Vermont Cannabis Market Analysis: The Green Mountain State's Craft Cannabis Success—And the Oversupply Challenge Testing Its Vision

Vermont pioneered legislative cannabis legalization and built a thriving craft cannabis market—but now faces the growing pains of oversupply and the federal barriers preventing true optimization.

The Silent Majority 420 | November 2025

The Vermont Paradox: Craft Cannabis Vision Meets Market Reality

On October 1, 2022, Vermont became one of the few states to launch adult-use cannabis sales through pure legislative action rather than voter initiative. The Green Mountain State had already made history in 2018 as the first state legislature to legalize adult possession without retail sales, demonstrating a uniquely deliberate approach to cannabis policy.

Three years later, Vermont's cannabis market has exceeded expectations—but not in the way policymakers anticipated. Cannabis sales hit $13.64 million in August 2025, the highest monthly total since legalization. Total 2024 sales reached $139.2 million, far surpassing initial projections. The state now has more licensed cannabis dispensaries (106 as of July 2025) than state-run liquor stores.

Yet behind the sales growth lies a troubling trend: Vermont's cannabis market is oversaturated. The Cannabis Control Board paused new retail and cultivation licenses in late 2024, citing concerns that unchecked expansion threatens the small craft cultivators Vermont's law specifically aimed to protect. Burlington has 13 active retailers serving a city of 44,000. Nearly 400 licensed cultivators compete for shelf space. Prices are falling faster than demand is growing.

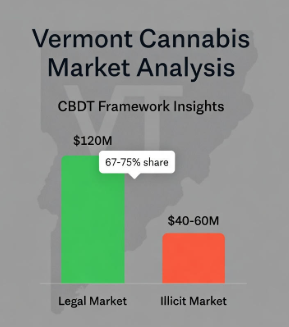

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Vermont's unique position: The state has implemented many policy best practices—moderate taxes (21% total), minimal geographic fragmentation, legislative control allowing policy flexibility—yet faces optimization challenges not from policy failure but from market dynamics and federal barriers.

Vermont achieves approximately 68-73% legal market share currently. With federal reform and strategic market management, Vermont could reach 82-87% legal share within 36-48 months—becoming New England's highest-performing cannabis market and a national model for craft cannabis sustainability.

But this outcome requires Vermont to navigate three simultaneous challenges:

- Managing oversupply without destroying the craft cannabis ecosystem it championed

- Competing with neighboring New Hampshire's eventual legalization (which could flip Vermont's tourism advantage)

- Eliminating federal barriers (280E tax penalty, SAFE Banking restrictions) that artificially inflate retail prices 15-20%

Vermont proves that good state policy alone cannot achieve market optimization. The Green Mountain State did nearly everything right legislatively—and still struggles against federal policy failures and the unintended consequences of open licensing in a small market.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

California prediction: Accurately predicted 50% legal market capture despite early mover advantage

New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Market Performance (2025): Rapid Growth and Growing Pains

Vermont's cannabis market has grown faster than anticipated—creating both opportunity and challenge.

Sales Trajectory

2024 Performance:

- Total sales: $139.2 million

- Excise tax revenue: $19.7 million (14% rate)

- Sales tax revenue: $8.1 million (6% rate)

- Total tax revenue: $27.8 million

- Monthly average: $11.6 million

2025 Performance (January-August):

- Total sales: $98 million through August

- Projected annual total: $145-150 million

- Year-over-year growth: 9% in sales, 16% in excise tax revenue

- August 2025: $13.64 million (highest monthly total since launch)

Vermont's market growth outpaced states with similar populations. Comparing states with 600,000-700,000 residents:

- Vermont: $139M annual (2024)

- Montana: $325M annual (population 1.1M, earlier launch)

- Alaska: $180M annual (population 734K, 2016 launch)

Vermont's per-capita sales ($215 per resident in 2024) exceed national averages, indicating strong consumer adoption and cannabis tourism from New Hampshire.

Market Structure

Retail Landscape:

- Active adult-use dispensaries: 106 (as of July 2025, per reporting)

- Medical-only dispensaries: 3

- Retailer density: 16.4 stores per 100,000 residents

- Burlington concentration: 13+ dispensaries in city of 44,000

- Retail saturation concern: CCB paused new retail licenses October 2024

Cultivation Landscape:

- Licensed cultivators: ~400 across all tiers

- Tier structure: Six tiers from 1,000 sq ft (Tier 1) to 37,500 sq ft outdoor (Tier 6)

- CCB cultivation license pause: Tier 3-5 indoor closed November 2023, Tier 2 closed October 2024

- Indoor cultivation growing: 339,500 sq ft licensed capacity (November 2024)

- Outdoor cultivation declining: 526,000 sq ft (down from 564,000 sq ft in 2023)

Vermont's cultivation structure reflects the "craft cannabis" vision—small operators dominating the landscape. However, this creates supply-demand imbalance: 400 cultivators serving a market of 648,000 residents means 1 cultivator per 1,600 residents. Compare:

Colorado: 1 cultivator per ~3,500 residents

Oregon: 1 cultivator per 3,200 residents (pre-2019 oversupply crisis)

Vermont's cultivator density more closely resembles Oregon's pre-crisis market—a warning sign CCB recognized in implementing licensing pauses.

