Washington DC Cannabis Market Analysis: The Capital Paradox—Congressional Prohibition in America's Most Progressive City

The nation's capital stands at a crossroads—voters overwhelmingly legalized cannabis in 2014, yet Congress blocks sales, creating a chaotic gray market in the shadow of the Capitol dome.

The Silent Majority 420 | November 2025

The DC Paradox: Democracy Denied

Drive through Washington DC's neighborhoods and you'll see them: storefronts with cannabis leaf imagery, "gifting" shops, pop-ups offering flower as a "bonus" with t-shirt purchases. This isn't a regulated cannabis market—it's a policy disaster created when federal lawmakers overrode the democratic will of DC voters.

In November 2014, 64.87% of District residents approved Initiative 71, legalizing possession of up to two ounces of cannabis and home cultivation of up to six plants. The margin was decisive—DC voted more strongly for legalization than Colorado (55.3%) or Washington State (55.7%) in 2012.

But there was a catch: Initiative 71 didn't authorize retail sales. DC's ballot initiative process doesn't allow measures requiring government spending. Establishing a regulated market would require the DC Council to pass legislation creating a licensing system, taxation framework, and regulatory oversight—all requiring appropriations.

Congress had other plans.

In December 2014, Maryland Representative Andy Harris attached a budget rider—now known as the "Harris Rider"—to the federal appropriations bill funding DC's government. The provision prohibits the District from spending any funds "to enact or carry out any law, rule, or regulation to legalize or otherwise reduce penalties associated with" any Schedule I controlled substance. Congress has renewed this rider in every budget since 2014, maintaining it through both Democratic and Republican control.

The result: DC residents can legally possess cannabis but have no legal way to purchase it. The initiative's provision allowing adults to "gift" up to one ounce created a loophole—businesses sell legal products (t-shirts, stickers, art) at inflated prices and include cannabis as a "gift." This gray market operates in legal limbo: not explicitly illegal under Initiative 71, but clearly circumventing the intent of federal prohibition.

Meanwhile, DC's neighbors offer fully legal markets. Maryland launched adult-use sales in July 2023, with dispensaries just miles from the DC border. Virginia legalized adult-use possession in 2021, though retail sales remain prohibited pending regulatory framework completion.

DC's medical cannabis program, operating since 2013, has become a workaround. The Medical Cannabis Self-Certification Emergency Amendment Act of 2022 allows DC residents 21 and older to register as medical patients without physician approval—essentially creating quasi-adult-use access. Registration surged: from 27,756 unique patients served in June 2025 to 32,440 by August 2025, according to the Alcoholic Beverage and Cannabis Administration (ABCA).

By August 2025, DC operated 85 licensed medical dispensaries for a city of 700,000+ residents—a density rivaling established adult-use markets. Yet monthly sales per dispensary average just $101,000, roughly half Maryland's average. Medical program sales through August 2025 totaled approximately $50.3 million year-to-date, compared to $30.8 million over the same period in 2024—a 63% increase driven by expanded licensing and self-certification.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error, cannot properly assess DC's market because DC doesn't have a legal adult-use market to measure. But the framework reveals something critical: IF Congress removed the Harris Rider and DC implemented regulated adult-use sales with evidence-based policy, the District could achieve 82-88% legal market share within 36-48 months—outperforming Maryland (68-73%) and Virginia (projected 70-76% if retail launches).

DC possesses exceptional advantages: geographic compactness, educated high-income population, progressive political culture, existing medical infrastructure, and tourist economy. The District that should be America's cannabis policy model instead serves as a case study in how federal overreach creates policy chaos.

The question isn't whether DC should have regulated adult-use sales—65% of voters already answered that. The question is: How long will Congress override DC democracy while chaos flourishes in the nation's capital?

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Important Note: The framework cannot accurately measure DC's current market because DC lacks a legal adult-use retail system. Medical self-certification creates quasi-adult-use access, but the gray market "gifting economy" operates outside any regulatory framework, making legal/illicit market share calculations impossible. This analysis focuses on DC's potential performance IF Congress removes barriers and DC implements regulated adult-use sales.

Current Status (2025): Policy Chaos in the Nation's Capital

DC's cannabis market exists in three parallel systems: legal medical, quasi-legal gifting economy, and traditional illicit market. None function optimally.

The Harris Rider: Democracy Overridden

Since December 2014, the "Harris Rider" has prohibited DC from spending funds to implement adult-use cannabis regulation. Named for Maryland Representative Andy Harris, the provision states:

"None of the Federal funds contained in this Act may be used to enact or carry out any law, rule, or regulation to legalize or otherwise reduce penalties associated with the possession, use, or distribution of any Schedule I controlled substance."

Because the rider specifically references Schedule I substances, proposed federal rescheduling of cannabis to Schedule III would technically eliminate this barrier. Congressional Research Service analysis confirms that rescheduling would permit DC to:

- Repeal local prohibitions on adult-use distribution and sales

- Establish comprehensive commercial regulation

- Implement taxation and licensing frameworks

- Regulate the previously unregulated gifting economy

Until then, DC Council cannot appropriate funds for adult-use regulation, regardless of voter support.

The Gifting Economy: Gray Market by Design

Initiative 71 legalized transferring up to one ounce of cannabis as a gift "without remuneration." Enterprising businesses exploited this language: customers purchase t-shirts, art, or stickers for $50-300, receiving cannabis as a "gift" with their purchase.

The gifting model operates in legal gray area:

- Not explicitly illegal under Initiative 71 (transfer without remuneration)

- Arguably illegal under traditional commerce (cannabis clearly motivates transaction)

- Unregulated: No testing requirements, no age verification, no taxation

- Variable quality: Products range from safe to potentially dangerous

- Federal liability: Still violates federal Controlled Substances Act

By April 2025, DC enforcement closed 50 illegal gifting shops, seizing 529.9 pounds of cannabis, 82.2 pounds of entheogenic mushrooms, 17.4 pounds of mushroom edibles, 25.6 pounds of THC wax, and non-registered firearms from nine locations. Twenty additional shops closed voluntarily as enforcement intensified.

Yet gifting shops continue proliferating. With no legal adult-use purchase option, consumers have limited choices: register as medical patients, buy from gifting shops, or access traditional illicit markets.

The Medical Program: Rapid but Chaotic Expansion

DC's medical cannabis program, authorized by Initiative 59 in 1998 but blocked by Congress until 2009, finally sold its first products in 2013. For years, the program struggled with limited access, high costs, and restrictive qualifying conditions.

