Pennsylvania Cannabis Market Analysis: The Keystone State's Medical Success and the Adult-Use Opportunity Waiting at the Border

How 460,000 medical patients, the nation's sixth-largest cannabis market, and 70% public support can't overcome a Republican Senate—while five neighboring states collect Pennsylvania's tax revenue

The Silent Majority 420 | November 2025

The Prohibition Island Paradox

Is weed legal in Pennsylvania? Medical yes, recreational no—but that simple answer obscures America's most consequential cannabis policy failure.

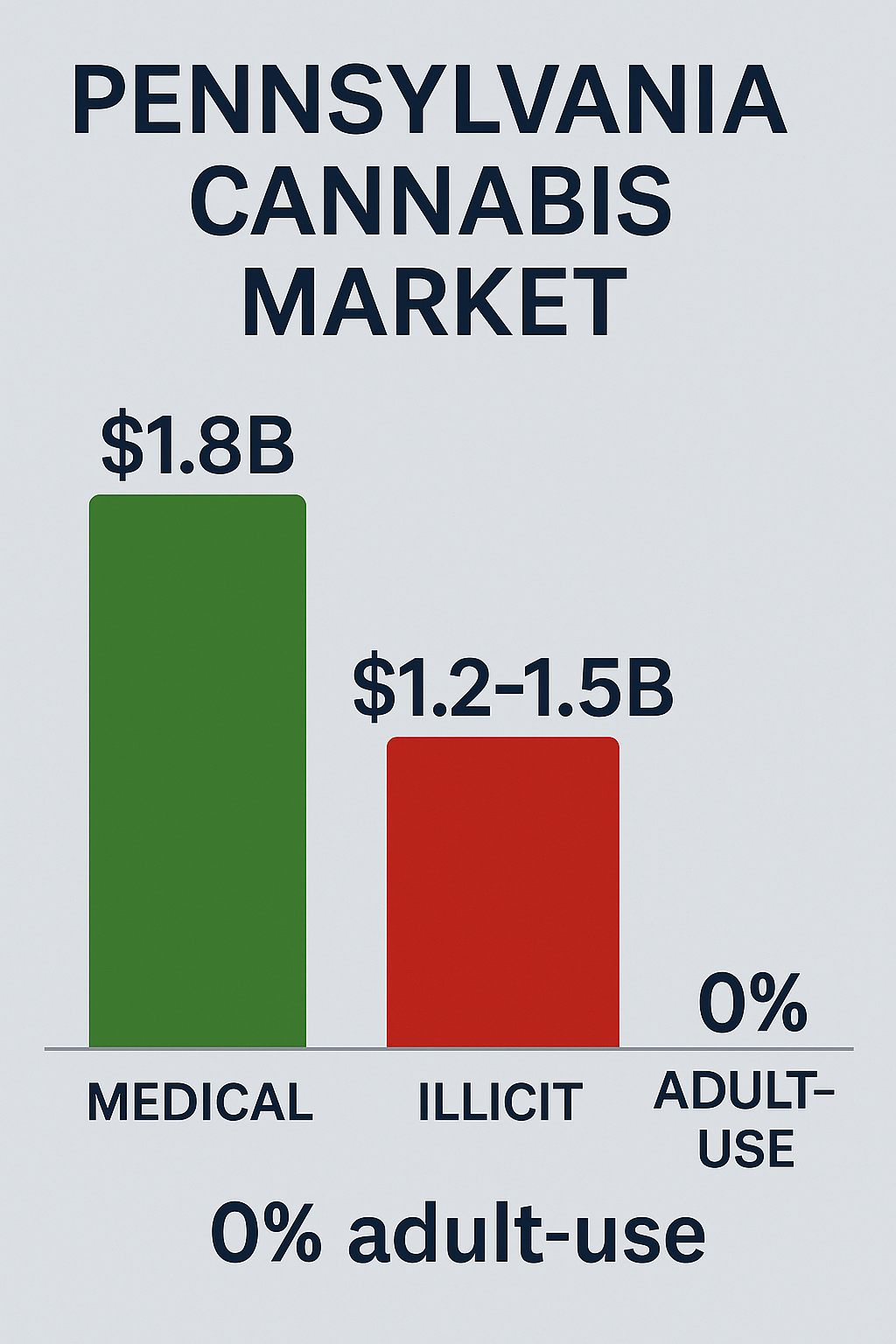

Pennsylvania operates the nation's sixth-largest cannabis market with $1.73 billion in annual medical sales, 460,000 registered patients (11-13% of the adult population—the HIGHEST medical participation rate in America), and 188 operational dispensaries generating 25,000+ jobs. Governor Josh Shapiro's February 2025 budget proposal included adult-use legalization. The Democratic-controlled House passed recreational cannabis legislation 102-101 in May 2025. Seventy percent of Pennsylvania voters support legalization.

Yet Pennsylvania remains recreational cannabis prohibition's last island in the Northeast—surrounded on five sides by legal adult-use states actively harvesting Pennsylvania's tax revenue.

Drive 20 minutes from Philadelphia to New Jersey: adult-use legal since 2022. Drive 90 minutes from Pittsburgh to Ohio: recreational sales launched November 2023. Head north to New York, south to Maryland, or southeast to Delaware—all adult-use legal. Five of six neighboring states (only West Virginia excluded) collect tax revenue from Keystone State residents.

Governor Shapiro articulated the absurdity in his budget address: "I've talked to the CEOs of companies right across the border in New Jersey, Maryland and New York, who tell me 60% of their customers in those shops are Pennsylvanians. We're losing out on revenue that's going to other states instead of helping us right here."

