Washington State Cannabis Market Analysis: The Pioneer's Paradox

America's cannabis pioneer now watches Oregon undercut it on price while Idaho's prohibition forces residents to cross state lines—and the nation's highest tax rate ensures the trend continues.

The Silent Majority 420 | November 2025

The Evergreen State's Fading Bloom

Washington made history on November 6, 2012, becoming—alongside Colorado—the first state to legalize adult-use cannabis. On July 8, 2014, the first legal cannabis retail transaction occurred at Bellingham's Top Shelf Cannabis. The pioneering spirit that drove Initiative 502's passage with 56% voter support promised innovation, public health improvements, criminal justice reform, and robust tax revenue.

Eleven years later, Washington's cannabis market tells a cautionary tale about policy stagnation.

Washington State generated $1.23 billion in cannabis sales in 2024, down from the 2021 peak of $1.47 billion. Tax revenue totaled $455 million in 2024, declining from $466 million in 2023. Monthly sales averaged $96.6 million in August 2025, representing an 8% year-over-year decline. The trend is unmistakable: Washington's cannabis market is contracting.

The root cause is equally clear: Washington maintains the highest cannabis excise tax in the continental United States—a flat 37% on all retail sales. This draconian tax burden, combined with federal 280E penalties and banking restrictions, prices legal cannabis out of competitive reach. The result is predictable and measurable market erosion.

Meanwhile, southern neighbor Oregon operates with a 17% tax rate and $12.16 average item prices in September 2025, compared to Washington's $11.82 average. The price similarity masks different realities: Oregon achieves comparable retail prices despite having lower taxes because of massive oversupply, while Washington's high taxes force businesses to operate on razor-thin margins just to compete.

Eastern neighbor Idaho maintains complete prohibition, creating cross-border trafficking that Washington law enforcement must address while receiving zero benefit from cannabis consumed by Idaho residents purchasing in Spokane and the Tri-Cities.

The Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. states with 5% mean absolute error, reveals Washington achieves approximately 60-65% legal market share—middle-of-the-pack performance despite being first to market. The framework predicts that with federal reform (Schedule III + SAFE Banking) and state tax restructuring to 18-22%, Washington could reach 78-85% legal market share within 36-48 months, comparable to Michigan's current 85%.

But continuing current policy ensures further decline. Washington's 37% excise tax was defensible in 2014 when no competing legal markets existed. In 2025, surrounded by Oregon's lower prices and serving Idaho's cross-border consumers, the tax rate represents policy failure. The data is unambiguous: Washington is losing market share to both illicit operators and neighboring states' legal markets.

The pioneer advantage has become the pioneer's burden—and without reform, Washington's cannabis market faces continued erosion.

Framework Validation and Methodology

The CBDT Framework has demonstrated exceptional predictive accuracy:

- Rank-order correlation: r = 0.968 across 24 U.S. states

- Mean absolute error: 5% (out-of-sample validation)

- Oregon prediction: Correctly forecasted ~95% transaction share, 82% volume share

- California prediction: Accurately predicted 50% legal market capture despite early mover advantage

- New York prediction: Validated 30% legal share amid policy crisis

The framework quantifies five policy levers determining legal market capture:

- Price competitiveness (4× weight—most critical variable)

- Access density (store availability, delivery infrastructure)

- Safety and quality advantage (testing standards, consistency)

- Convenience (payment methods, operating hours, friction reduction)

- Enforcement intensity (illicit supply interdiction)

A sixth variable—market fragmentation—acts as a penalty reducing effective access through local retail bans and geographic barriers.

Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

Framework methodology: The Black Market Death Equation: Why Cannabis Will Follow Nevada's Path to Single-Digit Illicit Markets

Current Market Performance (2025): Decline After Peak

Washington's cannabis market has contracted significantly since its 2021 peak, revealing structural problems.

Sales Trajectory: The Decline

Historical Performance:

- 2014 (partial year): $259 million

- 2015: $259 million (first full year)

- 2016: $730 million (integration of medical market)

- 2017: $945 million

- 2018: $1.047 billion (first time exceeding $1B)

- 2019: $1.098 billion

- 2020: $1.429 billion (COVID-era surge)

- 2021: $1.467 billion (peak)

- 2022: $1.277 billion (-13% from peak)

- 2023: $1.226 million (-16% from peak)

- 2024: $1.230 billion (-16% from peak)

2025 Performance (through August): Monthly average $96.6 million represents 8% year-over-year decline. Projected 2025 annual sales: $1.16-1.20 billion, continuing the contraction trajectory.

The peak-to-present decline represents:

- $250-300 million in lost annual sales

- $90-110 million in lost annual tax revenue

- 1,500-2,000 jobs that would exist at 2021 levels

This isn't market maturation—mature markets stabilize or grow modestly. This is market erosion driven by policy failure.

Tax Revenue: Declining Despite High Rates

Washington collected $454.7 million in cannabis excise taxes in 2024, down from $465.4 million in 2023 and $471.4 million in 2022. The irony is stark: Washington maintains the nation's highest excise tax rate yet collects declining revenue because the tax burden shrinks the taxable base.

Tax revenue allocation (per RCW 69.50.535):

- Health care programs (majority allocation)

- Basic Health Plan trust account

- State General Fund

- Substance abuse prevention and treatment

- Local governments and education

The declining revenue constrains funding for programs that cannabis taxes were meant to support—demonstrating how excessive taxation undermines its own purpose.

