Texas Cannabis Market Analysis: The Lone Star State's $8+ Billion Question

Everything's bigger in Texas—including the cannabis market that prohibition can't eliminate.

The Silent Majority 420 | November 2025

The Texas Paradox: A $13 Billion Cannabis Economy Nobody Admits Exists

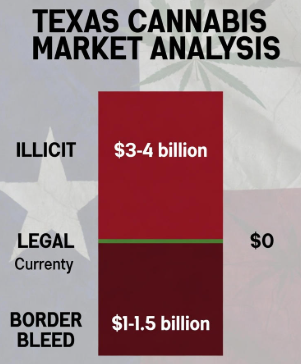

Texas maintains one of America's strictest cannabis prohibition regimes while simultaneously hosting the nation's largest unregulated cannabis marketplace. The state arrested 26,602 residents for marijuana possession in 2024—more than any other state—yet operates an $5.5 billion legal hemp-derived THC industry alongside an estimated $4.2 billion illicit traditional cannabis market. Add Texas's expanding medical program, and the Lone Star State's total cannabis economy approaches $13 billion annually.

This creates an absurd reality: Texans can legally purchase intoxicating Delta-9 THC gummies at gas stations, but face arrest and incarceration for possessing traditional cannabis flower. The state operates 8,500+ hemp dispensaries generating 53,300 jobs, while simultaneously prosecuting residents for a nearly identical product. Law enforcement made more marijuana arrests in Texas than California, despite California's 10 million more residents and full adult-use legalization.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Texas's extraordinary potential: IF the state legalizes adult-use cannabis with evidence-based policy design, Texas could capture 80-88% legal market share within 36-48 months—exceeding every current legal state except Oregon.

Texas possesses structural advantages rivals can't match:

- Scale: 30 million residents create $8-10 billion potential adult-use market

- Geographic concentration: Dallas-Fort Worth, Houston, San Antonio, and Austin metros contain 60%+ of population

- Existing infrastructure: 8,500 hemp retailers provide instant distribution network

- Border insulation: No neighboring states with adult-use programs (Oklahoma, New Mexico, Arkansas, and Louisiana have limited medical programs only)

- Conservative fiscal culture: Revenue optimization likely trumps ideological prohibition once legalization occurs

- Clean slate: No legacy medical program complications, no interstate competition pressure

But this outcome requires three conditions: Texas must legalize (politically uncertain), federal reform must occur (Schedule III + SAFE Banking), and the state must implement evidence-based policy rather than replicating Illinois' high-tax failure.

Current trajectory: Texas legalization probability remains LOW short-term (2025-2027), MODERATE medium-term (2028-2032 medical, 2033-2037 adult-use), HIGH long-term (2038+). The state's Republican supermajority maintains prohibition despite 60%+ public support for medical cannabis and 50%+ support for adult-use legalization.

The framework prediction: IF Texas legalizes with optimized policy and federal reform by 2030, the state will achieve 80-88% legal market share by 2033, generating $1.6-2.0 billion in annual sales, $280-360 million in state tax revenue, and 18,000-24,000 direct jobs. The illicit market would collapse from $4.2 billion to $500-800 million within 48 months.

This represents the largest potential cannabis market transformation in U.S. history. Texas's prohibition isn't sustainable—it's just expensive.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy across diverse market conditions:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid regulatory crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—dominant variable): Legal market pricing relative to illicit alternatives

- Access density: Store availability per capita, delivery infrastructure, geographic coverage

- Safety and quality advantage: Testing standards, product consistency, brand reliability

- Convenience: Payment methods (cash vs. card), operating hours, friction reduction

- Enforcement intensity: Illicit supply interdiction, cultivation disruption

A sixth variable—market fragmentation—acts as a penalty, reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Market Status (2025): Prohibition Theater Masking Quasi-Legalization

Texas presents a unique cannabis landscape in 2025: official prohibition coexists with widespread legal and quasi-legal availability.

The Hemp Loophole: A $5.5 Billion "Legal" Market

The 2018 federal Farm Bill legalized hemp containing ≤0.3% THC by dry weight. Texas implemented enabling legislation in 2019, intending to create an agricultural fiber industry. Instead, manufacturers exploited a loophole: synthesizing intoxicating hemp-derived cannabinoids (Delta-8, Delta-9, Delta-10 THC) that produce effects virtually identical to traditional cannabis.

By 2025, this created a massive semi-regulated industry:

Market size: $5.5 billion annual revenue (Whitney Economics report, March 2025)

- Retail sales: $4.3 billion

- Manufacturing/wholesale: $1.2 billion

Business ecosystem:

- 8,500+ registered hemp dispensaries (more than all adult-use legal states combined)

- 53,300 employees

- 72% of businesses reporting profitability

- $268 million in estimated tax revenue

Products available: Delta-8 THC, Delta-9 THC (hemp-derived), Delta-10 THC, THC-O, HHC, and dozens of other synthesized cannabinoids sold in:

- Vape shops

- Gas stations

- Convenience stores

- Dedicated hemp retailers

- Online delivery

Regulatory gaps: While Texas requires Certificates of Analysis (COAs) from independent labs, the Department of State Health Services lacks enforcement capacity to verify product safety. Independent testing reveals:

- Products frequently exceed 0.3% THC limit

- Inconsistent dosing (labeled 10mg often contains 15-30mg)

- Heavy metal contamination in some products

- Pesticide residues

- Mold in poorly manufactured flower

Age restrictions: None until September 2025, when Governor Greg Abbott issued executive order requiring 21+ age verification—but only after Lt. Governor Dan Patrick's attempted blanket THC ban (SB 3) failed.

This quasi-legal market undermines any future regulated adult-use program: consumers already have widespread access to intoxicating THC products, making traditional legalization less urgent to voters while creating a powerful industry lobby opposing change.

The Traditional Illicit Market: $4.2 Billion and Persistent

Alongside the hemp market, Texas maintains one of America's largest traditional cannabis black markets:

Market size: $4.2 billion annually (New Frontier Data/GrowCola analysis)—representing 7% of total U.S. illicit cannabis sales, the highest of any non-legal state

Consumer base: Estimated 3.2-3.8 million regular cannabis users among Texas's 30 million residents (10.5-12.5% of adults)

Average spending: $1,100-1,300 annually per consumer

Why the illicit market persists despite hemp availability:

- Price: Illicit flower costs $6-10/gram vs. hemp-derived products at $15-25/gram equivalent

- Product familiarity: Traditional consumers prefer flower over synthesized cannabinoids

- Quality perception: Illicit flower often perceived as higher quality than lab-synthesized alternatives

- Selection: Illicit market offers strain variety hemp products can't replicate

- Distrust: Some consumers wary of synthesized cannabinoids' unknown long-term effects

Medical Program Expansion: The TCUP Transformation

Texas's Compassionate Use Program (TCUP), established 2015, historically served as one of America's most restrictive medical programs. House Bill 46, signed into law June 2025, dramatically expanded access:

Previous restrictions:

- Only 3 licensed dispensaries statewide

- Maximum 1% THC in products

- 8 qualifying conditions only

- No inhalation products (flower, vape) allowed

- Limited product forms

- ~4,000 active patients monthly (December 2024)

HB 46 reforms (effective 2025-2026):

- Licensing expansion: 15 total dispensaries (12 new licenses)

- THC increase: Up to 10mg per dosage unit (from 1% product limit)

- New qualifying conditions: Chronic pain, palliative care, hospice care, traumatic brain injury (TBI), spinal neuropathy, Crohn's disease, inflammatory bowel disease, degenerative disc disease

- Product forms: Patches, lotions, suppositories, approved inhalers, nebulizers, vaping devices added

- Satellite locations: Licensed dispensaries can operate satellite pickup locations in underserved regions

- Timeline: New regulations effective October 1, 2025; new licenses awarded December 2025 (9 licenses) and April 2026 (3 licenses)

Program administration: Texas Department of Public Safety, Regulatory Services Division manages TCUP through the Compassionate Use Registry of Texas (CURT), a secure physician-patient registry.