The numbers validate his concern:

- $300-400 million annually: Pennsylvania cannabis spending flowing to neighboring states (conservative estimate)

- $60-100 million: Tax revenue collected by New Jersey, Maryland, Ohio, New York instead of Pennsylvania

- 11,000+ arrests: Annual Pennsylvania marijuana arrests despite medical program (2023 data)

- 460,000 medical patients: Demonstrating consumer demand at 3.4% of total state population

- $1.6 billion budget deficit: Creating urgency for new revenue sources (FY 2025-2026)

The political reality: Democratic Governor pushing legalization + Democratic House passing bills + 70% voter support = irrelevant when Republican-controlled Senate blocks every proposal. House Bill 1200 passed 102-101 in May 2025; Senate Law & Justice Committee tabled it 7-3 six days later.

Pennsylvania joins the elite club of states where overwhelming public support, neighboring state success, massive medical infrastructure, and severe budget crisis still cannot overcome divided government gridlock.

But this stalemate creates opportunity. The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Pennsylvania's exceptional potential: IF the state legalizes with evidence-based policy and federal reform occurs, Pennsylvania could achieve 75-82% legal market share within 36-48 months—outperforming most neighboring states despite later entry.

Pennsylvania possesses advantages no other state enjoyed at legalization:

- Seven years of medical program infrastructure ($7.68 billion cumulative sales)

- Five neighbors providing real-world comparison data on what works and what fails

- 188 operational dispensaries ready for rapid adult-use conversion

- 460,000 proven customers demonstrating demand

- Geographic concentration (92% of population in 7 metros) reducing dispensary density requirements

The state that built America's most successful medical-only program could become one of the nation's most optimized adult-use markets—by learning from every mistake its neighbors made.

The question isn't whether Pennsylvania should legalize. Voters decided that in polling years ago. The question is: How much longer will Pennsylvania subsidize New Jersey, Maryland, and Ohio while arresting its own residents for behavior legal 20 minutes away?

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted 82% volume share, ~95% transaction share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Status: Is Weed Legal in Pennsylvania?

Medical Cannabis: LEGAL (Since 2016)

Pennsylvania Medical Marijuana Act (Act 16): Signed April 17, 2016 by Governor Tom Wolf. Dispensaries opened February 2018.

Pennsylvania medical marijuana card:

- State fee: $50/year (Pennsylvania Department of Health)

- Reduced fee: $0-25 for Medicaid, SNAP, WIC, PACE/PACENET, CHIP participants

- Doctor consultation: $99-249 (varies by provider - QuickMedCards $99, Veriheal $199, FadeMD $99)

- Total cost: $149-299/year first time, $99-249/year renewal

- Processing time: 21 days (7 days printing, 14 days mail)

- Replacement card: $25 first replacement, $50 subsequent

Patient count: 460,000+ active (as of April 2025) - LARGEST medical program participation rate nationally at 11-13% of adult population

Comparison:

- Florida: 920,000 patients (4.2% population)

- Oklahoma: 369,000 (8.5%)

- Pennsylvania: 460,000 (11-13% - HIGHEST)

Pennsylvania Marijuana Qualifying Conditions

24 serious medical conditions:

- ALS (Amyotrophic Lateral Sclerosis)

- Anxiety disorders (most common - 300,000+ of 460K patients)

- Autism spectrum disorder

- Cancer (including remission therapy)

- Chronic hepatitis C

- Crohn's disease

- Damage to nervous tissue of CNS with intractable spasticity

- Dyskinetic and spastic movement disorders

- Epilepsy

- Glaucoma

- HIV/AIDS

- Huntington's disease

- Inflammatory bowel disease (IBD)

- Intractable seizures

- Multiple sclerosis (MS)

- Neuropathies

- Opioid use disorder (when conventional treatments ineffective)

- Parkinson's disease

- Post-traumatic stress disorder (PTSD)

- Severe chronic or intractable pain (includes fibromyalgia, chronic back pain)

- Sickle cell anemia

- Terminal illness

- Tourette syndrome

- Neurodegenerative diseases

Broad qualifying conditions enable wide access while maintaining medical program integrity.

Pennsylvania Marijuana Possession Limits

Medical patients (with valid PA medical card):

- 30-day supply as determined by dispensary pharmacist

- Alternative measure: 192 medical marijuana units per 90 days (max 64 units = 30-day supply at once)

- Must keep product in original packaging

- Must have valid Pennsylvania medical marijuana ID card

Recreational (ILLEGAL statewide):

- ANY amount = criminal misdemeanor offense

- First offense under 30g: Eligible for probation + drug education instead of jail

- Over 30g: Misdemeanor, up to 1 year jail + $5,000 fine

Pennsylvania marijuana decriminalization (6 cities only):

- Philadelphia (2014): Up to 30g (1.06 oz) = $25 civil fine (NOT criminal)

- Pittsburgh (2015): Up to 30g = $25 fine

- York (2017): Up to 30g = $100 fine

- Lancaster (2018): Up to 28g (1 oz) = $25-75 fine

- Erie (2018): Up to 30g = $25 fine

- Harrisburg (2019): Up to 30g = $75 fine

Outside these 6 cities: ANY recreational possession = criminal record

Pennsylvania marijuana arrests: ~11,000 annually statewide (2023), though decriminalization cities saw 90%+ arrest reductions after policy changes

Pennsylvania Home Grow

Answer: ILLEGAL for both medical and recreational

Details:

- NO home cultivation permitted in Pennsylvania (medical or adult-use)

- Even one plant = felony cultivation charge

- Penalties: 36 months to 5 years prison + $15,000 fine

- Medical patients MUST purchase from licensed dispensaries only

Comparison:

- Unlike Michigan (12 plants), Colorado (6-12 plants), Oregon (4 household)

- Similar to New Jersey, Illinois restrictions

SB 76 (proposed): Would allow medical home cultivation - not yet passed

CBDT impact: Lack of home grow channels ALL medical consumption through dispensaries = higher compliance, better tax capture. But forces low-income/rural patients to pay retail prices or use illicit market.