Market Structure

Licensing (2024 data): 1,698 active cannabis licenses including 816 producer/processor licenses, 476 retailer licenses, 161 producer licenses, 221 processor licenses, 10 cooperative licenses, 2 research licenses, and 12 transportation licenses.

Washington's integrated producer/processor license model differs from states requiring separate licenses. This integration creates efficiency but also concentrates market power—many of Washington's largest producers also process, reducing competition at wholesale level.

Retailer Density: 476 dispensaries for 7.8 million residents = 6.1 stores per 100,000 population

Comparison:

- Oregon: 16.8 per 100k (over-saturated)

- Colorado: 10+ per 100k (mature market)

- Michigan: 8-10 per 100k (growing)

- Washington: 6.1 per 100k (adequate but below optimal)

Medical Endorsements: 284 retailers (60%) hold medical endorsements allowing them to serve registered patients. As of June 2024, medical cannabis patients are exempt from the 37% excise tax, though still subject to sales tax. This medical tax exemption addresses a long-standing inequity but creates compliance complexity for retailers.

Pricing Reality: Forced Competitiveness Through Margin Compression

Washington's average item price: $11.82 (August 2025), among the lowest in the nation despite the highest excise tax rate. This apparent contradiction reveals Washington retailers' desperation: to remain competitive with Oregon prices and illicit markets, they've compressed margins to unsustainable levels.

Price Comparison:

- Washington: $11.82 average

- Oregon: $12.16 average (17% excise tax)

- Colorado: $14.42 average (15% excise tax)

- California: $18.87 average (15% excise + local taxes)

- Illinois: $27.98 average (25-40% total tax)

Washington's prices should be 20-25% higher than Oregon given the tax differential. That they aren't means Washington businesses absorb the difference through reduced margins—a business model that isn't sustainable long-term.

The framework shows legal markets fail when prices exceed illicit alternatives by more than 20%. Washington barely maintains competitiveness, but only by squeezing businesses so tightly that many operate near break-even or at losses after federal 280E taxes.

What Washington Gets Right

Despite policy shortcomings, Washington implemented some foundational elements well.

Rigorous Testing and Quality Standards

Washington requires comprehensive testing for all cannabis products including heavy metals testing (effective April 2019) in addition to potency, pesticides, and microbial contaminants.

Testing panels include:

- Potency (THC, CBD, other cannabinoids)

- Pesticides (comprehensive screening)

- Heavy metals (lead, arsenic, cadmium, mercury)

- Microbial contaminants (E. coli, Salmonella, Aspergillus)

- Residual solvents (for concentrates)

- Moisture content and water activity

Washington's testing standards were industry-leading in 2014 and remain rigorous today. The safety and quality advantage over illicit markets is clear and measurable. Consumers know licensed products undergo comprehensive screening—a significant value proposition.

Seed-to-Sale Tracking: BioTrack THC to Leaf Data Systems

Washington implemented seed-to-sale tracking via BioTrack THC at launch, later transitioning to Leaf Data Systems for improved functionality. Real-time inventory tracking prevents diversion to illicit markets and enables efficient regulatory oversight.

The traceability system works: Washington hasn't experienced large-scale diversion scandals that have plagued some other states. The Washington State Liquor and Cannabis Board (WSLCB) can audit any product's journey from cultivation to retail sale, ensuring compliance and accountability.

Medical Cannabis Integration (Eventually)

Washington's medical cannabis program existed since 1998 but operated without state regulation until 2016. The Cannabis Patient Protection Act (SB 5052, 2015) integrated medical into the I-502 framework, creating:

- Medical cannabis authorization database (replaced cards)

- Medical endorsements for retailers

- Compliant medical products meeting specific standards

- Tax exemptions for registered patients

The integration was contentious—many medical dispensaries closed rather than transition into the regulated system. But the result created a single regulated market where medical patients can access tested, tracked products while maintaining modest tax benefits.

The 2024 medical excise tax exemption addressed a legitimate grievance: patients using cannabis as medicine shouldn't pay the same punitive 37% tax as recreational consumers. This reform came late but demonstrates policy improvement based on stakeholder feedback.

Minimal Geographic Fragmentation

Unlike California (61% of jurisdictions ban cannabis retail), Washington maintains relatively few local bans. State law allows municipalities to zone cannabis businesses but doesn't provide blanket ban authority. Result: Over 600 marijuana dispensaries operate statewide (note: this figure includes all license holders; active retailers number 476).

Most major population centers permit cannabis retail:

- Seattle metro: Excellent coverage

- Spokane metro: Good coverage

- Tacoma/Pierce County: Good coverage

- Tri-Cities: Adequate coverage

- Vancouver/Clark County: Good coverage

Rural areas face greater access challenges, but state law doesn't prohibit delivery—individual municipalities do. The framework counts Washington's fragmentation penalty as moderate rather than severe.

Strong Law Enforcement Cooperation

Washington law enforcement agencies coordinate effectively on illicit cannabis enforcement. The state hasn't adopted California's de facto decriminalization of illegal cultivation. When WSLCB identifies unlicensed operators, local law enforcement responds. This enforcement maintains pressure on illicit supply chains—a critical variable the framework weighs at 0.6×.

States that abandon enforcement (California, New York early-phase) see 15-25 percentage point lower legal market share than states maintaining interdiction efforts.

