jersey S4154):

- Uncompetitive legal prices ($300-350/oz)

- Punish CONSUMERS for high legal prices

- Result: Predicted 35-45% legal market share (worse than current)

Cannabis advocates' response:

- "Deeply unethical" (Bill Caruso, attorney)

- "Could arrest people with cancer for accessing medicine" (Michael Brennan, medical patient advocate)

- "Opposite of what legalization set out to achieve" (Grant, Coalition for Medical Marijuana)

Alternative approach:

Better enforcement targets SUPPLIERS, not consumers:

- Large-scale illegal cultivation (1,000+ plants)

- Unlicensed storefronts (brick-and-mortar operations)

- Interstate trafficking networks

- Budget: $10-15M annually, 20-30 dedicated agents

Combined with price competitiveness (via supply expansion + federal reform), supplier-focused enforcement achieves 70-80% legal market share.

Framework recommendation: REJECT S4154. Implement supplier-focused enforcement AFTER making legal prices competitive. Enforcement without price competitiveness = wasted resources + new criminal records + no market improvement.

Disaster #3: 63% Municipal Opt-Outs—California-Level Fragmentation

Current reality:

- 357 of 564 municipalities (63%) ban or restrict cannabis businesses

- Tied with California (61%) for worst fragmentation among major markets

Impact on legal market:

- Creates geographic access gaps

- Forces 20-40 minute drives for many residents

- Some choose illicit convenience over legal travel

- Concentrates competition (and costs) in permitting municipalities

Framework assessment: Fragmentation penalty = -0.20 to -0.25 on legal market share

Translation: New Jersey's 63% opt-out rate reduces legal market share by 10-12 percentage points below what competitive pricing + adequate access would achieve.

Why municipalities opt out:

- Public safety concerns (largely unfounded—legal cannabis reduces crime)

- Reefer Madness stigma (older residents, conservative areas)

- Fear of federal intervention (diminishing since 2013 Cole Memo)

- Tax revenue not compelling enough (municipalities without fiscal stress)

Solution approaches:

Massachusetts model (partial preemption):

- State allows but doesn't require municipal approval

- Creates opt-out friction but not prohibition

- Result: 70% of municipalities permit over time

Michigan model (incentivized opt-in):

- Revenue sharing with permitting municipalities

- Technical assistance for zoning

- Public education on successful implementation

- Result: 75% of municipalities permit

New Jersey opportunity:

- Increase state revenue sharing from cannabis taxes to permitting municipalities

- Target: 1-2% of state cannabis tax revenue

- Cost: $10-20M annually

- Benefit: Reduce opt-outs from 63% to 40%, improve legal market share 5-8 pp, INCREASE total state revenue through volume

Framework recommendation: Implement municipal incentive program. $15M annual investment to reduce opt-outs generates $40-60M additional state revenue through improved legal market share.

Policy Bills in Play: Bright Spots and Continued Challenges

Beyond the disasters, several bills demonstrate proper policy direction (though none have passed yet).

Home Cultivation Bills: The Missing Link

New Jersey is one of only two adult-use states prohibiting home cultivation (the other is Washington, which also underperforms at 65% legal share).

Pending legislation:

S1985 / A3867 (most comprehensive):

- Adult-use: 6 plants per person, 12 per household maximum

- Medical: 10 plants per patient/caregiver, 12 per household maximum

- Status: Pending committee (no floor votes scheduled)

S1393 / A846 (medical-only):

- Medical patients: 4 mature + 4 immature plants

- Status: Pending committee

Current law: Growing ANY amount is a felony (3-20 years prison depending on plant count)

Why home cultivation matters:

Framework insight: Home cultivation reduces retail sales by 3-7 percentage points but increases TOTAL legal market participation by 8-12 percentage points.

How? Home cultivation provides affordable legal option for price-sensitive consumers who would otherwise buy illicit. 85-90% of consumers still prefer retail convenience, but home grow captures the 10-15% who can't afford $300-350/oz legal prices.

States with home cultivation:

- Michigan (12 plants): 85% legal share

- Massachusetts (6 plants): 78-82% legal share

- Oregon (4 plants): 82% legal share

- Colorado (6 plants): 73-78% legal share

- Connecticut (3 mature + 3 immature): 70-75% legal share

States without home cultivation:

- New Jersey: 48-55% legal share

- Washington: 65% legal share

Correlation clear: Home cultivation improves legal market capture 5-8 percentage points.