Pennsylvania Marijuana Prices

Answer: HIGHEST MEDICAL PRICES IN THE NATION (ironic for largest medical program)

Medical retail prices:

- Flower: $10-15/gram (vs. $3-7/gram other states)

- Pre-rolls: $12-20/each

- Concentrates: $50-90/gram

- Cartridges: $40-80/0.5g

Why so expensive?:

- High licensing fees ($200,000 grower/processor, $30,000 per dispensary location)

- 5% tax at wholesale (grower/processor → dispensary)

- Limited competition despite 188 dispensaries (vertical integration restrictions)

- No recreational market creating price pressure

- Federal 280E tax penalty forcing 15-22% markup

Comparison to recreational markets:

- Oregon: $3.75/gram recreational

- Michigan: $5-7/gram recreational

- Illinois: $12-18/gram recreational (also expensive)

- Pennsylvania medical: $10-15/gram (MORE than many recreational markets)

Border bleed impact: Cheaper recreational in NJ ($8-10/gram), OH ($8-11/gram), MD ($9-12/gram) drives PA residents across state lines

Pennsylvania Medical Marijuana Dispensaries

188 operational dispensaries statewide (as of March 2025)

Structure:

- ~50 dispensary licenses × up to 3 locations each = 150+ locations

- Additional grower/processor co-located dispensaries

- Concentrated in Philadelphia metro, Pittsburgh, Harrisburg-Lancaster corridor

- Rural areas less served but improving

Products allowed:

- Flower (for vaporization only - smoking PROHIBITED)

- Pills/capsules

- Oils/tinctures

- Topicals (gels, creams, ointments)

- Concentrates/extracts

- Forms appropriate for vaporization/nebulization

- NOT allowed: Edibles (cookies, candies) - bill introduced 2022 to allow, not yet passed

Purchase limits: 30-day supply at a time, cannot purchase more until patient has less than 7-day supply remaining

Out-of-state cards: NO reciprocity - Pennsylvania medical marijuana cards ONLY

Pennsylvania Marijuana DUI

Answer: ZERO TOLERANCE PER SE LAW - ANY detectable THC = DUI, medical patients NOT exempt

Current law (most controversial aspect of PA program):

Pennsylvania marijuana DUI law:

- 1 nanogram/milliliter (ng/mL) THC in blood = automatic DUI (highest tier offense)

- Medical marijuana cardholders get NO exemption (Commonwealth v. Dabney, 2017)

- THC detectable days or weeks after use when person is NOT impaired

- Same penalties as alcohol DUI (fines, jail, license suspension)

- 460,000 medical patients technically "DUI 24/7/365" if using medication regularly

Pennsylvania marijuana employment: Medical patients can be arrested for DUI while driving to/from work even when not impaired

Example: Patient uses medical marijuana Sunday evening for chronic pain. Monday morning feels completely normal, drives to work. Pulled over for broken tail light. Officer sees medical marijuana card in wallet during ID check. Field sobriety test + blood draw. THC still in system from Sunday. DUI conviction despite zero impairment.

This happens to Pennsylvania medical patients regularly.

Proposed reforms (bipartisan support, not yet passed):

- HB 983/SB 63 (2025): Would require proof of actual impairment (not just THC presence) for medical patients

- HB 983: Removes strict liability provision for medical marijuana

- Actual impairment still illegal, but trace amounts alone insufficient for conviction

Comparison to other states:

- Colorado/Washington: 5 ng/mL rebuttable presumption (fairer)

- Montana: 5 ng/mL threshold

- Oklahoma: Per se law but working on reforms

- Pennsylvania: 1 ng/mL zero tolerance, medical NOT exempt (HARSHEST nationally)

CBDT impact: Some professionals avoid medical cards due to DUI/employment risk—prefer untraceable illicit sources despite wanting legal access

Pennsylvania Marijuana Employment

Answer: LIMITED protections - medical patients protected from discrimination BUT major exceptions

Act 16 employment protections:

- Cannot fire/refuse to hire "solely on basis" of medical marijuana patient status

- Applies to preemployment and random drug testing

- Protections for off-duty use with valid card

- Private right of action - can sue for discrimination (out-of-pocket + punitive damages)

MAJOR exceptions (employers CAN prohibit/fire):

- NO requirement to accommodate on-site use

- Federal contractors exempt (federal law supersedes state)

- Safety-sensitive positions: >10 ng/mL THC in blood serum = prohibited from:

- Operating chemicals requiring government permits

- Operating high-voltage electricity or public utilities

- Mining, work at heights, confined spaces

- Tasks employer deems "life-threatening"

- Employers can still discipline for actual impairment

Reality: "Blue collar" workers have weaker protections than desk jobs. Safety-sensitive industries can maintain zero tolerance.

Pittsburgh ordinance (unique):

- Bans pre-employment marijuana testing for medical cardholders (employers 5+ employees)

- Limits during-employment testing absent suspicion of impairment

- Exceptions: DOT-regulated, firearm carriers, collective bargaining agreements

HB 1766 (2025 - workers' compensation reimbursement):

- Would require workers' comp insurers to reimburse medical cannabis costs

- $250/month, $3,000/year caps

- Opioid alternative for chronic pain (injured workers)

- Pennsylvania would be FIRST STATE if passes

- Status: House Labor & Industry Committee review

Comparison:

- Better than federal law (zero protections)

- Weaker than New York (comprehensive protections)

- Similar to New Jersey (protections but limited accommodations)

Recreational Cannabis: ILLEGAL (But Proposed Multiple Times)

Status: NOT legal statewide, no adult-use sales, criminal penalties remain

Major 2025 legislative push:

House Bill 1200 (May 2025):

- Passed House 102-101 (party-line, Democrats) on May 7, 2025

- Would authorize state-run sales through PA Liquor Control Board (PLCB model - "Fine Wine & Cannabis Spirits")