The 37% Problem: Nation's Highest Tax Creates Structural Disadvantage

Washington's 37% excise tax on all cannabis sales was implemented in 2014 as part of I-502. At the time, with no competing legal markets, the rate didn't face competitive pressure. Voters approved it as part of the legalization package, and revenue projections underwhelmed actual results (a problem policymakers considered fortunate).

In 2025, the 37% rate is indefensible.

Tax Rate Comparison

State excise taxes on adult-use cannabis (selected states):

- Washington: 37% (highest in continental U.S.)

- Alaska: $50 per ounce (cultivation tax)

- Arizona: 16% excise + sales tax

- California: 15% excise + local taxes (25-35% total)

- Colorado: 15% excise + sales tax (19-21% total)

- Illinois: 10-25% (THC-tiered) + local taxes (25-40% total)

- Massachusetts: 10.75% excise + 6.25% sales tax (17% total)

- Michigan: 10% excise + 6% sales tax (16% total)

- Nevada: 10% retail excise + 15% wholesale excise + sales tax (20-22% total)

- Oregon: 17% excise + local option (17-20% total)

Only Illinois rivals Washington's effective tax burden—and Illinois achieves only 55-60% legal market share, among the lowest of mature markets.

Washington's 37% rate is the highest in the nation, while neighboring Oregon taxes recreational cannabis at 17%.

The Oregon Competitive Threat

Oregon and Washington share 300+ miles of border. Portland and Vancouver (Washington) are separated by the Columbia River—literally a bridge connecting the markets. Spokane sits 90 minutes from Idaho (prohibition state) but faces Oregon competition from the south.

Oregon's cannabis pricing (September 2025):

- Average item price: $12.16

- Flower: $7-9 per gram (retail)

- Pre-rolls: $5-7 per unit

- Concentrates: $15-25 per gram

- Edibles: $10-15 per package

Washington's cannabis pricing (August 2025):

- Average item price: $11.82

- Flower: $7-10 per gram (retail)

- Similar concentrate and edible pricing to Oregon

The price similarity is remarkable given Washington's 37% tax versus Oregon's 17%. Oregon achieves low prices through massive oversupply—Oregon produces twice as much cannabis as its residents consume, creating record-low wholesale prices. Washington achieves low prices through margin compression—retailers and producers accepting minimal profits to remain competitive.

For southern Washington residents (Vancouver, Longview, Camas, Kelso), Oregon represents convenient alternative:

- Cross Columbia River

- Pay essentially same prices

- Support Oregon businesses rather than Washington

Economic Loss Estimate: Southern Washington border counties (Clark, Cowlitz, Skamania) represent ~550,000 residents. If 10% regularly purchase in Oregon:

- 55,000 consumers × $800/year average = $44 million annually lost to Oregon

- Washington loses ~$16 million in potential tax revenue

This is conservative—actual leakage likely higher given proximity and price equivalence.

The Idaho Opportunity/Challenge

Eastern neighbor Idaho maintains complete prohibition—no medical program, no decriminalization, possession of any amount remains criminal. For eastern Washington (Spokane metro: 550,000 residents; Tri-Cities metro: 300,000 residents), Idaho's prohibition creates:

Opportunity: Idaho residents cross into Washington for legal cannabis purchases

- Spokane dispensaries benefit from Idaho consumer base

- Tri-Cities dispensaries serve southeastern Idaho market

- Revenue Washington wouldn't otherwise capture

Challenge: Idaho enforcement targets Washington cannabis crossing border

- Idaho law enforcement monitors Washington license plates leaving dispensaries

- Creates tension between states

- Washington receives no tax revenue from Idaho residents' consumption—that revenue goes to Washington dispensaries, but Idaho residents then transport home illegally

The framework shows border state dynamics cut both ways. Washington captures Idaho consumer spending (good) but faces enforcement complications (bad) while receiving zero cooperation from Idaho on shared policy challenges.

If Idaho ever legalizes, Washington's eastern market shrinks immediately. Competitive advantage: temporary and contingent on neighbor's prohibition.

The Margin Compression Crisis

Here's why 37% taxation combined with federal 280E is unsustainable:

Washington Dispensary Example ($1.5M annual revenue):

Normal business (without 280E):

- Revenue: $1,500,000

- COGS: $525,000 (35% of revenue)

- Operating expenses: $700,000

- Operating profit: $275,000

- Federal tax (21%): $57,750

- Net profit: $217,250

Cannabis business (with 280E, Washington's 37% tax):

- Revenue: $1,500,000

- COGS (deductible): $525,000

- Operating expenses (NON-deductible): $700,000

- Taxable income: $975,000 (not $275,000)

- Federal tax: $204,750

- Actual profit after federal tax: $70,250

- Effective federal rate: 74% of operating profit

Then add state obligations:

- Washington B&O tax: ~$20,000

- State corporate income: N/A (Washington has no income tax)

- Other fees and regulatory costs: $15,000

Final net profit: $35,250 (2.35% net margin)

This retailer operates on razor-thin margins—any market disruption (supply shortage, regulatory change, local competition) pushes them into losses. Many Washington cannabis businesses report break-even or negative profitability after federal taxes.

The 37% excise tax forces retail prices higher, but 280E forces them even higher. Washington businesses face:

- Highest state excise tax in nation (37%)

- Effective federal tax rate of 40-70% due to 280E

- Combined burden makes profitability nearly impossible without high prices

- High prices drive consumers to illicit markets

This is the margin compression crisis: Washington businesses can't raise prices (Oregon competition + illicit competition) but can't reduce costs (fixed COGS + non-deductible expenses). Result: business failures and market exit.