Framework prediction for New Jersey:

IF S1985/A3867 passes:

- Legal market share: 48-55% → 56-65% (+8-10 pp improvement)

- Why: Provides affordable legal option ($200-400/oz equivalent for dedicated growers)

- Who benefits: Medical patients (specific strains), budget-conscious consumers, cannabis enthusiasts

- Retail impact: Minimal (85-90% still prefer convenience)

- Total legal market: Expands because home growers replace illicit purchases, not retail purchases

Political challenge: Dispensary lobbying opposes home cultivation, fearing cannibalization. Evidence from 18 states with home cultivation proves fears unfounded—retail sales grow alongside home cultivation as total legal market expands.

Framework recommendation: PASS S1985/A3867. Home cultivation is critical for New Jersey to escape 48-55% legal share stagnation.

Hemp Regulation: S3235/S4509 (Already Passed)

New Jersey successfully addressed hemp-derived intoxicating products in 2024 with emergency legislation:

S3235 / S4509 (signed into law 2024):

- Banned Delta-8, Delta-10, HHC, THC-O, THCP, synthetic cannabinoids

- Prohibited smokable hemp products

- Required CRC licensing for compliant hemp vendors

- Age 21+ restriction

- 180-day emergency rulemaking period

Framework significance: POSITIVE enforcement intervention (unlike S4154 consumer criminalization)

Before hemp ban:

- Unlicensed "gas station weed" competing with licensed dispensaries

- No testing, no age verification, no quality control

- Estimated $40-70M annual market

- Revenue bypassing New Jersey cannabis taxation

After hemp ban:

- Intoxicating hemp must go through licensed dispensary channel OR meet strict requirements

- Eliminates unlicensed competition from convenience stores

- Channels demand to legal market (supports CBDT optimization through enforcement variable)

Framework prediction: +3 to +5 percentage points legal market share from hemp regulation

Comparison:

- Nevada AB 504/SB 356: Similar approach, channels intoxicating hemp through dispensaries

- Minnesota: Separate hemp beverage pathway (bars/liquor stores) = cannibalizes licensed cannabis

- Kentucky/Texas: Permissive hemp = chaos, zero safety oversight

New Jersey approach: Restrictive but rational—protects licensed market while maintaining safety standards.

Predicted Market Outcomes: Three Scenarios

Optimized Scenario: Evidence-Based Reform

Policy changes:

- Federal: Schedule III (280E elimination) + SAFE Banking passage

- State: SEEF maintained at $2.50/oz (NOT increased to $15/oz)

- Supply expansion: Expedite conditional-to-annual conversion, 600-800 cultivators operational by 2027

- Home cultivation: S1985/A3867 passes (6 plants adult-use, 10 plants medical)

- Municipal opt-outs: Reduce from 63% to 40% via revenue-sharing incentives

- Enforcement: $10-15M annual budget targeting suppliers (not consumers), S4154 rejected

Framework inputs:

- Price: g = -0.15 to -0.18 (legal 15-20% more expensive—tolerable gap)

- Access: D = 0.70 (370-450 dispensaries, reduced opt-outs, delivery expansion)

- Safety: S = 0.80 (hemp ban + existing strong standards)

- Convenience: F = 0.75 (SAFE Banking enables cards + home cultivation option)

- Enforcement: E = 0.65 (dedicated budget, supplier focus)

- Fragmentation: F_frag = -0.12 (40% opt-out vs current 63%)

Predicted outcomes:

- Transaction share: 78-85%

- Volume share: 75-82%

- Timeline: 36-48 months after implementation

Economic impact:

- Legal market: $2.8-3.4B annually (vs current $1.05B)

- Illicit market: $450-650M (down from $1.2-1.4B—65% reduction)

- State tax revenue: $195-235M annually (vs current $70M)

- Jobs: 18,000-24,000 (vs current 8,000-12,000)

Comparable performance: Massachusetts (78-82%), approaching Michigan (85%)

This represents what New Jersey legalization SHOULD achieve.