- Personal cultivation allowed

- Expungement provisions for possession convictions

- 12% cannabis tax + 6% sales tax = 18% total

- Senate Law & Justice Committee tabled 7-3 (May 13, 2025) - KILLED

Gov. Shapiro budget proposals:

2025-2026 budget (February 2025):

- Legalization effective July 1, 2025, sales January 1, 2026

- 20% wholesale tax

- Projected revenue: $15.6M excise + $11.4M sales tax (first year)

- $1.3 billion over 5 years as market matures

- $10 million restorative justice initiatives

- $25 million small/diverse business fund

- Immediate expungement for possession-only offenses

Previous proposals:

- 2024-2025 budget: Similar legalization proposal, blocked by Senate

- Multiple House/Senate bills since 2019 - all blocked by Republican Senate

Senators Laughlin/Street bipartisan bills (SB 120/HB 1735/HB 20):

- Private retail model (unlike HB 1200's state-run stores)

- Cannabis Control Board oversight (new agency)

- Social equity provisions

- Licensing for existing medical + new entrants

- Similar to New Jersey/Ohio models

Public support: 67-70% of Pennsylvanians support legalization (February 2025 polling, includes majority of Republicans)

Challenges:

- Republican Senate opposition: Health concerns, prefer federal resolution, cultural opposition

- Budget crisis creates urgency ($1.6B deficit, $250M+ cannabis revenue appealing)

- Border bleed: Estimated 60% of NJ/NY/MD border dispensary customers from PA = political pressure

- All surrounding states legal (except West Virginia) = policy failure evidence

Timeline: Possible late 2025 or 2026 if:

- Budget crisis worsens ($2B+ deficit forces action)

- Federal Schedule III rescheduling occurs (removes primary excuse)

- 2026 elections flip Senate Democratic or reduce GOP majority

- Border-district Republicans feel constituent pressure

What Pennsylvania Gets Right: Medical Market Excellence

Pennsylvania's medical program demonstrates competence—creating solid foundation for adult-use transition.

Massive Medical Participation

460,000 active patients = 11-13% of adult population - HIGHEST medical participation rate nationally

Why Pennsylvania's medical program succeeds:

- Broad qualifying conditions (24 serious medical conditions including anxiety, chronic pain)

- Accessible certification (telehealth available, competitive doctor pricing $99-249)

- Reasonable state fee ($50/year, waivable for low-income)

- Statewide dispensary access (188 locations, minimal fragmentation)

Anxiety disorders alone: 300,000+ of 460,000 patients (65%) certified for anxiety

This demonstrates:

- Consumer demand exists (11-13% adult population willing to navigate medical program)

- Medical pathway serves subset well (but leaves 1+ million adult consumers in illicit market)

- Pennsylvania has cannabis culture ready for adult-use expansion

Professional Regulatory Infrastructure

Pennsylvania Department of Health built sophisticated oversight:

- Seed-to-sale tracking (all product tracked cultivation → sale)

- Mandatory testing at approved laboratories (potency, pesticides, heavy metals, microbials, residual solvents)

- Quality control standards exceeding many states

- Patient registry and certification system (secure, professional)

- Practitioner oversight (doctors must be approved, maintain continuing care)

Result: Consumer confidence high. Pennsylvania medical cannabis trusted for safety and consistency.

Comparison: Pennsylvania avoided California's gray market chaos, New York's regulatory dysfunction, Illinois' corruption concerns.

Minimal Geographic Fragmentation

Unlike California's disaster (61% of jurisdictions ban retail):

- State law preempts most local bans

- Municipalities can regulate zoning, cannot prohibit outright

- 188 dispensaries operate statewide: Philadelphia to Pittsburgh, Erie to Scranton

Dispensary density: 1.4 per 100,000 residents (low for adult-use, adequate for medical)

Geographic coverage:

- Philadelphia metro: ~60-75 dispensaries (good density)

- Pittsburgh metro: ~30-40 dispensaries (adequate)

- Harrisburg-Lancaster corridor: ~25-35 dispensaries

- Rural areas: Less served but improving

CBDT significance: State preemption prevents fragmentation penalty. Pennsylvania maintains this for adult-use = major advantage over California, Massachusetts (initial), New York.

Rapid Infrastructure Development

Pennsylvania launched medical sales February 2018. Within 7 years:

- $7.68 billion cumulative sales (2018-2024)

- 188 operational dispensaries (from zero)

- 460,000+ patients enrolled (from zero)

- 32 grower/processor licensees (professional supply chain)

- 25,000+ jobs created (cultivation, retail, ancillary)

Few states achieved this scale in medical-only programs. Pennsylvania's infrastructure readiness = competitive advantage for adult-use transition.

Comparison: Maryland launched adult-use in 90 days using medical infrastructure. Pennsylvania could replicate—faster than New York's 21-month delay.

What Holds Pennsylvania Back: Medical-Only Trap and Policy Gaps

Despite medical success, Pennsylvania faces structural barriers preventing market optimization.

Barrier #1: Medical-Only Limitation Creates Massive Illicit Market

The core problem: Pennsylvania's program serves diagnosed patients only

Market reality:

- Estimated 1.5-2 million adult Pennsylvanians consume cannabis regularly

- Only 460,000 are legal medical patients (23-31% of total consumers)

- 1+ million remain in illicit market or cross state lines

Why non-patients stay illicit:

- Don't have qualifying medical conditions (or unwilling to obtain dubious diagnosis)

- Don't want medical record of cannabis use (employment, insurance concerns)

- Find medical card process burdensome ($149-299 cost, annual renewal, doctor visits)

- Can access cheaper illicit cannabis or cross state line to NJ/OH/MD for legal adult-use

Result: Medical program—even largest in nation—captures only ~60-65% of total Pennsylvania cannabis consumption

Barrier #2: Highest Medical Prices in Nation Drive Border Bleed

Pennsylvania medical marijuana prices: $10-15/gram flower, $50-90/gram concentrates

