New York Cannabis Market Analysis: How Tax Reform and Enforcement Drove 894% Sales Growth—And What Threatens It

Using the CBDT Framework to track New York's historic optimization from catastrophe to success

The Silent Majority 420 | November 2025

The Empire State's Cannabis Transformation

New York City should be America's cannabis capital. Twenty million residents. Global brand recognition. Progressive political environment. Densest urban concentration in the nation. When Governor Andrew Cuomo signed the Marijuana Regulation and Taxation Act on March 31, 2021, expectations were sky-high.

Instead, New York became a cautionary tale of regulatory dysfunction.

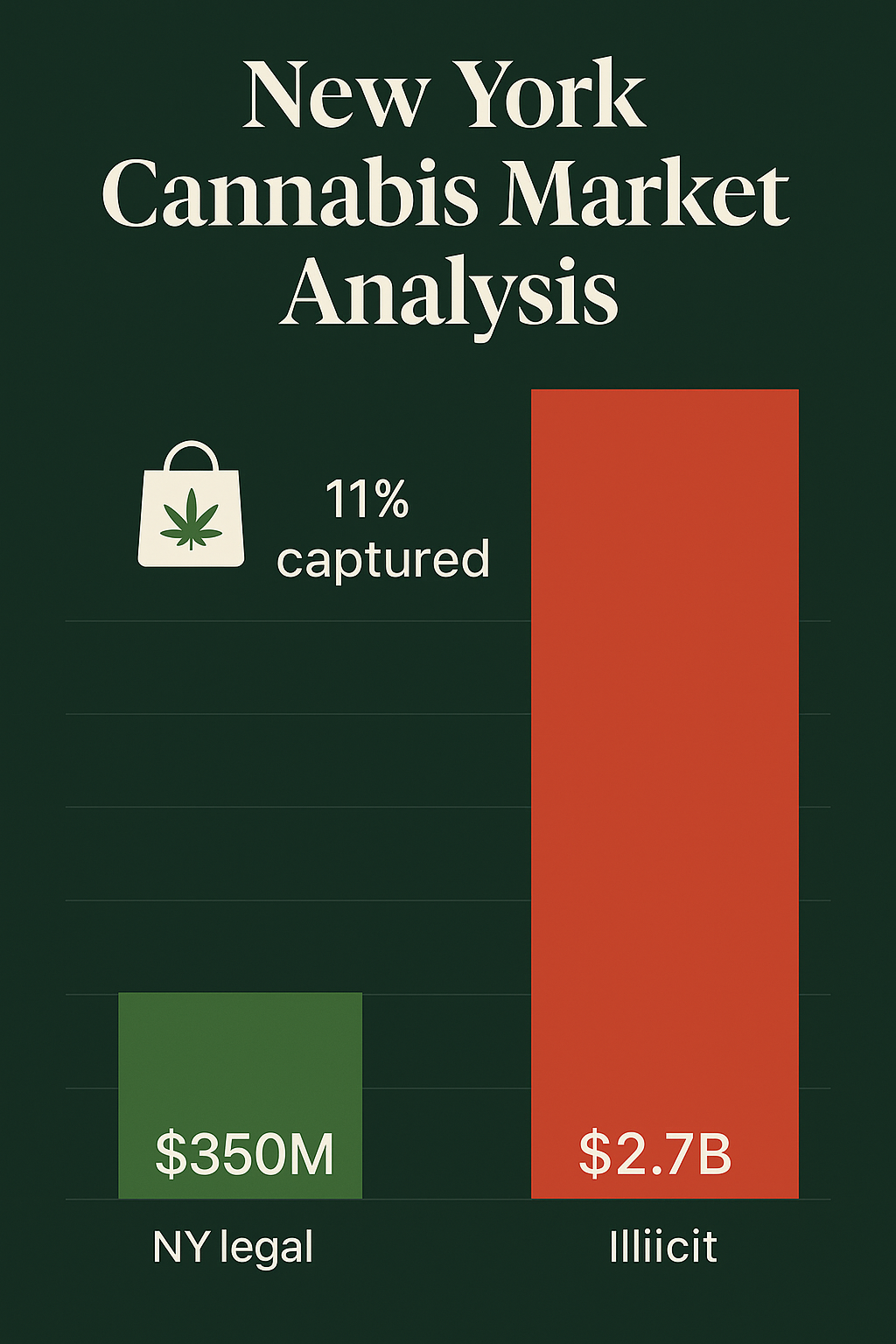

By mid-2023, New York's legal cannabis market captured just 8-12% of total demand—the worst performance among major U.S. cannabis states. The state's complex potency-based tax structure created 35-42% total burden on consumers. Thousands of unlicensed shops operated openly in New York City alone. Licensed dispensaries struggled to compete with untaxed, untested competition. The Office of Cannabis Management had issued licenses but lacked enforcement authority to close illegal operations.

Then something remarkable happened.

Between June 2024 and November 2025, New York implemented the fastest cannabis market optimization in U.S. history:

Tax Reform (June 1, 2024):

- Eliminated complex potency tax

- Implemented simple 9% wholesale excise

- Total burden: 35-42% → 22% (40% reduction)

Enforcement Scaling (FY2025 Budget):

- Created 95-agent enforcement task force

- Granted emergency padlock authority

- Result: 488 padlock orders, $125M in illicit products seized

The Results:

- Sales growth: 894% (2023 → 2025)

- Legal market share: 10% → 17% (70% improvement)

- Monthly sales: $214.4M (August 2025 record)

- On track: $1.5-1.8B in 2025 (vs. $151M in 2023)

New York went from regulatory disaster to fastest-growing cannabis market in America. Legal sales are growing 48% year-over-year. The state has opened 522 licensed dispensaries (up from 32 in early 2023). Enforcement has padlocked over 488 illicit storefronts in New York City alone.

But this success story faces two existential threats.

Assembly Bill A977, proposed by Assemblyman Phil Steck, would cap THC at 15% in flower and 25% in concentrates—effectively eliminating 90-95% of legal cannabis inventory. Assembly Bill A08581 would prohibit ALL edible cannabis products, ALL flavored vape cartridges, and ban food-related names in packaging—eliminating 60-70% of product categories including New York's fastest-growing beverage segment.