The Medical Cannabis Self-Certification Emergency Amendment Act of 2022 transformed everything. DC residents 21+ can now register as medical patients through online self-certification—no physician recommendation required. This effectively creates adult-use access through medical channels.

August 2025 Program Statistics (ABCA Official Data):

DC Resident Patients:

- Unique patients served: 19,052 (up from 13,025 in June)

- Total unique sales: 49,479

- Average sale: $65 (in-store), $144 (delivery)

- Monthly sales: $3.2 million

Non-Resident Patients (Reciprocity):

- Unique patients: 2,105 (down from 2,274 in June)

- Monthly sales: $494,263

Non-Resident Patients (Self-Certified Temporary):

- Total registered: 130,556 (cumulative)

- Unique patients who purchased in August: 11,284

- Monthly sales: $1.75 million

- Top states: Virginia (3,767 registrations), Maryland (1,611), North Carolina (783)

Total Program:

- Total unique patients registered: 73,407

- Dispensaries: 85 operational

- Monthly sales (August 2025): $5.45 million at retail

- Year-to-date sales through August: ~$50.3 million (vs. $30.8 million same period 2024)

Market Concentration:

- Average monthly sales per dispensary: ~$101,000

- Contrast: Maryland dispensaries average ~$200,000/month

- Flower dominates: 603 pounds sold in August (55-60% of sales)

- Vape cartridges second: 20,629 units ($1.03 million)

The numbers tell a story: DC's medical program is rapidly expanding but oversaturated. The District licensed 85 dispensaries for 700,000 residents (12.1 stores per 100K population)—higher density than Colorado (10.8 per 100K) or Nevada (9.2 per 100K), states with mature adult-use markets serving larger populations.

Many dispensaries struggle financially. Average monthly sales of $101,000 cannot sustainably support full operations, particularly with Internal Revenue Code Section 280E preventing normal business deductions, creating effective federal tax rates of 40-70%.

Visitor Program: Cannabis Tourism Without Regulation

DC's self-certification program allows temporary registration for non-residents. Virginia and Maryland residents comprise the majority of temporary registrations—individuals from neighboring states where adult-use cannabis is legal or quasi-legal coming to DC for access.

This creates perverse situation: visitors from Virginia (where adult-use possession is legal but retail sales aren't available) and Maryland (where adult-use sales are legal) register as DC medical patients for convenience or price advantages.

In August 2025, 11,284 temporary non-resident patients made purchases totaling $1.75 million. The top five states for temporary registrations:

- Virginia: 3,767 registrations

- Maryland: 1,611 registrations

- North Carolina: 783 registrations

- Texas: 391 registrations

- Florida: 367 registrations

DC essentially operates as a regional cannabis hub despite lacking legal adult-use framework—a testament to pent-up demand and policy dysfunction in surrounding states.

Enforcement: Closing Gray Market, Expanding Licensed Market

The Alcoholic Beverage and Cannabis Administration intensified enforcement in 2024-2025, working with Metropolitan Police Department to close unlicensed operations. Through August 2025:

- 50 illegal shops permanently closed and padlocked

- 20 additional shops closed voluntarily

- 7 unlicensed facilities closed in August alone

- 20 scheduled inspections in August

- 2,891 pounds of cannabis waste destroyed (August)

Simultaneously, DC expanded licensed dispensary count from 17 in February 2025 to 85 by August 2025—a 400% increase in six months. This rapid licensing aimed to:

- Provide legitimate access points reducing gray market appeal

- Generate tax revenue (6% sales tax on medical cannabis)

- Demonstrate self-regulation capability to Congress

- Position infrastructure for adult-use transition if Harris Rider lifts

The strategy shows early success: medical sales increased 63% year-over-year through August 2025, while aggressive enforcement reduced unregulated gifting market. But without legal adult-use sales, gray market will persist—consumers prefer regulated access but lack legal purchasing options.

DC's Structural Advantages: Why the District Should Lead, Not Lag

Despite congressional barriers, DC possesses characteristics that would enable exceptional legal market performance if prohibition ended.

Geographic Compactness: Maximum Efficiency

Total area: 68.3 square miles Population: ~700,000+ (as of 2025) Population density: 10,200+ per square mile

DC is among America's most geographically concentrated jurisdictions. Compare:

- DC: 68.3 square miles serving 700K residents

- Rhode Island: 1,214 square miles serving 1.1M (geographic challenges)

- Montana: 147,040 square miles serving 1.1M (massive rural access challenges)

- Nevada: 110,577 square miles, but 73% population in Las Vegas metro (concentrated like DC)

Framework significance: Geographic concentration reduces retail density requirements and delivery costs. DC's compact footprint means 40-50 strategically located dispensaries could provide convenient access to 95%+ of residents. Current density of 85 dispensaries (12.1 per 100K) exceeds optimal levels but positions infrastructure for adult-use transition.

Nevada demonstrates this advantage: Las Vegas metro concentration (73% of state population) enables 75-80% legal market share with moderate dispensary count. DC's even tighter concentration would amplify this effect.

Affluent, Educated Population: Premium Market Demographics

Median household income: $101,027 (2023) Bachelor's degree or higher: 64% of residents (vs. 34% U.S. average) Professional employment: High concentration of government, legal, consulting, tech sectors

DC's demographics favor legal market success:

- Higher income reduces price sensitivity (can afford legal market premium over illicit)

- Education correlates with preference for tested, regulated products

- Professional employment increases risk aversion (criminal records career-disqualifying)

- Progressive political culture embraces cannabis normalization

Research demonstrates high-income consumers show stronger preference for legal channels, accepting 10-20% price premiums for quality assurance and legal peace of mind. DC's affluent population would support premium pricing strategies enabling sustainable business operations.

Compare to California, where vast income inequality creates persistent price-sensitive consumer segment sustaining illicit markets. DC's relative income equality (by urban standards) reduces this challenge.

Progressive Political Culture: Social Equity Priority

Initiative 71 approval: 64.87% (2014) Demographic composition: 44% Black, 12% Hispanic/Latino Political orientation: Strongly progressive (2020 presidential vote: 92.1% Biden)

DC's progressive electorate strongly supports cannabis legalization, social equity, and criminal justice reform. This creates political will for:

- Automatic expungement of past cannabis convictions

- Social equity licensing preferences

- Community reinvestment programs

- Restorative justice initiatives

Unlike states where legalization remains politically contentious (Texas, Wyoming), DC has overwhelming voter support and political infrastructure to implement comprehensive equity programs. This isn't just moral imperative—it's political mandate.