Comparison to neighboring RECREATIONAL markets:

- New Jersey recreational: $8-10/gram (13% tax)

- Ohio recreational: $8-11/gram (10% + local)

- Maryland recreational: $9-12/gram (9% + local)

Pennsylvania MEDICAL costs MORE than neighboring RECREATIONAL

Why: High licensing fees + 5% wholesale tax + federal 280E penalty forcing 15-22% markup + limited competition

Border bleed estimate:

- 120,000-200,000 Pennsylvania consumers regularly purchase out-of-state

- $144-320 million annual spending in neighboring states

- $35-80 million tax revenue collected by NJ/MD/OH/NY instead of Pennsylvania

- 60% of border dispensary customers from Pennsylvania (Governor Shapiro citing industry reports)

The absurdity: Pennsylvania medical patients pay $12/gram taxed + medical card fees while recreational users drive to NJ for $9/gram untaxed (for them).

Barrier #3: Home Cultivation Prohibition Forces Retail Dependence

Pennsylvania home grow: ILLEGAL (even for medical patients)

Impact:

- Low-income patients cannot reduce costs through personal cultivation

- Rural patients in underserved areas have limited options (expensive dispensary or illicit market)

- Prohibition channels ALL medical use through retail = good for tax revenue, bad for patient access

Research shows: Home cultivation complements retail rather than competes. Most consumers prefer retail convenience at Pennsylvania's current prices. But 4-6 plant limits serve:

- Budget-conscious medical patients (chronic conditions, daily use)

- Rural residents (nearest dispensary 45+ minutes)

- Personal freedom principle (43 of 50 legal states allow home grow)

Comparison:

- Michigan: 12 plants allowed, 85% legal market share (home grow didn't hurt)

- Colorado: 6-12 plants allowed, 84% legal share

- Oregon: 4 plants allowed, 82% legal share

- Pennsylvania: 0 plants allowed, ~60-65% legal share (medical-only)

Barrier #4: Zero Tolerance DUI Law Creates 460,000 "Criminals"

Pennsylvania marijuana DUI: 1 ng/mL THC = automatic DUI, medical patients NOT exempt

The catastrophe: 460,000 medical patients using legally prescribed medication are technically "DUI 24/7/365" because THC remains detectable days/weeks after use

Real consequences:

- Patients arrested driving to work days after evening medication use

- No impairment required—any detectable THC sufficient for conviction

- Medical card in wallet = probable cause for DUI investigation (some officers)

- Same penalties as alcohol DUI (jail, fines, license suspension, employment consequences)

HB 983/SB 63 reform bills: Would require proof of actual impairment for medical patients—bipartisan support but not yet passed

Why this matters for legalization: Some professionals avoid medical cards due to DUI risk, preferring untraceable illicit sources. Zero tolerance law actively pushes people AWAY from legal market.

Barrier #5: Border State Competition Pennsylvania Cannot Match (While Illegal)

Five legal neighbors create competitive disadvantage:

New Jersey (18 miles from Philadelphia):

- Adult-use legal since April 2022

- 13% total tax burden (vs. PA medical effective 25-30% with licensing fees/280E)

- Lower prices than PA medical

- Philadelphia-area residents routinely cross Delaware River

Ohio (90 minutes from Pittsburgh):

- Adult-use launched November 2023

- 10% excise + local taxes

- Competitive pricing ($8-11/gram)

- Pittsburgh/Western PA access

Maryland (adjacent south-central PA):

- Adult-use legal since July 2023

- 9% + local taxes

- York, Lancaster, Harrisburg-area access

New York (northern tier):

- Adult-use legal since December 2022

- 13% state tax

- Scranton, Wilkes-Barre, Erie-area access

Delaware (Philadelphia suburbs):

- Adult-use legal since April 2023

- 15% total tax

- Southeastern PA access

The economic hemorrhage:

- Estimated $300-400 million annually flowing OUT of Pennsylvania

- $60-100 million in lost tax revenue

- Pennsylvania subsidizing neighbors' budgets while arresting own residents

As long as Pennsylvania remains illegal: This border bleed ACCELERATES as neighboring markets mature.

Barrier #6: Federal 280E and SAFE Banking (Brief Summary)

Federal IRC Section 280E prevents Pennsylvania medical businesses from deducting ordinary expenses:

- Forces 40-70% effective federal tax rates

- Requires 15-22% price markup to remain viable

- Makes PA medical MORE expensive than neighboring recreational

- Schedule III rescheduling would eliminate 280E, enable 12-18% price reductions

SAFE Banking Act absence forces cash operations:

- Security costs $50K-180K annually per location

- Consumer friction (cash-only reduces transactions 15-22%)

- No commercial lending (expansion capital inaccessible)

- SAFE Banking passage would enable cards, reduce crime, improve competitiveness

Pennsylvania cannot optimize without federal reform - even with perfect state policy, federal barriers create 15-20% competitive disadvantage vs. theoretical maximum.

Framework Assessment: Medical Success, Recreational Failure

The CBDT Framework reveals Pennsylvania's current position and optimization potential.