Tax Reform Proposals (Repeatedly Failed)

Washington cannabis industry has advocated for tax reduction since 2018:

Proposed reforms:

- Reduce 37% to 25% (modest reduction)

- Reduce 37% to 20% (competitive with most states)

- Convert flat 37% to THC-tiered system (copy Illinois/Connecticut)

- Convert excise tax to cultivation tax (copy Alaska)

- Implement tax holiday for first-time purchasers

Legislative response: None of these proposals have advanced beyond committee hearings.

Political reality: Washington state budget includes cannabis tax revenue projections. Reducing the rate creates short-term revenue reduction (even if long-term revenue increases through volume growth). Legislature views cannabis taxes as reliable revenue stream and resists any reduction.

This is classic short-term thinking: Protect current revenue numbers even as the market erodes. By 2027-2028, if current trends continue, declining sales will reduce tax revenue below what a lower rate would generate through higher volume.

The framework shows this pattern repeatedly: High-tax states protect rates until crisis forces reform (California's current situation) or market collapses entirely (New York's early-phase disaster). Washington is following the same trajectory.

The Federal Policy Barrier

Washington cannot optimize under current federal policy regardless of state-level reforms.

The 280E Problem

Internal Revenue Code Section 280E prevents cannabis businesses from deducting ordinary business expenses, treating them as trafficking operations for tax purposes despite state legality.

Impact on Washington businesses:

- Cannot deduct: rent, utilities, salaries, marketing, insurance, security, professional services, banking fees

- Can only deduct: Cost of Goods Sold (COGS)

This creates effective federal tax rates of 40-70% of gross profit—on top of Washington's 37% excise tax.

Washington businesses face:

- 37% state excise tax (highest in nation)

- 40-70% effective federal tax rate (280E)

- Total effective taxation: 60-85%

No business can sustain 60-85% taxation. Washington cannabis operators respond by:

- Maximizing COGS deductions (aggressive accounting)

- Compressing margins to remain competitive

- Operating at break-even or losses

- Exiting market entirely

The 280E burden forces retail prices 15-20% higher than economically necessary. In competitive markets (Oregon proximity, illicit competition), this price increase is the difference between capturing consumers and losing them.

Solution: Schedule III rescheduling eliminates 280E. Businesses could deduct normal expenses, reducing retail prices 12-18%, dramatically improving competitiveness.

The SAFE Banking Problem

Without SAFE Banking Act passage, Washington cannabis businesses remain largely unbanked:

Current banking situation:

- ~15-20 Washington banks/credit unions serve cannabis businesses

- All operate cautiously due to federal prohibition

- Services provided at 3-5× normal fees

- Constant risk of account closure

- Limited services available (basic checking only)

Mastercard prohibition (August 2023): Mastercard stopped processing cannabis debit transactions, eliminating the most popular cashless payment method. Result: increased cash reliance just as industry was moving toward cashless operations.

Impact on Washington operations:

Security costs:

- Cash-only creates robbery risk

- Armed security required: $50,000-150,000 annually per location

- Armored transport: $600-2,500 per pickup

- Insurance premiums: 30-50% higher than normal retail

Consumer friction:

- Cash-only reduces transaction frequency by 18-25% per Federal Reserve payment systems research

- Younger consumers particularly resistant to cash-only

- Average transaction 15-20% higher when cards accepted

Business operations:

- No access to SBA loans

- No conventional business credit

- Payroll complications

- Accounting costs 2-3× normal businesses

Washington's tech-savvy, cashless consumer base particularly values payment convenience. Seattle metro area leads nation in cashless adoption—forcing cannabis consumers back to cash creates friction competitive disadvantage.

Solution: SAFE Banking Act enables normal banking, card payments, business loans, and reduces security costs. Framework shows this improves consumer convenience score by 0.15-0.20, translating to 5-8 percentage point increase in legal market share.

The Interstate Commerce Prohibition

Washington's border position creates unique federal prohibition challenges:

Oregon competition: Oregon's massive oversupply and record-low wholesale prices stem from inability to export. If interstate commerce were permitted:

- Oregon could export surplus to non-production states

- Wholesale prices would stabilize

- Washington would face less extreme Oregon price competition

Idaho prohibition: Eastern Washington serves Idaho consumers but receives:

- No tax revenue from Idaho residents' actual consumption

- Enforcement complications from Idaho interdiction efforts

- No cooperative policy coordination

Federal legalization or Schedule III plus interstate commerce clarity would:

- Allow Oregon to export surplus, reducing extreme price competition

- Enable Washington to serve Idaho market legally (if Idaho legalizes)

- Reduce border state enforcement tensions

- Create national competitive market rewarding efficiency

Without federal reform, Washington's border position creates problems state policy cannot solve.

Framework Assessment: Washington Underperforms Potential

The CBDT Framework reveals Washington's current performance and optimization ceiling.

Current Performance: 60-65% Legal Market Share

Transaction share: Estimated 65-70% (percentage of consumers choosing legal over illicit for at least some purchases)

Volume share: Estimated 60-65% (accounting for heavy user behavior patterns)

This represents mid-tier performance:

- Better than: California (50%), New York (30%), Illinois (55-60%)

- Similar to: Washington's own metrics

- Worse than: Michigan (85%), Oregon (82%), Colorado (73-78%)

Washington should perform better as first-to-market with mature infrastructure. The 60-65% figure represents underperformance given advantages.

