Ohio Cannabis Market Analysis: Why Voter-Approved Legalization Faces Legislative Assault—And How Federal Reform Could Save It

Is weed legal in Ohio? Yes. Will it stay legal the way voters intended? That's what Senate Bill 56 threatens to change.

The Silent Majority 420 | November 2025

The Ohio Paradox

Is weed legal in Ohio? Yes. Adult-use cannabis became legal in December 2023 after 57% of voters approved Issue 2, and sales began in August 2024 from existing medical dispensaries. Ohioans can now legally possess up to 2.5 ounces of cannabis, grow up to 12 plants per household, and purchase from approximately 165 licensed dispensaries.

Is recreational marijuana legal in Ohio the way voters approved it? That's a different question—and the Ohio General Assembly is working hard to make the answer "no."

Senate Bill 56, which passed the Senate 23-9 in February 2025 and the House 87-8 in October 2025, would fundamentally alter voter-approved legalization by:

- Recriminalizing out-of-state cannabis (making it illegal to bring legal cannabis from Michigan or Pennsylvania if it legalizes)

- Reducing home grow from 12 to 6 plants per household (cutting cultivation rights in half)

- Lowering THC limits from 90% to 70% for extracts

- Eliminating the Cannabis Social Equity and Jobs Program (defunding equity provisions)

- Capping dispensaries at 400 statewide (creating artificial scarcity)

- Repealing non-discrimination protections for adult-use consumers

The Senate unanimously rejected (0-32) the House version in late October 2025, sending it to conference committee where it now sits—a legislative tug-of-war over whether Ohio's voters or politicians control cannabis policy.

This matters because Ohio marijuana laws directly determine whether the state achieves 75-80% legal market share (capturing most of the $3.8-4.2 billion total cannabis market) or collapses to 45-55% (California-style policy failure despite voter approval).

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, predicts Ohio will achieve approximately 55-60% legal market share under current policy. With comprehensive optimization and federal reform, 75-80% is achievable. But if SB 56 becomes law in its most restrictive form and federal barriers persist, Ohio could fall to 45-55%—turning voter-approved legalization into policy failure.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Status: Is Weed Legal in Ohio? What You Need to Know

Adult-Use (Recreational) Cannabis: LEGAL

Is recreational marijuana legal in Ohio? Yes, as of December 7, 2023.

Ohio Issue 2 passed on November 7, 2023 with 57% voter approval, legalizing:

- Possession: Up to 2.5 ounces of cannabis flower, up to 15 grams of cannabis extract

- Home cultivation: Up to 6 plants per person, 12 per household maximum

- Purchase: From licensed dispensaries (sales began August 6, 2024)

- Age: 21 and older

- Tax: 10% excise tax on adult-use purchases

Licensed dispensaries: Approximately 165 dual-use dispensaries as of November 2025

Ohio home grow rules (as of current law, before SB 56 changes):

- Maximum 12 plants per household (regardless of number of adults)

- Must be in secured, enclosed area not visible from public

- Cannot be accessible to individuals under 21

- Located at primary residence only

Where can you legally use cannabis in Ohio?

- Private residences ONLY

- NOT in vehicles, public spaces, parks, or on government property

- Landlords can prohibit use in rental properties

Medical Cannabis: LEGAL (Since 2017)

Ohio medical marijuana card requirements:

- Qualifying medical condition (21+ conditions including chronic pain, PTSD, cancer, epilepsy)

- Ohio resident

- Physician certification from state-certified doctor

- $50 registration fee

- Valid for 1-2 years depending on physician recommendation

Medical program stats (2024):

- 160,000+ registered patients

- 8-10% of qualifying conditions are adult-use consumers who prefer medical benefits (no excise tax, higher purchase limits)

Ohio Marijuana Penalties (What's Still Illegal)

Despite legalization, these remain criminal offenses:

| Offense | Penalty | Criminal Record? |

|---|---|---|

| Possession over 2.5 oz (under 100g) | Minor misdemeanor, $150 fine, license suspension 6mo-5yr | YES* |

| Possession 100-200g | Misdemeanor, up to 30 days jail, $250 fine | YES |

| Possession over 200g | Felony charges, imprisonment | YES |

| Public consumption | Minor misdemeanor | YES* |

| DUI/OVI (2+ ng/mL THC in blood) | Misdemeanor to felony, jail, fines $375-$10,500, license suspension | YES |

| Sale without license | Trafficking felony, 6-18 months jail, $5,000 fine | YES |

| Growing over 12 plants per household | Trafficking/manufacturing felony | YES |

*Minor misdemeanors don't create traditional "criminal record" but appear in background checks and carry license suspension

Important: Under current Ohio marijuana laws, per se DUI thresholds (2 nanograms THC per milliliter blood) can criminalize completely sober drivers who consumed cannabis legally days earlier. Active THC metabolites persist 2-7 days in regular users.

What Ohio Does Well: A Surprisingly Strong Start

Ohio's adult-use launch demonstrated regulatory competence rare among new markets:

Rapid Implementation

Timeline:

- November 2023: Voters approve Issue 2

- December 7, 2023: Possession and home grow legal

- August 6, 2024: Retail sales begin

- 8 months from voter approval to sales (vs. 18-36 months in many states)

How: Built on existing medical infrastructure. Licensed medical dispensaries received dual-use authorization, avoiding New York's years-long delays.

Competitive Pricing

Price trajectory:

- August 2024 launch: $9.41/gram average

- September 2025: $6.54/gram average

- 30% price decline in 13 months

This rapid price compression indicates:

- Adequate supply (no artificial scarcity)

- Competition working (multiple cultivators/processors)

- Market maturing faster than Illinois or New Jersey

Market performance data: OSU Moritz College of Law Drug Enforcement and Policy Center tracks Ohio's cannabis market development

Comparison:

- Ohio: $6.54/gram

- Michigan: $2.52/gram (mature market, 5+ years)

- Illinois: $12-15/gram (high taxes, limited competition)

- Illicit market: $4-6/gram (mid-tier product)

Ohio's pricing sits between expensive Illinois and cheap Michigan—competitive enough to attract mainstream consumers, not yet optimized for heavy users.