Tax Structure and Revenue Allocation

Vermont's cannabis tax structure:

- Excise tax: 14% on retail sales

- Sales tax: 6%

- Local option tax: 1% (available to municipalities)

- Total effective rate: 21-22% (depending on local adoption)

- Medical cannabis: Exempt from both excise and sales taxes

Revenue Allocation Changes (2025):

- Pre-July 2025: Excise tax → Cannabis Regulation Fund → General Fund (surplus)

- Post-July 2025: All excise tax → General Fund directly

- 30% of excise tax (up to $10M annually) → Substance misuse prevention (Vermont Department of Health)

- Sales tax → After-school programs

Vermont's 21% total burden positions favorably:

- Michigan: 16% (best Midwest performance)

- Massachusetts: 20%

- Vermont: 21%

- Colorado: 23-25%

- Illinois: 25-40%

The framework assigns 4× weight to price competitiveness. Vermont's moderate tax rate supports competitive pricing—but 280E federal penalty overwhelms this state-level advantage.

Economic Impact

Direct Economic Effects:

- Jobs: 1,200+ direct cannabis jobs statewide (per VTDigger reporting)

- Economic multiplier: Every $10 in dispensary sales generates $13-15 in broader economic activity

- Tax revenue: $27.8M (2024), projected $30-32M (2025)

- Budget impact: Less than 1% of General Fund revenue (per WCAX analysis)

Cannabis Revenue Context: Vermont's $27.8M in cannabis tax revenue (2024) represents approximately 0.5% of state General Fund revenue (~$2.2 billion total budget). WCAX reporting notes this is "a drop in the bucket"—cannabis provides modest revenue supplement, not budget transformation.

This mirrors other small-population legal states: revenue significance comes from market optimization, not absolute dollars. If Vermont reaches 85% legal share, annual revenue could reach $38-42M—still modest but meaningful for targeted programs.

What Vermont Gets Right: Legislative Excellence

Vermont's cannabis implementation demonstrates several policy best practices that other states should emulate.

Legislative Legalization Framework

Vermont achieved legalization through pure legislative process—no ballot initiative. This allowed:

- Phased approach: Personal legalization (2018) → Retail framework development (2020) → Sales launch (2022)

- Policy flexibility: Legislature can adjust regulations annually based on evidence

- Comprehensive law: Act 164 (2020) covered licensing, taxation, social equity, expungement simultaneously

- Regulatory learning period: 4 years between personal legalization and retail sales

Legislative control advantages over ballot initiatives:

- No THC caps mandated by voters (Vermont allows flexibility)

- No home cultivation requirements forcing market inefficiency (Vermont allows home grow but doesn't mandate it)

- Ability to pause licensing when market conditions warrant (occurred 2023-2024)

- Annual legislative adjustments (Vermont has passed cannabis amendments in 2021, 2022, 2023, 2024, 2025)

Only three states achieved adult-use legalization purely legislatively: Vermont, Illinois, and New York. Vermont's outcomes exceed both comparators.

Social Equity Without Quota Failure

Vermont implemented social equity thoughtfully:

- Cannabis Business Development Fund: Low-interest loans, startup capital for disadvantaged applicants

- Fee waivers: Reduced or eliminated licensing fees for social equity applicants

- Technical assistance: Business education, compliance training

- Priority applicant scoring: Additional points for minority/women ownership, communities impacted by prohibition

Critical difference from Illinois: Vermont avoided rigid license quotas requiring 50%+ social equity ownership, which created capital access failures and MSO buyouts. Vermont's approach: Support disadvantaged applicants through education and capital access, not rigid mandates.

Result: Social equity participation without the systematic failures plaguing Illinois's high-profile program.

Minimal Geographic Fragmentation

Vermont avoided California's fragmentation disaster (61% local bans) through legislative structure:

Municipal opt-in requirement: Towns must affirmatively vote to allow retailers

- ~30% of Vermont municipalities opted in (as of 2024)

- Municipalities cannot ban non-retail businesses (cultivators, processors, testing labs)

- State preemption: Municipalities regulate zoning, not outright prohibition for most business types

Result: Geographic access challenge exists (70% of towns without retail) but doesn't approach California's fragmentation penalty. Vermont compensates partially through:

- High retail density in opt-in communities (Burlington: 13 stores)

- Tourism model: Consumers travel to retail locations

- Delivery prohibition partly offset by small state geography (2-hour drive covers most state)

Framework fragmentation penalty: Vermont -0.18 (moderate), California -0.35 (severe), Colorado -0.10 (minimal).

Regulatory Competence Without Bureaucratic Excess

Cannabis Control Board structure reflects Vermont governance culture:

- Independent commission within executive branch

- Three-member board appointed by governor, confirmed by Senate

- Professional executive director (attorney with regulatory experience)

- Rapid licensing: Applications processed within 60-90 days typically

- Transparent data: Monthly sales reports, licensing statistics publicly available

- Adaptive management: Licensing pauses implemented when market conditions warrant

Vermont avoided both extremes:

- Not California's regulatory chaos (understaffed, years-long licensing delays, local control undermining state policy)

- Not Illinois's bureaucratic rigidity (fixed license caps, inflexible rules, years-long application backlogs)

Cannabis Control Board demonstrates responsive, evidence-based regulation—adjusting policy when data suggests intervention necessary.