Why Washington Underperforms

Price Competitiveness (4× weight): POOR

Washington legal prices equivalent to Oregon despite 37% vs. 17% tax rates—achieved only through unsustainable margin compression. Illicit market prices:

- Illicit flower: $6-8 per gram

- Illicit concentrates: $15-25 per gram

- Legal prices comparable but only because retailers operate near break-even

The framework shows cannabis consumers are highly price-sensitive. A 10% legal price increase reduces legal market choice probability by 2.3%. Washington's 37% tax should create 25-30% price premium over Oregon—that it doesn't means businesses absorb the difference.

Heavy users (20% of consumers, 80% of volume) are most price-sensitive and most likely to use illicit markets when legal prices lack competitiveness.

Access Density (2.8× combined weight): ADEQUATE

476 dispensaries for 7.8 million residents = 6.1 per 100K

- Urban areas well-served

- Rural areas adequate but could improve

- No statewide delivery mandate (local option)

Optimal Washington density: 550-650 dispensaries (7-8 per 100K). Current level adequate but below optimal. Not Washington's primary problem.

Safety/Quality (1.2× weight): STRONG

Washington excels here:

- Comprehensive testing requirements

- Seed-to-sale tracking (Leaf Data Systems)

- Rigorous compliance standards

- Quality advantage over illicit market clear

This variable can't carry market performance—consumers value safety but won't pay 40% premiums for it.

Convenience (includes payment friction): MODERATE

- Cash-only or limited debit (Mastercard prohibited since 2023)

- No statewide delivery authorization

- Operating hours reasonable (8 AM - midnight typical)

- Online ordering for pickup available

Cash-only reduces transaction frequency 15-20%. Lack of statewide delivery hurts rural access. This is federal problem (SAFE Banking) more than state problem.

Enforcement (0.6× weight): MODERATE-STRONG

Washington maintains active enforcement against illegal cultivation and unlicensed retail. Not Nevada-level interdiction but significantly better than California's abandonment. Enforcement adequate—not Washington's primary problem.

Fragmentation Penalty: LOW-MODERATE

Minimal local bans compared to California. Most population centers permit retail. Delivery prohibition in some jurisdictions creates rural access gaps. Penalty moderate but not severe.

The Framework Verdict

Washington achieves 60-65% legal market share. Framework predicts potential outcomes:

With federal reform (280E elimination + SAFE Banking) and state tax reduction to 18-22%:

- Transaction share: 83-88%

- Volume share: 78-85%

- Timeline: 36-48 months

- Washington would match Michigan's current performance

With federal reform only (no state tax reduction):

- Transaction share: 70-75%

- Volume share: 65-72%

- Improvement but not optimization

With state tax reduction only (no federal reform):

- Transaction share: 68-74%

- Volume share: 63-70%

- Modest improvement constrained by federal barriers

With current policy continued:

- Transaction share: 60-68% (continued slow decline)

- Volume share: 55-63% (erosion continues)

- Market approaches 50% threshold where reform becomes politically urgent

The underperformance: 18-25 percentage points below optimization potential.

This translates to:

- $550-750M annual black market that should be legal

- $200-275M lost tax revenue annually (at reformed rates)

- 3,500-5,000 jobs that don't exist

- Continued market erosion as consumers choose Oregon or illicit alternatives

Policy Recommendations: Path to Optimization

Washington needs both state and federal reform to achieve market optimization.

State-Level Priorities

Priority #1: Reduce Excise Tax to Competitive Levels

Recommendation: Reduce 37% excise tax to 18-22% total effective burden

- Phase 1 (immediate): Reduce to 25% (saves face politically while providing relief)

- Phase 2 (12 months): Reduce to 20% (competitive with most legal states)

- Phase 3 (24 months): Reduce to 18% (undercuts Oregon, maximizes volume)

Rationale: Revenue optimization through volume, not rates. Lower taxes → lower prices → higher legal share → more transactions → higher total revenue despite lower per-unit taxation.

Tax modeling:

- Current: $1.23B sales × 37% = $455M revenue (2024 actual)

- With 20% rate: $1.65B sales × 20% = $330M revenue (initial)

- With 20% rate (36 months): $2.1B sales × 20% = $420M revenue (restored)

- With 18% rate (48 months): $2.4B sales × 18% = $432M revenue (exceeded)

Yes, revenue drops short-term. But 2027-2028 revenue under current policy will be $410-430M anyway due to continued market erosion. Tax reduction accelerates return to revenue growth.

Alternative approach: Convert 37% flat rate to wholesale taxation

- Tax producers/processors at $60-80 per pound

- Eliminates retail taxation complexity

- Reduces consumer sticker shock

- Generates similar revenue through upstream taxation

Alaska model demonstrates wholesale taxation works. Washington's integrated producer/processor licenses make this feasible.

Priority #2: Authorize Statewide Delivery

Recommendation: Mandate delivery availability statewide, override local delivery bans

- Target rural areas lacking retail proximity

- Require retailers to offer delivery OR contract with licensed delivery services

- Maintain all tracking/verification requirements

- Implement delivery permits similar to California model

Rationale: 15-20% of Washington residents lack convenient retail access. Delivery expands access without retail construction costs. Framework shows delivery availability improves access score 0.10-0.15, translating to 3-5 percentage point legal market share increase.

Rural Washington (eastern counties, Olympic Peninsula, Cascade foothills) particularly benefits. Current policy allows local delivery bans—creating fragmentation penalty. State preemption eliminates this barrier.