Illinois demonstrates both opportunity and risk: strong social equity rhetoric but underfunded implementation created symbolic program without substantive impact. DC could learn from these mistakes, properly funding equity initiatives from day one.

Existing Medical Infrastructure: Turnkey Transition

Unlike states starting from scratch, DC already operates:

- 85 licensed dispensaries with established supply chains

- Cultivation facilities producing for medical market

- Testing laboratories ensuring product safety

- Regulatory oversight (ABCA) with operational experience

- Patient registration system (73,407+ registered)

- Delivery infrastructure serving all eight wards

Michigan successfully leveraged existing medical infrastructure for rapid adult-use rollout in 2019, achieving 85% legal market share within four years. DC's even more mature medical system (operating since 2013) would enable faster, smoother transition.

The current oversaturation challenge (85 dispensaries, $101K average monthly sales) would resolve immediately with adult-use authorization. Dispensaries struggling on medical-only volume would become financially sustainable serving broader adult-use population. DC's current "too many dispensaries" problem becomes competitive advantage enabling immediate widespread access.

Tourism Economy: Cannabis-Friendly Destination

Annual visitors: 24+ million (pre-pandemic levels returning 2025) Tourism economic impact: $8+ billion annually Hotel rooms: 30,000+ across metro area Visitor profile: Domestic travelers (majority), international guests, business conventions

DC's tourism economy creates unique opportunity. Nevada demonstrates tourism-driven cannabis market success: Las Vegas leverages 42+ million annual visitors for robust retail sales, with tourists accounting for 40-50% of dispensary revenue.

DC tourism profile differs from Las Vegas (cultural/educational vs. entertainment gambling), but cannabis-friendly hospitality could attract specific demographic: younger professionals, cannabis enthusiasts, policy advocates. National Cannabis Festival already draws ~30,000 attendees annually—imagine expansion with legal retail.

States benefit from DC tourism cannabis spending:

- Maryland dispensaries near DC border serve District residents and Virginia visitors

- Virginia (when retail launches) will capture DC consumers

- DC loses tourism dollars and tax revenue

With legal adult-use sales, DC would capture these revenues while enhancing tourism appeal for cannabis-friendly travelers choosing between East Coast destinations.

Federal District Status: Double-Edged Sword

DC's unique constitutional status creates both challenge and opportunity:

Challenge: Congress exercises oversight DC Council cannot override. Harris Rider demonstrates this power—voter-approved Initiative 71 implementation blocked by federal appropriations restriction. No state faces equivalent federal interference.

Opportunity: Federal policy changes would immediately apply. If Congress removes Harris Rider or cannabis reschedules to Schedule III, DC gains regulatory authority instantly. No state constitutional amendments required. No voter referendums needed. DC Council can act immediately.

This means DC policy landscape could transform dramatically within months if:

- Cannabis reschedules to Schedule III (Harris Rider no longer applies)

- Congress explicitly removes Harris Rider from appropriations

- Federal legalization occurs (preempts rider entirely)

DC currently suffers maximum federal control. But federal policy shift would enable maximum flexibility to implement evidence-based regulation quickly.

Predicted Market Outcomes: IF Congress Removes Barriers

The framework allows prediction of DC's market performance under different policy scenarios, contingent on elimination of federal barriers.

Optimized Scenario: Capital Excellence

Policy Assumptions:

- Congress removes Harris Rider OR cannabis reschedules to Schedule III

- DC Council implements comprehensive adult-use regulation

- Federal Schedule III eliminates 280E tax burden

- SAFE Banking Act enables normal financial services

- Total state tax rate: 15-18% (competitive but sustainable)

- Retail licensing: Expand from current 85 medical to 95-110 adult-use dispensaries

- Delivery: Maintain current infrastructure (already operational)

- Testing standards: Maintain current medical program requirements

- Social equity licensing: Well-funded capital access ($15-25M fund)

- Enforcement: $3-5M annual budget targeting illicit operations

Framework Inputs:

- Price competitiveness: g = -0.20 (legal 20% cheaper than illicit)

- Illicit DC cannabis: $9-11/gram typical

- Legal with 15% tax, no 280E, bulk pricing: $7.20-8.80/gram

- Federal reform eliminates 280E burden, enabling competitive pricing

- Access density: D = 0.92 (95-110 dispensaries + delivery covers 98%+ population)

- Current: 12.1 dispensaries per 100K (85 stores)

- Optimized: 13.6-15.7 per 100K (95-110 stores)

- Geographic compactness means every resident within 10-minute transit

- Safety/quality: S = 0.90 (maintain medical program testing standards, professional retail)

- DC's educated population values tested products

- Professional retail environment (not warehouse-style budget shops)

- Convenience: F = 0.82 (SAFE Banking enables cards, existing delivery, tourist-friendly)

- Card payments available (major friction reducer vs. cash-only)

- Hotel-friendly policies for tourists

- Online ordering + delivery (already operational)

- Enforcement: E = 0.75 (continued ABCA/MPD coordination, focus on illegal operations)

- DC already demonstrated enforcement capability (70 shop closures)

- Redirect resources from arrests to supply interdiction

- Fragmentation: F_frag = -0.05 (minimal—no separate jurisdictions, single city government)

Predicted Outcomes:

- Transaction share: 87-92% (users choosing legal over illicit)

- Volume share: 82-88% (accounting for heavy user patterns)

- Timeline: 36-48 months to reach steady state (faster than average due to existing infrastructure)

Economic Impact:

- Adult cannabis consumers: 90,000-120,000 (13-17% of adults 21+, higher than national average due to demographics)

- Legal market size: $145-185M annually (mature market, DC residents only)

- Tourist market: $35-50M annually (estimated 8-12% of visitors purchasing)

- Combined market: $180-235M annually

- State tax revenue: $27-42M annually (at 15-18% rate)

- Federal taxes: $15-25M annually (income taxes, payroll taxes)

- Jobs: 1,800-2,400 direct + indirect

- Illicit market reduction: From estimated $95-135M currently to $15-25M (85-90% reduction)

Comparable Performance:

DC would achieve outcomes similar to:

- Michigan: 85% legal share (current best)

- Massachusetts: 78-82% legal share (established East Coast market)

- Nevada: 75-80% legal share (tourism-driven)

DC's combination of geographic compactness, affluent educated population, existing infrastructure, and progressive culture positions it for top-tier performance—IF federal barriers lift and evidence-based policy is implemented.