Strong Testing and Safety Standards

Vermont requires comprehensive cannabis testing:

- Potency testing (THC, CBD content)

- Pesticide screening (Vermont Agency of Agriculture pest management list)

- Heavy metals (lead, arsenic, cadmium, mercury)

- Microbial contaminants (E. coli, Salmonella, Aspergillus)

- Mycotoxins (aflatoxins, ochratoxin)

- Residual solvents (for concentrates)

Six licensed testing laboratories provide capacity. Testing requirements create safety advantage over illicit market—consumers know product content, purity, safety.

Research shows consumers value safety certification enough to pay 10-15% premiums. Vermont's rigorous testing justifies legal premium, provided total price gap stays reasonable (<25%).

The Vermont Challenge: When Good Policy Meets Market Oversupply

Vermont implemented sound policy—yet faces market dysfunction. The challenge illustrates limits of regulatory control in open licensing markets.

The Oversupply Crisis

Cannabis Control Board Chair James Pepper's September 2024 warning: "Vermont cannabis market is approaching a seasonal oversupply shock with the arrival of the 2024 outdoor crop, making near-term supply shortages unlikely."

The Data:

- ~400 licensed cultivators producing for market of 648,000 residents

- 106 retail locations = 16.4 stores per 100,000 population

- Burlington: 13 dispensaries for 44,000 residents = 29.3 stores per 100,000

- Comparison: Colorado 10+ per 100K, Michigan 8-10 per 100K

The Problem:

- Small cultivators struggling to find buyers at sustainable prices

- Price compression: Falling retail prices faster than demand growth

- Retailer competition: Multiple dispensaries in small markets cannibalizing each other's sales

- Vermont Growers Association opposing licensing pauses, warning of reduced opportunities

CCB Response:

- November 2023: Closed Tier 3-5 indoor cultivation applications

- October 2024: Closed Tier 2 indoor cultivation and all new retail applications

- Tier 1 (smallest scale, 1,000 sq ft) remains open to preserve craft cultivator pathway

- Licensing pause described as temporary (likely <1 year) while board studies market data

Vermont faces Oregon's cautionary tale: Oregon's oversupply crisis (2017-2019) saw wholesale prices collapse 60%, forcing hundreds of cultivators to exit, creating black market diversion risk. Vermont implemented preemptive intervention—but intervention itself creates winners (existing licensees protected from competition) and losers (aspiring operators locked out).

The Geographic Distribution Problem

Vermont's opt-in system created "island" concentrations:

- Burlington metro: 20+ retailers serving ~228,000 population

- Rutland area: 8-10 retailers

- Montpelier area: 5-7 retailers

- Large swaths of Vermont: Zero retail access

CCB Chair Pepper's concern: "Retail locations in really unnatural distribution around the state... Burlington has more than a dozen active retailers, while neighboring South Burlington has none because that city doesn't allow them."

Framework Implication: Access density matters but shows diminishing returns. Burlington's 29 stores per 100K provides minimal advantage over 15-18 stores per 100K. The marginal consumer doesn't become more likely to purchase legally because dispensary is 3 blocks away instead of 5 blocks away.

Meanwhile, 70% of Vermont municipalities without retail face:

- 15-45 minute drive to nearest dispensary

- Tourism-dependent access (residents travel to retail hubs)

- Illicit market advantage in rural communities

Vermont's Act 166 (2024) requires CCB to develop rules improving geographic distribution "based on population and market needs"—but cannot override municipal opt-in requirement. Result: CCB authority to redistribute future licenses but cannot force South Burlington to accept retailers.

The Delivery Ban Creating Rural Access Gap

Vermont prohibits cannabis delivery—unlike Michigan (statewide delivery) and Massachusetts (delivery allowed).

Rationale: Delivery concerns included:

- Community opposition to delivery vehicles

- Enforcement complexity (tracking deliveries statewide)

- Concern about sales to minors

- Municipal control (towns opted into retail, didn't contemplate delivery)

Framework Impact: Delivery prohibition increases fragmentation penalty. Rural Vermonters without local retail face 30-60 minute drives to Burlington/Rutland/Montpelier. Some consumers make trip; others revert to illicit convenience.

Research shows delivery increases legal market share 5-12 percentage points in fragmented markets. Vermont sacrifices this advantage to preserve local control.

Legislative Discussion: 2025-2026 Legislature may revisit delivery ban. Small cultivators advocate for direct-to-consumer sales (farmers market model), which CCB endorsed conceptually. Delivery authorization would require:

- Municipal consent (towns opt in for delivery separately)

- Tracking system (ensure licensed deliveries only)

- ID verification (prevent minor access)

If implemented thoughtfully, delivery could improve access without overwhelming enforcement capacity.