Priority #3: Stabilize Licensing Environment

Recommendation: Provide regulatory certainty for businesses

Washington hasn't issued new retail licenses since 2014 (except replacing closed licenses). This creates:

- Artificial scarcity maintaining marginal dispensaries

- License values inflated beyond business fundamentals

- Barriers to new entrants with innovative approaches

Options:

- Open limited new license window (50-100 additional retailers)

- Focus new licenses on underserved areas (rural, suburban)

- Implement performance-based licensing (poor performers lose licenses, better operators gain opportunity)

Goal: Maintain quality control while allowing market-driven optimization. Current freeze prevents natural business improvement.

Priority #4: Leverage Enforcement Strategically

Recommendation: Maintain enforcement pressure on illicit operators

Budget: $12-18M annually ($1.50-2.30 per capita) for dedicated cannabis enforcement

- Focus: Large illegal cultivation, unlicensed retail

- Coordinate: Local, state, federal resources

- Avoid: Small personal cultivation, consumer possession

Washington does this adequately already—recommendation is maintain current approach while other states struggle. Enforcement distinguishes Washington from California's abdication.

Federal-Level Advocacy

Priority #1: Pressure Congressional Delegation for SAFE Banking

Washington Senators Patty Murray and Maria Cantwell have supported cannabis reform. Washington House delegation split but majority supportive. State should:

- Governor Jay Inslee public advocacy for SAFE Banking

- Legislative memorial to Congress requesting SAFE Banking passage

- Business coalition (Washington CannaBusiness Association + mainstream business groups) joint advocacy

- Emphasize economic harm: $40-60M annual security costs, payment friction, consumer inconvenience

SAFE Banking has broad bipartisan support. Washington's delegation can help push it across finish line.

Priority #2: Support Schedule III Rescheduling (Minimum)

Schedule III designation eliminates 280E, allowing normal business deductions. This is THE federal reform that changes Washington's competitive position.

Current status: DEA rescheduling process ongoing (2024-2025). Washington should:

- Official state support for Schedule III minimum

- Public comment during DEA process

- Coalition with other legal states (Oregon, Colorado, Michigan)

- Business community testimony on 280E impact

Schedule III doesn't solve everything but solves the biggest problem.

Priority #3: Interstate Commerce Advocacy (Longer-term)

Washington's border position creates unique interstate commerce interests:

- Oregon oversupply affects Washington market

- Idaho prohibition creates enforcement complications

- National market would reward quality/efficiency

Washington should support:

- Federal interstate commerce framework

- Reciprocal recognition of state licenses

- Shared compliance standards

This is 5-10 year timeline but Washington should position itself as national leader advocating for rational interstate rules.

Comparison to Other Markets: Where Washington Fits

Washington's performance falls in middle tier of legal states.

High-Performing Markets (75-85%+ legal share)

Michigan (85%)

- Moderate taxes: 16% total

- Strong enforcement

- Excellent access (growing network)

- Achieves what Washington should

Oregon (82%)

- Low taxes: 17-20% total

- Massive oversupply = rock-bottom prices

- Excellent access (over-saturated)

- Different path but successful outcome

Colorado (73-78%)

- Moderate taxes: 19-21% total

- Mature market (10+ years)

- Strong infrastructure

- Balanced policy approach

Mid-Tier Markets (55-70% legal share)

Washington (60-65%)

- High taxes: 37% + sales tax = 45-47% total

- Adequate access

- Strong quality standards

- Underperforms potential due to tax burden

Nevada (60-65%)

- Moderate taxes: 20-22% total

- Tourism focus

- Strong enforcement

- Desert geography limits access

Illinois (55-60%)

- Very high taxes: 25-40% total

- Adequate access

- Social equity complications

- Tax burden prevents optimization

Low-Performing Markets (30-50% legal share)

California (50%)

- Moderate-high taxes: 25-35% local variation

- Severe fragmentation: 61% local bans

- Minimal enforcement

- Policy disaster despite resources

New York (30%)

- Moderate taxes: 13% + local

- Severe access problems (store shortage)

- Regulatory paralysis

- Worst market in nation

Washington's Position

Washington sits in mid-tier—better than disasters (California, New York, Illinois) but far worse than success stories (Michigan, Oregon, Colorado).

The frustrating reality: Washington has advantages California lacks (minimal fragmentation, strong enforcement) and disadvantages it shouldn't have (highest tax rate despite no structural justification).

If Washington simply copied Michigan's tax structure (16% total), the state would likely achieve 75-80% legal market share. Instead, Washington maintains 37% excise tax—a policy holdover from 2014 that made sense then but is indefensible now.

Timeline and Path Forward

Optimization requires coordinated state and federal reform across 4-5 years.