Failed Scenario: Policy Disaster (SEEF Increase + S4154)

Policy changes:

- Federal: No reform (280E remains, no SAFE Banking)

- State: SEEF increased to $15/oz (+$6-8/eighth retail)

- S4154 passes: Consumer criminalization enacted

- Supply: Stagnates (no conditional conversion acceleration)

- Home cultivation: Bills die in committee

- Municipal opt-outs: Remain at 63%

Framework inputs:

- Price: g = -0.35 to -0.40 (legal 50-70% more expensive—catastrophic)

- Access: D = 0.55 (dispensary closures from uncompetitive pricing)

- Safety: S = 0.78 (unchanged)

- Convenience: F = 0.45 (cash-only, no home cultivation)

- Enforcement: E = 0.40 (S4154 marginally improves but wrong focus)

- Fragmentation: F_frag = -0.22 (unchanged 63%)

Predicted outcomes:

- Transaction share: 38-48%

- Volume share: 35-45%

- Timeline: 24-36 months degradation

Economic impact:

- Legal market: $700-900M annually (-15 to -33% from current)

- Illicit market: $1.5-1.8B (growing from current $1.2-1.4B)

- State tax revenue: $53-69M annually (-8% to -27% DECLINE)

- Jobs: 6,000-9,000 (layoffs from dispensary closures)

- Dispensary closures: 20-30% of current operators

- Social equity: Catastrophic collapse (56.8% growth → negative growth)

Comparable performance: Worse than California (50%), approaching New York (30%)

This represents Illinois-level policy failure despite New Jersey's superior structural advantages.

Most Likely Scenario: Muddling Through

Policy changes:

- Federal: Schedule III passes (280E eliminated), SAFE Banking uncertain

- State: SEEF maintained at $2.50/oz (Murphy's increase rejected by Legislature)

- Supply: Gradual expansion as new cultivators operationalize (no policy acceleration)

- Home cultivation: S1985/A3867 passes (political momentum strong)

- Municipal opt-outs: Decline gradually to 55% (slow organic improvement)

- Enforcement: Moderate improvement, S4154 rejected

Framework inputs:

- Price: g = -0.20 to -0.23 (legal 20-30% more expensive—moderate gap)

- Access: D = 0.65 (300 dispensaries by 2028)

- Safety: S = 0.80 (hemp ban + standards)

- Convenience: F = 0.70 (SAFE Banking + home cultivation)

- Enforcement: E = 0.55 (moderate improvement)

- Fragmentation: F_frag = -0.18 (55% opt-out)

Predicted outcomes:

- Transaction share: 68-75%

- Volume share: 65-72%

- Timeline: 48-60 months

Economic impact:

- Legal market: $2.0-2.5B annually

- State tax revenue: $135-170M annually

- Jobs: 14,000-18,000

- Illicit market: $650-900M (significant reduction but not optimized)

Comparable performance: Good but not optimal—Connecticut-level (70-75%), below Massachusetts (78-82%)

This represents competent execution without excellence—New Jersey's conservative political culture producing moderate success.

The Federal Policy Barrier

New Jersey cannot achieve optimized outcomes under current federal law. While comprehensive coverage is available in our pillar pages on IRC Section 280E and the SAFE Banking Act, here's why federal reform is critical for New Jersey specifically:

280E: The Hidden Tax Driving Prices Higher

280E prohibits cannabis businesses from deducting ordinary expenses, creating an effective federal tax rate of 40-70% before state taxes. This forces New Jersey dispensaries to raise retail prices 12-18% just to remain viable.

New Jersey impact:

- Already-high prices (supply scarcity) become unbearable when 280E stacks on top

- Small businesses and social equity licensees disproportionately harmed

- Solution: Schedule III rescheduling eliminates 280E, reduces retail prices 12-18%

SAFE Banking: Cash Friction in America's Densest State

Without SAFE Banking Act passage, New Jersey dispensaries operate cash-only, reducing transaction frequency 18-25%.

New Jersey impact:

- Wealthy, tech-savvy population expects seamless card payments

- Cash-only creates significant friction in state accustomed to digital payments

- Mastercard prohibition (August 2023) eliminated debit access for 70-80% of customers

- Solution: SAFE Banking enables card payments, increases transaction frequency 25%, improves capital access

Combined Federal Impact

With Schedule III + SAFE Banking:

- Retail prices drop 12-18% (280E eliminated)

- Transaction frequency increases 20-25% (card payments)

- Capital access improves (banking relationships, business lending)

- Net effect: +10-15 percentage points to legal market share

Without federal reform:

- New Jersey ceiling: 60-68% legal share (even with optimal state policy)

With federal reform:

- New Jersey potential: 75-82% legal share

New Jersey's congressional delegation (Senators Cory Booker, Bob Menendez, House members) should champion both as economic necessity, not cultural endorsement.