Moderate Tax Structure

Ohio cannabis taxes:

- 10% excise tax (adult-use only)

- 5.75% state sales tax

- 0.25-2.25% local sales tax

- Total: 16-18.5% effective rate

This moderate approach avoids:

- California's disaster (15% excise + 7.25-10.25% sales + cultivation taxes = 30%+ total)

- Illinois's failure (25-37% effective rate depending on THC content and local taxes)

- Washington's initial 75% tax (since reduced after market failure)

Revenue generated (Aug 2024-Sep 2025):

- $1+ billion in sales

- $125+ million in state tax revenue

- Projected mature market: $2.1-2.3 billion sales, $340-390 million tax revenue

Home Cultivation Rights

Current law: 6 plants per person, 12 per household

This is critical because:

- Provides legal alternative for price-sensitive consumers

- Reduces market power of licensed operators

- Creates competitive pressure on retail pricing

- Actually less economically attractive than retail for most consumers (equipment, time, inconsistency)

BUT: SB 56 would reduce this to 6 plants per household total—cutting cultivation rights in half and reducing competitive pressure on dispensaries.

Geographic and Demographic Advantages

Population: 12 million (7th largest state)

Urban concentration: 60% of residents in 5 metros (Columbus, Cleveland, Cincinnati, Toledo, Akron)

- Allows efficient dispensary coverage

- Reduces delivery infrastructure costs

- Creates competition (multiple stores per city)

Border opportunities: Ohio borders five states:

- Michigan: Legal (since 2018), mature market, price competition

- Pennsylvania: Medical only, 13M population, potential future market

- West Virginia: Medical only (limited), small population

- Kentucky: Medical starting 2025, potential adult-use

- Indiana: Complete prohibition, conservative culture

Framework significance: Ohio sits at crossroads—could become Midwest hub like Nevada serves the West, OR lose market share to Michigan if policy fails.

What Limits Optimization: SB 56 and Structural Barriers

Senate Bill 56: Legislative Assault on Voter Intent

SB 56 represents the Ohio General Assembly's systematic attempt to undermine voter-approved legalization:

What SB 56 does:

- Recriminalizes out-of-state cannabis

- Makes it illegal to possess cannabis purchased legally in Michigan or any other state

- Unenforceable in practice (how do police determine where you bought it?)

- Creates legal liability for Ohioans near Michigan border who cross-shop

- Reduces home cultivation from 12 to 6 plants per household

- Cuts cultivation rights in half

- No medical or safety justification (illicit grows remain illegal regardless)

- Protects dispensary profit margins at consumer expense

- Lowers THC limits from 90% to 70% for extracts

- Arbitrary limit not based on safety research

- Forces product reformulation

- 70% still adequate for most consumers but reduces patient/heavy user options

- Eliminates Cannabis Social Equity and Jobs Program

- Defunds equity provisions (40% of excise tax revenue)

- Entrenches existing operators

- Blocks entry for minority-owned businesses and those impacted by war on drugs

- Caps dispensaries at 400 statewide

- Creates artificial scarcity

- Ohio currently has ~165 dispensaries (1 per 73,000 residents)

- Michigan has 1,500+ (1 per 6,600 residents)—5× better access

- Prevents competition from improving pricing/service

- Repeals non-discrimination protections

- Removes Issue 2's protections against employment discrimination, custody determinations

- Maintains stigma despite legal status

- Affects medical patients too (removes protections extended to adult-use)

- Requires expungement applications with $50 fee

- Automatic expungement would be free and proactive

- $50 fee + application burden ensures many won't pursue

- Keeps criminal records despite legalization

Current status (November 2025):

- Passed Senate 23-9 (Feb 2025)

- Passed House 87-8 (Oct 2025)

- Senate REJECTED House version 0-32 (Oct 2025)

- In conference committee

- Likely final vote December 2025

Predicted outcome: Compromise version passes with some restrictions (home grow reduction, THC limits, dispensary caps) but not all (out-of-state ban likely dropped as unenforceable).

CBDT impact: If SB 56's most restrictive provisions become law, Ohio's legal market share could decline from projected 55-60% to 45-55%—policy failure despite voter approval.

Insufficient Dispersary Density

Current: ~165 dispensaries, 1 per 73,000 residents

Comparison:

- Michigan: 1 per 6,600 (5× better)

- Colorado: 1 per 6,000 (4× better)

- Nevada: 1 per 10,000 (3× better)

- Illinois: 1 per 130,000 (worse than Ohio)

Geographic gaps:

- Columbus, Cleveland, Cincinnati: "Respectable" coverage (4-8 stores each)

- Akron, Toledo, Dayton: Limited (2-4 stores)

- Rural counties: Many have ZERO stores, nearest is 30-60 minutes away

- Small cities (10,000-50,000 population): Underserved or zero access

Municipal bans: ~124 municipalities (5% of local governments) enacted temporary moratoriums as of Dec 2024

- Far better than Michigan (75% ban rate) or New York (50%)

- But still creates dead zones

Framework significance: Access density weighs approximately 1× in market outcomes. Ohio's current density is adequate for urban consumers, inadequate for rural. SB 56's 400-dispensary cap would prevent optimization.

