New Mexico Cannabis Market Analysis: How the Land of Enchantment Could Reach 82% Market Share With Tribal-Led Reform

Using the CBDT Framework to understand why New Mexico achieves 70-75% legal share in just 3.5 years—and how federal reform plus competitive taxation could reach 82-86%

The Silent Majority 420 | November 2025

The Border State Advantage

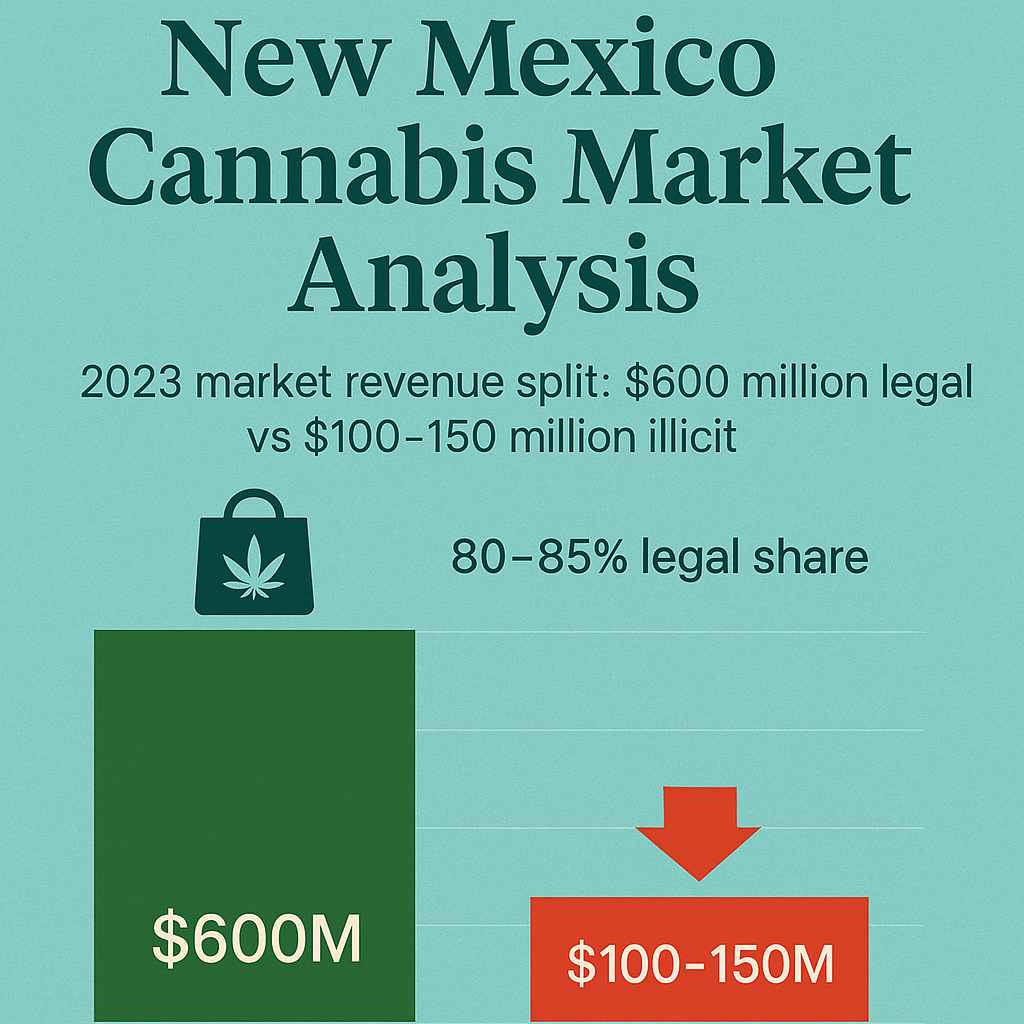

New Mexico launched adult-use cannabis sales on April 1, 2022, and immediately demonstrated what strategic geography combined with sound policy can accomplish. Within three and a half years, the state generated nearly $2 billion in total cannabis sales—a remarkable achievement for a state of just 2.1 million residents.