Failed Scenario: High Taxes, Low Performance

Policy Design:

- DC Council implements adult-use regulation with Illinois-style mistakes

- High tax rate: 28-35% (attempting to maximize per-unit revenue)

- License restrictions: Artificial scarcity, extended delays

- Social equity: Rhetoric without sufficient capital access

- 280E remains in effect (no federal Schedule III)

- SAFE Banking not passed (continued cash operations)

Predicted Outcomes:

- Transaction share: 62-68%

- Volume share: 55-62%

- Legal market: $95-135M annually

- Tax revenue: $27-41M (high rate, smaller base—similar to optimized but less efficient)

- Illicit market: $40-65M persistent (limited reduction)

DC becomes Illinois East: high taxes undermine legal market competitiveness despite progressive values and good intentions. Social equity remains symbolic rather than transformative.

Most Likely Scenario: Gradual Implementation

Given DC's political culture and existing infrastructure, moderate-to-good implementation most probable:

Policy Design:

- Congress removes barriers (2026-2028 timeline probable)

- DC Council takes measured approach: studied rollout, stakeholder input

- Moderate taxes: 18-22% (balancing revenue and competitiveness)

- Leverage existing medical dispensaries for dual licensing

- Phase-in: Medical conversion first (6 months), new applicants later (12-18 months)

- Strong testing/regulatory oversight (DC strength)

- Well-intentioned social equity with moderate funding ($10-18M)

Predicted Outcomes:

- Transaction share: 78-84%

- Volume share: 73-80%

- Timeline: 48-60 months (slower rollout than optimized, but methodical)

- Legal market: $155-200M annually (mature state)

- Tax revenue: $31-40M annually

- Jobs: 2,000-2,600

This represents good-but-not-optimal performance: Better than Illinois (55-60%), New York (30-35%), approaching Massachusetts (78-82%). DC's progressive culture and existing expertise produce competent implementation even if not perfectly optimized.

The Federal Barriers: Why DC Can't Succeed Alone

DC faces unique federal constraints no state experiences.

The Harris Rider: Congressional Budget Provision

Since 2014, this appropriations rider prohibits DC from spending funds to implement adult-use cannabis regulation. The provision appears annually in federal spending bills, renewed by Congress regardless of party control.

Representative Andy Harris (R-MD), original sponsor, represents Maryland's Eastern Shore—a conservative district contrasting with DC's progressive politics and Harris's own state's adult-use legalization. Harris argued DC legalization would:

- Create public safety concerns

- Increase drugged driving

- Undermine federal government's symbolic position in capital city

The reality: Harris Rider created exact problems it claimed to prevent. Without regulated sales, DC developed chaotic gray market with no quality control, no age verification, no taxation. Meanwhile, Maryland legalized adult-use cannabis in 2023, with Harris's own constituents able to purchase legally—yet he maintains DC prohibition.

Political Path to Removal:

Three scenarios remove the barrier:

- Congressional action: Democrats control appropriations, remove rider proactively

- Probability: Moderate (requires political will, Harris opposition minimal in Democratic Congress)

- Timeline: 2026-2028 if Democrats maintain/regain appropriations control

- Cannabis rescheduling to Schedule III: Harris Rider specifically references Schedule I substances

- Congressional Research Service confirms Schedule III reclassification would eliminate legal basis for rider

- Probability: High (DEA rescheduling proposal advanced 2024-2025)

- Timeline: 2025-2027 probable

- Federal legalization: Preempts all state/local prohibition authority

- Probability: Lower medium-term, likely long-term

- Timeline: 2028-2032+

Most likely: Cannabis reschedules to Schedule III (2026-2027), eliminating Harris Rider's legal foundation. DC Council could then appropriate funds for adult-use regulation without federal interference.

The 280E Problem: Federal Tax Discrimination

Internal Revenue Code Section 280E prohibits cannabis businesses from deducting ordinary expenses:

Impact on Hypothetical DC Dispensary:

Normal business (without 280E):

- Revenue: $1,500,000

- COGS: $450,000 (deductible)

- Operating expenses: $850,000 (rent, labor, security, utilities, marketing)

- Profit: $200,000

- Federal tax (21%): $42,000

- Net profit: $158,000

Cannabis business (with 280E):

- Revenue: $1,500,000

- COGS (deductible): $450,000

- Operating expenses (NON-deductible): $850,000

- Taxable income: $1,050,000 (not $200,000)

- Federal tax: $220,500

- Actual profit: -$20,500 (loss despite $200K operating profit)

280E forces DC dispensaries to raise prices 15-22% just to survive federal tax burden. DC consumers pay this premium. Legal market competitiveness suffers.

DC's current 85 dispensaries averaging $101,000 monthly sales (~$1.2M annually) operate on razor-thin margins or losses. Many survive only through:

- Vertical integration (cultivation profits offset retail losses)

- Investor subsidies (losing money but building position for adult-use transition)

- Creative accounting (aggressive COGS categorization)

Solution: Schedule III rescheduling eliminates 280E. DC businesses can deduct normal expenses. Retail prices drop 12-18%. Legal market becomes dramatically more competitive versus illicit alternatives.

This single policy change—federal rescheduling—would transform DC's cannabis economics more than any local policy intervention.

The SAFE Banking Problem: Cash Operations and Crime

Without SAFE Banking Act passage:

- Cash-only operations: Most banks refuse cannabis accounts (federal prohibition risk)

- Security costs: $50,000-180,000 annually per location (armed guards, safes, armored transport)

- Consumer friction: Research from Federal Reserve payment systems analysis shows cash-only operations reduce transaction frequency 18-25%

- Crime risk: Cash-heavy businesses attract robbery

- No credit building: Minority entrepreneurs cannot establish credit, limiting capital access

- Tax complications: Cash reconciliation challenges, IRS audit risks

DC's educated, professional population particularly values card payments. Credit/debit card usage in DC (~88% of transactions) exceeds national average (84%). Cash-only dispensaries create friction for target demographic.

Maryland adult-use market demonstrates impact: dispensaries with card payment options average 59% more transactions than cash-only, per industry data. DC would show even more dramatic effect given population preferences.

Solution: SAFE Banking Act enables normal banking services, card payments, reduced friction. Convenience factor (F in framework) increases from ~0.55 (cash-only) to ~0.82 (full banking), translating to 5-8 percentage point increase in legal market share.

DC Statehood: Ultimate Solution

DC's lack of statehood creates all these problems. If DC achieved statehood, Congress would lose appropriations authority over local cannabis policy—Harris Rider would become irrelevant.