The Michigan Problem: Border Pressure

Michigan presents Ohio's most significant competitive threat:

Michigan advantages:

- $2.52/gram average pricing (60% cheaper than Ohio)

- 1,500+ dispensaries (5× Ohio's per-capita density)

- Mature market (legal since 2018)

- No residency requirements for purchases

- More product variety, established brands

Economic impact on Ohio:

- Northern border residents (Toledo, Cleveland, Youngstown, Akron): 3-4 million Ohioans within 30-60 minutes of Michigan

- Price differential: $4+/gram savings = $30-40/ounce

- Monthly savings for regular user: $120-160 by driving to Michigan

- Estimated annual cross-border loss: $200-300 million in sales Ohio could capture

Why Michigan is cheaper:

- Longer market maturation (prices declined over 5 years)

- Massive oversupply (1,500+ dispensaries competing)

- Lower cost structure (280E affects both, but scale economies matter)

Ohio cannot match Michigan pricing without federal reform. But Ohio can reduce gap by:

- Expanding dispensary access (more competition)

- NOT increasing taxes (SB 56 proposals to raise excise tax to 15-20% would widen gap)

- Maximizing convenience (delivery authorization)

SB 56's out-of-state ban: Attempts to criminalize Ohioans bringing Michigan cannabis home. Unenforceable (how do police prove where you bought it?) but creates legal uncertainty.

Federal Barriers: 280E and Banking

Internal Revenue Code Section 280E prevents cannabis businesses from deducting normal operating expenses, creating effective federal tax rates of 40-70% before state taxes.

Ohio-specific impact:

- Dispensary with $5M revenue, $3M operating costs pays federal tax on full $5M (not $2M profit)

- Forces retail prices 15-20% higher to maintain viability

- Ohio's current $6.54/gram would drop to $5.25-5.50/gram without 280E

- At $5.50/gram, Ohio becomes competitive with illicit pricing and reduces Michigan gap

Solution: Schedule III rescheduling (currently under DEA consideration) would eliminate 280E.

SAFE Banking Act absence forces cash-only operations:

- Reduces transaction frequency 18-25% vs. card payments

- Increases security costs 25-40%

- Customer inconvenience (must bring cash)

- Prevents competitive payment processing

Ohio banks: Fewer than 10 Ohio banks/credit unions serve cannabis businesses (out of 200+ statewide), creating monopoly pricing on financial services.

CBDT assessment: Combined federal reform (280E repeal + SAFE Banking) could improve Ohio's legal market share by 20-25 percentage points—from 55-60% to 75-85%.

Framework Assessment: Ohio's Market Trajectories

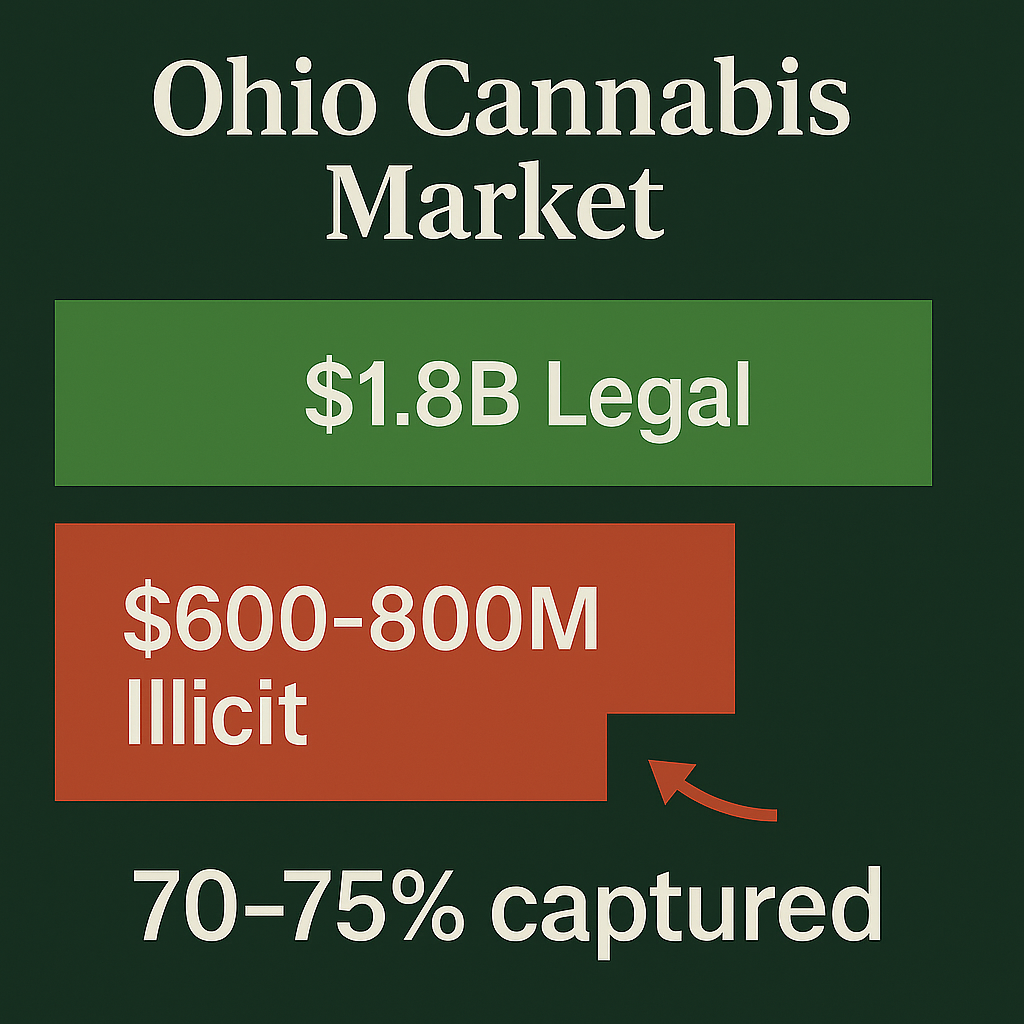

Current Performance: 55-60% Legal Market Share

Estimated total Ohio cannabis market: $3.8-4.2 billion annually (legal + illicit + cross-border)

Legal market capture: $2.1-2.3 billion (55-60% share)