The secret? Texas tourism and smart policy design.

Sunland Park, a small border city of 17,000 residents, sits adjacent to El Paso, Texas—a metropolitan area of 900,000 where cannabis remains completely prohibited. Since opening day in 2022, Texas residents have flooded across state lines, creating consistent demand that generates approximately $100 million annually just in border communities. Sunland Park alone captures $4 million monthly—second only to Albuquerque despite having a tiny population.

But New Mexico's success extends far beyond border tourism. The state has accomplished what many others have failed to achieve: creating a functional cannabis market with moderate taxation, generous home cultivation rights, minimal geographic fragmentation, and rapid supply expansion that drives competitive pricing.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals New Mexico's position: The state currently achieves approximately 70–75% legal market share—solid mid-tier performance that outperforms California (50%), Illinois (55-60%), and New York (30%).

Yet New Mexico could achieve even better outcomes. The framework predicts that with federal reform (Schedule III rescheduling eliminating 280E penalties and SAFE Banking Act passage enabling normal banking), plus stabilization of the state's escalating tax rates through pending legislation (SB 89), New Mexico could improve from 70-75% to 82-86% legal market share within 36-48 months.

This matters because every percentage point of market share represents better public safety outcomes, more tax revenue, and reduced organized crime activity. New Mexico has done most things right—now it's time to optimize.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Market Performance: Rapid Growth from Young Market

New Mexico's cannabis market demonstrates impressive trajectory despite the state's modest population.

Sales Performance (Through October 2025)

2025 Performance:

- Projected annual sales: $570-585 million

- Adult-use sales: $440-455 million (77% of total)

- Medical sales: $130 million (declining as percentage but stable in absolute terms)

- Monthly average: $44-47 million

- Year-over-year growth: 7.5%

All-Time Performance (April 2022–October 2025):

- Total cumulative sales: $1.97 billion

- Adult-use: $1.42 billion

- Medical: $562 million

- Total transactions: 44+ million

- Tax revenue collected: $142+ million in summer 2025 alone

Per-Capita Performance:

- Annual sales per resident: $270-280

- Comparable to Arizona ($260-280) despite being a younger market

- Below Colorado ($310-330) but approaching maturity

Geographic Concentration: The Border Effect

Top three markets by cumulative sales:

- Albuquerque: $220-235 million (state's largest city, 560,000 population)

- Sunland Park: $100-110 million (population 17,000—$5,880-6,470 per capita)

- Las Cruces: $65-75 million (population 112,000, also near El Paso)

The Texas Tourism Factor:

Sunland Park's extraordinary performance reveals the power of border proximity. With per-capita sales 15-20× the state average, an estimated 70-80% of customers are Texas residents making quick trips across state lines. Some border dispensaries advertise on El Paso billboards, offer drive-through service, and provide "Texas Tuesday" discounts.

Texas prohibition directly subsidizes New Mexico's cannabis economy. Every dollar spent by El Paso residents in Sunland Park represents tax revenue Texas could capture if legalization occurred. Tourism generates an estimated 20-25% of New Mexico's total market—$120-145 million annually.

Market Structure: Aggressive Licensing Strategy

License Distribution (as of November 2025):

- Total licenses issued: 2,873

- Retail dispensaries: 1,050+ licensed (~633 operationally active)

- Producers/cultivators: 878 licensed

- Micro-producers: 459 licensed

- No license caps: Market-driven approach

New Mexico pursued aggressive licensing similar to Michigan and Oklahoma. This created oversupply, compressed wholesale prices (down 40% from $4,000/lb in 2022 to $2,200-2,500/lb in 2025), and forced market consolidation—painful for marginal operators but beneficial for consumers through competitive pricing.

Approximately one-third of licensed businesses have closed since 2022. This is normal market consolidation, not policy failure.