Current Performance: ~60-65% Legal Market Share (Medical-Only)

Estimate: 60-65% of total Pennsylvania cannabis consumption occurs through legal medical program

Transaction share: Estimated 70-75% (percentage obtaining at least SOME supply legally - many patients supplement with illicit)

Volume share: 60-65% (accounting for heavy user behavior - some heavy users stay fully illicit or cross borders)

This represents mid-tier performance comparable to:

- Illinois (55-60% with adult-use but high taxes)

- New Jersey (60-65% with adult-use but slow rollout)

- Washington (60% with adult-use, price pressure)

Pennsylvania UNDERPERFORMS despite:

- Largest medical program (460K patients, 11-13% participation)

- Sophisticated infrastructure (7 years, $7.68B sales)

- Strong regulatory culture

Why? Medical-only limitation + highest prices nationally + 5 legal neighbors = inevitable failure

CBDT Variable Scoring (Current Medical-Only)

Price Competitiveness (4× weight): POOR (0.35/1.0)

- Medical costs $10-15/gram (highest nationally)

- Neighboring recreational $8-11/gram (cheaper AND legal for adults)

- Illicit Pennsylvania ~$8-11/gram

- Legal costs 20-40% MORE than illicit OR border recreational

- Federal 280E forces markup

Access Density (1× weight): MODERATE (0.55/1.0)

- 188 dispensaries for 13 million = 1.4 per 100K (low)

- Medical-only limits addressable market

- Urban areas adequately served (Philly, Pittsburgh)

- Rural areas underserved

- No home cultivation option

- Statewide delivery not mandated

Safety/Quality (1.2× weight): EXCELLENT (0.90/1.0)

- Rigorous testing requirements

- Seed-to-sale tracking

- Quality control standards

- Consumer confidence high

- Professional laboratory oversight

Convenience (1× weight): POOR (0.40/1.0)

- Cash-only or limited banking (SAFE Banking absence)

- Medical card requirement creates barrier

- Annual recertification burden

- Limited delivery

- Smoking prohibited (vaporization only)

Enforcement (0.6× weight): MODERATE (0.60/1.0)

- Active medical program enforcement

- 11,000+ annual arrests for illicit possession

- Border state enforcement impossible (interstate commerce)

- Sufficient to protect medical market integrity

- Insufficient to prevent border bleed

Market Fragmentation Penalty: MINIMAL (-0.08/1.0)

- State preemption prevents most local bans

- 188 dispensaries statewide coverage

- Some rural gaps but limited compared to California (61% local bans)

Summary: Pennsylvania's price competitiveness failure (0.35/1.0 on 4× weight variable) ensures medical market underperformance despite excellence in safety/quality. Medical-only limitation + highest prices + border competition = 60-65% ceiling.

Residual Illicit Demand (35-40%)

Who comprises Pennsylvania's illicit market?

- Adult consumers without medical cards (25-30%):

- 1-1.3 million adults who consume but don't qualify or don't want medical documentation

- Use traditional illicit market ($8-11/gram, untaxed, no medical record)

- Border recreational shoppers (5-8%):

- 120K-200K Pennsylvania residents purchasing in NJ/OH/MD/NY/DE

- Prefer legal recreational over illegal medical process

- $144-320M annual spending out-of-state

- Medical patients supplementing (2-4%):

- Some medical patients buy partial supply at dispensary (for legitimacy/quality)

- Supplement with cheaper illicit to reduce costs (high PA medical prices)

- Price-sensitive heavy users (3-5%):

- Cannot afford $10-15/gram medical prices

- Use illicit market exclusively ($8-11/gram)

Predicted Market Trajectories

Scenario 1: Optimized Adult-Use (Federal Reform + Evidence-Based Policy)

Requirements:

- Adult-use legalization (2026-2028 timeframe)

- 18-22% total tax burden (competitive with neighbors)

- Leverage existing medical infrastructure (188 dispensaries convert immediately)

- Add 40-80 new licenses (social equity priority, geographic gaps)

- Statewide delivery mandate

- Home cultivation (4-6 plants household)

- Automatic expungement (possession convictions)

- Federal Schedule III rescheduling (280E elimination)

- SAFE Banking Act passage

Predicted outcomes (36-48 months):

- Legal market share: 75-82% (transaction share ~88%, volume share 75-82%)

- Combined market size: $2.8-3.4B annually (medical + adult-use)

- State tax revenue: $500-680M annually (vs. current $87M medical)

- Jobs: 40,000-55,000 total (vs. current 25,000)

- Illicit market: Reduced from $900M-1.8B to $350-550M (70%+ reduction)

- Border bleed: Nearly eliminated (Pennsylvania prices competitive)

Price impact:

- 280E elimination enables 12-18% price reductions

- Legal flower: $6-9/gram (vs. current $10-15/gram medical)

- Competitive with New Jersey ($8-10/gram), Ohio ($8-11/gram)

- Legal costs LESS than illicit ($8-11/gram) OR equal

Comparable performance:

- Michigan: 85% legal share (best Northeast)

- Colorado: 84% (with federal reform could reach 88%)

- Massachusetts: 77% legal share

This represents best-case Pennsylvania: Learning from 5 neighbors' mistakes, leveraging medical infrastructure, federal support enabling price competitiveness.

Scenario 2: Failed Policy (High Taxes + Over-Regulation)

Policy design:

- High tax: 26-30% total (Gov. Shapiro initial 20% wholesale + markups)

- State-run model: "Fine Wine & Cannabis Spirits" (HB 1200 approach)

- Abandon medical infrastructure (political favoritism for new licenses)

- Limited delivery, no home cultivation

- Bureaucratic delays (New York model)

- 280E remains (no federal reform)

Predicted outcomes:

- Legal market share: 55-62%

- Combined market: $2.0-2.4B annually

- Tax revenue: $520-720M annually (high rate, smaller base = similar to optimized revenue but worse outcomes)

- Jobs: 15,000-20,000

- Illicit market: $800M-1.2B (persistent)

- Border bleed: Continues (PA prices still uncompetitive)

Comparable to:

- Illinois: 55-60% (high taxes, over-regulation)

- New Jersey: 60-65% (slow rollout, MSO consolidation)

This represents policy failure: Pennsylvania legalizes but repeats neighbors' high-tax mistakes.