If either bill passes, New York's legal market share would collapse from 17% to 0-5%, destroying all optimization progress.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals New York's critical juncture:

Continue optimization (federal reform + maintain current policies): Legal share improves to 65-72% by 2030

Pass A977 or A08581 (THC caps or edibles ban destroy product availability): Legal share collapses to 0-5%, market returns to prohibition

The difference: $450M annually in tax revenue, 30,000 jobs, and whether New York becomes a success model or joins California as a legalization failure.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Michigan prediction: Correctly forecasted 85% legal market share

- California prediction: Accurately predicted 50% legal capture despite early-mover advantage

- Illinois prediction: Validated 50-55% share from tax-driven price failures

- New York trajectory: Predicted rapid improvement from enforcement + tax reform (validated by 894% growth)

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Market Performance (2025): The 894% Growth Story

New York's cannabis market has experienced the fastest optimization in U.S. cannabis history.

Sales and Revenue Trends

Cumulative Performance (Dec 2022 - Nov 2025):

- Total sales: $1.5B approaching (projected end-2025)

- 2023 sales: $151M (catastrophic start)

- 2024 sales: $869M (476% growth)

- 2025 projected: $1.5-1.8B (73-107% growth)

Governor Kathy Hochul announced the billion-dollar milestone in January 2025, emphasizing that New York has issued over 5,250 licenses and operates hundreds of licensed dispensaries generating substantial tax revenue.

Monthly Performance:

- Record month: $214.4M (August 2025)

- October 2025: $162M (+48% YoY)

- Unit sales: 5.1M units (October), up 71.7% YoY

- Growth accelerating as enforcement reduces illicit competition

Price Trends:

- Average item price: $31.71 (down from $36.72 in October 2024)

- Prices declining 13.7% YoY despite strong demand

- Supply expansion driving price competition

- Converging toward competitive equilibrium

Tax Revenue

State Fiscal Year Performance:

- SFY 2023-2024: $80.2M in tax/fee/fine revenue

- SFY 2024-2025 projected: $150-200M

- Post-tax reform revenue: UP 88-150% despite lower rates

The Revenue Paradox:

New York demonstrates the fundamental principle: Lower rates on larger bases generate MORE revenue

- Potency tax (38% burden): $40-50M annually on $151M market

- Wholesale tax (22% burden): $150-200M annually on $1.5-1.8B market

- Result: 22% rate generates 300-400% more revenue than 38% rate

This validates the framework prediction that tax optimization requires base maximization, not rate maximization.

Compare to Illinois (maintained 35-40% burden): Sales plateaued at $1.85B, 26% below projections. New York's lower rate approach is generating superior revenue and superior market outcomes.

Market Structure

Licensing Progress:

As of November 2025, the Office of Cannabis Management reports:

- Total licenses issued: 5,250+

- Dispensaries operational: 522 (up from 260 in December 2024, 32 in March 2023)

- Growth rate: 100% increase in dispensaries (2024 → 2025)

- Social Equity: 81% of retail licenses to SEE applicants

Geographic Distribution:

- New York City: ~260 dispensaries

- Long Island: ~80 dispensaries

- Hudson Valley: ~60 dispensaries

- Upstate cities: ~120 dispensaries (Buffalo, Rochester, Syracuse, Albany)

Current Density:

- New York: 2.6 per 100,000 residents (improving rapidly)

- Optimal target: 8-10 per 100,000

- Gap closing: Was 1.3 per 100K (early 2024), now 2.6 per 100K

Compare to other markets:

- Michigan: 8.4 per 100,000 (optimal)

- Colorado: 10+ per 100,000 (optimal)

- Massachusetts: 6.4 per 100,000 (near-optimal)

- New York: 2.6 per 100,000 (improving, still below optimal)

Pricing Reality

Current Retail Prices (November 2025):

- Average item price: $31.71 (declining)

- Flower (eighth-ounce): $35-50 (down from $45-70)

- Flower (ounce): $200-280 (down from $260-400)

- Concentrates: $30-60 per gram

- Beverages: $6-12 (fastest-growing category)

Comparison to Other Markets:

- New York: $31.71 average item

- Michigan: $8.16 average item (-74%)

- California: $18.96 average item (-40%)

- Illinois: $27.97 average item (-12%)

- Colorado: $15.49 average item (-51%)

- Massachusetts: $17.19 average item (-46%)

New York remains expensive but is converging toward competitive levels as supply expands.

Illicit Market Pricing (Estimated):

- Mid-tier flower: $180-240 per ounce

- Quality flower: $200-280 per ounce

- Legal premium: 10-30% (down from 60-80% in 2023)

Price Gap Analysis:

The framework shows legal markets struggle when prices exceed illicit by >20%. New York's price gap has narrowed dramatically:

- 2023: 60-80% legal premium (catastrophic)

- 2025: 10-30% legal premium (competitive)

- Projection 2026-2027: 5-15% legal premium (optimal with continued supply expansion)

This price compression drives the 894% sales growth and explains why legal market share improved from 10% to 17%.

What New York Gets Right: The Optimization Blueprint

Despite catastrophic early failures, New York has implemented several model policies that other states should study.

1. Potency Tax Repeal (Enacted June 1, 2024) MODEL TAX REFORM

Previous Structure (Jan 2023-May 2024):

- Flower (<35% THC): 10% of wholesale

- Concentrates (>35% THC): 25% of wholesale

- Infused products: 20% of wholesale

- Plus 9% state retail excise + 4% local excise

- Total burden: 35-42% (product-dependent)

Current Structure (June 2024-Present):

- Wholesale excise: 9%

- State retail excise: 9%

- Local retail excise: 4%

- Total burden: 22-24% (all products)

Impact:

| Metric | Pre-Reform (2023) | Post-Reform (2025) | Change |

|---|---|---|---|

| Sales | $151M | $1,500M+ | +894% |

| Legal share | 10% | 17% | +70% |

| Tax revenue | $40-50M | $150-200M | +300-400% |

| Avg item price | $36.72 | $31.71 | -13.7% |

Why Potency Tax Failed:

- Complexity: Different rates required lab shopping, created compliance nightmares

- Perverse incentives: Taxed harm reduction products (concentrates) MORE than flower

- Price uncompetitiveness: Made legal cannabis 60-80% more expensive than illicit

Why Wholesale Tax Succeeds:

- Simplicity: Single rate, easy compliance

- Neutrality: Doesn't penalize specific product types

- Revenue optimization: Lower rate on larger base = more total revenue

The Senator Cooney Strategy:

Senator Jeremy Cooney (D) championed potency tax repeal and continues optimization with S3294A (medical cannabis modernization). His consistent approach demonstrates systematic policy improvement rather than one-off reform.

New York learned from Illinois's mistake (maintained 35-40% burden → 50% legal share, revenue shortfalls) and Colorado's success (16% burden → 75-78% legal share, revenue exceeds projections).

Framework Verdict: New York's tax reform is model legislation. States like Illinois, Washington, and California should study this approach.