Impact projection: TCUP enrollment expected to grow from ~50,000 annual patients (2024) to 125,000-175,000 annually by 2027, generating $85-125 million in medical sales. However, this remains small compared to the hemp and illicit markets due to:

- High costs: Medical products often $80-120/gram THC equivalent

- Limited physician participation: Many doctors hesitant to prescribe

- Stigma: Patients reluctant to register in government database

- Accessibility: Even with 15 dispensaries, geographic coverage remains limited in rural areas

The Legislative Battle: 2025 Session Outcomes

Texas's 2025 legislative session (January-May) featured intense cannabis policy debates:

Failed adult-use legalization bills:

- HB 1208 (Rep. Jessica González): Comprehensive adult-use framework with 2.5-ounce possession, home cultivation (6 plants), 10% tax rate—never received committee hearing

- SB 335: Senate companion to HB 1208—died in committee

- HB 1763: Reduced penalties for possession—killed without hearing

- HJR 70 (Rep. Ron Reynolds): Constitutional amendment authorizing medical cannabis—killed without hearing

Failed decriminalization:

- HB 3242 (Rep. Joe Moody): One-ounce possession as civil violation (no jail, no arrest) + expungement mechanism—denied committee hearing despite passing House in 2023 session

The hemp ban fight: Lt. Governor Dan Patrick made banning hemp-derived THC his top 2025 priority:

- SB 3 (Sen. Charles Perry): Would have banned ALL hemp-derived THC products, including Delta-8, Delta-9, Delta-10, HHC—creating de facto prohibition of the $5.5 billion hemp industry

- Patrick's rationale: Hemp products "unsafe," exceed legal limits, marketed to children, undermine medical program

- Industry response: 14-hour public hearing with veterans, patients, business owners testifying about hemp benefits; economic analysis showing 40,000+ jobs at risk

- Result: SB 3 passed Senate, House refused to vote

- Governor Abbott veto: After SB 3 passed both chambers in special session, Abbott vetoed it, stating existing hemp industry provides value while acknowledging need for regulation

The compromise: Abbott issued executive order September 2025 directing state agencies to implement:

- Age verification (21+ only)

- Child-resistant packaging

- Potency limits (specific thresholds TBD)

- Enhanced testing and labeling requirements

- School/church setback restrictions

- Bans on vape products already implemented

This preserved the hemp industry while adding consumer protections—satisfying neither prohibitionists (Patrick) nor full legalization advocates.

Local decriminalization victories: Despite state-level gridlock, Texas cities achieved ballot initiative successes:

- Dallas (November 2024): 67% approved Dallas Freedom Act—no arrest/citation for ≤4 ounces possession, smell of cannabis not probable cause

- Bastrop (November 2024): 69.8% approved decriminalization

- Lockhart (November 2024): 68% approved decriminalization

- Prior cities with decriminalization: Houston, Austin, San Marcos, Killeen

State legal challenges: Texas Attorney General Ken Paxton sued multiple cities to block implementation. Texas Supreme Court sided with state in some cases, creating ongoing litigation over municipal authority to decriminalize substances prohibited under state law.

Economic context: Texas faced $2 billion budget shortfall in 2025. Lawmakers explicitly rejected cannabis legalization as revenue source despite neighboring Oklahoma generating $300+ million medical cannabis tax revenue and New Mexico adult-use program producing $150+ million annually.

Enforcement Reality: America's Arrest Leader

Texas maintained its position as the national leader in cannabis arrests in 2024:

Arrest statistics (FBI Crime Data Explorer, NORML analysis):

- 26,602 marijuana arrests (2024)—most of any U.S. state

- 97%+ for possession (not sales/trafficking)

- 30% of all Texas drug arrests were cannabis-related

- Arrests decreased from 35,000+ (2019) due to local decriminalization policies

Enforcement disparities (Texas Department of Criminal Justice data, ACLU analysis):

- African Americans: 30.2% of cannabis possession arrests (2017-2019)

- African American population: 12.9% of Texas residents

- Disparity ratio: Black Texans arrested 2.3× more than white Texans for cannabis possession

Penalties under Texas law (Texas Health and Safety Code Chapter 481):

- ≤2 ounces: Class B misdemeanor, up to 180 days jail, $2,000 fine

- 2-4 ounces: Class A misdemeanor, up to 1 year jail, $4,000 fine

- 4 ounces - 5 pounds: State jail felony, 180 days - 2 years prison

- 5-50 pounds: 2nd-degree felony, 2-20 years prison

- >50 pounds: Enhanced felony charges

Economic cost: Estimated $125-185 million annually in enforcement, prosecution, and incarceration costs for cannabis violations that are legal 200-300 miles away in New Mexico.

San Marcos case study: Ground Game Texas analysis showed decriminalization (2023-2024) reduced possession arrests 83%, saving city $444,150 in enforcement costs. Arrests dropped from 201 (2018) to 19 (2024) during policy implementation.

Texas's Structural Advantages: Hidden Strengths Prohibition Wastes

Despite current prohibition, Texas possesses characteristics that would enable exceptional legal market performance.

Massive Scale: America's Second-Largest Cannabis Market

Population: 30.5 million residents (2025)—second only to California (39 million)

Adult population: 23.5 million adults 21+

Cannabis consumer base: Estimated 3.2-3.8 million regular users (13.5-16% of adults)—similar to national usage rates

Market size potential:

- Annual spending per consumer: $1,100-1,400 (mature legal market)

- Total adult-use market: $3.5-5.3 billion annually

- Medical market: $200-400 million annually (expanded TCUP)

- Combined market: $3.7-5.7 billion

Only California ($5.8B), Illinois ($1.7B), and Michigan ($3.0B) currently exceed Texas's potential market size. Texas adult-use legalization would create the 2nd or 3rd largest legal cannabis market nationally.

Geographic Concentration: Efficient Market Coverage

Unlike geographically dispersed states (Alaska, Montana, Wyoming), Texas's population concentrates in major metropolitan areas:

Major metros (60%+ of state population):

- Dallas-Fort Worth: 7.9 million (26% of Texas)

- Houston: 7.5 million (25%)

- San Antonio: 2.7 million (9%)

- Austin: 2.4 million (8%)

Framework significance: Dense urban cores enable efficient retail coverage. Where dispersed states require 300+ dispensaries for adequate access, Texas could serve 60% of population with 180-240 urban dispensaries in four metro areas.

Target density: 1.6-2.2 dispensaries per 100,000 residents = 370-510 statewide for optimal coverage. However, concentration means:

- 200-280 urban locations serve 18 million residents (77% of state)

- 90-230 rural/small city locations serve remaining 7 million residents

Comparable states:

- Colorado: Denver metro 55% of population, achieves 73-78% legal share with concentrated retail

- Nevada: Las Vegas metro 73% of population, achieves 75-80% legal share

- Illinois: Chicago metro 65% of population, but fragmentation (61% local bans) limits to 55-60% legal share

Texas geographic concentration enables high-efficiency, low-cost retail network—if local municipalities don't fragment market through bans.

Existing Hemp Infrastructure: 8,500 Dispensaries Ready to Convert

Texas's hemp industry accidentally created the distribution infrastructure a legal cannabis program needs:

Current assets:

- 8,500+ registered hemp retailers

- 53,300 trained employees

- Established supply chains

- Testing lab capacity

- Point-of-sale systems

- Regulatory compliance experience

- Customer bases

Conversion potential: If Texas legalizes adult-use cannabis, hemp retailers could convert to licensed dispensaries with minimal capital investment:

- Retail locations: Already established

- Build-out costs: $50,000-150,000 per location (vs. $300,000-600,000 greenfield)

- Employee training: Staff already understand cannabinoids, dosing, compliance

- Customer education: Consumers familiar with cannabis purchases

Framework advantage: States launching legal programs typically require 18-36 months for retail network to mature. Texas could achieve full retail density within 12-18 months by converting existing hemp infrastructure.

Complication: Hemp industry may lobby AGAINST adult-use legalization to protect existing quasi-monopoly. Current hemp operators face minimal regulation, low barriers to entry, and $5.5B market—why support strict adult-use framework that increases compliance costs and competition?