Tax Structure: Moderate But Escalating

Current Tax Burden (as of July 2025):

- Cannabis excise tax: 13% (increased from 12% on July 1, 2025)

- Scheduled increases: +1% annually until reaching 18% in July 2030

- Gross receipts tax: 5-9% (varies by location)

- Total effective burden: 18-22% currently, rising to 23-27% by 2030

Revenue Distribution:

- State general fund: ~67% of excise tax

- Local municipalities: ~33% of excise tax (allocated to location where sale occurred)

Comparison to Other Markets:

- Michigan: 16% total (10% excise + 6% sales)

- Colorado: 19-23% effective

- Illinois: 25-40% effective

- Oregon: 17% total

New Mexico's current 18-22% burden sits in the moderate-competitive range. The scheduled increase to 23-27% by 2030 moves toward less competitive territory, potentially threatening market share gains.

Critical Policy Battle: Senate Bill 89 would freeze the excise tax at 12-13% instead of allowing increases to 18%. This bill represents New Mexico's most important cannabis policy decision since legalization. Full CBDT analysis of SB 89 coming soon, demonstrating why revenue optimization comes through market share (volume) rather than tax rates.

What New Mexico Gets Right

New Mexico avoided most common policy mistakes that destroyed California, Illinois, and New York:

Moderate Initial Taxation

Starting at 12% excise tax allowed rapid market development without pricing legal cannabis out of reach. The state resisted revenue maximization temptation that destroyed California and Illinois early markets.

No License Caps

Unlike New Jersey or New York, New Mexico allowed market forces to determine retail density. Result: 1,050+ licenses issued, consumer access maximized, prices driven down through competition.

Minimal Geographic Fragmentation

State law prevents most local retail bans. New Mexico avoided California's disaster (61% of jurisdictions ban retail), which fragments markets and creates illicit supplier havens.

Home Cultivation Allowed

Adults 21+ can grow up to 6 mature plants and 6 immature plants for personal use (12 mature plant household maximum). Personal cultivation complements retail rather than competing with it, providing affordable options for budget-conscious consumers without cannibalizing retail sales.

New Mexico's home cultivation success validates framework predictions: allowing personal growing captures illicit demand (people who would never pay retail prices anyway) rather than displacing retail sales. The state's thriving $2 billion market proves home cultivation doesn't "destroy" commercial operations.

Delivery Authorized

Statewide delivery reduces geographic access barriers. Courier licenses enable service to rural areas, preventing fragmentation effects.

Comprehensive Testing Standards

Mandatory testing for potency, pesticides, heavy metals, microbial contaminants, and residual solvents establishes quality advantage over illicit markets.

New Enforcement Bureau (House Bill 10)

In 2025, New Mexico created the Cannabis Control Division Enforcement Bureau with 7 dedicated personnel and $1.6 million budget. This supplier-focused enforcement approach targets large-scale illegal operations rather than consumers—the correct strategy for legal market optimization.

Full CBDT analysis of HB 10's enforcement approach coming soon, examining how supplier interdiction complements (but cannot replace) price competitiveness.

Framework Assessment: New Mexico's Current Position

The CBDT Framework reveals New Mexico achieves solid mid-tier performance with clear optimization pathways.

Current Performance: 70-75% Legal Market Share

Transaction share: Estimated 75-80% (percentage of users choosing legal over illicit for at least some purchases)

Volume share: Estimated 70-75% (accounting for heavy user behavior patterns)

This places New Mexico in strong mid-tier territory, significantly outperforming:

- California (50%)

- Illinois (55-60%)

- New York (30%)

- New Jersey (48-55%)

But underperforming optimization leaders:

- Michigan (85%)

- Oregon (82%)

- Nevada (88-92%)

Why New Mexico Succeeds Relative to Struggling Markets

Price Competitiveness (4× weight): COMPETITIVE

Current pricing:

- Legal retail: $228-284/ounce (mid to high quality)

- Legal concentrates: $25-40/gram

- Medical prices: 10-15% lower than adult-use

Illicit pricing (estimated):

- Flower: $180-250/ounce

- Concentrates: $18-28/gram

Legal premium over illicit: 15-30%—higher than optimal but not catastrophic like Illinois (40-60%) or California (35-50%).