Statehood Status:

- House passed DC statehood bill (H.R. 51) in 2021: 216-208 vote (party-line)

- Senate has not acted (requires 60 votes, Republican opposition)

- Public support: 54% of Americans favor DC statehood (Gallup 2023)

- DC residents support: 86% (2016 statehood referendum)

Statehood timeline: Uncertain. Requires Democratic control of House, Senate (60 votes or filibuster reform), and presidency. Politically difficult but growing support.

Cannabis policy is minor issue in statehood debate, but exemplifies congressional overreach statehood would resolve. DC residents overwhelmingly supported legalization (64.87%), yet Congress blocks implementation—taxation without representation applied to cannabis policy.

Policy Recommendations: For DC Council and Congress

Evidence-based recommendations for when federal barriers lift.

For DC Council: Preparing for Post-Prohibition Future

DC Council cannot implement adult-use regulation while Harris Rider persists. But Council can prepare framework for rapid deployment when barriers lift.

Priority #1: Comprehensive Regulatory Draft

Develop detailed adult-use regulation ready for immediate implementation:

- Draft legislation: Complete bill text with licensing, taxation, oversight, social equity provisions

- Stakeholder input: Medical operators, social equity advocates, law enforcement, community groups

- Legal review: Ensure framework survives constitutional challenges, federal scrutiny

- Learn from others: Study Massachusetts, Michigan, New Jersey successes; Illinois, New York, California failures

When Congress acts or cannabis reschedules, DC should be ready to implement regulation within 90-180 days, not 18-24 months. Nevada prepared well: when voters approved legalization (November 2016), state implemented regulation rapidly (July 2017). DC should follow this model.

Priority #2: Competitive Tax Structure

Recommendation:

- State excise tax: 12-15%

- Existing sales tax: 6% (already applies to medical)

- Total state burden: 18-21%

- No local option: DC is single jurisdiction (no fragmentation risk)

Rationale: Revenue optimization comes through volume (market share) not rates. Lower taxes → lower prices → higher legal share → more transactions → more total revenue.

DC must compete with:

- Maryland: 9% excise tax, ~15% total (moderate pricing)

- Virginia: TBD (adult-use retail pending, but likely competitive)

- Illicit market: Zero taxes

Tax rates above 25% ensure persistent black market. DC should target 18-22% sweet spot—high enough for revenue, low enough for competitiveness.

Research across 24 states demonstrates cannabis consumers are highly price-sensitive. Every 1% tax increase reduces legal market choice probability ~0.8%. At 30% tax burden, legal market loses 15-25 percentage points versus 18% burden.

Priority #3: Leverage Existing Medical Infrastructure

DC already has 85 licensed dispensaries, testing labs, cultivation facilities. Don't start from scratch—transition systematically:

Phase 1 (Months 1-6): Medical Conversion

- Existing medical dispensaries apply for dual licensing

- Priority processing (established operators, proven compliance)

- Maintain medical patient priority (dedicated hours, dedicated inventory)

- Target: 60-75 dual-license dispensaries operational within 6 months

Phase 2 (Months 6-18): New Applicants

- Open adult-use licensing to new applicants

- Social equity preference points (50% of new licenses)

- Capital access fund ($15-25M for loans, technical assistance)

- Target: 95-110 total dispensaries operational within 18 months

Phase 3 (Month 18+): Market Maturation

- Monitor density, adjust licensing as needed

- Course-correct based on early data

- Expand operating hours, delivery zones

- Refine taxation based on price competitiveness data

This phased approach provides immediate access (existing dispensaries) while creating social equity opportunities (new licenses) without Illinois-style delays (2020 legalization, still licensing new dispensaries 2025).

Priority #4: Robust Social Equity Program

DC's demographics demand strong social equity focus. The District's enforcement historically impacted Black and Hispanic communities disproportionately despite similar usage rates across groups.

Automatic Expungement:

- All cannabis-related convictions cleared immediately upon adult-use implementation

- No petition process (automatic = no barriers to access)

- Restore voting rights, employment eligibility, housing access

- Model: Illinois expunged 770,000+ records (most transformative component)

Social Equity Licensing:

- 50% of new licenses reserved for equity applicants

- Preference for individuals with cannabis convictions or arrests

- Preference for residents of high-enforcement wards (Wards 7, 8 particularly impacted)

- Residency requirement: 3+ years DC residence (prevent MSO takeover)

Well-Funded Capital Access:

- $15-25M fund for low-interest loans, grants

- $50,000-150,000 grants per licensee (real capital, not token amounts)

- Technical assistance: Business planning, compliance, operations, accounting

- Ownership transfer restrictions: Prevent MSO buyouts of struggling equity licensees

Revenue Reinvestment:

- 30-40% of cannabis tax revenue to equity communities

- Job training, education scholarships, small business development

- Youth programs, mental health services, infrastructure

- Measurable outcomes: Track employment, entrepreneurship, community wealth

Illinois demonstrates failure mode: Strong equity rhetoric, insufficient capital ($30M for entire state program, spread across hundreds of applicants). Many equity licensees failed to open or sold to MSOs within 18 months. DC must learn from this—fund programs properly or don't create them at all.

Priority #5: Tourist-Friendly Framework

DC receives 24+ million visitors annually—significant revenue opportunity if properly designed:

Visitor Policies:

- Maintain self-certification temporary registration (already operational)

- Streamline process: Online registration, instant approval

- Purchase limits: Reasonable daily limits (match resident limits)

- Hotel-friendly: Allow possession in hotel rooms (private property owner discretion)

- Public consumption: Maintain prohibition but create licensed consumption lounges

- Licensed on-site consumption: Social consumption spaces in designated establishments

Nevada demonstrates tourist market success: 40-50% of dispensary revenue from visitors. DC won't match Vegas levels (different tourism profile), but 20-30% visitor revenue share achievable—$35-50M annually.

Tourism revenue has political advantage: Collected from non-residents, minimal impact on local community, enhances DC's appeal versus other East Coast destinations.

For Congressional Delegation: Federal Reform Advocacy

DC's non-voting House delegate (Eleanor Holmes Norton) and advocates should prioritize federal reform removing barriers.

Priority #1: Remove Harris Rider

Specific asks for appropriations process:

- Omit Harris Rider from FY2026+ appropriations bills

- If included, advocate for removal in conference committee

- Frame as democracy issue: 64.87% of DC voters approved Initiative 71

- Cite failed policy: Gray market chaos Harris Rider created

- Comparison: Maryland (Harris's own state) has legal adult-use

Political strategy: Harris is one member. Democratic control of appropriations enables removal. Make it embarrassing to maintain prohibition in nation's capital while 24 states have adult-use legalization.