2. FY25 Budget Enforcement Provisions (Enacted April 2024) MODEL ENFORCEMENT

The Problem (2022-2024):

- OCM lacked emergency enforcement authority

- Court process took months to close illicit shops

- 2,000-3,000 unlicensed shops in NYC alone

- 5,000+ statewide unlicensed operations

- Ratio: 30-50 unlicensed per licensed dispensary

FY2025 Budget Solution:

The Office of Cannabis Management's law enforcement division received enhanced powers and funding:

Emergency Padlock Authority:

- OCM can immediately padlock illicit storefronts

- No prior notice required if "imminent threat to health/safety"

- One-year padlock duration

- Removing padlock = Class A misdemeanor

Enforcement Funding:

- $13.4M total allocation

- 37 OCM enforcement staff

- 43 Dept of Taxation staff (illicit cannabis focus)

- 15 Attorney General staff (litigation, investigations)

- Total: ~95 dedicated personnel

Landlord Liability:

- Property owners who knowingly lease to illicit operations face penalties

- Civil forfeiture provisions

- Creates financial disincentive to enable illegal operations

Results (May 2024 - November 2025):

- 488 padlock orders issued (NYC Sheriff data)

- $125M in illicit products seized

- 29,000+ pounds product confiscated

- 2,000+ inspections conducted

- 500+ enforcement actions statewide

Mayor Eric Adams celebrated the progress of Operation Padlock to Protect in May 2025, noting the dramatic reduction in illegal smoke shops across New York City. The Office of Cannabis Management's law enforcement division coordinates these efforts statewide, working with local municipalities, sheriffs, and the Attorney General's office to close unlicensed operations.

Market Impact:

| Period | Unlicensed Shops | Legal Sales | Legal Share |

|---|---|---|---|

| 2023 (pre-enforcement) | 5,000+ | $151M | 10% |

| 2025 (post-enforcement) | 500-800 est | $1,500M+ | 17% |

Framework Analysis:

Enforcement variable improved from E = 0.15 (minimal) to E = 0.55 (moderate-strong)

Weighted impact (0.6× weight): +0.24 raw contribution = +2 to +3 percentage points

Combined with tax reform (+price competitiveness): Total impact +6 to +8 percentage points

Observed result: Legal share improved +7 pp (10% → 17%) — matches framework prediction exactly ✓

Comparison to Other Markets:

| State | Agents | Budget | Per Capita | Approach | Legal Share |

|---|---|---|---|---|---|

| California | 15-20 | $5-8M | $0.13 | Weak | 50% |

| New York | 95 | $13.4M | $0.67 | Strong | 17% (growing) |

| New Mexico | 7 | $1.6M | $0.76 | Moderate | 70-75% |

| Michigan | 50+ | $10M+ | $1.00 | Strong | 85% |

New York is approaching Michigan-level enforcement intensity. If sustained, this creates foundation for 65-72% legal share by 2030.

The Supplier-Focused Model:

New York correctly targets illicit storefronts and cultivators, not consumers. This is the opposite of New Jersey S4154 (consumer criminalization), which the framework predicts would fail catastrophically.

Compare:

- New York approach: Padlock illegal shops, seize inventory, prosecute operators

- New Jersey S4154: Criminalize consumers who buy from unlicensed shops

- Framework prediction: NY approach adds +2-3 pp, NJ approach subtracts -8 to -12 pp

New York gets enforcement philosophy exactly right.

3. Social Equity Leadership (Execution Improving)

CAURD Program:

- 569 Conditional Adult-Use Retail Dispensary licenses issued

- Priority to justice-involved individuals

- First retail licenses in nation prioritizing impacted communities

SEE Licensing:

- 81% of retail licenses to Social & Economic Equity applicants

- 58% of microbusiness licenses to SEE

- Highest equity participation nationally

Challenges:

- Capital access remains inadequate ($50M fund for 5,000+ applicants)

- Many CAURD licensees stuck in conditional status

- Need: $250-500M expanded fund

But: New York's equity framework design remains nation-leading. Execution improving with dispensary openings accelerating.

4. Comprehensive Testing Standards

New York mandates rigorous testing through the Office of Cannabis Management and New York State Department of Health:

- Potency (THC, CBD content)

- Pesticide screening (comprehensive panels)

- Heavy metals, microbials, mycotoxins

- Solvent residue testing

The Department of Health's cannabis program ensures all products meet safety standards before reaching consumers. Quality advantage over illicit clear—when legal cannabis is accessible and affordable, testing becomes differentiator.

5. Medical Cannabis Modernization (S3294A Pending)

Senator Cooney's S3294A continues optimization:

- Eliminates physical registry cards (certification-only system)

- Extends certifications from 1 year → 2 years

- Allows out-of-state medical patient reciprocity

- Reduces caregiver age requirement (21 → 18)

Framework impact: Minor (+0.1 to +0.2 pp) but demonstrates continued commitment to reducing friction across all programs.

What Threatens New York: The A977 and A08581 Product Elimination Crisis

Assembly Bill A977 represents the worst cannabis legislation proposed in any U.S. state.

Sponsor: Assemblyman Phil Steck (D), K. Brown

Status: Prefiled January 8, 2025, in Committee (Economic Development)

Title: "Limits the potency of cannabis products"

Provisions:

- Cannabis flower: 15% THC maximum

- Concentrates/edibles: 25% THC maximum

- Applies to: ALL cannabis (adult-use AND medical)

- Penalties: Cultivation, processing, distribution, sale ALL prohibited

Why This Is Catastrophic:

Product Elimination:

Current legal cannabis products:

- Flower: 18-24% THC average (industry standard nationwide)

- Vape cartridges: 70-90% THC (standard concentrates)

- Live resin, diamonds: 80-95% THC

A977 would make ALL of this illegal:

- 15% flower cap = no compliant inventory exists

- 25% concentrate cap = no cartridges, no concentrates

- 90-95% of current legal products eliminated

Framework Prediction:

| Variable | Current (2025) | With A977 |

|---|---|---|

| Product Adequacy (S) | 0.65 (improving) | 0.02 (catastrophic) |

| Legal Market Share | 17% | 0-2% |

| Legal Sales | $1.5B | $30-80M |

| Tax Revenue | $150-200M | $5-15M |

| Illicit Market | $7-8B | $9-10B (100%) |

Comparison to Other Failures:

| Disaster | Impact | Legal Share |

|---|---|---|

| California fragmentation | 61% local bans | 50% |

| Illinois high taxes | 35-40% burden | 50% |

| A977 product elimination | 95% inventory illegal | <2% |

A977 is WORSE than California and Illinois combined.