Policy Recommendations

New Jersey must act decisively at state and federal levels:

Priority #1: REJECT Governor Murphy's SEEF Increase

Current proposal: $2.50/oz → $15/oz (500% increase)

Framework verdict: CATASTROPHIC for legal market, social equity, and state revenue

Recommendation: Maintain SEEF at $2.50/oz through 2026, consider REDUCTION to $1-1.50/oz as supply expands (2027-2028)

Rationale: Revenue optimization through VOLUME (legal market share), not RATE (per-unit taxation)

Priority #2: REJECT S4154 Consumer Criminalization

Recommendation: Implement supplier-focused enforcement ($10-15M budget, 20-30 agents) targeting large-scale illegal cultivation and unlicensed storefronts

Avoid: Consumer prosecution (counterproductive when legal prices uncompetitive)

Framework insight: Enforcement COMPLEMENTS price competitiveness; doesn't REPLACE it

Priority #3: PASS S1985/A3867 Home Cultivation

Recommendation: Authorize 6 plants adult-use, 10 plants medical

Impact: +8-10 percentage points legal market share (provides affordable legal option)

Political challenge: Industry opposition—counter with evidence from 18 states showing retail grows alongside home cultivation

Priority #4: Accelerate Supply Expansion

Recommendations:

- Expedite conditional-to-annual license conversion (30-60 days vs 6-18 months)

- $50M state loan fund for cultivation facilities (low-interest for social equity)

- Allow greenhouse/outdoor cultivation in appropriate zones (reduce costs 40-70%)

- Target: 600-800 operational cultivators by 2027

Goal: Wholesale prices $800-1,200/lb (vs current $2,600/lb), retail $180-220/oz

Priority #5: Reduce Municipal Opt-Outs via Incentives

Recommendation: Revenue-sharing program (1-2% of state cannabis tax to permitting municipalities)

Cost: $15M annually

Benefit: Reduce opt-outs 63% → 40%, improve legal share 5-8 pp, INCREASE total revenue $40-60M

Priority #6: Federal Reform Advocacy

New Jersey's congressional delegation should champion:

- Schedule III rescheduling (280E elimination)

- SAFE Banking Act passage

Economic argument: Not about endorsing cannabis—about letting New Jersey's democratically-enacted policy succeed

Priority #7: Support Social Equity Through Price Competitiveness

Current success: 56.8% YoY social equity business growth, 98.1% prior conviction owner growth

Threat: SEEF increase destroys growth through economic exclusion

Solution: All price-reduction policies (federal reform, supply expansion, home grow) directly support social equity by making legal cannabis affordable to working-class consumers

Timeline and Economic Projections

Phase 1 (2025-2026): Supply Growth, Price Decline Begins

Current: 240 dispensaries, $2,600/lb wholesale, $300-350/oz retail

Focus:

- New cultivators operationalize

- SEEF increase defeated

- Home cultivation bills advance

- Federal Schedule III process continues

Market performance:

- Legal market: $1.3-1.5B annually (+24-43% from current)

- Legal share: 52-60% (modest improvement)

- Wholesale: Declines to $1,800-2,200/lb

- Retail: Declines to $260-300/oz

Phase 2 (2026-2027): Schedule III + Home Cultivation

Assumes: Schedule III rescheduling + S1985/A3867 passes

Impact:

- 280E eliminated: Prices drop 12-18%

- Home cultivation: Affordable legal option for 10-15% of consumers

Market performance:

- Legal market: $1.8-2.2B annually (+38-47% from Phase 1)

- Legal share: 62-68% (+10-13 pp from Phase 1)

- Tax revenue: $120-150M annually

- Retail: $220-260/oz

Phase 3 (2027-2029): Supply Optimization + SAFE Banking

Assumes: SAFE Banking + 600-800 cultivators operational

Impact:

- Card payments: Transaction frequency +20-25%

- Supply equilibrium: Wholesale $800-1,200/lb

- Retail prices: $180-220/oz (competitive with illicit)

Market performance:

- Legal market: $2.8-3.4B annually (+56-55% from Phase 2)

- Legal share: 75-82% (+13-14 pp from Phase 2)

- Tax revenue: $195-235M annually

- Jobs: 18,000-24,000

- Illicit market: $450-650M (65% reduction from current)

Phase 4 (2029-2032): Optimized Steady State

Sustained outcomes:

- Legal market: $3.0-3.6B annually

- Legal share: 75-82%

- Tax revenue: $200-240M annually

- Jobs: 20,000-26,000

Comparable performance: Massachusetts (78-82%), approaching Michigan (85%)

Economic Reality: What's at Stake

Current Trajectory (No Reform)

2025-2030 projection:

- Legal market stagnates: $1.3-1.6B annually

- Market share erodes: 45-50% by 2030 (worsening)

- Tax revenue disappoints: $85-105M annually

- Illicit market expands: $1.5-1.8B

- Social equity collapses: MSO consolidation

Cumulative cost (2025-2030):

- Lost tax revenue vs optimized: $500-700M over 5 years

- Lost jobs: 8,000-12,000 vs optimized

- Persistent illicit market: $7-9B in black market activity

Optimized Scenario

2025-2030 projection:

- Legal market grows: $3.0-3.6B by 2030

- Legal share: 75-82%

- Tax revenue: $200-240M annually by 2030

- Jobs: 20,000-26,000

Cumulative benefit (2025-2030):

- Additional tax revenue: $500-700M over 5 years

- Additional jobs: 12,000-16,000

- Black market reduction: $4-6B eliminated

The difference: Federal reform + state supply expansion + home cultivation = $100-150M annually in additional tax revenue, 12,000-16,000 jobs, massive public safety improvement.

Conclusion: New Jersey's Choice

New Jersey legalized cannabis with a 67% supermajority to create jobs, generate revenue, and undo prohibition's harms. Three years later, the implementation underperforms structural advantages.

The state possesses everything needed for success:

- Second-highest income nationally

- Highest population density

- Geographic center of 30M-person megalopolis

- Extraordinary social equity momentum (56.8% YoY growth)

- Strong regulatory framework

Yet New Jersey captures only 48-55% of cannabis demand—barely better than California's disaster, worse than Illinois, and 30-37 percentage points below Michigan.

The culprit: Highest cannabis prices in America ($300-350/oz vs $30-40 illicit), driven by supply scarcity, not excessive taxation.

The threat: Governor Murphy proposes 500% SEEF tax increase that would raise prices further, destroy social equity gains, and REDUCE total state revenue despite higher tax rate.

The solution requires:

Federal level:

- Schedule III rescheduling (280E elimination)

- SAFE Banking Act passage

State level:

- REJECT Murphy's SEEF increase to $15/oz

- REJECT S4154 consumer criminalization

- PASS S1985/A3867 home cultivation (6 plants adult-use, 10 medical)

- Accelerate supply expansion (600-800 cultivators by 2027)

- Reduce municipal opt-outs (63% → 40% via revenue incentives)

- Implement supplier-focused enforcement ($10-15M budget)

IF New Jersey implements evidence-based reform:

- Legal market share: 48-55% → 75-82%

- Tax revenue: $70M → $195-235M annually

- Jobs: 8,000-12,000 → 20,000-26,000

- Illicit market: -65% reduction

- Social equity: Thrives through economic accessibility

IF New Jersey continues current path:

- Legal market share: 48-55% → 45-50% (worsening)

- Tax revenue: Stagnates or declines

- Social equity: Collapses (high prices exclude target communities)

- Becomes cautionary tale alongside California, Illinois, New York

The CBDT Framework, validated across 24 states, demonstrates what policy choices produce. Revenue optimization comes through VOLUME (legal market share), not RATE (per-unit taxation). Price competitiveness is 4× more important than any other variable.

New Jersey voters chose legalization. State policymakers chose supply constraints prioritizing incumbent profits over market optimization. Now those choices produce predictable underperformance.

The path to success exists. Massachusetts demonstrates it (78-82% legal share). Michigan proves it (85% legal share). Connecticut pursues it (70-75% projected).

New Jersey can join the success stories or cement its position as a failure alongside Illinois and California. The choice is entirely policy-driven.

67% of New Jersey voters supported legalization to create opportunities and undo prohibition's harms. Three years later, policymakers must honor that mandate by implementing policies that actually work—not symbolic gestures that sound good while ensuring failure.

The framework provides the roadmap. The data demonstrates what works. The question is whether New Jersey will learn from evidence or repeat ideological mistakes.

New Jersey can harvest its potential. The question is whether political courage exceeds incumbent industry lobbying.

The Garden State's cannabis market future is a choice, not destiny.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Delaware | Florida | Ohio | Washington DC

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0