Scenario 3: Status Quo (Medical-Only Continues)

Current trajectory:

- No adult-use legalization through 2027+

- Medical program continues growing modestly

- Border bleed accelerates as neighbors mature

- 280E/SAFE Banking remain unresolved

Predicted outcomes (2025-2030):

- Legal market share: 58-62% (slight growth from medical expansion, offset by border competition)

- Medical sales: $1.9-2.2B annually

- State tax revenue: $95-110M annually (5% wholesale tax)

- Border bleed: $400-600M annually to neighbors

- Lost tax revenue: $80-120M annually

- Arrests: 11,000+ annually continue

The opportunity cost vs. optimized scenario:

- $410-570M in potential tax revenue sacrificed annually

- 20,000-30,000 potential jobs foregone

- $3-6 billion in legal market activity lost over 10 years

- Interstate trafficking continues enriching neighbors

Policy Recommendations: When Pennsylvania Legalizes

When—not if—Pennsylvania legalizes, these evidence-based policies maximize outcomes.

Priority #1: Competitive Tax Structure (18-22% Total Max)

Recommendation:

- State excise: 12-15%

- State sales tax: 6% (existing rate)

- Local option: Maximum 2% cap

- Total: 18-22%

Rationale: Revenue optimization through volume (market share), not rates.

Pennsylvania must compete with:

- New Jersey: 13% total

- Ohio: 10% + local

- Maryland: 9% + local

Gov. Shapiro's 20% wholesale tax: Reasonable starting point but monitor total effective consumer burden. Wholesale taxes can obscure retail prices if pass-through unpredictable.

Better: Transparent retail-level excise tax + sales tax + limited local option.

Tax revenue comparison:

- High-tax failure (28% total, 55% market share): $520-580M annually

- Optimized (20% total, 78% market share): $600-680M annually

- More revenue at lower rates through higher volume

Priority #2: Leverage Medical Infrastructure (90-180 Day Launch)

Recommendation:

- Existing 188 dispensaries: Automatic adult-use authorization within 90 days

- Existing grower/processors: Expand to adult-use production immediately

- New licenses: Add 40-80 dispensaries (social equity priority, geographic gaps)

- Final density: 220-260 dispensaries statewide

- Timeline: Maryland model (90-180 days), NOT New York's 21 months

State-run vs. private debate:

HB 1200 proposed state-run model ("Fine Wine & Cannabis Spirits"). Arguments:

- FOR: Prevent MSO consolidation, state revenue capture, rural service mandate

- AGAINST: Abandons $7.68B infrastructure investment, 2-3 year delays, unprecedented nationally, legal exposure

Better solution: Hybrid approach

- Medical dispensaries convert (private, immediate)

- New licenses competitive (social equity priority)

- State regulatory oversight (maintain PA thoroughness)

- Consider state wholesale (PA grows, private retail) if revenue capture desired

Priority #3: Statewide Access Without Fragmentation

Recommendation:

- State preemption of local bans (preserve medical precedent)

- Municipalities regulate zoning, cannot prohibit

- Statewide delivery mandate (rural access critical)

- Rural cultivation incentives (agricultural economic development)

Prevent California disaster (61% local bans = 12-18 pp market share penalty)

Priority #4: Home Cultivation Rights (4-6 Plants)

Recommendation:

- Adult-use: 4-6 plants per household

- Medical: 6-8 plants per patient

- Not just medical (SB 76) but for all adults

Research shows: Home cultivation complements retail, doesn't compete at Pennsylvania's prices. Serves budget-conscious, rural residents instead of illicit market.

43 of 50 legal states allow home cultivation - Pennsylvania outlier.

Priority #5: DUI Law Reform (HB 983/SB 63)

Pass HB 983/SB 63:

- Require proof of actual impairment for medical patients

- Remove strict liability for trace THC amounts

- Maintains DUI penalties for actual impairment

Current zero tolerance law actively pushes consumers AWAY from legal market due to employment/legal risk.

Priority #6: Employment Protections Expansion

Strengthen Act 16 protections:

- Expand safety-sensitive definitions (current >10 ng/mL reasonable)

- Prohibit discrimination based solely on off-duty use

- Pass HB 1766 (workers' comp reimbursement for medical cannabis)

Priority #7: Social Equity and Expungement

Automatic expungement:

- All cannabis possession convictions (any amount)

- Immediate upon legalization

- Estimated 150,000-250,000 records eligible

- Model: Illinois (770,000+ records expunged)

Social equity licensing:

- Preference: Prior convictions, high-arrest areas, minority-owned, PA residents

- $50-75M capital fund (grants, low-interest loans, technical assistance)

- Avoid Illinois mistakes (inadequate funding → MSO control)

Restorative justice:

- 25-30% of cannabis tax revenue to communities with high cannabis arrest rates

- Job training, education, small business development

- Measurable outcomes tracked annually

Priority #8: Federal Reform Advocacy

Pennsylvania Congressional Delegation (18 House, 2 Senate) should champion:

- Schedule III rescheduling: Eliminates 280E, enables price competitiveness

- SAFE Banking Act: Public safety (reduces cash crime), economic development

- Conservative case: Federal reform isn't mandate to legalize—it's removing federal barriers to state choice

Comparison to Neighboring States

Pennsylvania's market position depends on learning from 5 neighbors' experiences.

High-Performing Neighbor: Michigan

Michigan (opened November 2019):

- Legal share: 85% (best in Northeast/Midwest)

- Tax burden: 16% total (10% excise + 6% sales)

- Prices: $5-7/gram flower

- Strategy: Competitive pricing, rapid licensing, statewide delivery

Why Michigan succeeds:

- Moderate taxes (price competitive)

- Fast rollout (licensed medical dispensaries first, avoided delays)

- Home cultivation allowed (12 plants - complements retail)

- Enforcement intensity (protects legal market)

What Pennsylvania should copy:

- Tax structure (18-22% competitive with Michigan's 16%)

- Infrastructure leverage (use medical foundation)

- Delivery mandate (serves all residents)

Mid-Performing Neighbors: New Jersey, Ohio

New Jersey (opened April 2022):

- Legal share: 60-65%

- Tax burden: 13% (among lowest)

- Why underperforms: Slow rollout, limited dispensaries initially, proximity to NY gray market

Lesson: Low taxes alone don't guarantee success. Infrastructure density + rollout speed matter.