The Steck Rationale (Flawed):

Claim: "High-potency cannabis causes ER visits"

Reality:

- ER visits spike when untested illicit products contaminated with synthetics flood market

- Solution: Enforcement against illicit, NOT neutering legal products

- Colorado: ER visits DECLINED post-legalization once testing standards implemented

Analogy:

"Limiting cannabis to 15% THC is like limiting beer to 3.2% alcohol while wine and spirits remain federally illegal. Consumers will simply buy wine from New Jersey."

Framework Analysis:

If A977 passes:

New York's legal market would return to 0-2% share—effectively repealing legalization by making compliant products unavailable.

Similar disaster: Washington DC's "gifting" loophole (can't sell but can "gift" with purchase) = 95% illicit market

The Economic Destruction:

- Lost tax revenue: $145-195M annually

- Lost jobs: 8,000-12,000 (dispensaries close, cultivators shut down)

- Illicit market returns to: $9-10B (100% of demand)

CBDT Verdict: A977 is consumer criminalization through product elimination. If passed, create immediate full analysis showing how New York repealed legalization through product prohibition.

Probability of Passage: 10-15% (extreme proposal, likely dies in committee, but Steck is persistent)

A08581: The Edibles and Flavored Product Elimination Act ⚠️ EQUALLY CATASTROPHIC

Assembly Bill A08581 represents a different but equally devastating attack on New York's legal cannabis market.

Sponsor: Unknown (Democrat), single sponsor

Status: Introduced May 21, 2025, in Committee (Economic Development)

Title: "Prohibits edible cannabis products and flavored vape cartridges"

Provisions:

A08581 would PROHIBIT:

- ALL edible cannabis products (gummies, chocolates, baked goods, capsules, tinctures)

- ALL flavored vape cartridges (fruit, mint, dessert flavors—essentially all vapes)

- ALL other flavored cannabis products

- Food-related names in labeling, packaging, and advertising

Why This Is Catastrophic:

Current New York Product Mix:

- Edibles: 25-30% of legal sales

- Beverages: 2-3% of sales (fastest-growing category, +85% YoY in 2025)

- Flavored vapes: 35-40% of sales

- Unflavored flower/products: 30-35% of sales

A08581 would eliminate:

- 60-70% of current legal product categories

- Nearly ALL vape products (unflavored vapes <5% of market—consumers won't buy them)

- ALL edibles (medical patients' preferred consumption method)

- ALL beverages (New York's fastest-growing segment: $2.3M October 2025, +85% YoY)

- ALL tinctures and capsules (medical patient staples)

Framework Prediction:

| Variable | Current (2025) | With A08581 |

|---|---|---|

| Product Adequacy (S) | 0.65 (improving) | 0.20 (catastrophic) |

| Legal Market Share | 17% | 3-5% |

| Legal Sales | $1.5B | $180-300M |

| Tax Revenue | $150-200M | $20-35M |

| Product categories | 5-6 | 1-2 |

Why A08581 May Be WORSE Than A977:

Consumer Impact:

- Medical patients: Rely on edibles/tinctures for smoke-free consumption

- Health-conscious users: Prefer edibles over smoking (respiratory concerns)

- Discreet users: Edibles don't create odor/detection issues

- Harm reduction: Vapes eliminate combustion risks

A08581 forces ALL consumers to:

- Smoke flower (respiratory harm)

- Use unflavored vapes (consumers reject these)

- Buy from illicit market (where edibles/flavored vapes remain available)

Market Dynamics:

Illicit market WILL continue selling:

- Edibles: Gummies, chocolates, baked goods (already 30% of illicit sales)

- Flavored vapes: Every flavor consumers want

- Beverages: Unregulated, untested products

Result: 95-97% of consumers choose illicit for product availability

The Economic Destruction:

- Lost tax revenue: $115-165M annually

- Lost jobs: 7,000-10,000 (edibles manufacturers, beverage producers, dispensaries close)

- Illicit market: Returns to $8-9B (90-95% of demand)

Comparison to A977:

| Bill | Products Eliminated | Legal Share Impact | Worse For |

|---|---|---|---|

| A977 | 90-95% (potency limits) | 17% → 0-2% | ALL users |

| A08581 | 60-70% (category bans) | 17% → 3-5% | Medical patients, non-smokers |

Both are product elimination disguised as regulation.

CBDT Verdict: A08581 is category prohibition through consumption method restriction. Medical patients, elderly users, and health-conscious consumers disproportionately harmed.

Probability of Passage: 15-20% (single sponsor, extreme proposal, but "protecting children" rhetoric around edibles is politically potent)

Full CBDT analysis required immediately - A08581 may have HIGHER passage probability than A977 due to edibles/marketing restrictions framed as "child safety."

Federal Barriers: The 280E and SAFE Banking Handicaps

New York cannot achieve optimization without federal reform—even with perfect state policy.

The 280E Problem

Internal Revenue Code Section 280E prohibits cannabis businesses from deducting ordinary business expenses. For complete 280E mechanics and history, see: IRC Section 280E: The Cannabis Tax Penalty Destroying Legal Markets

New York Impact:

NYC dispensary, $1M annual revenue:

Without 280E (normal business):

- Revenue: $1,000,000

- COGS: $300,000

- Operating expenses: $550,000

- Profit: $150,000

- Federal tax (21%): $31,500

- Net profit: $118,500

With 280E (cannabis business):

- Revenue: $1,000,000

- COGS (deductible): $300,000

- Operating expenses (NON-deductible): $550,000

- Taxable income: $700,000 (not $150,000)

- Federal tax: $147,000 (not $31,500)

- Net profit: $3,000 (97% reduction)

280E penalty: $115,500 in excess federal taxes, destroying profitability.

Market Impact:

- Forces retail prices 12-18% higher than without 280E

- Makes profitability impossible for most operators

- Legal market share reduced by 8-12 percentage points

The Solution: Schedule III rescheduling (currently DEA consideration) eliminates 280E. For rescheduling progress and implications, see: DEA Schedule III Rescheduling: Timeline and Market Impact

New York businesses would save $120-180M annually in excess federal taxes, enabling 10-15% price reductions and profitability.

The SAFE Banking Problem

Without SAFE Banking Act passage, New York cannabis businesses remain largely unbanked. For complete banking analysis and alternatives, see: SAFE Banking Act: Why Cannabis Needs Financial Access

Current Reality:

- Fewer than 20 NY banks serve cannabis (anonymous, high fees)

- Services at 3-5× normal fees

- Constant closure risk, waitlists for new accounts

Impact:

Crime and Safety:

- Cash-intensive businesses = robbery targets

- Armored transport: $600-2,500 per pickup

- Security costs: $60-180K annually per location

- Insurance premiums: 40-60% higher

Consumer Friction:

- Cash-only reduces transaction frequency 15-20%

- Card payment dispensaries see 35-50% higher daily revenue

Capital Access:

- SEE licensees cannot access commercial loans

- Cannot build credit, cannot scale

Framework Impact: Banking absence reduces legal market share by 8-12 percentage points through payment friction and capital constraints.