Border Insulation: No Interstate Leakage

Unlike Indiana (surrounded by Michigan, Illinois, Ohio legal markets) or Arizona (competing with California, Nevada, New Mexico), Texas faces minimal interstate cannabis competition:

Neighboring states (all prohibition or limited medical):

- Oklahoma: Medical only (generous, but not adult-use)

- New Mexico: Adult-use legal BUT small population (2.1M), limited border crossings

- Arkansas: Medical only (restrictive program)

- Louisiana: Medical only (restrictive program)

Distance to nearest adult-use states:

- New Mexico: 250+ miles from Dallas, 150+ from El Paso (only major Texas city with reasonable access)

- Colorado: 400+ miles from Dallas, 600+ from Houston/San Antonio

- Illinois: 600+ miles from Dallas, 800+ from Houston

Framework significance: Border proximity determines revenue leakage. States within 50-100 miles of legal neighbors lose 15-30% of cannabis spending to cross-border purchases. Texas's geographic isolation ensures:

- Minimal consumer leakage to legal states

- No competitive pricing pressure from neighbors

- Captive market for Texas dispensaries

- Tourism revenue from Mexico border (if legalized)

When/if Texas legalizes, the state wouldn't compete for consumers—it would capture them. This enables higher tax rates (18-25%) without pricing pressure from cheaper neighboring markets.

Conservative Fiscal Culture: Revenue Optimization Over Ideology

Texas's political culture leans heavily conservative, typically resisting new government programs and "social engineering." But the state also strongly favors fiscal pragmatism and revenue optimization—creating competing pressures that could favor legalization if framed correctly.

Budget context:

- Texas operates on 2-year budget cycle

- 2025-2027 budget faces recurring structural deficits

- $2 billion shortfall acknowledged in 2025 session

- Property tax relief and education funding consume increasing shares

- No state income tax (constitutional prohibition)

- Sales tax and property tax dependent

Cannabis revenue potential (at 18-22% effective tax rate):

- Adult-use market: $3.5-5.3B annually

- State tax revenue: $630-1,165M annually

- Plus: License fees ($25-75M), local option taxes ($150-300M)

- Total potential: $805-1,540M annually

This would represent 1.5-2.8% of Texas's $60+ billion biennial budget—substantial but not transformative. However, it equals:

- Education funding: $800M = 4,000 new teachers at $200K/teacher (salary + benefits)

- Border security: Current Texas border spending ~$800M annually

- Property tax relief: $1B = ~$150 annual reduction per household

Political framing challenge: Republicans control Texas government with supermajorities. The party traditionally opposes legalization on cultural grounds, but also champions:

- Personal freedom (limited government intrusion)

- Fiscal responsibility (revenue optimization)

- Law and order (enforcement efficiency)

- Economic development (job creation)

- Veterans' issues (medical access)

Conservative case FOR legalization:

- Revenue without tax increases: Generate $800M-1.5B annually without raising income/property taxes

- Personal liberty: Adults making own choices (core conservative principle)

- Law enforcement efficiency: Redirect resources from low-level possession to violent crime, trafficking

- Economic development: 18,000-24,000 jobs, $4-6B in economic activity

- Border security: Legal market reduces cartel influence, disrupts smuggling economics

- Veterans' access: Medical program expansion serves military communities

Framework prediction: IF Texas legalizes, conservative fiscal culture likely produces LOWER taxes (18-22%) and BETTER policy design than progressive states that view cannabis primarily as social justice issue. Compare:

- Illinois (progressive): 25-40% tax, social equity focus, 55-60% legal share

- Colorado (moderate): 21-27% tax, revenue focus, 73-78% legal share

- Michigan (moderate): 16% tax, business focus, 85% legal share

Texas's conservatism could paradoxically produce BETTER outcomes: revenue pragmatism over per-unit taxation, enforcement efficiency over symbolic justice programs, market-driven optimization over social engineering.

Clean Regulatory Slate: No Legacy Constraints

Unlike states transitioning from medical to adult-use programs (California, Illinois, Michigan, Arizona), Texas starts with nearly blank canvas:

Advantages of late adoption:

- No entrenched medical operators: Avoiding California-style battles between legacy medical and new adult-use businesses

- No complicated dual-market: Single integrated adult-use + medical framework from inception

- No prior licensing mistakes: Can study 24 states' successes and failures before designing licensing

- No legacy grow limitations: Can authorize outdoor, greenhouse, indoor cultivation based on data rather than historical precedent

- No grandfathered operators: Level playing field for new businesses

Learning opportunities: By 2028-2035 (likely Texas legalization window), the state would have 15-20 years of multi-state data to inform policy:

- Optimal tax rates (demonstrated: 15-22%)

- Retail density targets (1.6-2.2 per 100K residents)

- Enforcement priorities (supply-side, not consumer)

- Social equity program design (capital access critical)

- Fragmentation prevention (state preemption of local bans)

- Home cultivation impact (minimal effect on legal sales, per CBDT data—see home grow analysis)

Caveat: Clean slate temporary. The longer Texas delays:

- Hemp industry entrenches, complicating transition

- Illicit market solidifies, making displacement harder

- Other states capture innovation, talent, capital

- Federal reform may remove state-level advantages

Optimal window: 2028-2032. Later than this, legacy hemp industry creates transition challenges. Earlier, federal reform unlikely to have occurred.

Predicted Market Outcomes: The Three Texas Scenarios

The framework enables prediction of Texas's market performance under different policy pathways.

Optimized Scenario: Lone Star Leadership (80-88% Legal Share)

Policy design:

- Tax structure: 15-18% state excise + 8.25% sales tax = 23.25-26.25% total

- Local option: 2% maximum (capped to prevent stacking) = 25.25-28.25% effective rate

- Retail authorization: State-issued licenses, minimal local opt-out authority

- Density target: 420-510 dispensaries statewide (1.4-1.7 per 100K residents)

- Major metros: Dallas-Fort Worth 110-135, Houston 105-130, San Antonio 40-50, Austin 35-45

- Rural coverage: 130-200 locations + mandatory statewide delivery

- Delivery mandate: Licensed retailers must offer delivery to underserved areas OR state authorizes delivery-only licenses

- Testing requirements: Rigorous potency, contaminants, pesticides (leverage existing lab infrastructure)

- Enforcement budget: $45-65M annually ($1.50-2.15 per capita) focused on illegal cultivation/trafficking

- Social equity: Well-funded ($75-150M) capital access program, automatic expungement, license preference for conviction records

- Federal reform: Assumes Schedule III (280E elimination) + SAFE Banking passage

Framework inputs:

- Price competitiveness (g = -0.22): Legal 22% cheaper than illicit

- Illicit Texas cannabis: $8-11/gram average

- Legal with federal reform + 25% tax: $6.25-8.75/gram

- Hemp market experience shows Texans will pay premium for quality/safety, but illegal market sets price floor

- Access density (D = 0.88): Excellent coverage via dispensaries + delivery

- 420-510 dispensaries serves 78%+ of population within 15 miles

- Statewide delivery covers remaining 22%

- Safety/quality (S = 0.85): Strong testing, regulatory culture

- Convenience (F = 0.80): SAFE Banking enables cards, apps, normal business operations

- Enforcement (E = 0.75): Strong interdiction, cultural acceptance of law enforcement

- Fragmentation (F_frag = -0.12): Minimal local bans due to state preemption, urban concentration

Predicted outcomes:

- Transaction share: 84-90% (users choosing legal over illicit)

- Volume share: 80-88% (accounting for heavy user segments)

- Timeline: 36-48 months to reach steady state from legalization

Economic impact (mature market, Year 5+):

- Legal market size: $3.0-4.3B annually

- State tax revenue: $680-1,110M annually

- Local tax revenue: $90-180M annually

- Total tax revenue: $770-1,290M annually

- Direct jobs: 18,000-24,000

- Indirect jobs: 22,000-30,000 (hospitality, real estate, professional services, supply chain)

- Illicit market: Reduced from $4.2B to $500-800M (81%+ reduction)

Comparable states:

- Michigan: 85% legal share (current best)

- Oregon: 82-85% volume share, ~95% transaction share

- Nevada: 75-80% legal share

Texas would match or exceed best-performing states through:

- Scale advantages (population concentration)

- Border insulation (no interstate competition)

- Federal reform timing (280E elimination reduces prices)

- Conservative fiscal culture (revenue optimization, not per-unit taxation)

- Learning from predecessors (avoiding Illinois/California mistakes)

Failed Scenario: Texas Replicates Illinois Dysfunction (52-60% Legal Share)

Policy design:

- High tax rate: 28-38% effective total (state 20-30% + local option)

- Limited retail licenses: Political favoritism, artificial scarcity (200-280 statewide)

- Social equity symbolic: Under-funded capital access, license preferences without lending support

- No delivery mandate: Local control prevents statewide coverage

- Weak enforcement: Budget constraints or deprioritization of illicit supply interdiction

- Fragmentation: Major municipalities opt-out (Houston suburbs, rural counties)

- 280E remains: No federal Schedule III rescheduling

Predicted outcomes:

- Transaction share: 60-68%

- Volume share: 52-60%

- Timeline: 60-84 months to plateau (slower adoption due to price/access barriers)

Economic impact:

- Legal market: $1.8-2.8B annually

- Tax revenue: $510-1,065M annually (high rate, smaller base)

- Jobs: 12,000-16,000

- Illicit market: $2.0-2.8B persistent (minimal reduction from prohibition baseline)

Why this scenario fails:

- Price uncompetitive: 280E + high taxes = legal flower $12-18/gram vs. illicit $8-11/gram

- Access limited: 200-280 dispensaries inadequate for 30.5M population, fragmentation creates deserts

- Social equity undermined: Without capital access, license preferences become tokens—licenses awarded to disadvantaged communities but immediately sold to MSOs

- Enforcement deprioritized: Illicit market thrives without supply-side interdiction

Texas would replicate Illinois' policy failure: high taxes reduce competitiveness, artificial scarcity creates access barriers, under-funded equity programs produce symbolic change without substantive outcomes.