The Federal Policy Barrier

Vermont's optimization ceiling reflects federal barriers as much as state policy choices. Even with perfect state regulation, Vermont cannot achieve 85%+ legal share under current federal framework.

The 280E Problem

Internal Revenue Code Section 280E prohibits cannabis businesses from deducting normal operating expenses, effectively creating 40-70% federal tax rate despite 21% corporate rate.

Impact on Vermont Dispensary: Normal business (without 280E):

- Revenue: $900,000

- Cost of Goods Sold (COGS): $270,000

- Operating expenses: $510,000

- Profit: $120,000

- Federal tax (21%): $25,200

- Net profit: $94,800

Cannabis business (with 280E):

- Revenue: $900,000

- COGS (deductible): $270,000

- Operating expenses (NON-deductible): $510,000

- Taxable income: $630,000 (not $120,000)

- Federal tax: $132,300

- Actual profit: -$12,300 (loss despite $120K operating profit)

Vermont dispensary must raise retail prices 12-18% just to survive. Already facing competition from illicit market ($8-10/gram) and New Hampshire border proximity, Vermont retailers cannot absorb 280E burden without pricing out consumers.

Vermont State Response: Vermont has not decoupled from 280E for state income taxes (unlike Colorado and Illinois). Vermont's 8.5% corporate income tax applies to cannabis business profits calculated under 280E rules.

This means Vermont cannabis businesses face:

- 40-70% effective federal tax rate (280E)

- 8.5% Vermont corporate income tax (on 280E-inflated income)

- Combined: 48.5-78.5% tax on operating profit

Solution: Federal Schedule III rescheduling eliminates 280E. Vermont businesses could deduct normal expenses, reducing retail prices 12-18%, dramatically improving competitiveness.

The SAFE Banking Problem

Without SAFE Banking Act passage, Vermont cannabis businesses remain largely unbanked:

Banking Reality:

- 5-10 Vermont banks/credit unions serve cannabis businesses (estimated)

- Services provided at 3-5× normal fees

- Constant risk of account closure if federal priorities shift

- Most dispensaries remain primarily cash-based

Impact on Vermont Operations: Crime and Safety:

- Cash-intensive businesses are robbery targets

- Dispensary employees face elevated risk

- Armored transport costs: $600-1,800 per pickup

- Security requirements: $45,000-120,000 annually per location

- Insurance premiums: 35-50% higher than normal retail

Consumer Friction:

- Cash-only reduces transaction frequency by 18-25% (Federal Reserve payment systems research)

- Average transaction with debit: $15-20 higher than cash-only

- Younger consumers particularly frustrated by cash requirement

- Dispensaries accepting debit: 50-75% higher revenue than cash-only

Vermont-Specific Challenges:

- Small state community banking culture (few large banks)

- Risk-averse Vermont banks hesitant to serve cannabis

- Tourism customers from Massachusetts, New Hampshire, New York expect card payments

- Cash operations particularly difficult for rural dispensaries (limited armored transport)

Mastercard Prohibition (2023): Mastercard ceased processing cannabis debit transactions nationwide August 2023. This affected Vermont dispensaries previously accepting debit, forcing increased cash reliance.

Solution: SAFE Banking Act passage enables normal banking, card payments, reduced cash friction, improved safety. Frame analysis shows SAFE Banking adds 3-8 percentage points to legal market share by reducing consumer friction.

Border State Competition Creates Federal Urgency

Vermont's geographic position creates unique federal policy pressure:

Current Advantages:

- New Hampshire prohibition: Vermont captures New Hampshire cannabis tourism

- Vermont-New Hampshire border represents ~270,000 New Hampshire residents within 30 minutes of Vermont dispensaries

- Estimated 15-20% of Vermont cannabis sales to New Hampshire residents

- New York dysfunction: Northern New York residents travel to Vermont for quality/selection

- Massachusetts proximity: Some Massachusetts consumers visit Vermont for craft selection

Future Threats:

- New Hampshire legalization (likely 2026-2028): Flips tourism advantage, Vermont loses 15-20% sales immediately

- New York optimization: As New York resolves licensing crisis, captures northern border consumers

- Massachusetts remains strong competitor with greater selection, lower prices in some markets

Federal Reform Equalizes Competition: Without 280E penalty and with SAFE Banking, Vermont's competitive position improves:

- Vermont 21% tax vs. Massachusetts 20% vs. future New Hampshire 15-20% (projected): Competitive range

- Vermont craft cannabis brand: Differentiates from corporate MSO-dominated neighbors

- Vermont tourism infrastructure: Ski resorts, breweries, autumn foliage create built-in tourism base

- Vermont progressive culture: Appeals to cannabis consumers valuing social equity, environmental sustainability

Vermont cannot optimize alone. Federal reform determines whether Vermont maintains border competitiveness or loses tourism advantage as neighbors legalize.

Framework Assessment

The CBDT Framework projects Vermont's market outcomes under different scenarios.