New Mexico's moderate tax burden (currently 18-22% total) combined with supply expansion (wholesale prices down 40% since 2022) allows reasonable price competitiveness. The framework shows markets fail when legal prices exceed illicit by >40%. New Mexico stays well below this threshold.

Challenge: Scheduled tax increases to 18% excise (23-27% total) by 2030 will compress price competitiveness unless wholesale costs decline further. SB 89 would prevent this deterioration.

Access Density (1× weight): EXCELLENT

- 1,050+ retail licenses issued

- Population 2.1 million = ~50 stores per 100K residents (theoretical max if all operational)

- Operational dispensaries estimated at 400-500 = 19-24 per 100K—excellent density

Comparison:

- Oregon: 16.8 per 100K (oversaturated)

- Colorado: 10+ per 100K

- California: 4.2 per 100K (fragmentation disaster)

- New Mexico: 19-24 per 100K (strong)

Delivery authorized statewide further expands effective access. New Mexico avoided fragmentation that destroyed California and constrained New Jersey.

Safety/Quality (1.2× weight): STRONG

New Mexico implements comprehensive testing requirements:

- Potency testing (THC/CBD content)

- Pesticide screening

- Heavy metals testing

- Microbial contaminant testing

- Residual solvent testing for concentrates

Quality advantage over illicit market is clear. However, research shows consumers value safety certification enough to pay ~10-15% premiums, not 30-40%. Quality cannot overcome excessive price premiums.

Convenience (includes payment friction): WEAK

Banking access remains severely limited:

- Estimated 10-15 banks/credit unions serve cannabis businesses

- All operate discreetly, charge 3-5× normal fees

- Cash remains primary payment method for most dispensaries

- Federal Reserve research shows cash-only reduces transaction frequency 18-25%

Payment friction costs New Mexico approximately 8-12 percentage points of potential market share. Without SAFE Banking Act passage, this ceiling persists.

Enforcement (0.6× weight): ADEQUATE, IMPROVING

The new Cannabis Control Division Enforcement Bureau (7 agents, $1.6M budget) represents the correct supplier-focused approach. While smaller than Michigan's operation (50+ agents, $10M+ budget), it's appropriate for New Mexico's smaller market.

Enforcement focuses on:

- Unlicensed cultivation operations

- Interstate trafficking (particularly to Texas)

- Sales to minors

- Product safety violations

Market Fragmentation Penalty: MINIMAL

New Mexico avoided the fragmentation disaster that destroyed California (61% local bans) and constrained Massachusetts (~40% bans). State preemption prevents most local prohibition.

The Framework Verdict

New Mexico achieves 70-75% legal market share—solid mid-tier performance. The state:

- Avoided policy disasters that destroyed California, Illinois, New York

- Implemented moderate taxation, aggressive licensing, minimal fragmentation

- Captured border tourism effectively ($120-145M annually)

- Built comprehensive testing/safety framework

- Validated home cultivation framework predictions (retail thrives despite cultivation rights)

- Created supplier-focused enforcement approach

Limitations:

- Federal barriers (280E, SAFE Banking) cost 8-12 points of market share

- Tax escalation schedule threatens price competitiveness (SB 89 addresses this)

- Payment friction reduces convenience

- Medical program declining (28-35% from peak)—though this represents normal adult-use cannibalization, not policy failure

Federal Policy Barriers: The Optimization Ceiling

New Mexico's optimization potential is limited not by state policy choices but by federal prohibition remnants that survive even in legalized states.

The 280E Tax Penalty

Internal Revenue Code Section 280E, enacted in 1982, prohibits cannabis businesses from deducting ordinary business expenses. This creates effective federal tax rates of 40-70% even before state taxes apply.

Impact on New Mexico dispensaries:

- Cannot deduct: rent, utilities, salaries, marketing, insurance, security

- Can deduct: only cost of goods sold (wholesale cannabis cost)

- Forces retail prices 12-18% higher just to survive federal tax burden

- Makes already-moderate state taxes (18-22%) problematic when combined with 280E

Solution: Schedule III rescheduling (currently under DEA consideration) would eliminate 280E, allowing normal business deductions. This single change would reduce legal prices by 12-18% industry-wide.