Priority #2: Support Schedule III Rescheduling

Cannabis rescheduling to Schedule III would eliminate Harris Rider's legal foundation. DC delegation should:

- File Congressional comment supporting rescheduling during DEA review period

- Publicly advocate for rescheduling as democracy issue

- Emphasize Schedule III enables DC self-governance on cannabis

- Coordinate with national reform organizations (NORML, MPP, Drug Policy Alliance)

Rescheduling doesn't require Harris's cooperation—administrative process through DEA. DC benefits immediately when final rule publishes.

Priority #3: SAFE Banking Act

Co-sponsor and actively advocate for SAFE Banking Act passage:

- Enables normal banking for DC cannabis businesses

- Reduces crime (less cash on premises)

- Improves consumer convenience (card payments)

- Supports social equity (credit access for entrepreneurs)

- Bipartisan support (passed House multiple times)

SAFE Banking has strongest bipartisan support of any cannabis reform. DC delegation should make this legislative priority.

Priority #4: Full Federal Legalization

Long-term goal: Remove cannabis from Controlled Substances Act entirely.

- Co-sponsor comprehensive legalization bills

- Frame as racial justice issue (DC enforcement disparities mirror national patterns)

- Economic argument: Legal market generates tax revenue, creates jobs

- States' rights argument: Federal prohibition prevents DC self-governance

Federal legalization timeline uncertain (2028-2035+ probable), but building support now creates political momentum.

For Maryland and Virginia: Regional Coordination

DC's neighbors have opportunity to support or hinder DC reform.

For Maryland:

Maryland legalized adult-use in 2023. Representative Harris represents Maryland district, yet maintains DC prohibition. Maryland delegation should:

- Publicly oppose Harris Rider (fellow Marylanders blocking DC democracy)

- Coordinate regional policy: Reciprocity agreements, tax harmonization

- Support DC statehood (ends congressional interference)

For Virginia:

Virginia legalized adult-use possession (2021) but hasn't implemented retail sales. Virginia should:

- Launch adult-use retail (bills pending annually)

- Coordinate with DC, Maryland on regional standards

- Recognize DC's medical program offers quasi-adult-use access, undermining Virginia's own policy goals

Regional coordination benefits all three jurisdictions: Reduces cross-border shopping, harmonizes enforcement, creates DMV cannabis corridor attracting tourism and investment.

Comparison to Other Markets

DC's unique situation makes direct comparison challenging, but framework reveals potential performance tier.

Top-Performing Markets (80%+ Legal Share)

Michigan (85% legal share):

- Strategy: Competitive pricing, rapid licensing, statewide delivery

- Tax burden: 16% total (moderate)

- Result: Best Midwest market, steady growth

Massachusetts (78-82%):

- Strategy: Methodical rollout, high standards, competitive pricing

- Tax burden: 17-20% (state + local)

- Result: Strong East Coast market despite conservative culture

Colorado (73-78%, improving):

- Strategy: First mover, learning through iteration, competitive pricing

- Tax burden: 15% + local

- Result: Mature market, continuous optimization

DC Potential: With optimized policy, DC should perform at Michigan/Massachusetts tier (82-88% legal share). Geographic compactness, affluent population, existing infrastructure all favor top-tier outcomes.

Mid-Tier Markets (60-75%)

Nevada (75-80%):

- Strategy: Tourism-driven, high quality, moderate pricing

- Challenge: Geographic dispersion outside Vegas

- Result: Strong market with tourism advantage

New Jersey (65-70%):

- Strategy: Rushed launch, moderate taxes, improving

- Challenge: New York competition, initial policy mistakes

- Result: Mid-tier, trending upward

Washington State (65-70%):

- Strategy: Early success, but stagnated

- Challenge: Oregon price competition, no delivery, geographic fragmentation

- Result: Mature but could optimize further

DC Risk: If DC implements high taxes (Illinois-style mistakes), performance drops to 62-68% range—mid-tier at best.

Struggling Markets (30-60%)

Illinois (55-60%):

- Problem: High taxes (25-40%), price uncompetitive

- Result: Persistent black market, legal market underperforms

- Lesson: Progressive values + bad tax policy = failure

California (50%):

- Problem: Local bans (61% of population), high taxes, weak enforcement

- Result: Fragmented market, illicit dominates

- Lesson: Early mover advantage wasted through dysfunction

New York (30-35%):

- Problem: Delayed licensing, enforcement gaps, illicit market entrenched

- Result: Policy crisis, legal market struggling

- Lesson: Incompetent implementation creates disaster

DC Must Avoid: Illinois and New York represent failure modes DC must study and reject. Both started with progressive intentions, good demographics, strong political support—then botched implementation through high taxes, licensing delays, and weak enforcement.

DC has advantages Illinois and New York lack:

- vs. Illinois: Geographic compactness (no fragmentation), no home grow entitlement creating competing supply

- vs. New York: Existing infrastructure (85 dispensaries ready to transition), enforcement capability (70 shop closures demonstrate will), smaller market size (easier to manage)

But DC risks repeating their mistakes if Council prioritizes revenue-per-unit over market share, or creates symbolic social equity without proper funding.

Where DC Fits: Top Tier or Disappointment?

Framework analysis suggests:

IF Optimized Policy:

- Legal market share: 82-88%

- Performance tier: Top 5 nationally

- Comparable to: Michigan, Massachusetts

- National model: Capital city demonstrates cannabis regulation success

IF Poor Policy:

- Legal market share: 55-65%

- Performance tier: Mid-tier, below potential

- Comparable to: Illinois, Washington State

- Wasted opportunity: Progressive city fails due to tax greed or implementation incompetence

DC has every structural advantage. The only question is whether policymakers will learn from other markets' experiences and implement evidence-based regulation, or repeat predictable mistakes.

Timeline and Path Forward

When will DC implement adult-use regulation?

Short-Term (2025-2026): Harris Rider Status Quo

Likelihood: VERY HIGH (90%+)

Federal barriers persist:

- Harris Rider renewed in FY2026 appropriations (probable)

- Cannabis rescheduling delayed (DEA review ongoing but slow)

- Statehood not advancing (Senate obstacles)

DC continues current system:

- Medical program expansion (85+ dispensaries, self-certification)

- Gifting economy operates in gray area

- Enforcement targets unlicensed operations

- Tax revenue: $3-5M annually (medical 6% sales tax only)

- Economic opportunity unrealized

Federal policy shift required before DC can act. Timeline depends on:

- Cannabis Rescheduling (Most Probable):

- DEA rescheduling proposal under review

- Public comment period, final rule publication

- Timeline: Late 2025-2027 probable

- Congressional Research Service confirms Schedule III eliminates Harris Rider legal foundation

- Congressional Rider Removal:

- Requires Democratic appropriations control

- Political will to override Harris opposition

- Timeline: 2026-2028 if Democrats regain House/maintain Senate

- Federal Legalization:

- Long-term solution but least probable short-term

- Timeline: 2028-2032+ more realistic

Most likely catalyst: Cannabis rescheduling to Schedule III (2026-2027), enabling DC regulatory action.