Phase 1 (2025-2026): State Tax Relief

State Actions:

- Reduce excise tax from 37% to 25% (initial reduction)

- Authorize statewide delivery (override local bans)

- Open limited new license window (50-100 additional retailers in underserved areas)

- Launch federal advocacy campaign (SAFE Banking, Schedule III)

Expected Impact:

- Legal market share: 60-65% → 65-70%

- Sales growth: Stabilize decline, begin modest growth

- Revenue: Short-term reduction offset by volume within 18 months

Phase 2 (2026-2027): Federal Reform

Federal Actions (aspirational timeline):

- SAFE Banking Act passage (enables normal banking)

- DEA Schedule III rescheduling (eliminates 280E)

State Response:

- Further excise tax reduction: 25% → 20%

- Implement delivery infrastructure statewide

- Expand testing/quality programs with saved compliance costs

Expected Impact:

- Legal market share: 65-70% → 72-78%

- Sales growth: 15-25% annually

- Revenue: Returns to 2021 peak levels

Phase 3 (2027-2029): Full Optimization

State Actions:

- Final excise tax reduction: 20% → 18% (if revenue permits)

- Performance-based licensing refinements

- Interstate commerce preparation (if federal framework emerges)

Federal Actions:

- Interstate commerce authorization (possible)

- Full descheduling (longer-term possibility)

Expected Impact:

- Legal market share: 78-85% (optimization achieved)

- Sales: $2.4-2.8B annually (double 2025 levels)

- Revenue: $430-475M annually (exceeds current despite lower rate)

- Jobs: 16,000-22,000 (double current employment)

Failure Scenario: Continued Policy Stagnation

If Washington maintains current policy:

2026-2027:

- Legal market share: 55-60% (continued erosion)

- Sales: $1.05-1.15B annually (15-20% below 2024)

- Revenue: $380-425M annually (declining)

- Business closures accelerate

2028-2030:

- Legal market share: 50-55% (crisis territory)

- Sales: $950M-1.05B annually (approaching medical-era levels)

- Revenue: $350-390M annually (collapse)

- Political pressure for emergency reform

The framework shows markets approaching 50% legal share face crisis dynamics—consumers perceive legal market as failing, businesses exit, illicit operators entrench. Recovery from 50% is harder than preventing decline from 65%.

Washington should act now, during relative strength, rather than waiting for crisis.

Economic Reality: Current State vs. Optimized State

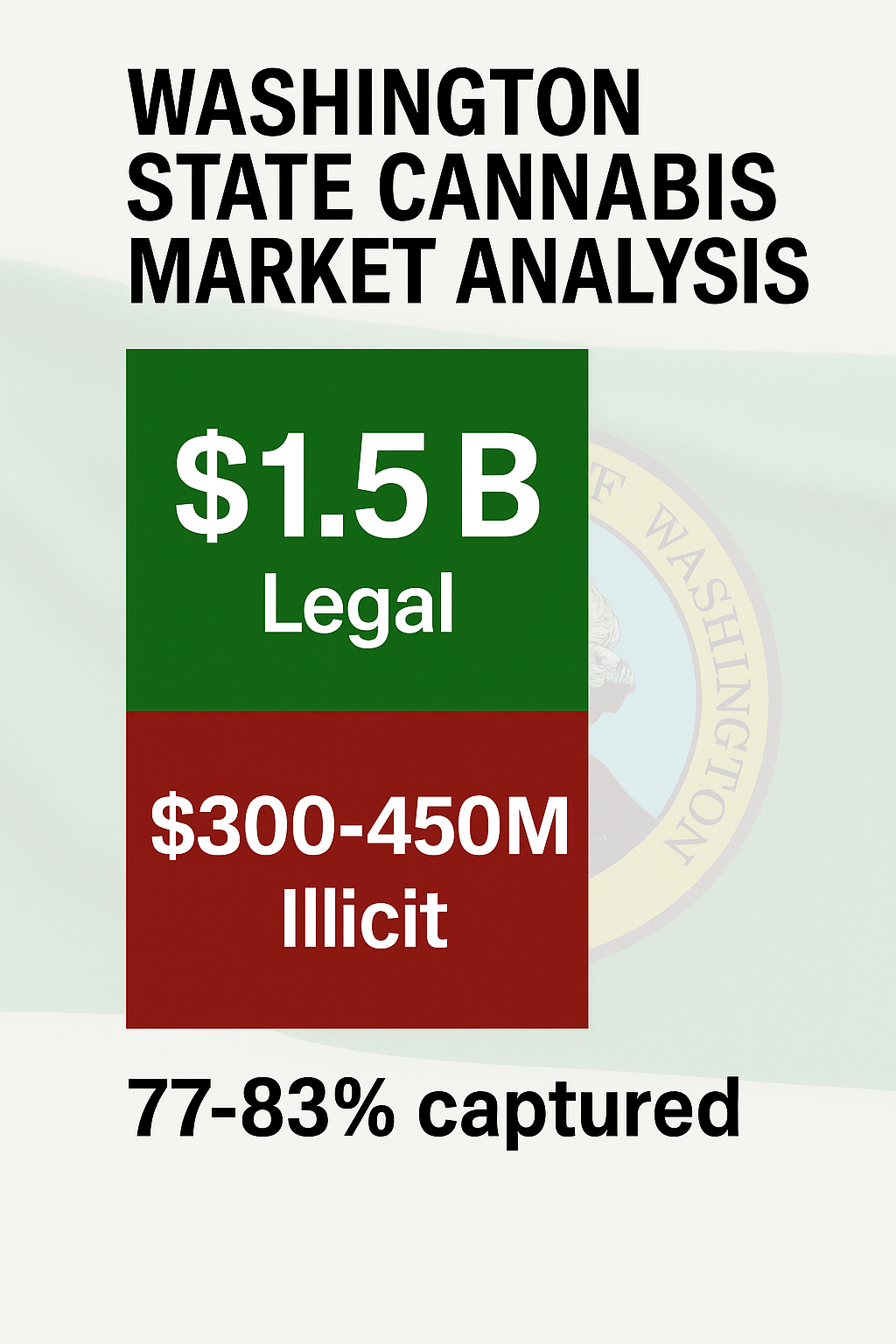

Current State (2025)