SAFE Banking Crisis

Without SAFE Banking Act passage, New Mexico cannabis businesses remain largely unbanked:

Current banking situation:

- ~10-15 New Mexico banks/credit unions serve cannabis businesses

- Services provided at 3-5× normal fees

- Constant risk of account closure

- Mastercard ceased processing cannabis debit transactions (August 2023)

Impact on operations:

- Cash-only reduces transaction frequency 18-25%

- Security costs: $40,000-120,000 annually per location

- Armored transport: $400-1,800 per pickup

- Younger, tech-savvy consumers particularly frustrated

- Border tourism impacted (Texas visitors accustomed to card payments)

SAFE Banking impact: Would increase transaction frequency 18-25%, reduce security costs, expand delivery viability, and add 8-12 percentage points to legal market share.

Price Trends: Supply Expansion Working

New Mexico's wholesale cannabis prices have declined dramatically since market launch:

Wholesale Price Trajectory:

- 2022 (launch): $4,000/pound

- 2023: Down 30% to ~$2,800/pound

- 2024: Down additional 13% to ~$2,400/pound

- 2025: Currently $2,200-2,500/pound

Result: Retail prices declining despite tax increases. Mid-quality flower now $228/ounce, down from $300+ at launch.

Industry Perspective: Operators complain about "oversupply" and "price compression"

Framework Perspective: Price competition is GOOD—improves legal market competitiveness

This validates the framework's core principle: revenue optimization comes through market share (volume) captured, not tax rates (per-unit).

The Critical Policy Choice:

Path 1 - Let market work (pass SB 89):

- Prices continue declining through competition

- Market consolidation occurs naturally

- Legal market share: 80-85% by 2028

- Tax revenue: $150-170M annually (lower rate × larger base)

Path 2 - Tax increases proceed (current law):

- Scheduled increases offset price declines

- Retail prices stay flat despite wholesale declines

- Legal market share: 65-72% by 2028

- Tax revenue: $115-135M annually (higher rate × smaller base)

The paradox: Lower taxes with higher market share generate MORE total revenue than higher taxes with market share erosion.

Texas Border Dynamics: The $120-145 Million Question

New Mexico's geography creates unique competitive advantages through border proximity to Texas, the nation's second-largest state by population and economy.

Texas Market Context:

- Population: 30+ million

- El Paso metro: 850,000+

- Cannabis status: Prohibited (limited medical CBD only)

- Illicit market: Estimated $6-8 billion annually

- Legalization timeline: Uncertain, likely 2027-2030 at earliest

New Mexico Border Communities Performance:

- Sunland Park: $100-110M cumulative (70-80% Texas customers)

- Las Cruces: $65-75M cumulative (significant Texas tourism)

- Deming: $5M+ (disproportionate for small town)

- Combined border tourism: $120-145M annually (20-25% of state market)

Risk Factor: Texas Legalization

If Texas legalizes cannabis, New Mexico would lose $95-135M in annual border tourism revenue. However:

- Timeline uncertain: Texas political environment suggests 2027-2030 at earliest

- New Mexico advantages persist: More competitive prices, established infrastructure, better location for West Texas

- Optimization offsets: Federal reform + competitive taxation could recapture lost tourism through resident demand

Even with Texas legalization, optimized New Mexico maintains $720-840M annual market.

Medical Program Cannibalization: Not a Problem

New Mexico's medical cannabis sales have declined 28-35% from peak:

- Peak: $15.3M monthly (March 2023)

- Current: $10-11M monthly (October 2025)

Why occurring:

- Adult-use more convenient (no card required)

- Price similarity despite medical tax exemption

- More adult-use retailers (1,050 vs. fewer medical-only)

- Home cultivation (adult-use allows 6 plants, reducing medical PPL benefit)

Framework Assessment: This is normal market evolution, NOT policy failure.