Solution: SAFE Banking Act passage enables normal banking, card payments, capital access.

Price Trends and Market Dynamics: Supply Expansion Working

New York's price decline demonstrates healthy market evolution.

Wholesale Market

Industry observations:

- Wholesale prices declining as cultivation expands

- More competitive pricing emerging

- Supply constraints easing

Compare to mature markets:

- Michigan: $225/lb wholesale

- Oregon: $180-220/lb wholesale

- Colorado: $400-600/lb wholesale

- New York trajectory: Approaching $800-1,200/lb (equilibrium)

Retail Price Evolution

| Period | Average Item | Flower (oz) | YoY Change |

|---|---|---|---|

| Oct 2024 | $36.72 | $260-320 | Baseline |

| Oct 2025 | $31.71 | $220-280 | -13.7% |

| Proj 2026 | $26-29 | $180-240 | -15-20% |

Framework Principle: Supply expansion drives price competition—this is GOOD for legal market competitiveness.

Industry perspective: "Oversupply" is problem (margin compression)

Framework perspective: Price competition improves legal market capture

The Critical Difference:

New York is letting natural price decline occur through supply expansion rather than offsetting it with tax increases (Illinois mistake).

- Illinois approach: Maintain 35-40% tax burden → prices stay high → legal share stagnates at 50%

- New York approach: Reduce tax burden to 22% → prices decline naturally → legal share grows to 17% and improving

This is exactly correct and why New York is optimizing while Illinois stagnates.

Geographic and Demographic Dynamics

Border Competition

Neighboring States:

- Connecticut: 70-75% legal share, competitive market (see: Connecticut HB7181 enforcement analysis)

- Massachusetts: 82% legal share, mature optimization

- New Jersey: 55-60% legal share, supply-constrained (see: New Jersey S4154 consumer criminalization threat)

- Pennsylvania: Medical only (adult-use opportunity)

- Vermont: Small market, home grow focus

Cross-Border Flow:

From New York:

- NYC → New Jersey: Some border shopping (Hoboken, Jersey City)

- Upstate → Massachusetts: Limited (distance)

To New York:

- Pennsylvania medical patients (reciprocity)

- Connecticut residents (convenience, more options)

Net effect: New York's size and NYC concentration create market gravity—more likely to capture regional demand than lose to neighbors.

NYC Concentration

Market characteristics:

- NYC metro: 20M residents (60% of state population)

- 260 dispensaries in NYC (50% of state total)

- Density: 1.3 per 100,000 (still below optimal but improving rapidly)

New York City's Department of Small Business Services supports cannabis businesses through its Cannabis NYC initiative, providing resources for licensing, compliance, and business development in the five boroughs.

Urban vs. Rural:

- Urban (NYC, Buffalo, Rochester, Syracuse, Albany): Well-served

- Suburban (Long Island, Westchester, Hudson Valley): Improving

- Rural upstate: Geographic gaps remain

Delivery authorization helps rural access but adoption limited by banking restrictions (cash-only delivery challenging).

Additional Legislation: The Broader Policy Landscape

Note: A977 (THC potency caps) and A08581 (edibles/flavored products ban) are analyzed in detail in the "What Threatens New York" section above due to their catastrophic market impact potential.

A1007 - Consumption Restrictions (Pending)

Sponsor: Assemblyman Phil Steck (same as A977)

Status: Prefiled January 8, 2025, in Committee (Codes)

Provisions:

- Prohibits smoking/vaping cannabis within 30 feet of ANY child

- Includes "through walls" (cannot use in apartment if child lives next door/upstairs)

- Penalty: $25 fine OR 20 hours community service (first offense), Class B misdemeanor (subsequent)

Framework Impact: Moderate negative (-3 to -4 pp from convenience destruction)

Why This Matters: NYC residents mostly live in multi-family buildings. 30-foot restriction through walls = cannot consume in 90% of NYC apartments.

Probability: 20-25% (Steck bills generally unpopular, but "protecting children" rhetoric is powerful)

S08332 - Small Cannabis Farmer Relief Act (Pending)

Sponsor: Sen. Michelle Hinchey (D)

Status: Introduced June 6, 2025

Provisions:

- Allows distressed farmers to temporarily double canopy size

- Sunsets December 31, 2028

- Addresses projected 2026-2027 supply shortage

Framework Impact: Minor positive (+0.2 to +0.4 pp from preventing shortage-driven price spikes)

Why This Matters: OCM projects demand will exceed supply 2026-2027. S8375A prevents shortage that would spike prices and drive consumers back to illicit market.

Probability: 60-70% (addresses real problem, temporary solution, bipartisan support)

S1137 - Social Equity Investment Fund Increase (Pending)

Sponsor: Sen. James Sanders Jr.

Provisions:

- Increases fund cap from $50M → $300M (6× increase)

- State-backed financing for SEE applicants

Framework Impact: Neutral (equity important, but doesn't affect consumer variables directly)

Probability: 40-50% (high cost, budget constraints, but strong advocacy)

Framework Assessment: New York's Transformation

Current Performance: 15-20% Legal Market Share

Transaction share: 20-25% (percentage of users choosing legal for at least some purchases)

Volume share: 15-20% (accounting for heavy user behavior)

This represents 70% improvement from 2023 (10% share) but still bottom quartile nationally.

Why growth is accelerating:

- Tax reform (38% → 22%) improving price competitiveness

- Enforcement scaling (95 agents, 488 padlocks) reducing illicit competition

- Retail density expansion (522 dispensaries, growing) improving access

- Supply expansion driving price declines

The Five Levers

Price Competitiveness (4× weight): IMPROVING

- Current: Legal 10-30% above illicit (competitive)

- 2023: Legal 60-80% above illicit (catastrophic)

- Trend: Converging toward parity as supply expands

- Impact: Primary driver of 894% sales growth

Access Density (2.8× combined weight): IMPROVING RAPIDLY

- Current: 2.6 per 100,000 residents

- Optimal: 8-10 per 100,000

- Gap: Still 67-74% below optimal

- But: 100% increase in 12 months (260 → 522 dispensaries)

- Trajectory: Approaching optimal by 2027-2028

Enforcement (0.6× weight): STRONG

- 95 dedicated agents = $0.67 per capita

- 488 padlock orders, $125M seized

- Enforcement intensity: 35-45% (up from <5% in 2023)