Most Likely Scenario: Conservative Competence (68-78% Legal Share)

Texas's political culture suggests neither optimal nor disastrous policy—rather, cautious-but-competent implementation:

Policy design:

- Moderate tax: 20-24% effective total (state 12-16% + sales tax)

- Phased rollout: Medical expansion (2028-2030) → Adult-use (2032-2035)

- Controlled licensing: 300-400 dispensaries initially, expanding based on demand

- Strong regulatory oversight: Typical Texas bureaucratic thoroughness

- Enforcement maintained: Apply existing capacity to illegal cultivation/sales

- Limited local opt-out: State preemption in major metros, local control in rural areas

- Federal reform partial: Schedule III likely by legalization date, SAFE Banking passage uncertain

Predicted outcomes:

- Transaction share: 73-82%

- Volume share: 68-78%

- Timeline: 48-72 months to steady state (conservative phasing slows adoption)

Economic impact:

- Legal market: $2.4-3.6B annually

- Tax revenue: $530-865M annually

- Jobs: 15,000-20,000

- Illicit market: $950M-1.6B (65-75% reduction)

This represents good-but-not-optimal: Better than Illinois/California high-tax failure, not quite matching Michigan/Nevada excellence. Texas's conservatism produces competent implementation but ideological caution prevents full optimization.

Most probable pathway:

- 2028-2030: TCUP medical expansion proves successful, generates $85-125M annual sales

- 2030-2032: Federal Schedule III rescheduling removes stigma, provides political cover

- 2032-2035: Adult-use legalization passes via legislative action (not ballot initiative—Texas lacks initiative process)

- 2035-2038: Retail network expands, tax revenues stabilize, market matures

By 2038-2040, Texas would operate a mid-tier legal cannabis market: generating $530-865M annual state revenue, 15,000-20,000 direct jobs, 68-78% legal market share. Not exceptional, but functional—and vastly superior to continued prohibition.

The Federal Policy Barrier

Even with optimal state policy, Texas cannot fully optimize outcomes under current federal cannabis prohibition.

The 280E Problem: A 40-70% Federal Tax Penalty

Internal Revenue Code Section 280E prohibits businesses trafficking Schedule I or II controlled substances from deducting ordinary business expenses. Because cannabis remains federally Schedule I (as of November 2025), 280E applies to all state-legal cannabis businesses.

Impact on hypothetical Texas dispensary:

Normal business (without 280E):

- Revenue: $1,800,000

- Cost of Goods Sold (COGS): $540,000

- Operating expenses: $990,000

- Taxable income: $270,000

- Federal tax (21%): $56,700

- Net profit: $213,300

Cannabis business (with 280E):

- Revenue: $1,800,000

- COGS (deductible): $540,000

- Operating expenses (NON-deductible): $990,000

- Taxable income: $1,260,000 (not $270,000)

- Federal tax: $264,600

- Actual profit: $5,400 (97% tax on operating profit)

280E forces Texas dispensaries to raise retail prices 15-22% just to survive—making price competition with illicit market nearly impossible. When combined with 24-28% state/local taxes, legal cannabis becomes 40-50% more expensive than illicit alternatives.

State-specific impact for Texas:

- Border insulation provides partial protection (no neighboring legal states undercutting prices)

- But illicit market remains price-competitive

- At 280E + 25% state tax, legal flower costs $12-16/gram vs. illicit $8-11/gram

- This pricing gap limits legal market share to 68-78% even with good access

Solution: Federal Schedule III rescheduling (expected 2026-2028) eliminates 280E. Texas dispensaries can deduct normal expenses, reducing retail prices 12-18%, dramatically improving competitiveness.

Texas-specific 280E advantage: If Texas delays legalization until 2032-2035, federal 280E repeal will likely have occurred—giving Texas pricing advantage states that legalized under 280E regime never enjoyed.

The SAFE Banking Problem

Without SAFE Banking Act passage, Texas dispensaries face:

Operational burdens:

- Cash-only operations: Security costs $55,000-180,000 annually per location

- Armored transport: $800-3,500 per pickup (multiple weekly pickups required)

- Consumer friction: Federal Reserve payment systems research shows cash-only reduces transaction frequency 18-28%

- Banking access: No checking accounts, credit cards, loans, lines of credit for businesses

- Audit challenges: Cash accounting increases errors, IRS audit exposure

- Lending barriers: Entrepreneurs (especially minority-owned, social equity applicants) cannot access traditional business loans

Texas-specific impacts:

- Scale disadvantage: Operating 400-510 dispensaries cash-only requires massive armored car fleet, security infrastructure—costs that reduce profitability and limit expansion

- Social equity undermined: Without banking access, under-capitalized social equity licensees cannot scale, forcing sale to MSOs

- Violence risk: 400+ cash-intensive locations across Texas create robbery targets

- Consumer convenience: Cash-only operations in major metros (Dallas, Houston, Austin) frustrate consumers accustomed to card payments

Solution: SAFE Banking Act passage (likely 2026-2028, following Schedule III) normalizes cannabis banking, enabling:

- Card payments (Visa, Mastercard, debit)

- Business checking accounts

- Commercial loans for expansion

- Normal business operations

- Reduced cash handling costs

- Improved safety

Conservative framing for Texas legislators: SAFE Banking isn't pro-drug policy—it's pro-safety, pro-business, pro-law-enforcement. Cash-only businesses attract robbery, money laundering, tax evasion. Banking normalization enables:

- Better tax compliance

- Reduced robbery risk

- Financial transparency

- Small business access to capital

- Law enforcement visibility into transactions

Texas's law-and-order culture should favor SAFE Banking as public safety measure, not oppose it as drug policy.

The Interstate Commerce Barrier

Even post-legalization, federal prohibition prevents interstate cannabis commerce—creating state-level market constraints:

Current problem:

- Texas growers cannot export to Oklahoma, Louisiana, Arkansas (even if all legalize)

- Texas cannot import from Colorado, Oregon (lower production costs)

- Each state operates closed market

Impact on Texas:

- Production costs: Texas climate varies significantly—optimal outdoor growing in limited regions, requiring expensive greenhouse/indoor cultivation elsewhere

- Supply chain inefficiency: Cannot leverage comparative advantage (Texas grown outdoor, import concentrate from Oregon at $300/lb wholesale)

- Price floors: Closed market prevents arbitrage, keeping prices higher than open interstate commerce would allow

Solution: Federal legalization + interstate commerce enablement would allow:

- Texas outdoor cultivation to compete nationally (warm climate advantage for outdoor/greenhouse)

- Import of low-cost concentrate from Oregon, Oklahoma

- Export of Texas-grown cannabis to Mexico (if/when legalization occurs)

Timeline: Interstate commerce likely 5-10 years POST-federal legalization (2032-2038 earliest), as states resist federal preemption of state-level regulatory frameworks.

For Texas legalization 2032-2035, interstate commerce unlikely to impact initial market development—but by 2038-2040, could enable price reductions and export opportunities.

Federal Reform Timeline and Texas Coordination

Optimal Texas legalization timing: 2032-2035

- 2026-2028: Schedule III rescheduling (280E elimination)

- 2027-2029: SAFE Banking passage (normal banking operations)

- 2032-2035: Texas adult-use legalization when federal barriers removed

This sequencing allows Texas to avoid California/Illinois early-adopter disadvantages (operating under 280E handicap) while maintaining fast-follower learning advantage.