Impact on total legal market: NONE (shift from medical to adult-use still legal)

Revenue impact: Medical decline is revenue POSITIVE for state (+$25M annual tax revenue from shifted purchases)

Medical program advantages remaining:

- Tax exemption (saves 18-21% total)

- Higher possession limits (8 oz/90 days)

- Higher plant count (16 vs. 12 for adult-use)

- Employment protections

Optimized Scenario: What New Mexico Could Achieve

With federal reform + tax stabilization through SB 89 + continued supply expansion:

Policy Changes:

- Schedule III eliminates 280E (prices decline 12-18%)

- SAFE Banking enables card payments (transaction frequency up 18-25%)

- SB 89 passes (tax frozen at 13-14% vs. increasing to 18%)

- Enforcement bureau expands to 15+ agents

Market Response:

- Price-sensitive consumers shift from illicit to legal

- Heavy users complete transition (prices now competitive)

- Rural consumers gain better access (cashless delivery viable)

- Legal market captures volume share, not just transaction share

Predicted Outcomes (36-48 months post-implementation):

- Legal market: $850-950M annually (vs. current $570-585M projection)

- Legal market share: 82-86% (vs. current 70-75%)

- State tax revenue: $150-170M annually (vs. current $105-115M projection)

- Jobs: 12,000-15,000 (vs. current 8,000-10,000)

- Illicit market: Reduced from $200-250M to $90-120M

The difference: Federal reform + SB 89 passage = $280-365M additional annual legal sales worth $45-55M in additional state revenue.

Policy Recommendations

Priority #1: Pass SB 89 (Tax Stabilization)

Senate Bill 89 would freeze cannabis excise tax at 12-13% instead of allowing increases to 18% by 2030.

Why critical: Framework analysis across 24 states shows legal markets struggle when total tax burden exceeds 22-25%. New Mexico's scheduled path moves from current 18-22% to eventual 23-27%—approaching Illinois-level failure territory.

Revenue optimization principle:

- Lower rate (13%) × larger market share (82%) = Higher total revenue

- Higher rate (18%) × smaller market share (68%) = Lower total revenue

Full CBDT analysis of SB 89 coming soon.

Priority #2: Expand Enforcement Bureau

Current 7 agents adequate for 2.1M population, but scaling to 15+ agents would improve enforcement variable from 0.60-0.70 to 0.70-0.80.

Budget: $3-5M annually (up from $1.6M) Focus: Large-scale illegal cultivation, interstate trafficking to Texas ROI: Every $1M in enforcement spending returns $3-5M in additional legal market capture

Full CBDT analysis of HB 10 enforcement approach.

Priority #3: Federal Reform Advocacy

New Mexico's congressional delegation should champion Schedule III and SAFE Banking as:

- States' rights issue (let New Mexico's voter-approved policy succeed)

- Border security issue (reduce illicit trafficking to Texas)

- Economic development issue (job creation, legal business support)

- Rural access issue (cashless delivery enables underserved communities)

Priority #4: Maintain Pro-Access Policies

DO NOT:

- Implement license caps

- Allow local retail bans

- Restrict delivery authorization

- Reduce home cultivation limits

DO:

- Continue market-driven licensing

- Maintain state preemption of local bans

- Expand delivery infrastructure

- Support home cultivation as complement to retail

Comparison to Other Young Markets

New Mexico's 70-75% legal share in 3.5 years represents strong performance among recently launched markets:

Better Performance:

- Arizona (70-75%, launched 2021)

- Connecticut (65-70%, launched 2023)

- Montana (75-78%, launched 2022)

Worse Performance:

- New Jersey (48-55%, launched 2022)

- New York (30%, launched 2023)

- Delaware (55-65%, launched 2025)

Established Market Comparisons:

- Michigan (85%, launched 2019)—New Mexico's realistic goal

- Colorado (84%, launched 2014)—mature market leader

- Oregon (82%, launched 2015)—oversupply creates extreme price competitiveness

New Mexico's trajectory: With federal reform + SB 89 passage, could match or exceed Michigan within 4-5 years of launch.