Medium-Term (2027-2029): Post-Prohibition Transition

Likelihood: HIGH (70-80%)

Assuming federal barriers lift 2026-2027:

2027: Legislative Framework

- DC Council passes comprehensive adult-use regulation

- Stakeholder input, legal review, final bill passage

- Licensing applications open

- ABCA ramps up enforcement, oversight capacity

- Timeline: 6-12 months legislation → implementation

2028: Market Launch

- Phase 1: Existing medical dispensaries transition to dual-license (60-75 stores)

- Phase 2: New adult-use applications, social equity licensing (20-35 additional stores)

- Initial sales: $8-15M monthly (building phase)

- Legal market share: 45-60% (early stage, ramping up)

2029: Growth Phase

- Dispensary network expands to 95-110 locations

- Delivery infrastructure scales

- Enforcement targets remaining illicit operators

- Sales: $12-18M monthly

- Legal market share: 70-80% (maturing)

Long-Term (2030+): Market Maturation

2030-2032: Steady State Achievement

Market reaches maturity:

- 95-110 dispensaries operational (optimal density)

- Legal market share: 82-88% (optimized scenario)

- Sales: $15-20M monthly ($180-240M annually including tourists)

- Tax revenue: $27-42M annually

- Jobs: 1,800-2,400 sustained

- Illicit market: Reduced to 12-18% (persistent but marginal)

Performance Indicators:

Year 1 (2028): 45-60% legal share (building) Year 2 (2029): 70-80% legal share (growing) Year 3 (2030): 78-85% legal share (maturing) Year 4+ (2031+): 82-88% legal share (optimized)

Timeline assumes:

- Federal reform 2026-2027

- Competent DC implementation

- Federal Schedule III + SAFE Banking

- No major policy mistakes

Risk Factors:

- Federal reform delayed beyond 2027

- DC implements Illinois-style high taxes

- Social equity underfunded

- Enforcement deprioritized

- Political resistance emerges

Most likely overall timeline: Adult-use implementation 2028-2029, market optimization 2030-2032. DC will not be first-mover (24 states already legalized), but benefits from learning other markets' experiences.

Economic Reality: What DC Sacrifices Through Prohibition

Current economic analysis of prohibition's costs.

Current State: Fragmented Market, Lost Revenue

Estimated Current Market (2025):

Legal Medical Program:

- 2025 sales projection: $60-75M annually (based on $50.3M through August)

- Tax revenue (6% sales tax): $3.6-4.5M annually

- Jobs: 800-1,200 direct employees

- Federal taxes paid: Minimal (280E burden eliminates most taxable income)

Gray Market "Gifting Economy":

- Estimated sales: $40-60M annually (pre-enforcement surge)

- Declining due to enforcement: 70 shops closed 2024-2025

- Tax revenue: $0 (unregulated, untaxed)

- Quality control: None (untested products)

- Age verification: Minimal (enforcement varies)

- Consumer safety risks: Product contamination, mislabeling, potency inconsistencies

Traditional Illicit Market:

- Estimated sales: $35-55M annually

- Declining as medical/gifting options expand

- Tax revenue: $0

- Enforcement costs: ABCA/MPD resources spent on arrests, prosecutions

- Social costs: Arrests, convictions, incarceration

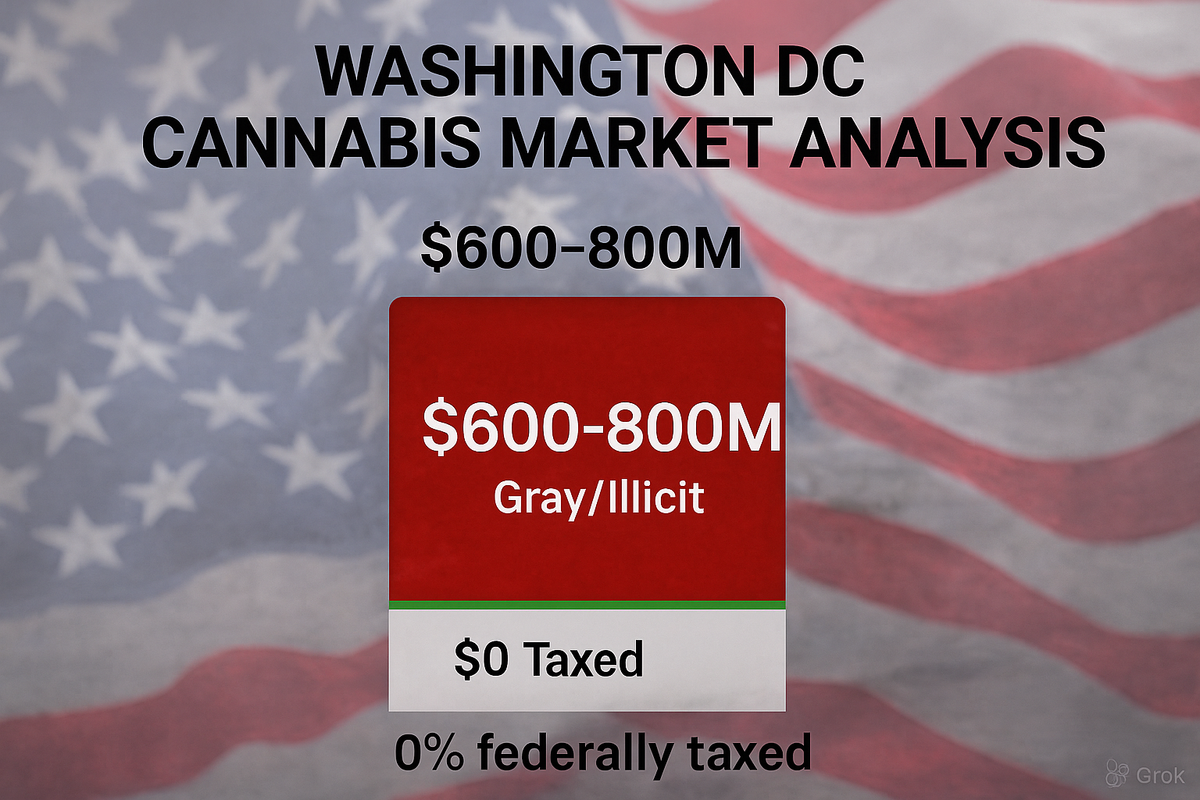

Total Current Market: $135-190M annually (combined medical + gray + illicit)