Ohio (opened November 2023):

- Legal share: 68-72% (early estimate)

- Tax burden: 10% + local

- Why performing well: Competitive pricing, learned from neighbors, faster than NJ rollout

Lesson: Recent legalizers perform better by learning from mistakes. Pennsylvania has 5 neighbors' data.

Struggling Neighbors: Maryland, New York

Maryland (opened July 2023):

- Legal share: 65-70%

- Tax burden: 9% + local (very low)

- Why moderate: Medical transition successful BUT MSO consolidation, Delaware/Virginia competition

New York (opened December 2022):

- Legal share: 30-35% (WORST major market)

- Why catastrophic failure: 21-month delays, insufficient retail density, enforcement abdication (tolerated unlicensed shops)

What Pennsylvania MUST avoid:

- New York delays (21 months legalization → sales)

- New York fragmentation (retail authorization chaos)

- Under-enforcement (protect legal market from illegal competition)

Pennsylvania's Opportunity

Advantages Pennsylvania has that neighbors lacked:

- Larger medical infrastructure than NJ or OH started with (188 vs. ~30-50)

- More regulatory experience than OH (recent legalizer)

- Better geography than NY (no NYC-scale gray market)

- More functional government than NY (avoid regulatory chaos)

- Five neighbors' data (unprecedented learning opportunity)

Target performance:

- Match or exceed Michigan (75-85% legal share)

- Significantly outperform NJ (60-65%), MD (65-70%), NY (30-35%)

- Capture Pennsylvania consumers currently crossing state lines

- Attract border tourism from West Virginia (remaining prohibition neighbor)

Pennsylvania could become Northeast's best adult-use market by synthesizing 5 neighbors' lessons.

Conclusion: The $1.3 Billion Question

Pennsylvania built America's most successful medical-only cannabis program: 460,000 patients (highest participation rate nationally), $1.73 billion annual sales (sixth-largest market despite medical-only), $7.68 billion cumulative sales, and professional regulatory infrastructure that took seven years to perfect.

Yet Pennsylvania hemorrhages $300-400 million annually to five neighboring states that legalized adult-use while the Keystone State arrests 11,000+ residents for cannabis possession.

The numbers are undeniable:

- 70% of Pennsylvanians support legalization

- 60% of border dispensary customers are from Pennsylvania

- $1.6 billion budget deficit demands new revenue

- $1.3 billion over 5 years available through legalization (Gov. Shapiro projection)

- All surrounding states legal except West Virginia

The political stalemate is temporary:

- Federal Schedule III rescheduling likely 2025-2027

- Border state revenue data becomes undeniable

- Budget crisis intensifies ($2B+ deficit possible)

- 2026 elections may shift Senate composition

- Generational change favors legalization

When—not if—Pennsylvania legalizes, the state possesses unique advantages:

- 188 operational dispensaries ready for immediate conversion

- 32 grower/processors with proven supply chains

- 460,000 proven customers validating demand

- Five neighbors' experiences showing what works and what fails

- Geographic concentration (92% population in 7 metros) reducing infrastructure needs

The CBDT Framework reveals Pennsylvania's potential: With optimized policy (18-22% taxes, infrastructure leverage, home cultivation, statewide delivery) and federal reform, Pennsylvania could achieve 75-82% legal market share—outperforming most neighbors despite later entry.

The failure scenario is equally clear: High taxes (26-30%), state-run monopoly displacing medical infrastructure, New York-style delays, and continued federal 280E penalties would ensure Pennsylvania replicates Illinois' mistakes (55-60% legal share).

The choice Pennsylvania faces:

Status quo: Continued medical-only prohibition = $80-120M annual revenue lost to neighbors, 11,000+ arrests continuing, 1+ million adults in illicit market, political dysfunction rewarded

Optimized legalization: Evidence-based policy = $500-680M annual tax revenue, 40,000-55,000 jobs, 75-82% legal market share, border bleed eliminated, automatic expungement for 150,000-250,000 residents

Failed legalization: High-tax over-regulation = $520-720M revenue (similar to optimized) BUT only 55-62% legal share, persistent illicit market, continued arrests, missed opportunity

Pennsylvania doesn't need to guess at optimal policy—New Jersey, Maryland, Ohio, New York, and Michigan already demonstrated it. The data is unambiguous: moderate taxes (18-22%), infrastructure leverage, rapid rollout, statewide access, home cultivation = 75-85% legal share. High taxes, delays, fragmentation, state monopolies = 55-65% failure.

The question before Pennsylvania legislators:

Will you legalize cannabis to optimize public health, maximize tax revenue, create tens of thousands of jobs, end mass arrests, and serve 70% of voters who support reform?

Or will you maintain prohibition while neighboring states collect Pennsylvania's money, Pennsylvania residents get arrested for behavior legal 20 minutes away, and the largest medical cannabis market in America remains trapped by political gridlock?

The framework provides the roadmap. The voters provided the mandate. Five neighbors provided the blueprint. Governor Shapiro provided the budget proposal. The Democratic House provided the votes.

Only the Republican Senate stands between Pennsylvania and $1.3 billion in revenue, 40,000-55,000 jobs, and evidence-based cannabis policy that could make the Keystone State the Northeast's model market.

The $1.3 billion question is: How long will prohibition's last island hold out while surrounded by legal states on every side?

CBDT Framework Citation

This analysis applies the Consumer-Driven Black Market Displacement Framework:

The Silent Majority 420, "Consumer-Driven Black Market Displacement (CBDT) Framework: A Behavioral-Utility Heuristic for Illicit-to-Legal Market Transition," Zenodo, 2025. DOI: 10.5281/zenodo.17593077

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Related State Analyses: Arkansas | Wyoming | Maine | Indiana

The Silent Majority 420 is an independent cannabis policy analyst. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0