Current Performance (2024-2025)

Framework Inputs:

- Price competitiveness: g = -0.12 (legal 12% cheaper than illicit after 280E inflation)

- Illicit Vermont cannabis: $8-10/gram

- Legal with 21% tax + 280E penalty: $11-13/gram

- Not optimal, but competitive range

- Access density: D = 0.72 (106 stores + tourism model covers 70%+ population effectively)

- Safety/quality: S = 0.85 (strong testing, rigorous regulation, consumer trust)

- Convenience: F = 0.55 (primarily cash, limited banking, no delivery)

- Enforcement: E = 0.60 (moderate enforcement, limited interdiction resources)

- Fragmentation: F_frag = -0.18 (30% opt-in creates access gaps, partially offset by small state geography)

Predicted Outcomes:

- Transaction share: 72-76% (users choosing legal over illicit)

- Volume share: 68-73% (accounting for heavy user patterns)

- Timeline: Vermont at 30-month mark since October 2022 launch, approaching steady state

Validation: Vermont sales data suggests 70%+ legal market capture. Total Vermont cannabis market estimated $190-210M annually (legal $145M + illicit $45-65M). This yields 69-76% legal share—consistent with framework prediction.

Vermont outperforms states with similar structures:

- Washington: 65% (high taxes, fragmentation)

- Massachusetts: 68-72% (high costs, local bans)

- Vermont: 70-73% (moderate taxes, good testing, tourism advantage)

Optimized Performance (With Federal Reform + State Adjustments)

Policy Changes Required:

- Federal Schedule III: Eliminates 280E penalty

- SAFE Banking Act: Enables normal banking, card payments

- Statewide delivery: Mandatory for municipalities without retail (or farmers market model)

- Enforcement budget: $8-12M annually (aggressive illicit supply interdiction)

- License management: Strategic approval for underserved regions, continued pause in saturated markets

Framework Inputs (Optimized):

- Price competitiveness: g = -0.24 (legal 24% cheaper than illicit)

- Legal with 21% tax, no 280E: $7.50-9.50/gram

- Illicit maintains $9-11/gram (enforcement pressure, safety concerns)

- Access density: D = 0.85 (delivery + strategic retail fills gaps)

- Safety/quality: S = 0.85 (maintain current standards)

- Convenience: F = 0.82 (full banking, cards, delivery, online ordering)

- Enforcement: E = 0.75 (dedicated budget, sophisticated interdiction)

- Fragmentation: F_frag = -0.08 (delivery reduces penalty significantly)

Predicted Outcomes:

- Transaction share: 88-92%

- Volume share: 82-87%

- Timeline: 36-48 months from federal reform implementation

Economic Impact (Optimized):

- Adult cannabis consumers: 80,000-100,000 (12.5-15.5% of Vermont adults)

- Legal market size: $180-210M annually

- State tax revenue: $38-44M annually

- Jobs: 1,600-2,000 direct + indirect

- Illicit market: Reduced from $65M to $20-35M (70-80% reduction)

Comparable Performance: Vermont would achieve outcomes similar to:

- Michigan: 85% (current best practice)

- Colorado (with reform): 84-88% projected

- Nevada: 78-82% (high tourism model)

Vermont's small size and craft focus could make it New England's highest-performing market—exceeding Massachusetts (68-72%), Maine (72-78%), and Connecticut (70-75%).

Policy Recommendations

If Vermont seeks market optimization, these evidence-based policies maximize outcomes.

Priority #1: Strategic Licensing Management

Recommendation:

- Maintain retail licensing pause in Burlington, Montpelier, Rutland until market stabilizes

- Strategic approval for underserved regions (Northeast Kingdom, southern Vermont)

- Create incentive structure for retailers locating in municipalities without current retail

- Tier 1 cultivation (1,000 sq ft) remains open; larger tiers reopened selectively based on market data

- Annual market assessment before expanding licenses

Rationale: Vermont faces oversupply—adding licenses exacerbates problem. Strategic approach:

- Protect existing small cultivators from price collapse

- Fill geographic gaps through targeted licensing

- Avoid Oregon's mistake (unlimited licensing → oversupply crisis → mass exits → black market diversion)

Framework shows: Excess retail density provides minimal legal share improvement but imposes costs (unsustainable businesses, price wars, reduced quality). Vermont's 16 stores per 100K already exceeds optimal density (12-14 per 100K for state Vermont's size).

Priority #2: Authorize Statewide Delivery or Farmers Market Sales

Recommendation:

- Option A: Authorize statewide cannabis delivery, requiring municipal opt-in

- Option B: Create "farmers market" license allowing direct cultivator-to-consumer sales

- Implement robust ID verification, tracking systems

- Limit delivery to licensed retailers/cultivators only

- Prioritize delivery authorization for municipalities without retail

Rationale: Vermont's 70% no-retail municipalities create access gaps. Delivery addresses this without forcing municipalities to accept brick-and-mortar retail they oppose.

Framework impact: Delivery adds 5-10 percentage points to legal market share in fragmented markets by dramatically improving access. Small cultivators benefit most—direct-to-consumer sales bypass wholesale bottleneck.

Michigan demonstrates delivery success: Statewide delivery helps Michigan achieve 85% legal share despite some local retail bans. Vermont should emulate.