What drives current performance:

| Variable | Score | Weight | Impact |

|---|---|---|---|

| Price competitiveness | 0.55 | 4× | MODERATE (280E inflates prices, Michigan undercuts) |

| Access density | 0.50 | 1× | MODERATE (urban adequate, rural poor) |

| Product quality/testing | 0.85 | 1.2× | STRONG (Metrc tracking, testing standards) |

| Convenience | 0.40 | 0.8× | WEAK (cash-only, no delivery) |

| Enforcement | 0.60 | 0.6× | MODERATE (some resources, but illicit grows persist) |

| Fragmentation penalty | -0.10 | - | MINIMAL (5% local bans, Michigan border bleed) |

Legal market breakdown:

- Retail sales: $2.0-2.2 billion

- Cross-border recapture from Pennsylvania: $100-150 million (PA residents buying in Ohio)

- Tourist/temporary residents: Minimal (unlike Nevada)

Illicit market: $1.5-1.8 billion (40-45% share)

- Untested products, no quality control

- No tax revenue generated

- Continued criminal justice burden

- Price advantage: 20-40% cheaper than legal

Tax revenue (mature market projection):

- $2.2B sales × 10% excise = $220M

- $2.2B sales × 5.75% state sales tax = $126M

- Local sales tax: $40-50M

- Total government revenue: $390-400M annually

Employment:

- Direct jobs: 7,400-9,000

- Indirect: 11,000-13,000

- Total economic footprint: 18,400-22,000 jobs

Optimized Scenario: 75-80% Legal Share (WITH Federal Reform)

Policy design:

- Federal 280E repeal + SAFE Banking passage

- Maintain 10% excise tax (reject SB 56 tax increases)

- Expand to 300-350 dispensaries (reject SB 56's 400 cap)

- Authorize statewide delivery

- Maintain 12-plant home grow (reject SB 56 reduction)

- Dedicate $15-25M to illicit market enforcement

Predicted outcomes:

- Legal market: $3.0-3.3 billion annually

- Illicit market: $800M-1.0 billion (20-25% residual)

- Tax revenue: $470-540M annually

- Jobs: 14,000-16,000 direct, 35,000-40,000 total

- Timeline: 24-36 months to reach steady state

Comparable markets:

- Michigan: 85% (mature, optimized)

- Colorado: 84% (with federal reform likely 90%+)

- Nevada: 75-80% (enforcement strong, access good)

Revenue increase over current: $80-140M annually—enough to fund:

- 1,000+ additional K-12 teachers

- Comprehensive opioid treatment infrastructure

- Economic development in struggling regions (Youngstown, Appalachian Ohio)

Failed Scenario: 45-55% Legal Share (SB 56 Enacted + No Federal Reform)

Policy design (nightmare scenario):

- SB 56 passes with most restrictive provisions

- Home grow reduced to 6 plants total

- Dispensary cap at 400 (prevents expansion)

- Excise tax increased to 15-20%

- No delivery authorization

- 280E and banking barriers persist

- Weak enforcement (budget cuts)

Predicted outcomes:

- Legal market: $1.7-2.3 billion

- Illicit market: $1.5-2.5 billion (DOMINANT 55-65%)

- Tax revenue: $340-520M (higher rate on smaller base generates similar revenue to current)

- Jobs: 8,000-11,000

- Result: Policy failure despite legalization

Comparable markets:

- California: 50% (high taxes, fragmentation, weak enforcement)

- Illinois: 55-60% (high taxes, limited access)

Difference from optimized: $1.0-1.6B less legal market activity, 5,000-8,000 fewer jobs, persistent criminal market

Policy Recommendations for Ohio

1. REJECT Senate Bill 56's Worst Provisions

Ohio General Assembly should:

REJECT:

- Home grow reduction (keep 12 plants per household)

- Out-of-state cannabis ban (unenforceable, creates liability)

- Dispensary cap at 400 (prevents optimization)

- Social Equity Program elimination (equity matters)

- Non-discrimination repeal (maintains stigma)

CONSIDER (if evidence-based):

- THC limit reduction from 90% to 70% (if medical exemption for patients)

- Edibles limits (10mg serving, 100mg package matches industry standard)

- Expungement with reduced/no fee (not $50 barrier)

Political reality: Compromise likely. Framework predicts outcome determines 10-15 percentage point swing in legal market share.

2. Expand Dispensary Access to 300-350 Statewide

Current: ~165 dispensaries

Target: 300-350 (1 per 35,000-40,000 residents, matching Colorado's ratio)

Prioritize:

- Rural counties with zero access

- Small cities (10,000-50,000 population)

- Appalachian Ohio (economic development opportunity)

- Border regions competing with Michigan

Delivery authorization: Critical for geographic gaps. Allow licensed dispensaries to deliver statewide with:

- Age verification (ID check)

- Order limits (prevent bulk resale)

- Secure transport

- Available in municipalities without retail locations

Framework impact: +10-12 percentage points improvement in legal share

3. Maintain Current Tax Rate (10% Excise)

Do NOT increase to 15% (proposed in some SB 56 versions) or 20% (Governor's budget proposals)

Why:

- Current 16-18.5% total effective rate is MODERATE

- Already competing with Michigan's lower prices

- Revenue optimization comes through VOLUME (market share growth), not RATE (per-unit increase)

- California proves high taxes = market failure

Economic research: 10% increase in legal prices reduces legal choice probability by 2.3% but $2.2B base × 60% share × 10% excise generates MORE revenue than $1.8B base × 50% share × 15% excise

Recommendation: Wait for federal 280E repeal (which reduces costs 15-20%) before considering tax increases. Let cost reduction improve market share FIRST, then potentially capture savings via tax increase LATER.