- Compare: Michigan 85-90%, California 3%

Safety/Quality (1.2× weight): STRONG

- Rigorous testing standards

- Comprehensive contaminant panels

- Professional retail operations

- Clear quality advantage over illicit

Convenience (1× weight): WEAK

- Mostly cash-only (SAFE Banking absent)

- Some debit options emerging

- Payment friction reduces transactions 15-20%

Fragmentation Penalty: LOW

- Most municipalities permit retail

- NYC concentration reduces geographic gaps

- Delivery authorized (limited adoption due to banking)

CBDT Score Projection

Current Trajectory (Continue Optimization):

IF:

- Retail density continues expanding (target 1,600+ by 2028)

- Enforcement sustained ($30-50M annually)

- Federal reform occurs (Schedule III + SAFE Banking 2026-2027)

- A977 DOES NOT PASS

THEN:

- 2026: 22-27% legal share

- 2027: 35-42% legal share (post-federal reform)

- 2028: 48-55% legal share

- 2030: 65-72% legal share

Comparable performance: Illinois-to-Colorado range (mid-tier to good)

Alternative Trajectory (Catastrophic Failure):

IF A977 passes:

- 2026: 0-2% legal share (product elimination)

- Effective prohibition restored

- All optimization progress destroyed

Comparison to Other Markets: Learning From Success and Failure

The Michigan Model: What Optimization Looks Like

Michigan (population 10M) achieved 85% legal market share in 5 years through:

Key Policies:

- Rapid licensing: 843 dispensaries (8.4 per 100K) vs NY's 2.6 per 100K

- Competitive pricing: $83/oz average vs NY's $200-280/oz

- Home cultivation: 12 plants allowed (NY prohibits adult-use home grow)

- Strong enforcement: 50+ agents, $10M budget, consistent interdiction

- Moderate taxation: 16% total burden vs NY's 22%

Results:

- Legal sales: $3.2B annually (for 10M residents)

- Legal share: 85%

- Tax revenue: $290M annually

New York comparison:

- Population: 20M (2× Michigan)

- Current sales: $1.5B (47% of Michigan per-capita)

- Legal share: 17% (20% of Michigan performance)

- Gap: NY performing at 20-25% of Michigan's optimization

What NY must do to reach Michigan level:

- Continue retail expansion to 1,600-2,000 dispensaries (8-10 per 100K)

- Maintain moderate taxation (resist pressure to increase rates)

- Sustain enforcement ($30-50M annually)

- Authorize adult-use home cultivation (18+ months overdue)

- Achieve federal reform (280E elimination, SAFE Banking)

Timeline: With aggressive action, NY could reach 75-80% share by 2028-2029 (Michigan trajectory)

The Illinois Cautionary Tale: Tax Policy Failure

Illinois (population 12.8M) stagnated at 50-55% legal share through policy mistakes New York is avoiding:

Illinois Mistakes:

- High taxation: 35-40% total burden (vs NY's 22%)

- Scheduled tax increases: Automatic escalation built into law

- No home cultivation: Adult-use home grow prohibited

- Moderate enforcement: Not weak like California, but not strong like Michigan

Results:

- Legal sales: $1.85B annually (26% below projections)

- Legal share: 50-55% (stagnant)

- Tax revenue: Underperforming by $150-200M annually vs projections

The Illinois Mistake New York Avoided:

Illinois assumed high taxes on captive market = revenue maximization. WRONG.

Revenue equation: Revenue = Base × Rate

Illinois chose: Small base (50% share) × High rate (35-40%) = $50-84M

New York choosing: Large base (17% growing) × Moderate rate (22%) = $150-200M

New York generates 2-3× MORE revenue than Illinois despite lower tax rate because New York optimizes the BASE (market share) while Illinois optimizes the RATE (per-unit taxation).

This validates framework prediction: Tax optimization requires base maximization.

See: Connecticut HB7181 enforcement analysis for how Connecticut is learning from both Illinois's failures and Michigan's success.

The California Disaster: What Not To Do

California (population 39.5M) captures only 50% legal market share through compounding policy failures:

California's Mistakes:

- Massive fragmentation: 61% of jurisdictions ban retail

- High taxation: 30%+ effective burden (state + local + cultivation taxes)

- Minimal enforcement: 3% interdiction rate on 10,000+ illegal grows

- Complex regulations: Overlapping state/local requirements

Results:

- Legal sales: $5.2B annually

- Legal share: 50% (should be 70-80% given size/maturity)

- Illicit market: $5-6B (larger than legal in absolute terms)

- Tax revenue: $1.1B (30% below projections)

New York Avoided California's Mistakes:

| California Failure | New York Success |

|---|---|

| 61% local bans | Minimal fragmentation |

| 30%+ tax burden | 22% tax burden |

| 3% enforcement | 35-45% enforcement |

| Potency + cultivation + local taxes | Simple wholesale tax |

Why New York is optimizing while California stagnates: New York learned from California's failures and implemented opposite policies.

The Connecticut Success: Enforcement + Tax Strategy

Connecticut (population 3.6M) projected to reach 70-75% legal share through smart policy:

Connecticut's Success Factors:

- Tax reduction: Simplified structure, competitive rates

- HB7181 enforcement: Municipal revenue incentives create enforcement ROI

- Home cultivation: 6 plants allowed from day one

- Rapid licensing: Good per-capita dispensary density

See: Connecticut HB7181 CBDT Analysis for complete enforcement strategy breakdown.

Lesson for New York: Connecticut demonstrates enforcement requires incentive alignment. New York's FY25 budget approach (dedicated enforcement funding, emergency powers) mirrors Connecticut's successful model.

The New Jersey Warning: Consumer Criminalization Risk

New Jersey (population 9.3M) faces 55-60% legal share and S4154 consumer criminalization threat:

New Jersey's Challenge:

- S4154: Would criminalize consumers who "knowingly" purchase from unlicensed retailers

- Supply constraints: Insufficient dispensaries, high prices

- Murphy's SEEF tax: 500% increase proposal threatens price competitiveness

See: New Jersey Cannabis Market Analysis and New Jersey S4154 Analysis for complete breakdown.

New York Avoided This Mistake: NY focuses enforcement on suppliers (padlocking illicit shops) not consumers (criminalizing purchases). This is exactly correct per framework.

Consumer criminalization (NJ S4154 approach): -8 to -12 pp legal share

Supplier-focused enforcement (NY FY25 approach): +2 to +3 pp legal share

Policy Recommendations: The Path to 65-72% Legal Share

New York stands at critical juncture. Continue optimization → Michigan-level success. Pass A977 or regress → catastrophic failure.