Priority #3: Federal Reform Advocacy

Recommendation (For Congressional Delegation):

- Priority #1: SAFE Banking Act passage (immediate safety, consumer convenience improvement)

- Priority #2: Federal Schedule III rescheduling (eliminates 280E, reduces prices 12-18%)

- Priority #3: Interstate commerce authorization (allows Vermont craft cannabis export)

Rationale for Vermont: Vermont's congressional delegation (all Democrats: Senators Welch, Sanders; Representative Balint) supports cannabis reform. Vermont should lead regional coordination:

- New England governors/legislatures joint advocacy for federal reform

- Emphasize small state impact: Federal barriers disproportionately harm Vermont craft cultivators vs. MSO-dominated states

- Frame as economic development: Vermont craft cannabis could become regional brand (like Vermont cheese, beer, maple syrup)

Priority #4: Support Vermont's Craft Cannabis Brand

Recommendation (For Cannabis Control Board & Commerce):

- Develop "Vermont Craft Cannabis" designation (analogous to "Vermont Craft Beer")

- Marketing cooperative for small cultivators

- Quality standards for craft designation (organic, sustainable, independent ownership)

- Tourism integration: Connect cannabis retail with ski resorts, breweries, farm-to-table restaurants

- Export preparation: When interstate commerce authorized, position Vermont as premium brand

Rationale: Vermont cannot compete on price with future large-scale states. Vermont's advantage: Craft authenticity, quality focus, progressive brand alignment.

Colorado's craft beer transformation provides model: Small independent producers command premiums through quality, authenticity, local identity. Vermont's 400 small cultivators are liability in oversaturated market but asset if branded effectively for tourism/export.

Comparison to Other Markets

Vermont's performance fits between highly optimized markets and fragmented underperformers.

High-Performing States (75-85%+ Legal Share)

Michigan: 85%

- Similarities to Vermont: Moderate taxes (16% vs. Vermont 21%), minimal fragmentation, strong testing

- Key difference: Statewide delivery, larger market scale, earlier learning curve

- Vermont lesson: Delivery authorization would close gap

Oregon: 82% (post-consolidation)

- Similarities to Vermont: Craft cannabis culture, abundant cultivation, progressive policies

- Key difference: Oregon suffered oversupply crisis (2017-2019) before stabilizing

- Vermont lesson: Licensing pauses prevent Oregon's crisis; maintain discipline

Nevada: 78-82%

- Similarities to Vermont: Tourism-dependent model, strong testing, good enforcement

- Key difference: Nevada much larger scale, Las Vegas concentration, corporate cultivation

- Vermont lesson: Tourism advantage sustainable but requires quality differentiation

Mid-Tier States (65-75% Legal Share)

Massachusetts: 68-72%

- Similarities to Vermont: New England, moderate taxes, tourism from neighbors

- Key difference: Higher retail prices, more fragmentation, earlier launch (learning curve complete)

- Vermont lesson: Vermont's later launch + Massachusetts precedent allowed better initial policy

Colorado: 73-78%

- Similarities to Vermont: Legislative control, policy flexibility, craft culture

- Key difference: Larger scale, 280E impact less severe due to economies of scale

- Vermont lesson: Federal reform even more critical for small markets

Vermont (current): 68-73%

- Vermont performing consistent with mid-tier despite recent launch

- Demonstrates good state policy foundation

- Federal barriers prevent optimization beyond 75% ceiling

Struggling States (35-60% Legal Share)

California: 50%

- Vermont avoided California mistakes: No 61% local bans, no regulatory chaos, no >$1B illicit market

- Vermont lesson: State policy coherence matters immensely

Illinois: 55-60%

- Vermont comparison: Better tax rates (21% vs. 25-40%), less bureaucracy, faster licensing

- Vermont lesson: Social equity through support, not rigid mandates

New York: 30%

- Vermont avoided New York disaster: No licensing collapse, no years-long delays

- Vermont lesson: Competent regulation baseline for any legal market success

Vermont's current 70%+ legal share after 30 months demonstrates strong policy foundation. With federal reform, Vermont could join 80%+ club within 36 months.

Timeline and Path Forward

Vermont's optimization follows phased approach:

Phase 1 (Current): Market Stabilization (2025-2026)

Duration: 12-18 months Objective: Prevent oversupply crisis while maintaining craft ecosystem

Actions:

- Maintain retail licensing pause in saturated markets (Burlington, Rutland, Montpelier)

- Strategic retail licensing for underserved regions (Northeast Kingdom, southern Vermont)

- Tier 1 cultivation remains open; larger tiers reopened selectively based on quarterly market assessments

- Cannabis Control Board develops geographic distribution rules (Act 166 mandate)

- Legislature considers delivery authorization or farmers market model

- Support existing businesses through technical assistance, cooperative marketing

Success Metrics:

- Wholesale prices stabilize (no crash below sustainable levels)

- Retail density remains 14-16 per 100K statewide (avoid further saturation)

- Small cultivator exit rate <10% annually

- Geographic access improves (municipalities served increases 30% → 40%+)

Phase 2 (Near-Term): Delivery and Access Expansion (2026-2027)

Duration: 12-18 months Objective: Fill geographic gaps without oversaturating core markets