IF Texas legalizes earlier (2028-2030): Would operate under 280E + no SAFE Banking for 2-4 years, handicapping market optimization and reducing legal share by 8-15 percentage points until federal reform occurs.

IF Texas delays longer (2038+): Loses first-mover advantage to Oklahoma, Louisiana, Arkansas—allowing neighboring states to capture Texas border residents' cannabis spending. Also risks federal preemption if comprehensive legalization passes nationally.

Strategic window: 2032-2035 legalization captures federal reform benefits while maintaining state-level policy control and avoiding regional competition.

Policy Recommendations: How Texas Achieves 80-88% Legal Market Share

IF Texas chooses the legalization path, these evidence-based policies maximize outcomes.

Priority #1: Conservative Tax Structure (Revenue Through Volume, Not Rates)

Recommendation:

- State excise tax: 12-16% on retail sales

- State sales tax: 8.25% (existing rate applies automatically)

- Total state burden: 20.25-24.25%

- Local option: 2-3% maximum (strictly capped to prevent stacking)

- Total effective rate: 22.25-27.25%

Rationale: Revenue optimization comes through market share (volume), not per-unit taxation (rate).

Math demonstration:

- High-tax scenario (35% effective rate, 55% legal share): $4.2B illicit market × 0.55 legal = $2.31B legal sales × 0.35 tax rate = $809M revenue

- Low-tax scenario (22% effective rate, 82% legal share): $4.2B illicit market × 0.82 legal = $3.44B legal sales × 0.22 tax rate = $757M revenue

- Optimal scenario (25% effective rate, 80% legal share): $4.2B illicit market × 0.80 legal = $3.36B legal sales × 0.25 tax rate = $840M revenue

Lower taxes (22-25%) paired with high legal share (78-85%) generate MORE total revenue than high taxes (32-38%) with low legal share (52-62%).

Research across 24 states demonstrates cannabis consumers are highly price-sensitive. Every 10% price increase reduces legal market choice probability by 2.3%. Texas must price-compete with:

- Illicit market ($8-11/gram, zero taxes)

- Hemp-derived products ($15-25/gram equivalent)

- Future Oklahoma/Louisiana legal markets (if/when they legalize)

Tax rates above 30% guarantee persistent illicit market competition. Texas should target 22-27% sweet spot: competitive with illicit pricing, generates maximum revenue through volume.

Conservative framing: Lower taxes = more revenue through market capture. This is fiscal responsibility, not liberal drug policy—optimizing revenue collection through smart market design rather than per-unit taxation.

Priority #2: Statewide Access Without Fragmentation

Recommendation:

- State-issued retail licenses (Texas Department of Licensing and Regulation or new Cannabis Control Board)

- Target density: 420-510 dispensaries statewide (1.4-1.7 per 100K residents)

- Geographic distribution:

- Dallas-Fort Worth: 110-135 dispensaries

- Houston: 105-130

- San Antonio: 40-50

- Austin: 35-45

- Regional hubs: Corpus Christi, El Paso, Lubbock, Amarillo, Tyler, Waco (40-70 combined)

- Rural areas: 60-100 locations + delivery coverage

- Statewide delivery mandate: Licensed retailers must offer delivery OR state authorizes delivery-only licenses

- Municipal authority: Cities can regulate zoning (distance from schools, churches), cannot ban retail outright

- State preemption: Cannabis regulation is state matter—municipalities cannot override state licensing

Rationale: Prevent California fragmentation disaster.

California's 61% local retail ban creates massive access barriers, limiting legal market to 50% despite optimal pricing. Fragmentation penalty in framework: -0.8 × F_frag reduces effective access density.

Texas has two advantages California lacks:

- No strong home rule tradition: Texas municipalities have limited authority to override state law

- Population concentration: 60% of Texans in four metros—state can mandate retail in major cities, allow local control in rural areas without severe fragmentation

Policy design:

- Tier 1 cities (Dallas, Houston, San Antonio, Austin, Fort Worth): State mandates minimum retail density (1 dispensary per 75,000-100,000 residents), cities control zoning only

- Tier 2 cities (100,000+ population): State mandates cannabis retail allowed, cities control number/zoning

- Tier 3 cities/rural: Local control, BUT if municipality bans retail, state authorizes delivery from nearest licensed location

This prevents urban fragmentation (where most consumers live) while respecting rural preferences.

Delivery critical: 35-40% of Texans in rural areas, small towns. Without delivery mandate, these residents have no access—forcing continued illicit market use. Statewide delivery ensures 95%+ of Texans have legal access within 24-48 hours.

Conservative framing: State licensing prevents patchwork chaos of conflicting local laws. Businesses need regulatory certainty, consumers need access—state-level framework provides both while respecting legitimate local zoning concerns (distance from schools).

Priority #3: Leverage Enforcement Strengths (Redirect, Don't Defund)

Recommendation:

- Budget: $45-65M annually ($1.50-2.15 per capita)

- Focus: Large-scale illegal cultivation (1,000+ plant operations), interstate trafficking, unlicensed manufacturing

- Avoid: Small-scale home cultivation (if allowed), consumer possession below legal limits, licensed businesses with minor violations

- Task force structure: Texas DPS + local sheriff departments + federal DEA coordination (for interstate trafficking)

- Metrics: Track illegal market indicators (unlicensed dispensary busts, large cultivation site seizures, illicit product seizures)

- Protect legal businesses: Frame as eliminating unfair competition from untested, untaxed, illegal operators

Rationale: Texas's strong law enforcement culture is ASSET, not liability.

States with robust illicit market interdiction consistently outperform states with deprioritized enforcement:

- Nevada: Strong enforcement, 75-80% legal share

- Michigan: Strong enforcement, 85% legal share

- California: Weak enforcement (budget cuts), 50% legal share

- New York: Weak enforcement (political deprioritization), 30% legal share

Framework weight: Enforcement = 0.6×, smaller than price but significant. $45-65M enforcement budget (equivalent to 100-140 FTE officers + equipment + task force coordination) sufficient to:

- Disrupt large illegal grows (500+ plant operations)

- Interdict interstate trafficking

- Shut down unlicensed dispensaries

- Reduce illicit supply 30-50% within 24 months

Conservative framing: Not "ending the drug war"—redirecting it. Law enforcement remains fully funded, fully operational. Target shifts from arresting consumers (26,602 possession arrests annually now) to protecting legal market from criminal networks. Officers prefer this: real criminals, real impact, not low-level possession.

Budget-neutral: Current enforcement costs $125-185M annually (arrests, prosecution, incarceration). Redirect 25-35% ($45-65M) to supply-side interdiction, remainder to violent crime, property crime.

Priority #4: Federal Reform Advocacy (Even From Prohibition State)

Even maintaining prohibition, Texas should support federal cannabis reform:

Schedule III Rescheduling:

- Not federal legalization (maintains state control, states can continue prohibition if desired)

- Eliminates 280E tax penalty (allows normal business deductions)

- IF Texas ever legalizes, federal reform ensures competitive pricing

- Bipartisan support (pharmaceutical industry, medical community, veterans groups back rescheduling)

SAFE Banking Act:

- Public safety issue: Reduces cash-related crime at dispensaries

- Economic development: Enables normal business operations, small business lending

- Banking sector benefits: Texas banks (Frost Bank, Texas Capital Bank, BBVA USA, regional credit unions) can serve legal state markets

- Law enforcement advantage: Banking transparency enables financial crime detection, tax compliance monitoring

Conservative case for Texas Congressional Delegation: Texas Senators John Cornyn and Ted Cruz, Texas House members (38 total):

- State sovereignty: Federal reform removes federal impediment to state choice. Texas can maintain prohibition if desired—but shouldn't force other states to suffer federal handicaps

- Economic: Legal states generate billions in economic activity, tax revenue. Federal barriers (280E, banking) harm state economies—federal government shouldn't sabotage state-legal industries

- Public safety: Cash-only cannabis businesses attract robbery, money laundering. SAFE Banking improves safety in legal states

- Veterans: Federal prohibition prevents VA doctors from recommending cannabis. Schedule III would allow veteran access to alternative pain management

Texas can oppose legalization while supporting federal reform that respects state sovereignty and improves public safety in legal states.