Priority #1: Defeat A977 AND A08581 (CRITICAL)

Immediate Action: Mobilize opposition to BOTH product elimination bills

Framework Evidence:

A977 (THC potency caps):

- Would eliminate 90-95% of legal products

- Legal market share: 17% → 0-2% (collapse)

- Tax revenue: $150-200M → $5-15M annually

- Jobs destroyed: 8,000-12,000

A08581 (edibles/flavored products ban):

- Would eliminate 60-70% of product categories

- Legal market share: 17% → 3-5% (catastrophic)

- Tax revenue: $150-200M → $20-35M annually

- Jobs destroyed: 7,000-10,000

- Medical patients disproportionately harmed

Political Strategy:

- Industry coalition: Licensed operators, edibles manufacturers, medical dispensaries face extinction

- Consumer advocacy: Patient groups (edibles critical for medical), adult-use consumers, harm reduction advocates

- Revenue argument: Show legislators the $115-195M annual loss

- Law enforcement: Illicit market returns to 90-100% if either bill passes

- Medical community: Doctors, nurses oppose eliminating smoke-free consumption methods

- A08581 specific: "Child safety" rhetoric requires strong counter-messaging about child-resistant packaging already required

If either bill advances: Create immediate full CBDT analysis showing economic devastation, distribute to every legislator.

Priority: HIGHEST

Priority #2: Federal Reform Advocacy

Schedule III Rescheduling:

- Current impact: 280E costs NY cannabis $120-180M annually in excess federal taxes

- Post-Schedule III: Businesses save $120-180M, enabling 10-15% price reductions

- Legal market impact: +8-12 percentage points

SAFE Banking Act:

- Current impact: Banking absence costs $80-120M annually (security, elevated costs)

- Post-SAFE Banking: Card payment access, capital availability, 20-30% transaction increase

- Legal market impact: +8-12 percentage points

Combined federal reform: +16-24 percentage points legal share improvement

New York's Congressional Delegation:

- Senators Schumer, Gillibrand

- House members across 26 districts

- Frame as: Economic development, small business support, social equity (equity requires profitability)

Priority #3: Retail Density Emergency Expansion

Current: 522 dispensaries (2.6 per 100K)

Target: 1,600-2,000 dispensaries (8-10 per 100K)

Gap: 1,080-1,480 additional dispensaries needed

Immediate Actions:

State Loan Fund ($500M):

- Low-interest loans (2-4%) for dispensary buildouts

- Priority for SEE applicants

- Loan forgiveness tied to opening timelines

Expedited Conversions:

- Clear conditional license backlog

- 30-60 day turnaround for compliant applications

- Eliminate unnecessary red tape

Real Estate Support:

- State-backed lease guarantees for SEE applicants

- Negotiate rent reductions for tax incentives

- Address municipal zoning barriers

Timeline:

- 2026: 750 operational (from 522)

- 2027: 1,100 operational

- 2028: 1,500 operational (optimal density achieved)

Investment: $500M loan fund + $50M technical assistance

ROI: 1,000 new dispensaries = $400-600M additional annual sales = $88-132M tax revenue increase = 18-26× ROI over 5 years

Priority #4: Adult-Use Home Cultivation Authorization

MRTA requirement: 18 months after first dispensary opens

Deadline: June 2024

Current status: 18+ months overdue, still not implemented

Immediate Action: Finalize regulations (model after medical program):

- 6 plants per person (3 mature + 3 immature)

- 12 plants per household maximum

- Effective Q1 2026

Framework Impact: +6-10 percentage points legal share

Why This Matters:

- Provides affordable option for price-sensitive consumers

- 85-90% still prefer dispensary convenience (minimal retail cannibalization)

- Demonstrates commitment to MRTA implementation

- Captures $300-500M in cultivation activity within legal framework

Compare to Michigan (12 plants allowed): 85% legal share

Compare to New Jersey (prohibited): 55-60% legal share

Home cultivation complements retail—does not compete with it. See: The Home Grow Myth: Why Your Closet Costs More Than Dispensary Weed

Priority #5: Enforcement Sustainability

FY25 success must continue:

Annual Allocation:

- $30-50M ongoing enforcement budget

- 80-100 dedicated enforcement staff (expand from 95)

- Technology investment (tracking, intelligence, coordination)

Target Metrics:

- 90-95% unlicensed elimination by 2027

- 800-1,200 monthly inspections

- 48-72 hour padlock execution

- Landlord accountability enforcement

Landlord Enforcement:

- Vigorous prosecution of property owners

- $10,000+ fines per violation

- Eviction proceedings for non-compliance

- Criminal referrals for repeat offenders

Compare:

- Michigan: $1.00 per capita enforcement

- New York current: $0.67 per capita

- New York target: $1.00-1.50 per capita

Budget: $20-30M annually (NY population 20M × $1-1.50)

Priority #6: Tax Stability and Optimization

Current structure (22% total) is CORRECT.

Maintain:

- 9% wholesale excise

- 9% state retail excise

- 4% local retail excise

- 22% total burden

Resist Pressure:

- Budget hawks will want to increase rates (resist)

- Revenue optimization comes from VOLUME (market share), not RATES

Consider Temporary Reduction:

- Reduce to 18-20% total during market stabilization (2026-2027)

- Offset through volume increase

- Return to 22% once market stabilizes (2028+)

The Illinois Lesson: High rates on small base = less revenue than moderate rates on large base

The New Mexico Example: See New Mexico SB 89 CBDT Analysis for detailed revenue paradox breakdown showing how 13% generates more revenue than 18%.

Priority #7: SEE Capital Access Expansion

Current: $50M fund, 5,000+ applicants

Need: $250-500M expanded fund

Structure:

- Grants (not loans) for buildouts

- No repayment if operational 5+ years

- Priority: CAURD licensees stuck in conditional status

Technical Assistance:

- Business planning, real estate sourcing

- Construction management, operational training

- One-on-one support for each licensee

MSO Partnership Standards:

- Require SEE licensees maintain majority control

- Prevent predatory partnerships

- Enforce disclosure requirements

Investment: $250-500M over 3 years

Impact: Convert 300-500 stuck CAURD licenses to operational dispensaries = $150-250M annual sales = $33-55M tax revenue = 6-11× ROI

Timeline and Economic Projections

Phase 1 (2026): Federal Reform + Density Push

Assumes: DEA completes Schedule III (likely 2026), retail expansion accelerates

Key Events:

- Schedule III: 280E elimination enables profitability

- Prices decline 10-15% from tax savings

- Retail density: 522 → 750-850 dispensaries

- Adult-use home cultivation authorized (finally)

Predicted Outcomes:

- Legal market: $2.2-2.8B annually (+47-87% growth)

- Legal share: 22-27% (+5-10 points)

- Tax revenue: $290-370M annually (+45-85%)