4. Federal Policy Advocacy (Ohio Congressional Delegation)

Ohio's delegation (2 senators, 15 representatives) should champion:

Priority #1: 280E Repeal

- Biggest single impact: 15-20% price reduction

- Improves Ohio's competitiveness with Michigan

- Not federal legalization—just tax fairness for state-legal businesses

Priority #2: SAFE Banking Act

- Enables card payments, reduces cash handling costs

- Public safety benefit (reduced robbery risk)

- Bipartisan support (has passed House 7 times)

Priority #3: Schedule III rescheduling

- Eliminates 280E automatically

- Resolves banking barriers

- Administration action (doesn't require Congress)

Conservative framing: "Not about legalizing federally—about letting states' voters' decisions work. Ohioans voted 57% for legalization. Federal policy shouldn't prevent Ohio from implementing that decision successfully."

Pragmatic framing: "Michigan is stealing Ohio's tax revenue. Federal reform would level the playing field."

5. Dedicate Enforcement Resources ($15-25M Annually)

Target: Large-scale illegal cultivation (1,000+ plants), interstate trafficking

Avoid: Small-scale home grow enforcement, consumer possession

Rationale: States with strong enforcement (Nevada, Colorado) outperform states with weak enforcement (California, New York) by 15-25 percentage points

Budget: $15-25M annual enforcement budget ($1.25-2.10 per capita) generates:

- Illicit market disruption worth $300-500M (reduces untaxed competition)

- ROI: Every $1 spent generates $12-20 in legal market shift

- Protects legal businesses from illegal competition

Framework impact: +8-12 percentage points legal market share

Geographic Neighbor Analysis

Michigan: The Competitive Threat

Michigan's mature market (legal since 2018) creates both challenge and lesson:

Challenge: $2.52/gram pricing (60% cheaper than Ohio), 1,500+ dispensaries (5× Ohio's density)

Lesson: Michigan proves that market maturation + adequate access + reasonable taxes = optimization (85% legal share)

Ohio cannot match Michigan pricing under current federal policy (280E affects both, but Michigan's scale and maturity create advantages).

But Ohio can reduce gap:

- Federal reform (280E repeal) narrows gap to $1-2/gram (manageable)

- Expanded access reduces convenience advantage

- Border-region dispensaries near Toledo/Cleveland can compete on convenience vs. long drives to Michigan

Long-term: If Ohio optimizes and Michigan raises taxes, competitive balance shifts. Michigan is considering tax increases to fund other priorities—Ohio should NOT make same mistake.

Pennsylvania: The Unrealized Opportunity

Pennsylvania (13 million residents, medical-only) represents Ohio's largest market opportunity:

Current: PA residents near border (Youngstown, Steubenville, Pittsburgh suburbs) can't legally purchase in Ohio (must be Ohio resident)

If PA legalizes adult-use (possible 2026-2028):

- Border cities see traffic surge (like Missouri near Illinois border)

- Ohio captures PA spending if pricing competitive

- BUT PA could also optimize and keep market share

If PA stays medical-only:

- Some PA medical patients may cross-shop Ohio adult-use (technically illegal but happens)

- Minimal revenue impact (medical patients prefer PA medical for protections)

Framework significance: PA legalization could add $50-100M to Ohio market (PA border residents purchasing in Ohio), but only if Ohio offers competitive pricing and access.

Kentucky, West Virginia, Indiana: Prohibition States

Kentucky: Medical starting 2025, adult-use unlikely short-term

West Virginia: Medical (limited), adult-use unlikely

Indiana: Complete prohibition, very conservative

Current impact: Minimal. Southern Ohio border regions aren't major population centers. Northern border (Michigan) matters far more.

Future: If any legalize adult-use, Ohio's central location becomes hub opportunity (like Nevada serves regional demand).

Timeline and Realistic Expectations

Phase 1: Current State (2024-2025)

Achievements:

- Rapid launch (8 months voter approval to sales)

- 165 dispensaries serving 12M residents

- $1B+ sales in first 14 months

- Pricing competitive (30% decline from launch)

- 57% voter approval demonstrates cultural acceptance

Challenges:

- SB 56 legislative uncertainty

- Michigan competitive pressure

- Federal 280E/banking barriers

- Rural access gaps

Status: Moderate performance (55-60% legal share) with strong foundation

Phase 2: Optimization Without Federal Reform (2026-2027)

State-level actions:

- Reject worst SB 56 provisions (maintain 12-plant home grow, prevent dispensary cap)

- Expand dispensary licensing to 250-300

- Authorize statewide delivery

- Increase enforcement budget

Expected outcome: 60-65% legal share

Limitations: Cannot achieve 75%+ without federal reform (280E pricing barrier too significant)

Phase 3: Federal Reform Era (2028-2030)

If federal reform occurs (Schedule III rescheduling + SAFE Banking):

Impact:

- 280E repeal reduces retail prices 15-20% → $5.25-5.50/gram

- SAFE Banking enables card payments, reduces costs 8-12%

- Combined: Ohio becomes competitive with Michigan, undercuts illicit pricing

Timeline:

- Immediate: Businesses adjust (6-12 months for full pass-through to consumers)

- 12-24 months: Legal market share grows from 60-65% → 70-75%

- 24-36 months: Steady state at 75-80%

Expected outcome: Ohio achieves top-tier performance (matching Colorado, Michigan)

Legal market: $3.0-3.3B annually, $470-540M tax revenue

Phase 4: Mature Market (2030+)

Characteristics:

- 300-350 dispensaries statewide

- Statewide delivery infrastructure

- Card payments universal

- Pricing: $4-6/gram (competitive with Michigan, undercuts illicit)

- Legal share: 75-80% steady state

- Illicit market: 20-25% residual (price-sensitive heavy users, extreme rural areas)

Economic impact:

- Legal sales: $3.0-3.3B

- Tax revenue: $470-540M

- Jobs: 35,000-40,000 total

- Illicit market reduced 75-80% from prohibition baseline

The Economic Reality: Current vs. Optimized

Current Performance (55-60% Legal Share)

Market size: $3.8-4.2B total demand

Legal capture: $2.1-2.3B (55-60%)

Tax revenue:

- Excise: $220M

- State sales: $126M

- Local: $40-50M

- Total: $390-400M annually

Employment:

- Direct: 7,400-9,000

- Indirect: 11,000-13,000

- Total: 18,400-22,000 jobs

Illicit market: $1.5-1.8B (untaxed, unregulated, criminal)

Optimized Performance (75-80% Legal Share with Federal Reform)

Market size: $3.9-4.1B total (slight growth as stigma reduces)

Legal capture: $3.0-3.3B (75-80%)

Tax revenue:

- Excise: $300-330M

- State sales: $172-190M

- Local: $65-75M

- Total: $540-600M annually

Employment:

- Direct: 14,000-16,000

- Indirect: 21,000-24,000

- Total: 35,000-40,000 jobs

Illicit market: $800M-1.0B (reduced 75-80%)

The $150-200M Annual Question

Difference between current and optimized: $150-200M in additional annual state tax revenue

What that funds:

- 2,000 additional K-12 teachers at $75,000 compensation

- $245,000 annual grants to each of Ohio's 612 school districts

- Comprehensive opioid addiction treatment infrastructure

- Economic development in Appalachian Ohio, Youngstown, Cleveland, Toledo

The barrier: Federal policy (280E, banking) prevents this optimization. Ohio has done most of what it can do at state level. The final 15-20 percentage points require federal action.

Why Federal Reform Matters More for Ohio Than Most States

The Michigan Squeeze

Without federal reform, Ohio faces permanent disadvantage:

- Michigan's mature market + scale economies = structurally lower costs

- Ohio's 280E burden = structurally higher costs

- Gap widens over time as Michigan matures further

With federal reform:

- 280E elimination narrows gap

- Ohio's larger population (12M vs. 10M) creates scale advantage

- Competitive balance shifts in Ohio's favor

Border State Dynamics Create Urgency

Unlike isolated states (Hawaii, Alaska), Ohio must compete with neighboring markets:

- Michigan (mature, cheap, accessible)

- Pennsylvania (if legalizes)

- Kentucky (medical starting, adult-use possible)

Without federal reform: Ohio loses market share to better-positioned neighbors

With federal reform: Ohio captures market share from prohibition states (Indiana, potentially WV)

The Conservative Economic Argument

Ohio's Republican congressional delegation could be persuaded by fiscal argument:

"Ohioans voted 57% for legalization. We're not asking you to support legalization federally. We're asking you to let Ohio's voters' decision work. Right now, federal policy ensures Michigan captures Ohio's tax revenue. 280E repeal and SAFE Banking would let Ohio compete fairly."

Not cultural issue: Pragmatic governance (respecting federalism, maximizing state revenue)

Not legalization advocacy: Tax fairness for businesses operating under state law

This argument works in conservative Ohio. The state's congressional delegation could lead bipartisan reform coalition.

Social Equity and the Stakes of SB 56's Defunding

The Cannabis Social Equity and Jobs Program (What SB 56 Would Eliminate)

Issue 2 dedicated 40% of excise tax revenue ($80-90M annually at mature market) to:

- Financial assistance for minority-owned cannabis businesses

- Application support for individuals impacted by marijuana prohibition

- Job training and workforce development

- Community reinvestment in areas disproportionately affected by drug enforcement

Why this matters:

War on drugs impact in Ohio:

- Black Ohioans are 4× more likely to be arrested for cannabis possession than white Ohioans, despite similar usage rates

- 20,000+ annual cannabis arrests pre-legalization

- Disproportionate impact in Cleveland, Cincinnati, Columbus, Toledo minority communities

- Criminal records create lifetime employment, housing, education barriers

Industry access barriers:

- Cannabis business licenses cost $150,000-500,000 (application, real estate, equipment, inventory)

- Existing medical license holders (predominantly white-owned corporations) have competitive advantage

- Without equity support, legalization entrenches existing operators rather than creating opportunities for those harmed by prohibition

SB 56's equity program elimination means:

- $80-90M annual funding redirected to general fund

- No financial assistance for minority entrepreneurs

- No application support or technical assistance

- No community reinvestment in impacted neighborhoods

- Perpetuates same racial disparities prohibition created

National evidence: States without robust equity programs (Alaska, Montana) see industry ownership that doesn't reflect demographics. States with strong programs (Illinois, Massachusetts) show measurable improvement (though still insufficient).

Ohio should learn from Illinois: Strong equity program on paper, but implementation delays and capital access barriers limited effectiveness. Money alone doesn't solve problem—need technical assistance, simplified licensing, and enforcement of equity provisions.

Framework impact: Equity program elimination doesn't directly affect legal market share (doesn't change price or access for consumers). But it determines who profits from legalization—existing corporations or new entrepreneurs including those harmed by prohibition.

Enforcement Strategy: Ohio's Unique Strength

Why Strong Enforcement Improves Legal Market Performance

Ohio's law enforcement culture represents potential competitive advantage if deployed strategically:

Current Ohio law enforcement capacity:

- Well-funded state/local coordination

- Cooperative relationships between jurisdictions

- Political support for drug interdiction

- Institutional knowledge from prohibition enforcement

Strategic redirection (from consumer arrests to illicit supply interdiction):

STOP: Arresting consumers for possession, targeting small-scale home grows (6-12 plants), street-level distribution

START: Targeting large-scale illegal cultivation (1,000+ plants), interstate trafficking, unlicensed dispensaries operating as "gift shops" or "hemp stores"

Budget allocation ($15-25M annually, $1.25-2.10 per capita):

- Illegal grow task forces ($8-12M): Target operations over 500 plants, coordinate with federal DEA

- Market investigations ($4-6M): Unlicensed retail, illicit online sales, social media dealers

- Testing/prosecution ($3-7M): Lab analysis, district attorney resources for trafficking prosecutions

ROI analysis: Every $1 spent on targeted enforcement generates $12-20 in legal market shift by:

- Eliminating price-competitive illicit supply (forces consumers to legal market)

- Protecting legal businesses from unfair competition

- Demonstrating regulatory effectiveness (builds public trust)

- Creating risk premium for illicit operators (increases their costs)

State comparisons:

Nevada (75-80% legal share):

- Aggressive enforcement of illegal grows in desert (easy to detect from air)

- Dedicated cannabis enforcement unit ($3-4 per capita)

- Strong local/state/federal coordination

Colorado (84% legal share):

- Marijuana Enforcement Division with $20M+ annual budget

- Targets illegal grows (300+ plants), unlicensed sales

- Cooperative relationship with legal operators (industry tips lead to investigations)

California (50% legal share):

- WEAK enforcement (interdicts only 3% of estimated 10,000+ illegal grows)

- Permits culture tolerates gray/black markets

- Result: Thriving illicit market despite legalization

Ohio's choice: Follow Nevada/Colorado model (strong targeted enforcement improves legal share) or California model (weak enforcement ensures market failure)

Framework weight: Enforcement = 0.6× multiplier. Well-executed enforcement strategy worth 8-12 percentage point improvement in legal market share. This means $300-500M shift from illicit to legal market, generating $30-50M in additional tax revenue.

Political sell: Frame as "protecting legal businesses from illegal competition" rather than "drug war continuation." Legal cannabis industry will support enforcement if it targets illicit competitors rather than consumers.

Cultural Context: Conservative State, Pragmatic Voters

How Ohio's Political Culture Affects Cannabis Policy

Ohio isn't Oregon or California. The state's conservative culture shapes both challenges and opportunities:

Voter approval (57% for Issue 2):

- Higher than Colorado's initial 55% (2012)

- Lower than Michigan's 56% (2018)

- Demonstrates pragmatic center (not overwhelming mandate, but clear majority)

What 57% approval means:

- Ohioans recognize prohibition failed

- Support regulated access over criminal market

- NOT necessarily enthusiastic endorsement

- Leaves political space for reasonable regulation, limited tolerance for dysfunction

Legislative response (SB 56):

- Reflects conservative skepticism (57% isn't 75%)

- Attempts to "fix" what voters approved

- Politically risky (voters approved specific framework)

- But not unusual (many states modify voter initiatives)

Workplace discrimination (Ohio allows):

- Employers can maintain zero-tolerance policies

- Can fire for off-duty legal use detected via testing

- No protection for medical patients either

- Cannabis is coffee, not cocaine—but Ohio law treats it like heroin for employment purposes

This maintains stigma despite legalization:

- Safety-sensitive positions (commercial drivers, healthcare, education): Reasonable restrictions

- Office workers, retail employees, service jobs: Zero-tolerance policies unjustified but legal

- Creates barrier to mainstream acceptance

DUI/OVI per se laws (2 ng/mL THC in blood):

- Criminalizes completely sober drivers who consumed legally days earlier

- Active THC metabolites persist 2-7 days in regular users

- No correlation with impairment (unlike alcohol's .08% BAC)

- Creates legal jeopardy for lawful consumers

Public consumption bans:

- Limited to private residences

- Landlords can prohibit (affecting renters)

- No legal consumption venues (unlike Alaska's pioneering approach)

- Creates access barrier for tourists, renters without private space

Framework significance: Stigma weighs approximately 0.5× in market outcomes. Workplace discrimination, DUI per se laws, public use bans maintain criminal justice system involvement despite legalization. Reduces legal market appeal vs. states with stronger protections.

Path forward: Ohio unlikely to lead on consumer protections (conservative culture). But could improve:

- DUI reform: Move to impairment-based testing rather than per se thresholds

- Workplace: Protect off-duty use for non-safety-sensitive positions

- Expungement: Automatic rather than application-based (eliminate SB 56's $50 fee)

- Public use: Create licensed consumption venues (revenue opportunity)

Ohio's Economic Development Opportunity

Cannabis as Post-Industrial Economic Engine

Ohio's struggling regions could benefit substantially from cannabis industry development:

Appalachian Ohio (southeastern counties):

- High unemployment, limited economic opportunities

- Coal mine closures, manufacturing decline

- Agricultural tradition (could support outdoor greenhouse cultivation)

- Low real estate costs (cultivation facility advantage)

Youngstown/Warren/Akron (northeastern Ohio):

- Post-industrial cities with available workforce

- Former manufacturing facilities suitable for conversion to cultivation

- Proximity to Cleveland, Pittsburgh markets

- Economic diversification need

Toledo region (northwestern Ohio):

- Competition with Michigan border

- Need competitive operations to retain market share

- Distribution hub for western Ohio, potential northern Indiana if legalizes

Potential impact (optimized scenario):

Cultivation jobs: 3,500-5,000

- Average wage: $35,000-48,000 ($18-25/hour)

- Prefer regions with: Lower real estate costs, available workforce, agricultural tradition

- Appalachian Ohio, northwestern Ohio, rural areas around metros

Processing jobs: 1,500-2,500

- Average wage: $38,000-52,000 ($20-28/hour)

- Require: Technical skills (extraction, formulation), quality control

- Mid-sized cities (Canton, Springfield, Lima, Mansfield)

Retail jobs: 3,500-5,000

- Average wage: $32,000-42,000 ($16-22/hour)

- Locations: All population centers

- Customer service skills, compliance knowledge

Testing/compliance: 800-1,200

- Average wage: $48,000-68,000 ($25-35/hour)

- Require: Lab technician training, certifications

- Clustered in metros (Columbus, Cleveland, Cincinnati)

Professional services: 1,500-2,500

- Lawyers, accountants, consultants, security, insurance

- Higher wages: $55,000-95,000

- Primarily metro areas

Total direct employment: 14,000-16,000 (optimized scenario)

Total economic footprint: 35,000-40,000 (including indirect/induced)

Regional distribution (optimized access):