Actions:

- Implement statewide delivery authorization or farmers market sales (Legislature 2026)

- Municipalities opt into delivery separately from retail

- Cannabis Control Board develops delivery tracking, ID verification requirements

- Prioritize delivery in municipalities without retail

- Consider online ordering integration (reservation + pickup or delivery)

- Expand municipal opt-in outreach (target 40%+ municipalities with retail/delivery)

Success Metrics:

- Legal market share increases 70% → 75-78%

- Rural access improves (delivery coverage reaches 85%+ of population)

- Consumer satisfaction increases (convenience, selection)

- Tourism sales maintain or increase despite future New Hampshire legalization

Phase 3 (Medium-Term): Federal Reform Integration (2027-2029)

Duration: 24-30 months Objective: Achieve 80%+ legal share through federal barrier elimination

Assumptions:

- Schedule III rescheduling occurs (280E eliminated)

- SAFE Banking Act passes (banking normalized)

- Timeline: Federal action 2027-2028 (optimistic scenario)

Actions:

- Vermont dispensaries implement card payment systems (SAFE Banking)

- Retail prices decline 12-18% immediately (280E elimination)

- Vermont decouples from 280E for state corporate income tax (increase small business competitiveness)

- Enforcement budget increases $8-12M annually (aggressive illicit supply interdiction)

- Cannabis Control Board reassesses licensing capacity post-federal reform

- Interstate commerce preparation begins (if authorized federally)

Success Metrics:

- Legal market share reaches 82-87%

- Annual sales reach $180-210M

- Tax revenue increases to $38-44M annually

- Vermont positioned as New England's highest-performing market

Phase 4 (Long-Term): Interstate Commerce and Export (2029+)

Duration: Ongoing Objective: Establish Vermont craft cannabis as premium regional/national brand

Assumptions:

- Federal interstate commerce authorized

- Consistent federal policy across states

- Market consolidation nationally (MSO dominance in some states, craft survival in others)

Actions:

- "Vermont Craft Cannabis" designation and marketing cooperative

- Export to New Hampshire, New York, Massachusetts, national markets

- Quality standards, organic certification, sustainability branding

- Tourism integration (Vermont ski resorts, autumn foliage, farm-to-table culture)

- Small cultivator support through export cooperative

- Vermont cannabis becomes economic development asset (like Vermont cheese, beer, maple syrup)

Success Metrics:

- Vermont craft cannabis commands 15-30% premium in export markets

- Small cultivators remain viable through premium pricing + export volume

- Vermont maintains 400+ independent cultivators (avoid MSO consolidation)

- Cannabis tourism generates $30-50M annually

Vermont's advantage: Legislative control allows phased, adaptive approach. Unlike states locked into ballot initiative constraints, Vermont adjusts policy annually based on market data and federal developments.

Economic Reality

Vermont's cannabis market size reflects small population but demonstrates strong per-capita performance.

Current State (2024-2025)

Market Sizing:

- Total Vermont cannabis market: $190-210M annually

- Legal market: $145M (2025 projected)

- Illicit market: $45-65M (estimated)

- Legal market share: 69-76%

Consumer Base:

- Vermont adults 21+: 515,000 (2024 estimate)

- Cannabis consumers (12-18% of adults): 62,000-93,000

- Average annual spend: $2,000-2,200 per consumer

- Tourism consumers: 15-20% of sales (New Hampshire, New York, Massachusetts residents)

Revenue Generation:

- Excise tax (14%): $20.3M (2025 projected)

- Sales tax (6%): $8.7M (2025 projected)

- Local option tax (1%): $0.8M (limited adoption)

- Total tax revenue: $29.8M (2025 projected)

- Revenue per capita: $46 per Vermont resident

- Percentage of General Fund: 0.5%

Employment:

- Direct cannabis jobs: 1,200+ (retail, cultivation, processing, testing, transport)

- Indirect jobs (supporting industries): 400-600 estimated

- Total: 1,600-1,800 jobs supported

- Average wage: $38,000-52,000 (range from retail to specialized cultivation)

Illicit Market Impact:

- Estimated illicit sales: $45-65M annually

- Untaxed revenue loss: $9.5-13.7M potential tax revenue

- Unregulated employment: 200-400 jobs in black market

- Safety risk: Untested products, no quality control, criminal activity

Optimized State (With Federal Reform, 2027-2029)

Market Sizing (Optimized):

- Total Vermont cannabis market: $200-230M annually

- Legal market: $180-210M

- Illicit market: $20-30M (residual)

- Legal market share: 85-90%

Consumer Base Expansion:

- Cannabis consumers: 75,000-105,000 (some new consumers, mostly illicit conversion)

- Average annual spend: $2,100-2,300 (stable, slight increase from selection/quality)

- Tourism consumers: Maintain 15-20% despite future New Hampshire legalization (Vermont quality/craft advantage)

Revenue Generation (Optimized):

- Excise tax (14%): $25.2-29.4M

- Sales tax (6%): $10.8-12.6M

- Local option tax (1%): $1.2-1.5M

- Total tax revenue: $37.2-43.5M

- Revenue per capita: $57-67 per Vermont resident

- Percentage of General Fund: 0.7-0.8%

Employment (Optimized):