Priority #5: Expungement and Social Equity (Repairing Past Harms)

IF Texas legalizes, must address historic enforcement disparities:

Automatic Expungement:

- All cannabis-related convictions expunged immediately upon legalization

- Offenses covered: Possession (any amount), cultivation (personal use), paraphernalia, minor sales

- Automatic process: No petition required—state proactively clears records

- Restoration: Voting rights, employment eligibility, housing access, education financial aid restored

- Priority: Repair harm before creating new legal market

Data:

- Texas made 26,602 marijuana possession arrests (2024)

- 200,000+ arrests 2015-2024 (estimated)

- African Americans 30.2% of arrests, 12.9% of population (2.3× disparity)

- Each conviction creates lifelong employment, housing, education barriers

Model: Illinois expunged 770,000+ records—most transformative component of legalization, benefiting communities harmed by enforcement disparity.

Social Equity Licensing: Texas must ensure communities harmed by prohibition participate in legal market:

Eligibility criteria:

- Cannabis conviction records (individual or immediate family)

- Residency in high-arrest zip codes (disproportionately Black, Hispanic communities in Dallas, Houston, San Antonio)

- Minority-owned businesses

- Veteran-owned businesses

Support mechanisms (critical—preferences without support = tokenism):

- Capital access fund: $75-150M for low-interest loans, grants, technical assistance

- Loan guarantees: State-backed lending reduces bank risk, enables access to private capital

- Technical assistance: Business planning, compliance training, operations support

- Accelerated licensing: Social equity applicants get expedited review

- Ownership protections: Restrictions on license transfers prevent immediate sale to MSOs

Avoid Illinois mistakes: Illinois awarded social equity licenses but provided insufficient capital access—most recipients unable to secure funding, forced to sell licenses to MSOs. Result: symbolic equity, not substantive.

Texas must fund capital access ($75-150M) OR social equity program becomes window dressing.

Conservative framing:

- Personal responsibility: Individuals harmed by enforcement should have opportunity to succeed in legal market

- Economic empowerment: Create businesses, jobs in communities with high unemployment

- Criminal justice reform: Conservative principle—excessive criminalization harms communities, opportunities for redemption preferred over permanent punishment

Budget: Social equity fund ($75-150M) can be revenue-neutral—allocate first 2-3 years of cannabis tax revenue exclusively to repairing prohibition harms, then shift to general fund.

Comparison to Other Markets

Texas's potential performance depends on policy choices—ranging from disaster to excellence.

High-Performing States (78-88% Legal Share)

Michigan (Opened November 2019):

- Legal market share: 85% (best in nation excluding Oregon)

- Tax burden: 16% total (10% excise + 6% sales)

- Retail density: 2.1 dispensaries per 100K residents

- Strategy: Competitive pricing, rapid licensing, statewide delivery

- Why Michigan succeeds: Price competitiveness + excellent access + strong enforcement

Texas comparison: With federal reform, Texas could match Michigan by:

- Similar tax rate (22-25% vs. Michigan 16%)

- Comparable density (1.6-2.0 per 100K vs. Michigan 2.1)

- Stronger enforcement culture (Texas advantage)

- Larger scale (30.5M vs. Michigan 10M)

Oregon (Opened October 2015):

- Legal market share: 82-85% volume, ~95% transaction

- Tax burden: 20% total (17% excise + 3% state sales in some areas)

- Retail density: 4.2 per 100K (oversupply)

- Strategy: Ultra-low prices ($3-5/gram), massive retail density, full delivery

- Why Oregon succeeds: Negative price gap (legal cheaper than illicit), maximum access

Texas comparison: Cannot replicate Oregon's wholesale collapse ($300-500/lb) causing $3-5/gram retail. But with federal reform, Texas could approach Oregon's performance through:

- Competitive pricing (22-25% tax)

- Strong access (420-510 dispensaries + delivery)

- Border insulation (no low-price neighbors)

Nevada (Opened July 2017):

- Legal market share: 75-80%

- Tax burden: 24-29% total (state + local)

- Strategy: Tourism focus, Las Vegas concentration, strong enforcement

- Why Nevada succeeds: Dense urban retail + enforcement + captive tourist market

Texas comparison: Similar structure (urban concentration, strong enforcement culture, border insulation). Texas could match Nevada by replicating policy design.

Mid-Tier States (65-78% Legal Share)

Colorado (Opened January 2014):

- Legal market share: 73-78% (strong but not optimal due to 280E)

- Tax burden: 21-27% total (15% excise + sales + local option)

- Strategy: Moderate approach, learning over time

- Why Colorado solid: Good access, moderate pricing, strong enforcement—but 280E handicaps optimization

Texas comparison: With federal reform (no 280E), Texas should exceed Colorado through:

- Similar tax structure (22-27% effective)

- Better border insulation (Colorado competes with neighboring states)

- Larger scale enabling efficiency

Struggling States (50-62% Legal Share)

Illinois (Opened January 2020):

- Legal market share: 55-60%

- Tax burden: 25-40% total (among nation's highest)

- Strategy: Social equity rhetoric, high taxes undermine goals

- Why Illinois struggles: Price uncompetitive, social equity under-funded, limited access

Texas risk: IF Texas implements high taxes (30%+), under-funds social equity, allows fragmentation → replicates Illinois failure (52-60% legal share)

California (Opened January 2018):

- Legal market share: 50%

- Tax burden: 30-37% total (reduced from 45% after crisis)

- Strategy: Complex regulations, local fragmentation (61% retail bans), weak enforcement

- Why California fails: Price uncompetitive, access fragmented, enforcement deprioritized

Texas advantage: Unlike California, Texas can:

- Avoid local fragmentation (state preemption authority)

- Implement enforcement (cultural acceptance)

- Start with lower taxes (learn from California mistakes)

Texas Positioning

With optimized policy: 80-88% legal share—#1 or #2 nationally (behind Oregon) With moderate policy: 68-78% legal share—top-tier performance (Colorado/Nevada range) With failed policy: 52-60% legal share—Illinois dysfunction

Texas has structural advantages no other state except California possesses (scale, concentration, border insulation). The question is: Will policymakers implement evidence-based design, or replicate Illinois's ideological mistakes?

Timeline and Political Reality

When will Texas legalize? Predictions by probability:

Short-Term (2025-2027): Continued Prohibition [95% Probability]

Current political dynamics:

- Republican supermajorities in House (86-64) and Senate (19-12)

- Governor Greg Abbott cautious, will sign medical expansion but opposes adult-use

- Lt. Governor Dan Patrick strongly opposes any THC liberalization

- House Speaker Dade Phelan marginally more open but won't push against Senate/Governor opposition

- 2025 session killed all adult-use bills without committee hearings

Factors maintaining prohibition:

- No ballot initiative process (reforms must pass through hostile legislature)

- Conservative base opposes legalization (despite 50%+ general public support)

- Hemp industry provides cannabis access without political cost

- Cultural symbolism valued over fiscal pragmatism

- Federal Schedule I status provides political cover

Accelerants (insufficient for 2025-2027 change):

- Budget shortfalls worsen beyond $2B annually

- Federal Schedule III rescheduling (normalizes cannabis medically)

- Multiple large Texas cities decriminalize via ballot initiatives

- Public support exceeds 65% (forcing political pressure)

Most likely 2025-2027 outcome: Prohibition continues, TCUP medical expansion occurs (HB 46), hemp market regulated but not banned, decriminalization battles continue at city level.

Medium-Term (2028-2032): Medical Expansion [60% Probability]

Pathway to medical program:

- Federal Schedule III rescheduling (2026-2028) removes stigma

- TCUP expansion proves successful (50,000-175,000 patients by 2028)

- Neighboring Oklahoma, Arkansas medical programs mature, demonstrate normalcy

- Budget pressure intensifies (recurring structural deficits)

- Generational change: 2026 and 2028 elections bring younger, more pragmatic legislators

- Governor post-Abbott (term expires 2027) potentially more open—or at minimum not actively hostile

Most likely medium-term scenario: Medical cannabis program expansion (2028-2030) with:

- 50-75 qualifying conditions (approaching comprehensive medical)

- 20-30 licensed dispensaries

- 5-10mg THC dosage cap (moderate limits)

- Smokeable flower allowed

- 200,000-400,000 patient enrollment

- $150-300M annual medical market

This creates precedent for adult-use but doesn't address illicit market (medical too limited/expensive).

Adult-use probability 2028-2032: 25-35%—possible but unlikely. Requires:

- Medical program proves successful (no public health crisis, popular support, revenue positive)

- Federal SAFE Banking passage (normalizes cannabis operations)

- Budget crisis severe enough to force revenue consideration

- Democratic gains in legislature (unlikely given Texas demographics)

Most likely: Medical expansion occurs 2028-2030, adult-use consideration delayed until 2032+.