Timeline and Economic Projections

Phase 1 (Current—2026): Consolidation with Tax Pressure

- Legal market: $570-630M annually

- Market share: 68-73% (slight erosion from tax increases)

- Tax revenue: $105-120M annually

- Key challenge: Tax increases begin (13% → 14% → 15%)

Phase 2 (2026-2027): Federal Reform Implementation

Assumes Schedule III rescheduling completed and SAFE Banking passed:

- Businesses save $45-65M annually in federal taxes (280E elimination)

- Savings partially passed to consumers (8-12% price reductions)

- Card payment access improves convenience dramatically

- Legal market: $670-750M annually (+17-27%)

- Market share: 73-77% (+5-9 points)

- Tax revenue: $125-145M annually

Phase 3 (2027-2029): Optimization with SB 89

Assumes SB 89 passes, freezing excise tax at 13-14%:

- Price competitiveness maintained despite ongoing wholesale declines

- Heavy users complete transition to legal market

- Border tourism sustained

- Legal market: $850-950M annually

- Market share: 82-86%

- Tax revenue: $150-170M annually

- Jobs: 12,000-15,000

Phase 4 (2029-2032): Mature Market

Even if Texas legalizes, optimized New Mexico maintains strong performance through resident demand:

- Legal market: $720-840M annually (accounting for potential Texas legalization)

- Market share: 80-84%

- Tax revenue: $135-160M annually

Cumulative Opportunity (2025-2030):

- Additional state tax revenue: $180-240M over 5 years (optimized vs. current trajectory)

- Reduced illicit market: $900-1,250M in black market eliminated over 5 years

What the Data Tells Us About Cannabis Safety

New Mexico's cannabis legalization includes comprehensive testing and quality control standards that create significant safety advantages over prohibition. The state's regulated market ensures consumers receive laboratory-tested products free from pesticides, heavy metals, and dangerous contaminants—protections entirely absent in illicit markets. This harm reduction through regulation demonstrates why legalization with proper oversight creates better public health outcomes than prohibition combined with thriving black markets.

Conclusion: Young Market Success Story with Optimization Potential

New Mexico has accomplished in three and a half years what many states failed to achieve in a decade: functional cannabis legalization that generates substantial revenue, creates jobs, reduces illicit markets, and—uniquely—validates the home cultivation framework through market success despite generous cultivation rights.

The numbers tell the story:

- $2 billion cumulative sales (April 2022–October 2025)

- 70-75% legal market share (solid mid-tier, outperforming California/Illinois/New York)

- 1,050+ retail licenses issued (no artificial scarcity)

- Moderate taxation (18-22% currently—competitive range)

- Home cultivation success (retail thrives with 6+6 plant rights)

- Border tourism ($120-145M annually from Texas visitors)

- Strong enforcement approach (supplier-focused, not consumer criminalization)

New Mexico avoided the policy disasters that destroyed California (high taxes + fragmentation), Illinois (extreme taxation), and New York (regulatory dysfunction).

But New Mexico could achieve more. The CBDT Framework reveals current 70-75% legal share could improve to 82-86% with:

- Federal reform: Schedule III eliminates 280E (prices decline 12-18%), SAFE Banking enables card payments (transaction frequency up 18-25%)

- SB 89 passage: Freeze excise tax at 13-14% instead of allowing increases to 18%

- Enforcement expansion: Scale bureau from 7 to 15+ agents

- Continued supply expansion: Let competitive market drive prices down

The economic stakes:

- $280-365M additional annual legal market activity

- $45-55M additional state tax revenue annually

- 4,000-6,000 additional jobs

- $160-225M reduction in annual illicit market

The policy choice: New Mexico can optimize to 82-86% legal share (Michigan-level performance) or allow tax increases to erode current success. SB 89 and federal reform determine which future New Mexico achieves.

The Land of Enchantment has done most things right. With strategic optimization through pending legislation and federal support, New Mexico could transform from solid performer to optimization exemplar—proving that young markets with sound policy can match or exceed established market leaders.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Arkansas | Iowa | New Hampshire | West Virginia

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0