- Direct cannabis jobs: 1,600-2,000

- Indirect jobs: 600-800

- Total: 2,200-2,800 jobs

- Wage improvement: $42,000-58,000 (more sustainable businesses, better wages)

Illicit Market Reduction:

- Illicit sales reduced to $20-30M (70-80% reduction from current)

- Recovered tax revenue: $18-25M additional annually vs. current

- Law enforcement savings: $2-3M annually (reduced cannabis-related enforcement)

- Public safety improvement: Fewer unregulated products, reduced criminal activity

Economic Multiplier:

- Every $10 in dispensary sales → $13-15 in broader economic activity

- Total economic impact (optimized): $260-315M annually

- 0.5-0.6% of Vermont GDP ($51.5B, 2024)

Budget Context

Vermont's cannabis revenue in perspective:

- Vermont General Fund: ~$2.2B (2024)

- Cannabis tax revenue: $29.8M (2025) = 1.4% of General Fund

- Optimized revenue: $37-44M = 1.7-2.0% of General Fund

Cannabis provides meaningful but not transformative revenue. Compare Vermont cannabis revenue to other Vermont revenue sources:

- Meals and rooms tax: $148M (2024)

- Sales and use tax: $485M (2024)

- Personal income tax: $960M (2024)

- Cannabis excise + sales: $29.8M (2025)

Cannabis ranks ~10th among Vermont revenue sources. Optimization increases ranking slightly but won't resolve major budget challenges.

However: For specific programs (substance misuse prevention, after-school programs), cannabis revenue provides substantial dedicated funding. $10M annually for substance misuse prevention (30% of excise tax) represents significant program expansion.

Conclusion

Vermont's cannabis journey demonstrates that good state policy creates strong foundation—but federal barriers determine ultimate ceiling.

The Green Mountain State implemented nearly every best practice:

- Legislative legalization allowing policy flexibility

- Moderate tax rates (21% total) avoiding Illinois/California mistakes

- Minimal geographic fragmentation compared to West Coast states

- Social equity through support rather than rigid mandates

- Competent regulation without bureaucratic excess

- Strong testing creating safety advantage over illicit market

Result: Vermont achieves 70%+ legal market share after just 30 months—outperforming many states with 5-10 year head starts.

Yet Vermont faces challenges exposing limits of state-only solutions:

- Oversupply from unlimited licensing threatens craft cultivator viability

- Geographic fragmentation (70% municipalities without retail) creates access gaps

- 280E federal tax penalty inflates retail prices 12-18%, preventing price optimization

- SAFE Banking absence forces cash operations, reducing consumer convenience, creating safety risks

- Border state competition (future New Hampshire legalization) threatens tourism advantage

Vermont's path forward requires coordinated state and federal action:

State Level:

- Strategic licensing management preventing oversupply while filling geographic gaps

- Delivery authorization or farmers market model improving rural access

- "Vermont Craft Cannabis" branding preparing for interstate commerce

- Continued policy adaptation based on market data

Federal Level:

- Schedule III rescheduling eliminating 280E (12-18% price reduction)

- SAFE Banking Act passage enabling card payments (5-8% legal share increase)

- Interstate commerce authorization allowing Vermont craft export

- Consistent federal framework removing legal uncertainty

With these combined actions, Vermont could reach 85-90% legal market share within 36-48 months—becoming New England's highest-performing market and national model for craft cannabis sustainability.

Vermont proves the cannabis policy thesis: Consumer choice drives market outcomes. Give consumers legal cannabis that costs 20-30% less than illicit (with federal reform), offers guaranteed safety and quality, provides convenient access, and backs enforcement against illegal operators—consumers overwhelmingly choose legal.

But make legal cannabis 40%+ more expensive through federal tax penalties, restrict banking forcing cash operations, leave rural communities without access, underfund illicit supply interdiction—even the best state policy cannot overcome these barriers.

The question for Vermont: Will federal reform arrive in time to prevent oversupply crisis and optimize the market state policy built? Or will Vermont join Oregon's cautionary tale—strong vision undermined by federal policy failure and market forces beyond state control?

About This Analysis

This prediction is based on the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error and r=0.968 correlation.

Resources:

- Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

- Framework methodology: The Black Market Death Equation

- Related analyses: Delaware, Rhode Island, Florida, Missouri, Hawaii

For Vermont policymakers, cannabis businesses, or investors seeking detailed analysis:

Comprehensive state-specific analysis available under commercial license, including:

- Exact market share predictions under multiple policy scenarios

- Delivery implementation framework and ROI analysis

- Craft cannabis branding and cooperative marketing strategies

- Licensing pause management and geographic distribution optimization

- Policy lever prioritization and sensitivity testing

- Revenue modeling and economic impact assessment

- Implementation roadmap for federal reform integration

- Interstate commerce preparation and export strategy

Contact: silentmajority420@proton.me | @The_Silent_420

The Silent Majority 420 is an anonymous cannabis policy analyst with 25 years of market participation. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0 (free use with attribution)