Long-Term (2032-2040): Adult-Use Probable [70-80% Probability]

Factors making legalization inevitable:

- Federal normalization: Schedule III rescheduling or full federal legalization by 2030-2035

- Multi-state precedent: 35-40 states with legal programs by 2035

- Lost revenue compounds: $7-11B cumulative revenue lost to continued prohibition (2025-2035)

- Demographic shift: Millennials/Gen-Z become voting majority—65-75% support legalization

- Neighboring states legalize: Oklahoma, Louisiana, Arkansas likely approve adult-use by 2035, creating border pressure

- Cultural normalization: 15-20 years of legal markets nationwide eliminate stigma

- Conservative pragmatism: Younger Republican legislators more economically pragmatic, less culturally conservative on cannabis

Most likely pathway (2032-2037 legalization):

- 2028-2030: Comprehensive medical program implemented

- 2030-2032: Medical program successful, 300,000+ patients, $250-450M annual market

- 2032-2035: Budget crisis forces revenue consideration, federal legalization removes political cover for prohibition

- 2033-2037: Adult-use legalization via legislative action

- Conservative implementation (phased rollout)

- Moderate taxes (20-25%)

- Strong regulatory oversight

- Evidence-based policy incorporating 20+ years of multi-state data

Texas legalization probability by year:

- 2027: <5%

- 2030: 15-25%

- 2033: 45-60%

- 2037: 70-85%

- 2040: 90%+

Optimal timing: 2032-2035 legalization captures federal reform benefits (280E eliminated, SAFE Banking operational) while maintaining state regulatory control and learning advantage (20+ years of multi-state data).

Latest plausible timeline: 2040-2045. By 2045, Texas will be one of the last 5-10 states without adult-use programs. Political, economic, and cultural pressure will be overwhelming.

Economic Reality: What Prohibition Costs Texas

Current State (2025): Hemorrhaging Revenue, Arresting Citizens

Illicit market: $4.2 billion annually, untaxed, unregulated, funding criminal networks

Hemp market: $5.5 billion annually, minimally taxed ($268M revenue), poorly regulated

Traditional illicit + hemp: $9.7 billion total cannabis market operating outside meaningful state control

State costs:

- Enforcement: $125-185M annually (arrests, prosecution, incarceration for violations legal 250+ miles away in New Mexico)

- Lost tax revenue: $750-1,100M annually at 18-22% effective rate on $4.2B market

- Economic opportunity: 18,000-24,000 jobs not created

- Health costs: Unregulated hemp products causing adverse events, poison control calls

- Social costs: 26,602 arrests annually, disproportionately harming Black and Hispanic Texans

10-year prohibition cost (2025-2035):

- Lost tax revenue: $7.5-11.0B cumulative

- Enforcement spending: $1.25-1.85B cumulative

- Arrests: 230,000-300,000 residents criminalized

- Economic opportunity lost: $40-60B in economic activity not generated

- Total cost: $15-25B+ over decade

Optimized Legal Market (Year 5+ Post-Legalization)

IF Texas legalizes 2032 with evidence-based policy + federal reform:

Legal market size: $3.0-4.3B annually (adult-use) + $250-400M (medical) = $3.25-4.7B total

State tax revenue:

- Adult-use: $680-1,110M annually (22-26% effective rate)

- Medical: $45-80M annually (18-20% effective rate)

- License fees: $35-65M annually

- Total state revenue: $760-1,255M annually

Local tax revenue: $90-215M annually (2-3% local option where implemented)

Total public revenue: $850-1,470M annually

Economic impact:

- Direct jobs: 18,000-24,000 (cultivation, processing, testing, retail, delivery)

- Indirect jobs: 22,000-30,000 (hospitality, real estate, professional services, supply chain, transportation)

- Total employment: 40,000-54,000 jobs

- Wages: $2.4-3.6B annually

- Economic multiplier: $6.5-9.4B total economic activity

Illicit market reduction: From $4.2B to $500-800M (80-88% reduction)

Social benefits:

- Arrests eliminated: 26,000+ annually no longer criminalized

- Records expunged: 200,000+ convictions cleared

- Employment access: Hundreds of thousands gain employment opportunities previously blocked by records

- Enforcement efficiency: $125-185M enforcement budget redirected to violent crime, trafficking

Tax revenue allocation (illustrative model):

- 30% education ($228-377M annually)

- 25% substance abuse treatment and mental health ($190-314M)

- 20% law enforcement and criminal justice reform ($152-251M)

- 15% social equity and community reinvestment ($114-188M)

- 10% general fund ($76-125M)

The 10-Year Comparison: Prohibition vs. Legalization (2025-2035)

Prohibition pathway:

- Tax revenue: $0

- Arrests: 230,000-300,000

- Enforcement costs: $1.25-1.85B

- Economic activity: $9.7B annually illicit/hemp (unregulated, minimal tax capture)

- Jobs: Hemp sector only (53,000 current, unregulated)

- Social impact: Continued criminalization, enforcement disparities

Legalization pathway (2032 start):

- Tax revenue: $2.5-4.2B cumulative (2032-2035, 3-4 years operational)

- Arrests: Near-zero post-legalization

- Enforcement redirection: Focus on illegal operations, not consumers

- Economic activity: $3.25-4.7B annually legal market (regulated, taxed)

- Jobs: 40,000-54,000 direct + indirect

- Social impact: Expungement, equity programs, enforcement reform

The difference: Choosing optimized legalization over prohibition 2032-2035:

- Gains $2.5-4.2B tax revenue (3-4 years operational by 2035)

- Avoids $1.25-1.85B enforcement costs (2025-2035 total)

- Eliminates 230,000-300,000 arrests

- Creates 40,000-54,000 jobs

- Generates $6.5-9.4B annual economic activity (mature market)

By 2040 (8 years post-legalization), cumulative difference approaches $20-35B in net economic benefit to Texas.

Addressing Cultural Concerns: Cannabis Health Reality

Texas's conservative culture resists legalization partly due to stigma: perception cannabis is dangerous drug warranting prohibition.

The Evidence: Cannabis Is Coffee, Not Cocaine

Research demonstrates cannabis health risks are comparable to alcohol and caffeine, not to cocaine, methamphetamine, or opioids. Key findings:

Mortality:

- Cannabis overdose deaths: Zero annually (impossible to consume lethal dose)

- Alcohol deaths: 95,000+ annually in U.S.

- Opioid deaths: 80,000+ annually

- Tobacco deaths: 480,000+ annually

Addiction rates:

- Cannabis: 9% of users develop dependence

- Alcohol: 15% of users develop dependence

- Tobacco: 32% of users develop dependence

- Cocaine: 17% of users develop dependence

Teen use concerns: Multi-state research shows legalization does NOT increase teen cannabis use:

- Colorado: Teen use flat or declining post-legalization (2014-2024 data)

- Washington: Similar pattern—teen use decreased slightly

- Mechanism: Legal markets increase ID verification rigor (illicit dealers don't check age), reduce teen access compared to prohibition

Impaired driving: Legal states have NOT seen traffic fatality increases:

- THC impairment is real but detectably different from alcohol

- Legal markets enable public education campaigns

- DUI enforcement applies to cannabis equally as alcohol

- Colorado, Washington 10+ years data shows no correlation between legalization and traffic fatalities

Conservative Case FOR Legalization

Texas can legalize while maintaining conservative values:

Personal freedom: Adults should make own choices about substances comparable in risk to alcohol, caffeine. Government shouldn't criminalize personal behavior that harms no one else—core conservative principle of limited government.

Fiscal responsibility: Prohibition costs $125-185M annually in enforcement. Legalization generates $760-1,255M annually in revenue. Net fiscal swing: $885-1,440M annually. Conservative governance means spending taxpayer money wisely—prohibition is expensive failure.

Law and order: Legal markets eliminate criminal networks more effectively than enforcement. Texans currently buy cannabis from cartels, gangs, illicit growers. Legalization redirects $4.2B from criminals to licensed Texas businesses, tax-paying citizens, job-creating entrepreneurs.

Enforcement becomes MORE effective: Instead of arresting 26,602 consumers annually (wasting officer time, court resources, jail space), law enforcement targets real criminals—illegal grow operations, interstate traffickers, unlicensed manufacturers. Officers prefer this: real impact, real threats, not low-level possession cases.