- Columbus metro: 3,500-5,000 jobs

- Cleveland metro: 3,000-4,000 jobs

- Cincinnati metro: 2,500-3,500 jobs

- Akron/Canton: 1,500-2,000 jobs

- Toledo metro: 1,200-1,800 jobs

- Dayton metro: 1,000-1,500 jobs

- Youngstown/Warren: 800-1,200 jobs

- Appalachian Ohio: 1,500-2,500 jobs (cultivation focus)

- Rural/small cities: 2,000-3,000 jobs (distributed)

Payroll impact: $550-750M annually (direct wages)

Property tax impact: Cultivation/processing facilities pay property taxes on real estate, equipment

- Converted industrial facilities revitalized

- Blighted properties repurposed

- Local tax base strengthened

Comparison to other industries (Ohio context):

- Ohio auto manufacturing: ~93,000 jobs, $8B+ annual production

- Potential cannabis industry: 35,000-40,000 jobs, $3.0-3.3B annual sales

- Cannabis would represent ~40% the size of auto industry by employment, similar revenue per worker

The Michigan Border: Detailed Competitive Analysis

Why Northern Ohio Loses to Michigan (And How to Compete)

Border region population (within 60 minutes of Michigan):

- Toledo metro: 650,000

- Cleveland metro west side: 800,000

- Youngstown/Warren: 400,000

- Total: ~1.85M Ohioans in Michigan's market reach

Estimated cross-border leakage: $200-300M annually

- Represents 10-15% of Ohio's total potential market

- Lost to Michigan dispensaries serving Ohio residents

Why Michigan wins:

- Price: $2.52/gram vs. $6.54/gram (60% cheaper)

- $30-40 per ounce savings

- For monthly users (1-2 oz): $360-480 annual savings

- Justifies 30-60 minute drive

- Selection: 1,500+ dispensaries = vast product variety

- Specific strains, brands, formats

- Ohio's 165 stores have limited selection

- Enthusiasts value variety enough to drive

- Maturity: 5+ years legal = established brands, consumer trust

- Ohio still building reputation

- Michigan has recognized quality operators

- No residency requirement: Michigan serves out-of-state customers legally

- Ohio requires residency for medical, allows adult-use for visitors

- But Michigan's infrastructure better serves nonresident traffic

How Ohio can compete (even without matching pricing):

Strategy #1: Convenience optimization

- Authorize delivery (eliminates drive to Michigan)

- Expand border-region dispensary density (Toledo, Cleveland suburbs)

- Extended hours (Michigan stores often close 9pm, Ohio could go later)

- Better locations (highway access, parking)

Impact: Captures 20-30% of current Michigan traffic (consumers valuing convenience over price)

Strategy #2: Federal reform advocacy

- 280E repeal narrows price gap from $4/gram to $1-2/gram

- At $1-2/gram difference, convenience matters more

- Ohio captures 50-70% of border traffic

Impact: $100-210M annual recapture

Strategy #3: Quality/safety differentiation

- Emphasize Ohio testing standards, consumer protections

- Market Ohio as "premium, tested, safe"

- Some consumers (parents, professionals, quality-focused) value safety over price

Impact: Captures 10-15% of Michigan traffic (safety-conscious segment)

Strategy #4: Host Community Fund competitive advantage

- Michigan has struggled with local tax distribution fights

- Ohio's 36% revenue to host communities creates local buy-in

- More Ohio communities welcome dispensaries = better access

Combined realistic recapture (without federal reform): 30-40% of current leakage = $60-120M

With federal reform: 60-80% recapture = $120-240M

SB 56 impact: Restrictive provisions (home grow cuts, dispensary caps, tax increases) would WORSEN Michigan competition, potentially increasing leakage to $350-450M. This is the hidden cost of legislative overreach—driving consumers to neighboring states.

Conclusion: Ohio at the Crossroads

Is weed legal in Ohio? Yes—voters decisively approved adult-use legalization in 2023 with 57% support.

Will Ohio's legalization succeed? That depends on two questions:

Question 1: Will the Ohio General Assembly respect voter intent, or will SB 56 undermine it?

Respect voter intent (reject worst SB 56 provisions): Ohio achieves 60-65% legal share without federal help, 75-80% with federal reform

Undermine voter intent (SB 56's restrictive version): Ohio falls to 45-55% legal share, policy failure

Question 2: Will federal reform occur, or will 280E and banking barriers persist?

Federal reform (Schedule III + SAFE Banking): Ohio becomes top-tier market (75-80% legal share, $470-540M tax revenue)

No federal reform: Ohio plateaus at moderate performance (55-65%, $390-460M tax revenue)

The stakes: $150-200M annual tax revenue difference, 15,000-20,000 jobs, fundamental success or failure of voter-approved policy.

Ohio has done most of what it can do at the state level. The state's voter-approved framework is sound, current tax rate is reasonable, and geographic position creates opportunity. What happens next depends on:

- State politicians: Respect voter intent or undermine it via SB 56

- Federal policy: Remove barriers (280E, banking) or maintain them

- Market dynamics: Compete with Michigan or lose share to neighbors

For Ohio policymakers: The path is clear. Reject SB 56's worst provisions, expand access, maintain moderate taxes, and advocate for federal reform. Success is achievable if politics allows evidence-based policy.

For Ohio's congressional delegation: Your state loses hundreds of millions annually because federal policy prevents state-legal markets from optimizing. 280E repeal and SAFE Banking aren't about supporting cannabis—they're about respecting Ohio's voters and protecting Ohio's revenue.

Ohio stands at a crossroads. With good state policy and federal reform, it could become the Midwest's cannabis success story. Without it, Ohio becomes another California—voters approved legalization, politicians undermined it, policy failed despite good intentions.

The Buckeye State's potential is clear. Whether it achieves that potential depends on decisions made in Columbus and Washington, D.C.

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Utah | Louisiana | Maryland | Rhode Island

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0