Revenue Breakdown:

- DC collects: $3.6-4.5M (medical sales tax only)

- Gifting economy: $0 (untaxed)

- Illicit market: $0 (untaxed)

- Total captured: 3-4% of potential revenue

Border State Competition:

DC residents purchasing in Maryland:

- Maryland dispensaries near DC border serve District residents

- Estimated DC resident spending in Maryland: $15-25M annually

- Maryland tax revenue from DC residents: $1.4-2.3M

- DC loses revenue, Maryland gains

Virginia residents visiting DC medical program:

- Self-certified temporary patients from Virginia: 3,767 registered (August 2025)

- Estimated Virginia resident spending in DC: $3-5M annually

- DC captures this revenue (6% sales tax)

- But Virginia will recapture if/when retail launches

What DC Currently Loses:

- Direct tax revenue: $20-30M annually (adult-use sales untaxed or underutilized)

- Federal taxes: $8-12M annually (businesses profitable enough to pay income taxes)

- Jobs not created: 1,000-1,600 (full adult-use market vs. medical-only)

- Tourism revenue: $25-40M annually (visitors can't legally purchase, choose other destinations)

- Economic multiplier: $45-75M annually (downstream spending from cannabis businesses/employees)

Optimized Legal Market Projection

IF DC implemented adult-use regulation with evidence-based policy:

Year 1-2: Launch Phase (2028-2029)

- Dispensaries operational: 60-85 (medical conversion + early adult-use)

- Sales: $95-145M

- Tax revenue: $17-29M

- Jobs: 1,200-1,800

- Legal market share: 50-70% (ramping up)

Year 3-4: Growth Phase (2030-2031)

- Dispensaries operational: 85-105 (expanded adult-use)

- Sales: $145-200M

- Tax revenue: $26-40M

- Jobs: 1,600-2,200

- Legal market share: 75-83% (maturing)

Year 5+: Steady State (2032+)

- Dispensaries operational: 95-110 (optimal density)

- Sales: $180-235M annually

- DC residents: $145-185M

- Tourists: $35-50M

- Tax revenue: $27-42M annually (state)

- Federal taxes: $15-25M annually (income, payroll)

- Jobs: 1,800-2,400 sustained

- Legal market share: 82-88% (optimized)

- Illicit market: Reduced from $90-130M to $15-25M (85-90% reduction)

Economic Multiplier:

For every $10 consumers spend at dispensaries:

- $18 injected into broader economy (MJBizFactbook research)

- Downstream spending: Employee wages → rent, food, services

- Business spending: Cultivation supplies, professional services, real estate, utilities

- Tourism spending: Hotel rooms, restaurants, attractions

Total Economic Impact (Mature Market):

- Direct cannabis sales: $180-235M annually

- Economic multiplier (1.8×): $324-423M total economic activity

- Jobs: 1,800-2,400 direct + 1,200-1,800 indirect = 3,000-4,200 total

- Tax revenue: $27-42M (state) + $15-25M (federal) = $42-67M total

10-Year Comparison: Prohibition vs. Legalization

Prohibition Path (2025-2035):

- Cumulative tax revenue: $36-45M (medical 6% tax only)

- Cumulative economic activity: $1.35-1.9B (medical + gray + illicit, but untaxed/unregulated)

- Jobs created: 800-1,200 (medical only, stagnant)

- Illicit market: $900M-1.3B unregulated activity

- Social costs: Continued gray market, no quality control, arrests continue

- Lost Maryland revenue: $150-250M captured by Maryland from DC residents

Legalization Path (2028 start, optimized by 2033):

- Cumulative tax revenue: $180-300M (2028-2035, state only)

- Federal taxes: $110-190M (2028-2035, income + payroll)

- Cumulative economic activity: $2.2-3.1B (regulated, taxed, safe)

- Jobs: 1,800-2,400 sustained through 2035

- Illicit market: $120-200M over 10 years (85-90% reduction from current)

- Tourism boost: $280-400M cumulative (2028-2035)

The Difference:

DC choosing legalization over prohibition (2028-2035 comparison):

- Gains $144-255M in state tax revenue

- Gains $110-190M in federal tax revenue

- Creates 1,000-1,600 net new jobs

- Reduces illicit market by $780M-1.1B

- Captures $150-250M currently flowing to Maryland

- Adds $900M-1.2B in regulated economic activity

- Eliminates gray market untested products

- Ends arrests for behavior 65% of voters approved

This is what congressional prohibition costs DC. Every year Congress maintains Harris Rider, District residents lose $20-40M in potential tax revenue funding schools, infrastructure, services. Meanwhile, Maryland profits from DC prohibition.

About This Analysis

This prediction is based on the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error and r=0.968 correlation.

Important Note: DC's unique situation (no legal adult-use market due to federal prohibition) prevents standard framework application. This analysis projects DC's potential performance IF federal barriers lift and adult-use regulation implements. Current medical program performance (oversaturated market, $101K average monthly sales per dispensary) reflects distorted policy environment, not underlying market potential.

Resources:

- Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

- Framework methodology: The Black Market Death Equation

- DC Official Data: Alcoholic Beverage and Cannabis Administration

- Related analyses: Georgia, Arizona, Connecticut, Kansas, North Dakota

For DC policymakers, Congressional delegation, or investors seeking detailed analysis:

Comprehensive analysis available under commercial license, including:

- Exact market share predictions under multiple policy scenarios (optimized, moderate, failed)

- Impact analysis of federal rescheduling (Schedule III) on DC market dynamics

- Harris Rider removal timeline probability analysis and market response modeling

- Tax structure optimization: Revenue modeling across 10-40% tax rate spectrum

- Social equity program design: Capital requirements, licensing structures, success metrics

- Tourism market sizing: Visitor purchasing patterns, seasonal variations, hotel policy impacts

- Competitive analysis: Maryland and Virginia policy impacts on DC market capture

- Timeline projections: Federal reform scenarios and DC implementation readiness

- Home cultivation policy analysis (current gray area under Initiative 71)

- Gray market transition strategies: Converting gifting economy to licensed operations

Contact: silentmajority420@proton.me | @The_Silent_420

The Silent Majority 420 is an anonymous cannabis policy analyst with 25 years of market participation. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0 (free use with attribution)