States' rights: Federal prohibition infringes Texas sovereignty. The state should determine its own cannabis policy, not defer to federal government. Supporting federal Schedule III rescheduling and SAFE Banking removes federal barriers while preserving state authority to choose legalization or prohibition.

Economic development: 40,000-54,000 jobs, $6.5-9.4B economic activity, 8,500 businesses (converting hemp retailers + new licenses). Texas excels at business-friendly policy, job creation, economic growth—cannabis is opportunity to demonstrate conservative economic policy works.

Veterans' issues: 1.4 million veterans live in Texas—large veteran population nationwide. Federal prohibition prevents VA doctors from recommending cannabis for PTSD, chronic pain, traumatic brain injury. Texas can lead on veteran care by legalizing medical cannabis, supporting federal reform enabling VA access.

Texas can legalize cannabis as conservative policy: fiscal responsibility, personal freedom, law enforcement efficiency, economic development, veterans' care. This isn't liberal drug policy—it's conservative governance optimizing outcomes for citizens.

Conclusion: The Lone Star State's Inevitable Choice

Texas in 2025 presents American cannabis policy's greatest paradox: official prohibition coexists with $9.7 billion largely unregulated cannabis marketplace. The state arrests 26,602 residents annually for marijuana possession while operating 8,500 hemp dispensaries selling virtually identical products. Law enforcement spends $125-185M prosecuting violations that are legal 250 miles away in New Mexico. Texas hemorrhages $750-1,100M in annual tax revenue to continued prohibition.

This cannot last forever.

The political reality: Short-term (2025-2027) legalization remains unlikely. Republican supermajorities maintain prohibition despite 60%+ public support for medical cannabis and 50%+ support for adult-use. No ballot initiative process insulates legislature from voter pressure. Lt. Governor Dan Patrick actively opposes any THC liberalization. Governor Abbott opposes adult-use despite supporting medical expansion.

But medium-term (2028-2032) and long-term (2032+) changes are inevitable:

Economic pressure intensifies: Lost tax revenue approaches $7-11B cumulative by 2032-2035. Border state examples (New Mexico, Oklahoma) demonstrate successful programs generating hundreds of millions annually while Texas arrests citizens.

Demographic shifts unstoppable: Millennials and Gen-Z become voting majority by 2030-2032. Even young Republicans support legalization 55%+ rates. Generational change forces political evolution.

Federal reform likely: Schedule III rescheduling probable 2026-2028, full federal legalization possible 2030-2038. Federal normalization removes primary excuse for state prohibition.

Multi-state precedent overwhelms: By 2035, 35-40 states will have legal programs. Texas standing as one of final holdout states becomes untenable—cultural, political, economic pressure forces change.

The Framework Prediction

IF Texas legalizes with evidence-based policy + federal reform by 2032-2035:

The state will achieve 80-88% legal market share by 2036-2038, generating:

- $3.0-4.3B annual adult-use sales (mature market)

- $760-1,255M annual state tax revenue

- 18,000-24,000 direct jobs, 40,000-54,000 total employment

- $6.5-9.4B annual economic activity

- Illicit market reduction: From $4.2B to $500-800M (80-88% collapse)

Texas possesses structural advantages no state except California can match:

- Massive scale: 30.5 million residents, $3.7-5.7B potential market

- Geographic concentration: 60% population in four metro areas enables efficient retail coverage

- Existing infrastructure: 8,500 hemp dispensaries provide instant distribution network

- Border insulation: No neighboring adult-use programs create pricing competition or revenue leakage

- Conservative fiscal culture: Revenue optimization likely trumps ideological taxation

- Clean regulatory slate: No legacy constraints from prior medical programs

- Federal reform timing: Legalization 2032-2035 occurs post-280E elimination, providing pricing advantages early-legal states never enjoyed

Performance comparison:

- With optimized policy: 80-88% legal share—matching Oregon, exceeding Michigan

- With moderate policy: 68-78% legal share—Colorado/Nevada tier, solid performance

- With failed policy: 52-60% legal share—Illinois dysfunction, policy failure despite legalization

The Conservative Case

Texas should legalize cannabis NOT as progressive social policy, but as smart conservative governance:

Fiscal responsibility: Prohibition costs $125-185M annually, generates $0 revenue. Legalization produces $760-1,255M annually—net fiscal benefit $885-1,440M. This is revenue optimization without tax increases.

Personal freedom: Adults should make own choices about substances comparable in risk to alcohol. Limited government means not criminalizing personal behavior harming no one else.

Law and order: Legal markets eliminate criminal networks more effectively than enforcement. Redirect $4.2B from cartels to Texas businesses. Refocus law enforcement on real criminals, not 26,602 possession arrests annually.

Economic development: 40,000-54,000 jobs, 8,500+ businesses, $6.5-9.4B economic activity. Texas excels at job creation—cannabis demonstrates conservative economic policy works.

Veterans' care: 1.4M Texas veterans deserve access to alternative pain management. Medical cannabis serves those who served.

States' rights: Federal prohibition shouldn't dictate Texas policy. State should determine own cannabis framework based on evidence, not federal Schedule I classification.

The Timeline

2025-2027: Prohibition continues, TCUP medical expansion occurs, hemp market regulated but preserved

2028-2032: Medical cannabis program likely expands significantly (50-75 conditions, 20-30 dispensaries, smokeable flower), adult-use consideration possible but not probable

2032-2038: Adult-use legalization probable (70-80% likelihood)—federal reform removes political cover, budget pressure intensifies, demographic shifts force policy change

2040+: Texas legalization near-certain if hasn't already occurred—one of last 10-15 states, overwhelming political/economic pressure

The Question

The question isn't IF Texas legalizes. The question is: When Texas finally chooses this path, will policymakers implement evidence-based policy maximizing outcomes, or will they replicate Illinois' high-tax ideology producing 52-60% legal share despite legalization?

Texas has luxury of hindsight—20+ years of multi-state data, neighboring state examples (Oklahoma, New Mexico), federal reform likely before state action. There is zero excuse for policy failure.

IF Texas legalizes smart (22-26% tax, 420-510 dispensaries, strong enforcement, federal reform): 80-88% legal market share, $760-1,255M annual revenue, 40,000-54,000 jobs, best-performing large market nationally.

IF Texas legalizes poorly (32-38% tax, fragmentation, weak enforcement, under-funded equity): 52-60% legal share, persistent illicit market, Illinois failure 2.0.

IF Texas maintains prohibition: Zero revenue, 26,000+ annual arrests, $750-1,100M revenue hemorrhaged annually, enforcement waste, social injustice continues while neighboring states prosper.

The data is clear. The framework is validated. The path forward is evident.

Texas will eventually legalize cannabis. The only question: How much longer will the state tolerate being the prohibition outlier while economic opportunity flows to neighbors and 26,602 residents face arrest annually for behavior legal 250 miles away?

Everything's bigger in Texas—including the $8 billion question the state can't avoid forever.

About This Analysis

This prediction is based on the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error and r=0.968 correlation.

Resources:

- Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

- Framework methodology: The Black Market Death Equation

- Related analyses: Florida, New Hampshire, W Virginia, Nebraska, N Dakota

For Texas policymakers, MSOs, or investors seeking detailed analysis:

Comprehensive state-specific analysis available under commercial license, including:

- Exact market share predictions under multiple policy scenarios (optimized, moderate, failed)

- IF Texas legalizes: Optimal regulatory framework design with specific tax rates, licensing structure, enforcement priorities

- Hemp market transition strategy and existing infrastructure conversion pathway

- Border dynamics analysis and interstate competition assessment (Oklahoma, New Mexico, Arkansas, Louisiana)

- Tax structure modeling and revenue projections under different rate scenarios (15% vs. 25% vs. 35%)

- Social equity program design with capital access requirements and community reinvestment allocation

- Political probability modeling and legislative pathway analysis

- Federal reform impact assessment (280E elimination, SAFE Banking, interstate commerce)

- Timeline projections with phase-based implementation roadmap

- Comparison analysis to similarly-sized states (California, Illinois, Florida)

- Veterans' access programs and PTSD treatment market sizing

- Medical program expansion projections (TCUP patient enrollment, revenue forecasting)

Contact: silentmajority420@proton.me | @The_Silent_420

The Silent Majority 420 is an anonymous cannabis policy analyst with 25 years of market participation. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0 (free use with attribution)