Legal market:

- Sales: $1.20B annually

- Tax revenue: $440-460M annually

- Direct employment: 11,000-13,000 jobs

- Average item price: $11.82

Illicit market (estimated):

- Volume: $650-850M annually

- Represents: 35-40% of total demand

- Zero taxes collected

- Unregulated quality/safety

Total Washington cannabis market: $1.85-2.05B annually

Optimized State (Federal Reform + State Tax Reduction)

Legal market:

- Sales: $2.4-2.8B annually (100-130% growth)

- Tax revenue: $430-475M annually (maintained/increased despite lower rate)

- Direct employment: 16,000-22,000 jobs (70-85% growth)

- Average item price: $9.50-11.00 (8-15% reduction)

Illicit market (estimated):

- Volume: $300-450M annually (55-65% reduction)

- Legal capture: 83-88% of total demand

- Functional elimination of large-scale illegal operations

Total Washington cannabis market: $2.7-3.25B annually (realistic demand level)

The Difference

Optimization would create:

- $1.2-1.6B increase in legal sales

- $70-120M additional jobs/economic activity (direct + multiplier effects)

- 5,000-9,000 new cannabis industry jobs

- $200-350M reduction in illicit market volume

- Maintained tax revenue despite lower rates (volume compensates)

The economic case is unambiguous: Washington leaves $1.2-1.6 billion annually on table through policy failure. This isn't theoretical—Michigan demonstrates the achievable outcomes with moderate taxation and federal reform.

Social Impact: Who Benefits from Reform?

Price-Sensitive Consumers

Current policy hurts:

- Working-class consumers

- Price-conscious individuals

- Fixed-income populations

These consumers face choice: Pay 37% premium for legal cannabis or use illicit markets. Many choose illicit—rational economic behavior.

Reformed policy:

- Legal prices drop 15-25%

- Legal cannabis becomes accessible to broader population

- Price no longer primary decision factor

Cannabis Businesses

Current policy creates:

- Unsustainable margins (2-4% net profit typical)

- 280E destroying profitability

- Cash-only increasing costs

- Business failures and market exit

Reformed policy:

- Sustainable margins (8-12% net profit achievable)

- Normal business deductions (no 280E)

- Banking access reducing security/cash costs

- Business stability and growth

Washington State Budget

Current trajectory:

- Declining sales → declining revenue

- 2027-2028: Revenue potentially $380-410M (10-15% below 2024)

- Budget pressure threatens programs funded by cannabis taxes

Reformed trajectory:

- Growing sales → growing/stable revenue

- 2027-2028: Revenue potentially $420-450M (maintained despite rate reduction)

- Budget stability supports health/education programs

Conclusion: The Pioneer Must Innovate Again

Washington made history in 2012 by co-pioneering adult-use legalization with Colorado. The state demonstrated regulated cannabis markets can function effectively, generate substantial revenue, and achieve public health goals better than prohibition.

Eleven years later, Washington risks becoming cautionary tale about policy stagnation.

The data is unambiguous: Washington's 37% excise tax—highest in the nation—combined with federal 280E penalties and SAFE Banking absence, prices legal cannabis into uncompetitive position. The result is measurable market erosion: sales down 16% from 2021 peak, revenue declining, businesses operating on unsustainable margins, and 35-40% of cannabis consumers choosing illicit markets.

The framework predicts Washington could achieve 78-85% legal market share with:

- Federal reform (Schedule III + SAFE Banking)

- State tax reduction (37% → 18-22%)

- Statewide delivery authorization

- Continued strong enforcement and quality standards

This would transform Washington from middle-tier market to national leader—matching or exceeding Michigan's current 85% legal market share.

But continuing current policy ensures further decline. By 2027-2028, without reform, Washington's legal market share will approach 55%—crisis territory where political pressure forces emergency action rather than thoughtful optimization.

Washington's choice: Lead again or fall further behind. The state that pioneered legalization should pioneer optimization. The data shows the path forward. The question is whether policymakers have courage to take it.

The Evergreen State's cannabis market can bloom again—but only if the pioneering spirit that drove legalization also drives reform.

About This Analysis

This prediction is based on the Consumer-Driven Black Market Displacement (CBDT) Framework, validated across 24 U.S. cannabis markets with 5% mean absolute error and r=0.968 correlation.

Resources:

- Validation data: Harvard Dataverse, DOI: 10.7910/DVN/MDVDTQ

- Framework methodology: The Black Market Death Equation

- Related analyses: Hawaii, Florida, Maine, Kansas, Ohio, Virginia, Texas

For Washington State policymakers, MSOs, or investors seeking detailed analysis:

Comprehensive state-specific analysis available under commercial license, including:

- Exact market share predictions under multiple policy scenarios

- County-by-county market analysis and optimization strategies

- Tax revenue modeling with sensitivity testing across rate ranges

- Border state competitive dynamics and Idaho legalization impact scenarios

- Timeline projections for federal reform and state policy responses

- Implementation roadmap for delivery infrastructure and license expansion

- Business survival strategies under current vs. reformed policy environments

Contact: silentmajority420@proton.me | @The_Silent_420

The Silent Majority 420 is an anonymous cannabis policy analyst with 25 years of market participation. The CBDT Framework represents the first validated consumer-utility model for predicting market outcomes in vice legalization.

Analysis licensed CC BY 4.0 (free use with attribution)