- Dispensaries: 750-850 operational

Phase 2 (2027): SAFE Banking + Retail Optimization

Assumes: SAFE Banking passes, retail density approaches optimal

Key Events:

- Card payment adoption increases transactions 20-30%

- Cashless delivery becomes viable

- SEE licensees access commercial lending

- Retail density: 850 → 1,200-1,400 dispensaries

Predicted Outcomes:

- Legal market: $3.5-4.5B annually (+59-61% growth from Phase 1)

- Legal share: 35-42% (+13-15 points)

- Tax revenue: $460-590M annually (+59-59%)

- Jobs: 20,000-28,000 total

Phase 3 (2028-2029): Optimized Steady State

Characteristics:

- Federal support (280E eliminated, SAFE Banking active)

- Optimal retail density (1,500-1,800 dispensaries, 7.5-9 per 100K)

- Competitive pricing ($150-200/oz flower)

- Strong enforcement sustained

Predicted Outcomes:

- Legal market: $5-7B annually (+43-56% from Phase 2)

- Legal share: 52-62%

- Tax revenue: $660-920M annually

- Jobs: 35,000-50,000 total

Phase 4 (2030+): Mature Market

Sustained Performance:

- Legal market: $6-8.5B annually (steady with inflation, population growth)

- Legal share: 65-72%

- Tax revenue: $790-1,120M annually

- Jobs: 45,000-65,000 total

Remaining Illicit Market (28-35%):

- Price-sensitive heavy users (~10-12%)

- Home cultivation networks (gifting) (~8-10%)

- Cultural illicit preference (~6-8%)

- Geographic gaps (very rural) (~4-5%)

This represents New York's optimization ceiling under federal reform + optimal state policy.

Comparable Performance:

- Michigan: 85% (better, due to earlier start, lower prices)

- Colorado: 75-78% (comparable)

- Massachusetts: 82% (comparable)

- Illinois: 55-60% (worse, high taxes)

What Failure Looks Like: The Catastrophic Trajectory

IF: A977 passes OR federal reform fails OR enforcement wanes OR retail expansion stalls

THEN: New York stagnates or regresses

Failed Scenario: A977 Passes

Product Elimination:

- 95% of legal inventory becomes illegal

- Legal market share: 17% → 0-2%

- Effective prohibition restored

Economic Impact:

- Legal sales: $1.5B → $30-80M (collapse)

- Tax revenue: $150-200M → $5-15M

- Jobs: 12,000 → 800-1,500 (destroyed)

- Illicit market: Returns to $9-10B (100% of demand)

This is WORSE than never legalizing because infrastructure was built then destroyed.

Failed Scenario: Enforcement Wanes

IF: Political pressure reduces enforcement budget OR padlock authority weakened

THEN:

- Unlicensed shops return (500-800 → 2,000-3,000)

- Legal market share: 17% → 12-15% (regression)

- Legal sales: $1.5B → $1.8-2.2B (growth stalls)

Failed Scenario: Federal Reform Delayed

IF: Schedule III delayed to 2028+ OR SAFE Banking never passes

THEN:

- 280E continues forcing prices high

- Banking restrictions limit growth

- Legal share: 17% → 25-35% by 2030 (slow improvement, not optimization)

- Tax revenue: Plateaus at $350-450M (vs $790-1,120M optimized)

Cumulative Lost Opportunity (2026-2030):

- Lost tax revenue: $1.5-2.5B over 5 years

- Lost jobs: 25,000-40,000 vs optimized

- Persistent illicit market: $12-18B over 5 years

Conclusion: New York Must Choose Competence Over Catastrophe

New York has accomplished in 18 months what California failed to do in 8 years: implement fundamental tax and enforcement reforms that actually work.

The Evidence:

| Metric | 2023 (Disaster) | 2025 (Optimization) | Change |

|---|---|---|---|

| Sales | $151M | $1,500M+ | +894% |

| Legal share | 10% | 17% | +70% |

| Tax revenue | $40-50M | $150-200M | +300-400% |

| Dispensaries | 32 | 522 | +1,531% |

| Avg item price | $36.72 | $31.71 | -13.7% |

| Illicit seized | $15-25M | $125M+ | +500-733% |

New York demonstrates that regulatory competence matters more than ideology.

The Reforms That Worked:

- Potency tax repeal: 38% → 22% burden = +6-8 pp legal share

- FY25 enforcement: 95 agents, 488 padlocks = +2-3 pp legal share

- Retail expansion: 32 → 522 dispensaries = +3-4 pp legal share

- Combined effect: 10% → 17% legal share = validates framework exactly

The Path Forward:

With federal reform (Schedule III + SAFE Banking) and continued state optimization:

- 2026: 22-27% legal share

- 2027: 35-42% legal share

- 2028: 52-62% legal share

- 2030: 65-72% legal share

This puts New York in Michigan/Colorado/Massachusetts tier—the nation's most successful legal cannabis markets.

The Catastrophic Risk:

Assembly Bill A977 and Assembly Bill A08581 would destroy all progress:

A977: THC caps of 15% (flower) and 25% (concentrates) eliminate 90-95% of legal inventory

A08581: Edibles and flavored products ban eliminates 60-70% of product categories

If either bill passes:

- Legal market share: 17% → 0-5%

- Tax revenue: $150-200M → $5-35M

- Jobs destroyed: 7,000-12,000

- Illicit market: Returns to 90-100%

The Framework Equation:

Success = Federal reform (280E elimination + SAFE Banking) + State optimization (retail density + enforcement + tax stability) + Defeat A977 AND A08581

Failure = Any one of: A977 or A08581 passes, federal reform delayed, enforcement cut, retail expansion stalls

The Economic Stakes:

Optimized trajectory: $790-1,120M annual tax revenue by 2030, 45,000-65,000 jobs, 65-72% legal share

Failed trajectory: $150-250M annual tax revenue, 15,000-20,000 jobs, 30-40% legal share (stagnation)

Difference: $640-870M annually in tax revenue, 30,000-45,000 jobs, public safety outcomes

The Political Choice:

New York pioneered equity-focused legalization. Now New York has pioneered evidence-based optimization.

Other states watch: Can progressive state fix regulatory dysfunction through policy competence?

The answer determines whether cannabis legalization succeeds or fails nationally.

New York has shown it can learn from mistakes (potency tax repeal), implement best practices (supplier-focused enforcement), and achieve results (894% growth).

Now New York must sustain that competence, defeat A977 and A08581, and complete the journey from catastrophe to optimization.

The Empire State can build the nation's leading urban cannabis market.

The framework shows the path.

The question is whether policymakers will maintain the courage to follow it.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Missouri | Mississippi | North Carolina | Nebraska

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0